CHAPTER 9

Inventories: Additional Valuation Issues

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Lower-of-cost-or-market.

1, 2, 3,

4, 5, 6

1, 2, 3

1, 2, 3,

4, 5, 6

1, 2, 3,

9, 10

1, 2, 3, 5

2.

Inventory accounting

changes; relative sales

value method; net real-

izable value.

7, 8

4

7, 8

Purchase commitments.

9

5, 6

9, 10

9

6

12, 13

14, 15,

16, 17

5.

Retail inventory method.

14, 15, 16

8

18, 19, 20,

22, 23, 26

6, 7, 8,

10, 11

4, 5

LIFO retail.

22, 23

12, 13, 14

Dollar-value LIFO retail.

24, 25,

26, 27

11, 13

Special LIFO problems.

13, 14

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Describe and apply the lower-

of-cost–or-market rule.

1, 2, 3, 4

1, 2, 3

1, 2, 3,

4, 5, 6

1, 2, 3,

9, 10

CA9-1,

CA9-2,

CA9-3,

CA9-5

2. Explain when companies value

inventories at net realizable

value.

5, 6, 7

1, 2, 3

1, 2, 3,

4, 5, 6

1, 2, 3,

9, 10

4. Discuss accounting issues

related to purchase

commitments.

9

5, 6

9, 10

9

CA9-6

5. Determine ending inventory by

applying the gross profit

method.

10, 11, 12,

13

7

11, 12, 13,

14, 15, 16,

17

4, 5

6. Determine ending inventory by

applying the retail inventory

method.

14, 15, 16

8

18, 19, 20

6, 7, 8

CA9-4,

CA9-5

analyze inventory.

17, 18

9

21

9

applying the LIFO retail

methods.

10, 11

22, 23, 24,

25, 26,

11, 12,

13, 14

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E9-1

Lower-of-cost-or-market.

Simple

15–20

E9-2

Lower-of-cost-or-market.

Simple

10–15

E9-3

Lower-of-cost-or-market.

Simple

15–20

E9-4

Lower-of-cost-or-market—journal entries.

Simple

10–15

E9-5

Lower-of-cost-or-market—valuation account.

Moderate

20–25

E9-6

Lower-of-cost-or-market—error effect.

Simple

10–15

E9-7

Relative sales value method.

Simple

15–20

E9-8

Relative sales value method.

Simple

12–17

E9-9

Purchase commitments.

Simple

05–10

E9–10

Purchase commitments.

Simple

15–20

E9–11

Gross profit method.

Simple

8–13

E9–12

Gross profit method.

Simple

10–15

E9–13

Gross profit method.

Simple

15–20

E9–14

Gross profit method.

Moderate

15–20

E9–15

Gross profit method.

Simple

10–15

E9–16

Gross profit method.

Simple

15–20

E9–17

Gross profit method.

Moderate

20–25

E9–18

Retail inventory method.

Moderate

20–25

E9–19

Retail inventory method.

Simple

12–17

E9–20

Retail inventory method.

Simple

20–25

E9–21

Analysis of inventories.

Simple

10–15

*E9-22

Retail inventory method—conventional and LIFO.

Moderate

25–35

*E9-23

Retail inventory method—conventional and LIFO.

Moderate

15–20

*E9-24

Dollar-value LIFO retail.

Simple

10–15

*E9-25

Dollar-value LIFO retail.

Simple

5–10

*E9-26

Conventional retail and dollar-value LIFO retail.

Moderate

20–25

*E9-27

Dollar-value LIFO retail.

Moderate

20–25

*E9-28

Change to LIFO retail.

Simple

10–15

P9-1

Lower-of-cost-or-market.

Simple

10–15

P9-2

Lower-of-cost-or-market.

Moderate

25–30

P9-3

Entries for lower-of-cost-or-market—cost-of-good-

sold and loss.

Moderate

30–35

P9-4

Gross profit method.

Moderate

20–30

P9-5

Gross profit method.

40–45

P9-6

Retail inventory method.

Moderate

20–30

P9-7

Retail inventory method.

