PROBLEM 21-12 (Continued)

Partial Amortization Schedule

(Annuity-Due Basis)

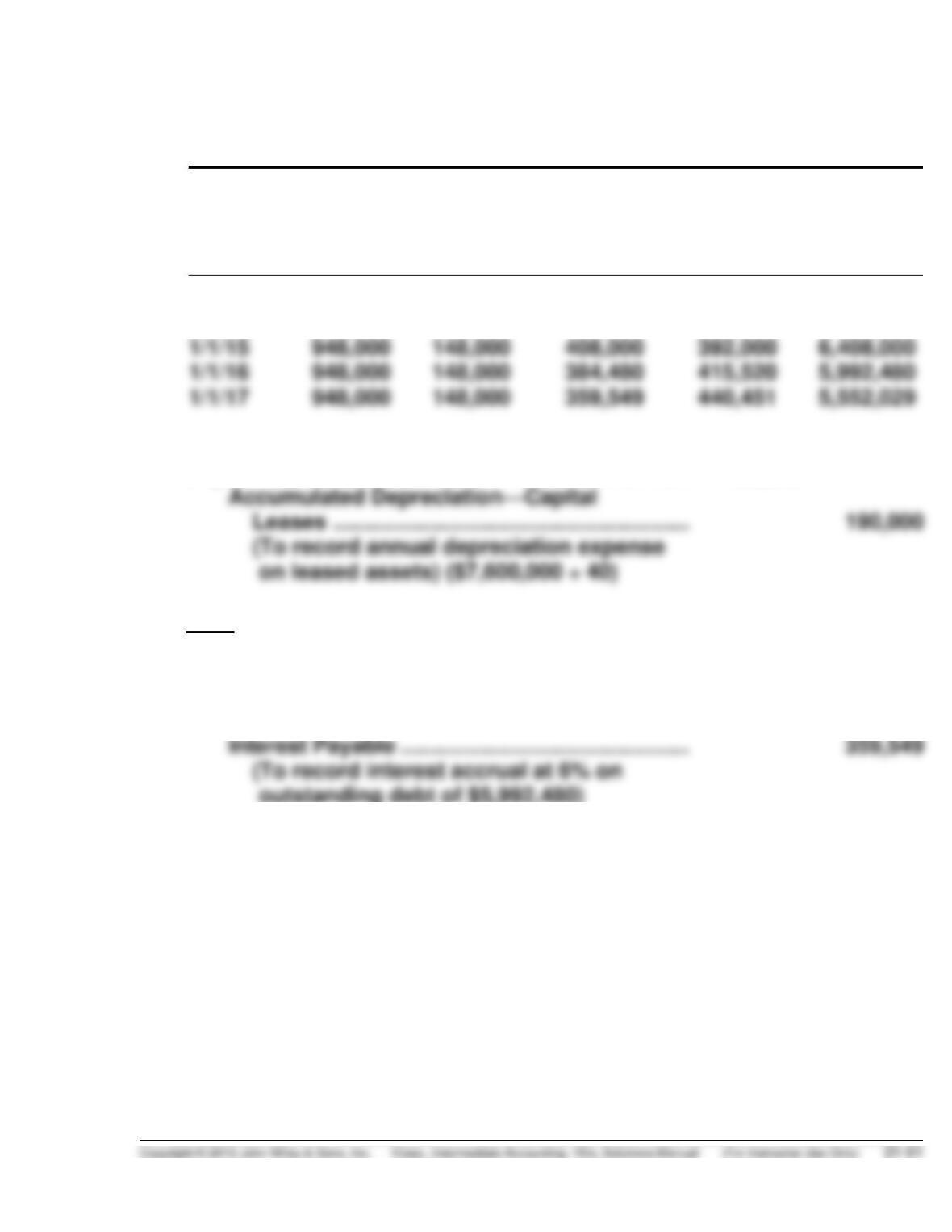

Date

Lease

Payment

Executory

Costs

Interest

(6%) on

Lease

Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/14

$ 0

$ 0

$ 0

$ 0

$7,600,000

1/1/14

948,000

148,000

0

800,000

6,800,000

1/1/15

948,000

148,000

408,000

392,000

6,408,000

1/1/17

948,000

148,000

359,549

440,451

5,552,029

(2) (12/31/16)

Depreciation Expense …………………………………….. 190,000

Note: The leased asset is depreciated over its economic life because a

bargain-purchase option is available at the end of the lease term.