Moderate

20–30

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Item

Description

Level of

Difficulty

Time

(minutes)

P9-8

Retail inventory method.

Moderate

20–30

P9-9

Statement and note disclosure, LCM, and purchase

commitment.

Moderate

30–40

P9–10

Lower-of-cost-or-market.

Moderate

30–40

*P9-11

Conventional and dollar-value LIFO retail.

Moderate

30–35

*P9-12

Retail, LIFO retail, and inventory shortage.

Moderate

30–40

*P9-13

Change to LIFO retail.

Moderate

30–40

*P9-14

Change to LIFO retail; dollar-value LIFO retail.

40–50

CA9-1

Lower-of-cost-or-market.

Moderate

15–25

CA9-2

Lower-of-cost-or-market.

Moderate

20–30

CA9-3

Lower-of-cost-or-market.

Moderate

15–20

CA9-4

Retail inventory method.

Moderate

25–30

CA9-5

Cost determination, LCM, retail method.

Moderate

15–25

CA9-6

Purchase commitments.

Moderate

10–15

SOLUTIONS TO CODIFICATION EXERCISES

CE9-1

(a) According to the Master Glossary, Inventory is defined as the aggregate of those items of tangible

personal property that have any of the following characteristics:

1. Held for sale in the ordinary course of business

2. In process of production for such sale

3. To be currently consumed in the production of goods or services to be available for sale.

The term inventory embraces goods awaiting sale (the merchandise of a trading concern and the

finished goods of a manufacturer), goods in the course of production (work in process), and goods

to be consumed directly or indirectly in production (raw materials and supplies). This definition of

(b) According to the Master Glossary, the phrase lower-of-cost-or-market, the term market means

current replacement cost (by purchase or by reproduction, as the case may be) provided that it

meets both of the following conditions.

1. Market shall not exceed the net realizable value

2. Market shall not be less than net realizable value reduced by an allowance for an approxi–

mately normal profit margin.

(c) According to the Master Glossary, two definitions are provided for the phrase net realizable value

1. Estimated selling price in the ordinary course of business less reasonably predictable costs of

Growing Crops

35-1 Costs of growing crops shall be accumulated until the time of harvest. Growing crops shall be

reported at the lower-of-cost-or-market.

> Developing Animals

35-2 Developing animals to be held for sale shall be valued at the lower-of-cost-or-market.

CE9-1 (Continued)

> Animals Available and Held for Sale

35-3 Animals held for sale shall be valued at either of the following:

(a) The lower-of-cost-or-market

(b) At sales price less estimated costs of disposal, if all the following conditions exist:

> Harvested Crops

35-4 Inventories of harvested crops shall be valued using the same criteria as animals held for sale in

the preceding paragraph.

CE9-2

According to FASB ASC 330-10–35-1 through 5: Adjustments to Lower-of-Cost-or-Market

A departure from the cost basis of pricing the inventory is required when the utility of the goods is no

longer as great as their cost. Where there is evidence that the utility of goods, in their disposal in the

ordinary course of business, will be less than cost, whether due to physical deterioration, obsolescence,

changes in price levels, or other causes, the difference shall be recognized as a loss of the current

Replacement or reproduction prices would not be appropriate as a measure of utility when the esti–

mated sales value, reduced by the costs of completion and disposal, is lower, in which case the realizable

value so determined more appropriately measures utility.

In addition, when the evidence indicates that cost will be recovered with an approximately normal profit

upon sale in the ordinary course of business, no loss shall be recognized even though replacement or

CE9-3

According to FASB ASC 330-10–35-6, if inventory has been the hedged item in a fair value hedge, the

the carrying amount of the hedged item and be recognized currently in earnings.

CE9-4

See FASB ASC 210-10-S99—Regulation S-X Rule 5-02, Balance Sheets

S99-1 The following is the text of Regulation S-X Rule 5-02, Balance Sheets.

The purpose of this rule is to indicate the various line items and certain additional disclosures

which, if applicable, and except as otherwise permitted by the Commission, should appear on

– (a) State separately in the balance sheet or in a note thereto, if practicable, the amounts of

major classes of inventory such as:

• 1. Finished goods;

– (b) The basis of determining the amounts shall be stated.

If cost is used to determine any portion of the inventory amounts, the description of this method

shall include the nature of the cost elements included in inventory. Elements of cost include,

among other items, retained costs representing the excess of manufacturing or production costs

CE9-4 (Continued)

– If any general and administrative costs are charged to inventory, state in a note to the

financial statements the aggregate amount of the general and administrative costs incurred in

each period and the actual or estimated amount remaining in inventory at the date of each

balance sheet.

– (c) If the LIFO inventory method is used, the excess of replacement or current cost over

– (d) For purposes of §§ 210.5–02.3 and 210.5–02.6, long-term contracts or programs include

• 1. all contracts or programs for which gross profits are recognized on a percentage-

of-completion method of accounting or any variant thereof (e.g., delivered unit,

be included, if deemed appropriate.

– For all long-term contracts or programs, the following information, if applicable, shall be stated

in a note to the financial statements:

(i) The aggregate amount of manufacturing or production costs and any related deferred

costs (e.g., initial tooling costs) which exceeds the aggregate estimated cost of all in–

process and delivered units on the basis of the estimated average cost of all units

ANSWERS TO QUESTIONS

1. Where there is evidence that the utility of goods to be disposed of in the ordinary course of

business will be less than cost, the difference should be recognized as a loss in the current period,

and the inventory should be stated at market value in the financial statements.

2. The upper (ceiling) and lower (floor) limits for the value of the inventory are intended to prevent the

inventory from being reported at an amount in excess of the net realizable value or at an amount

3. The usual basis for carrying forward the inventory to the next period is cost. Departure from cost is

required when the utility of the goods included in the inventory is less than their cost. This loss in

utility should be recognized as a loss of the current period, the period in which it occurred.

Furthermore, the subsequent period should be charged for goods at an amount that measures

their expected contribution to that period. In other words, the subsequent period should be

The arguments against the use of the lower-of-cost-or-market method of valuing inventories

include the following:

(a) The method requires the reporting of estimated losses (all or a portion of the excess of actual

cost over replacement cost) as definite income charges even though the losses have not been

sustained to date and may never be sustained. Under a consistent criterion of realization a

drop in replacement cost below original cost is no more a sustained loss than a rise above

cost is a realized gain.

(b) A price shrinkage is brought into the income statement before the loss has been sustained

reductions in sales prices do not materialize.

Questions Chapter 9 (Continued)

(f) In the application of the lower–of-cost-or–market rule a prospective “normal profit” is used in

determining inventory values in certain cases. Since “normal profit” is an estimated figure

based upon past experiences (and might not be attained in the future), it is not objective in

nature and presents an opportunity for manipulation of the results of operations.

4. The lower-of-cost-or-market rule may be applied directly to each item or to the total of the

inventory (or in some cases, to the total of the components of each major category). The method

5. (1) $14.50.

6. One approach is to record the inventory at cost and then reduce it to market, thereby reflecting a

loss in the current period (often referred to as the loss method). The loss would then be shown as

a separate item in the income statement and the cost of goods sold for the year would not be

distorted by its inclusion. An objection to this method of valuation is that an inconsistency is

7. An exception to the normal recognition rule occurs where (1) there is a controlled market with a

quoted price applicable to specific commodities and (2) no significant costs of disposal are

involved. Certain agricultural products and precious metals which are immediately marketable at

quoted prices are often valued at net realizable value (market price).

8. Relative sales value is an appropriate basis for pricing inventory when a group of varying units is

purchased at a single lump-sum price (basket purchase). The purchase price must be allocated in

9. The drop in the market price of the commitment should be charged to operations in the current year

if it is material in amount. The following entry would be made [($6.20 – $5.90) X 150,000] = $45,000:

Unrealized Holding Gain or Loss—Income (Purchase Commitments) …….

45,000

Estimated Liability on Purchase Commitments ………………………….

Questions Chapter 9 (Continued)

10. The major uses of the gross profit method are: (1) it provides an approximation of the ending

inventory which the auditor might use for testing validity of physical inventory count; (2) it means

that a physical count need not be taken every month or quarter; and (3) it helps in determining

damages caused by casualty when inventory cannot be counted.

11. Gross profit as a percentage of sales indicates that the markup is based on selling price rather

than cost; for this reason the gross profit as a percentage of selling price will always be lower than

12. A markup of 25% on cost equals a 20% markup on selling price; therefore, gross profit equals

$1,000,000 ($5 million X 20%) and net income equals $250,000 [$1,000,000 – (15% X $5 million)].

13.

Inventory, January 1, 2014 …………………………………………………………..

$ 400,000

Purchases to February 10, 2014 ……………………………………………………

$1,140,000

Freight-in to February 10, 2014 ……………………………………………………..

60,000

Merchandise available ………………………………………………………….

Sales revenue to February 10, 2014 ………………………………………………

Less gross profit at 40% ………………………………………………………..

780,000

Sales at cost ……………………………………………………………………

14. The validity of the retail inventory method is dependent upon (1) the composition of the inventory

remaining approximately the same at the end of the period as it was during the period, and

(2) there being approximately the same rate of markup at the end of the year as was used

throughout the period.

The retail method, though ordinarily applied on a departmental basis, may be appropriate for the

business as a unit if the above conditions are met.

15. The conventional retail method is a statistical procedure based on averages whereby inventory

figures at retail are reduced to an inventory valuation figure by multiplying the retail figures by a

percentage which is the complement of the markup percent.

Questions Chapter 9 (Continued)

Computation of Inventory

Cost

Retail

Ratio

Purchases

$100

$150

66 2/3%

Inventory at retail

Inventory at lower-of-cost-or-market $23 X 66 2/3% = $15.33

16. (a) Ending inventory:

Cost

Retail

Beginning inventory ………………………………………………….

$ 149,000

$ 283,500

Purchases ……………………………………………………………….

1,400,000

2,160,000

Freight-in ………………………………………………………………..

70,000

Add net markups ………………………………………………………

92,000

Deduct net markdowns ……………………………………………..

48,000

2,487,500

Deduct sales revenue …………………………..…………………..

2,175,000

(b) The retail method, above, showed an ending inventory at retail of $312,500; therefore, mer-

chandise not accounted for amounts to $17,500 ($312,500 – $295,000) at retail and $11,200

($17,500 X .64) at cost.

17. Information relative to the composition of the inventory (i.e., raw material, work–in-process, and

finished goods); the inventory financing where significant or unusual (transactions with related

18. Inventory turnover measures how quickly inventory is sold. Generally, the higher the inventory

turnover, the better the enterprise is performing. The more times the inventory turns over, the

19. Two major modifications are necessary. First, the beginning inventory should be excluded from the

numerator and denominator of the cost-to-retail percentage and second, markdowns should be

included in the denominator of the cost–to-retail percentage.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 9-1

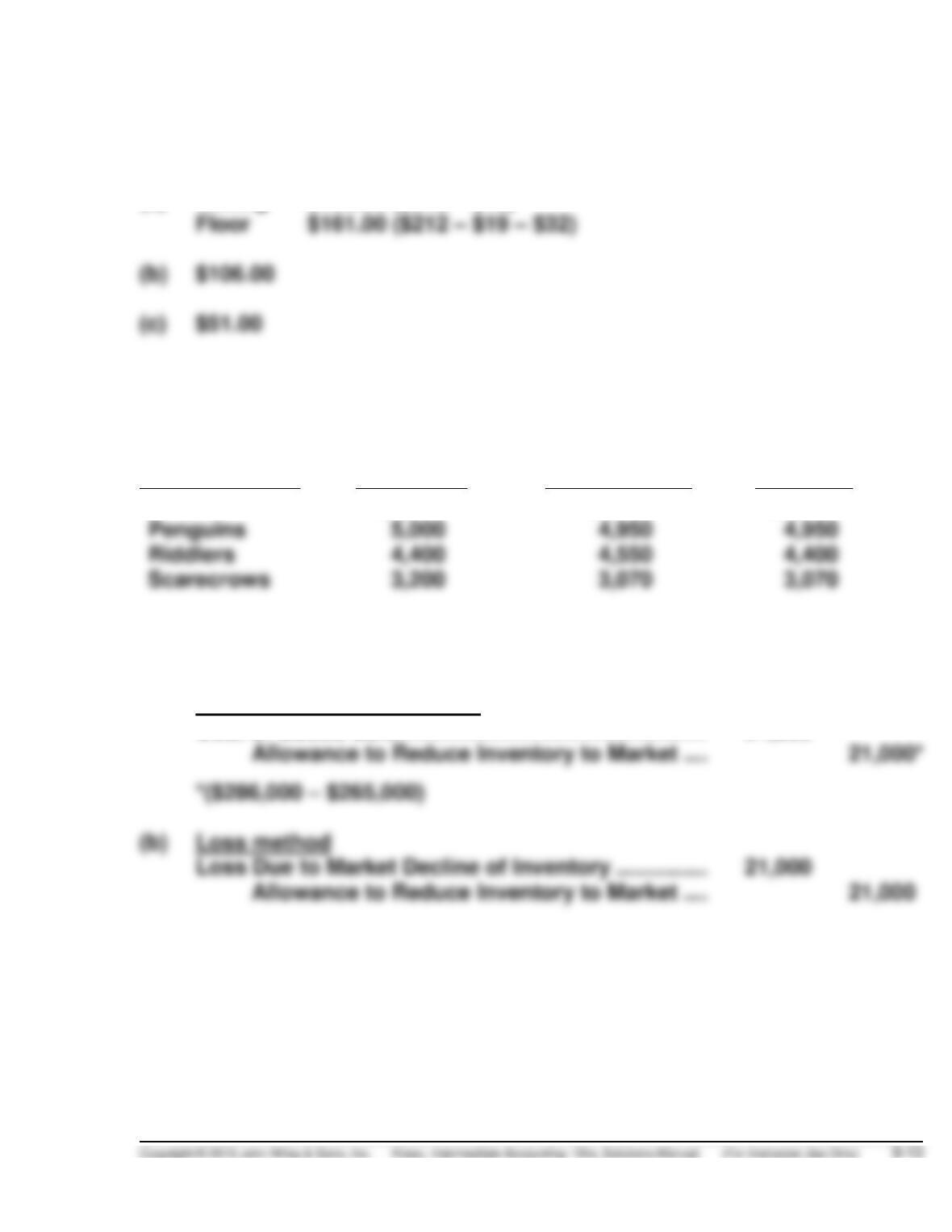

(a) Ceiling $193.00 ($212 – $19)

BRIEF EXERCISE 9-2

Item

Cost

Designated

Market

LCM

Jokers

$2,000

$2,050

$2,000

Penguins

Riddlers

Scarecrows

BRIEF EXERCISE 9-3

(a)

Cost-of–goods-sold method

Cost of Goods Sold …………………………………………………

21,000

Allowance to Reduce Inventory to Market ………..

(b)

Loss method

Loss Due to Market Decline of Inventory ………………….

21,000

Allowance to Reduce Inventory to Market ………..

BRIEF EXERCISE 9-4

Group

Number

of CDs

Sales

Price

per CD

Total

Sales

Price

Relative

Sales

Price

Total

Cost

Cost

Allocated

to CDs

Cost

per CD

1

100

$ 5

$ 500

5/100*

X

$8,000

=

$ 400

$ 4**

BRIEF EXERCISE 9-5

Estimated Liability on Purchase

Unrealized Holding Loss—Income (Purchase

BRIEF EXERCISE 9-6

Purchases (Inventory) ……………………………………………..

950,000

Estimated Liability on Purchase Commitments …………

50,000

Cash ………………………………………………………………

1,000,000

BRIEF EXERCISE 9-7

Beginning inventory ……………………………………………

$150,000

Purchases ………………………………………………………….

500,000

Cost of goods available ………………………………………

Sales revenue …………………………………………………….

Less gross profit (35% X 700,000) ………………………..

Estimated cost of goods sold ………………………………

Estimated ending inventory destroyed in fire ……….

BRIEF EXERCISE 9-8

Cost

Retail

Beginning inventory ………………………………………

$ 12,000

$ 20,000

Net purchases ………………………………………………

120,000

170,000

Net markups …………………………………………………

10,000

Totals …………………………………………………………..

$132,000

Deduct:

Net markdowns …………………………………………….

Sales revenue ……………………………………………….

Ending inventory at retail ………………………………

BRIEF EXERCISE 9-9

Inventory turnover:

Average days to sell inventory:

*BRIEF EXERCISE 9-10

Cost

Retail

Beginning inventory ……………………………………….

$ 12,000

$ 20,000

Net purchases ………………………………………………..

120,000

170,000

Net markups …………………………………………………..

10,000

Net markdowns ………………………………………………

Total (excluding beginning inventory) ……………..

Total (including beginning inventory) ………………

Deduct: Sales revenue …………………………………..

Ending inventory at retail ………………………………..

Ending inventory at cost

*BRIEF EXERCISE 9-11

Cost

Retail

Beginning inventory ……………………………………….

$ 12,000

$ 20,000

Net purchases ………………………………………………..

120,000

170,000

Net markups …………………………………………………..

10,000

Net markdowns ………………………………………………

(7,000)

Total (excluding beginning inventory) ……………..

Total (including beginning inventory) ………………

Deduct: Sales revenue …………………………………..

Ending inventory at retail ………………………………..

*BRIEF EXERCISE 9-11 (Continued)

Cost-to-retail ratio: $120,000 ÷ $173,000 = 69.4%

Ending inventory at retail deflated to base year prices

SOLUTIONS TO EXERCISES

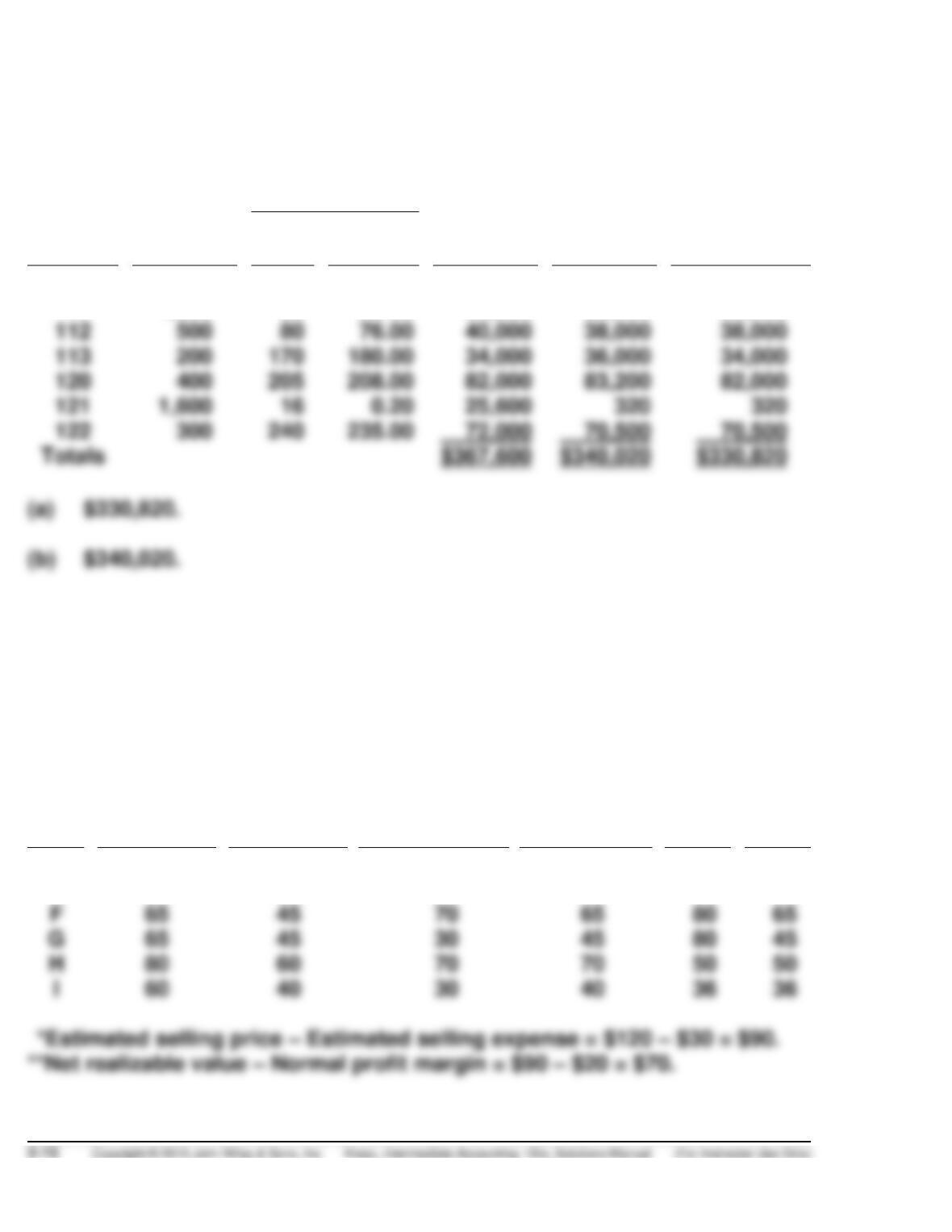

EXERCISE 9-1 (15–20 minutes)

Per Unit

Lower-of–

Part No.

Quantity

Cost

Market

Total

Cost

Total

Market

Cost-or–

Market

110

600

$ 90

$100.00

$ 54,000

$ 60,000

$ 54,000

111

1,000

60

52.00

60,000

52,000

52,000

112

500

80

76.00

40,000

38,000

38,000

113

200

34,000

36,000

34,000

121

1,600

16

0.20

25,600

320

320

122

300

72,000

70,500

70,500

EXERCISE 9-2 (10–15 minutes)

Item

Net

Realizable

Value

(Ceiling)

Net

Realizable

Value

Less

Normal

Profit

(Floor)

Replacement

Cost

Designated

Market

Cost

LCM

D

$90*

$70**

$120

$90

$75

$75

E

80

60

72

72

80

72

H

80

60

70

70

50

50

I

EXERCISE 9-3 (15–20 minutes)

Item

No.

Cost

per

Unit

Replacement

Cost

Net

Realizable

Value

Net Real.

Value

Less

Normal

Profit

Designated

Market

Value

Quantity

Final

Inventory

Value

1320

$3.20

$3.00

$4.15*

$2.90**

$3.00

1,200

$ 3,600

1333

2.70

2.30

3.00

2.50

2.50

900

2,250

1426

4.50

3.70

4.60

3.60

3.70

800

2,960

1437

3.60

3.10

2.95

2.05

2.95

1,000

2,950

1510

2.25

2.00

2.45

1.85

2.00

700

1,400

1522

3.00

2.70

3.40

2.90

2.90

500

1,450

1573

1.80

1.60

1.75

1.25

1.60

3,000

4,800

1626

4.70

5.20

5.50

4.50

5.20

1,000

4,700***

EXERCISE 9-4 (10–15 minutes)

(a)

12/31/13

Cost of Goods Sold…………………………..

19,000

Inventory……………………………………………………….

19,000

12/31/13

Cost of Goods Sold…………………………..

15,000

Inventory……………………………………………………….

15,000

EXERCISE 9-4 (Continued)

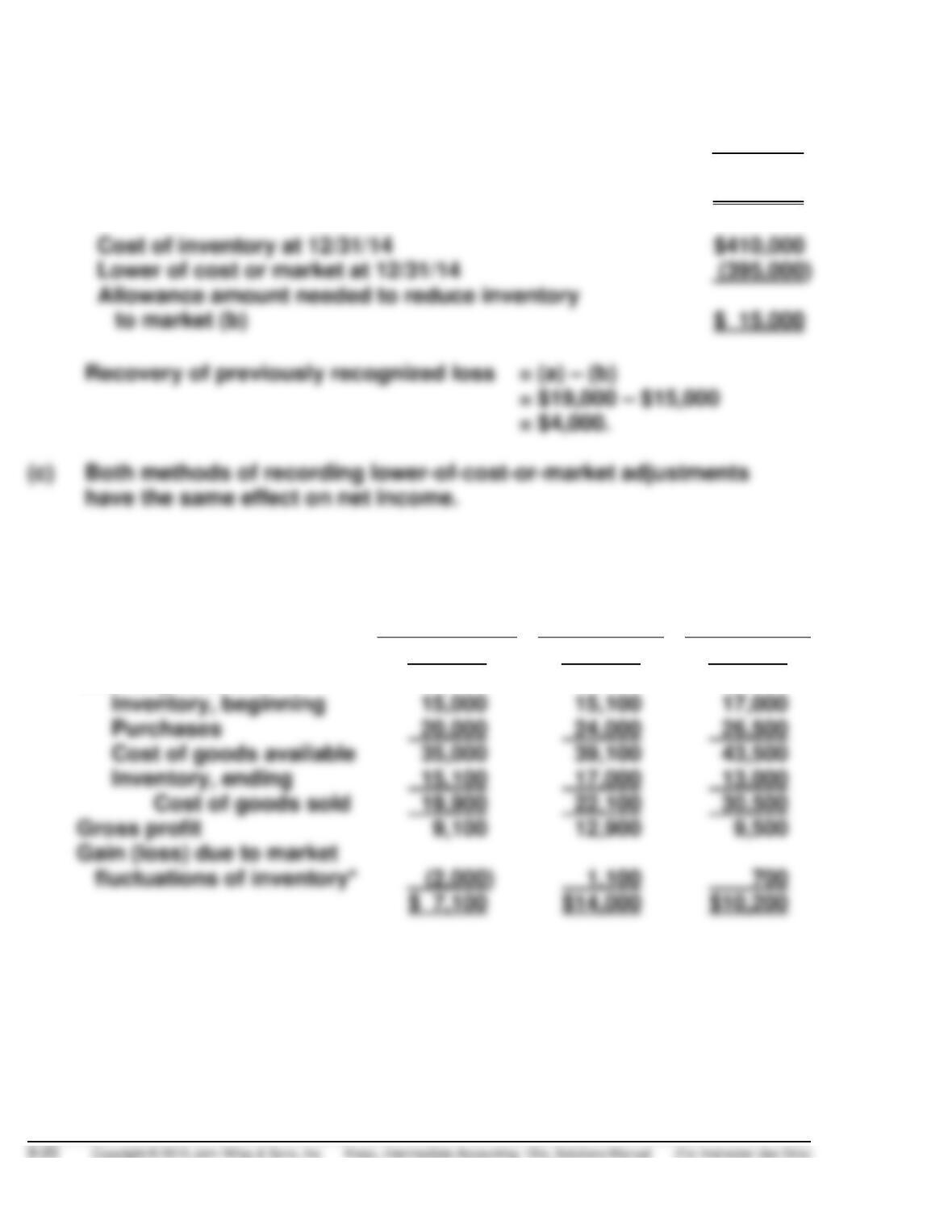

*Cost of inventory at 12/31/13

$346,000

Lower of cost or market at 12/31/13

(327,000)

Allowance amount needed to reduce inventory

to market (a)

$ 19,000

Cost of inventory at 12/31/14

Lower of cost or market at 12/31/14

Allowance amount needed to reduce inventory

to market (b)

$ 15,000

Recovery of previously recognized loss

= (a) – (b)

= $19,000 – $15,000

= $4,000.

EXERCISE 9-5 (20–25 minutes)

(a)

February

March

April

Sales revenue

$29,000

$35,000

$40,000

Cost of goods sold

Inventory, beginning

Purchases

Cost of goods available

Inventory, ending

Cost of goods sold

Gross profit

Gain (loss) due to market

fluctuations of inventory*