(3) (12/31/16)

Interest Expense …………………………………………….. 359,549

PROBLEM 21-13

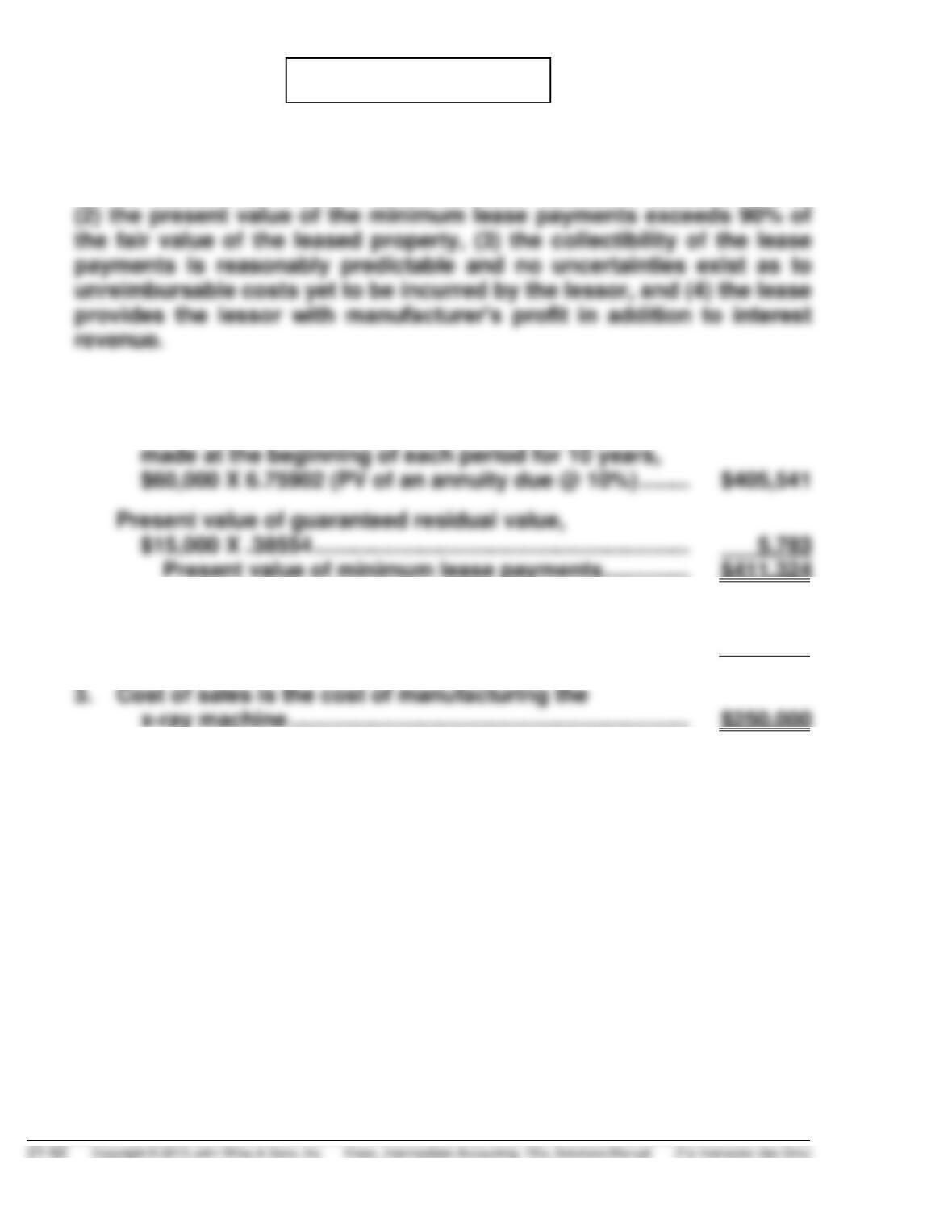

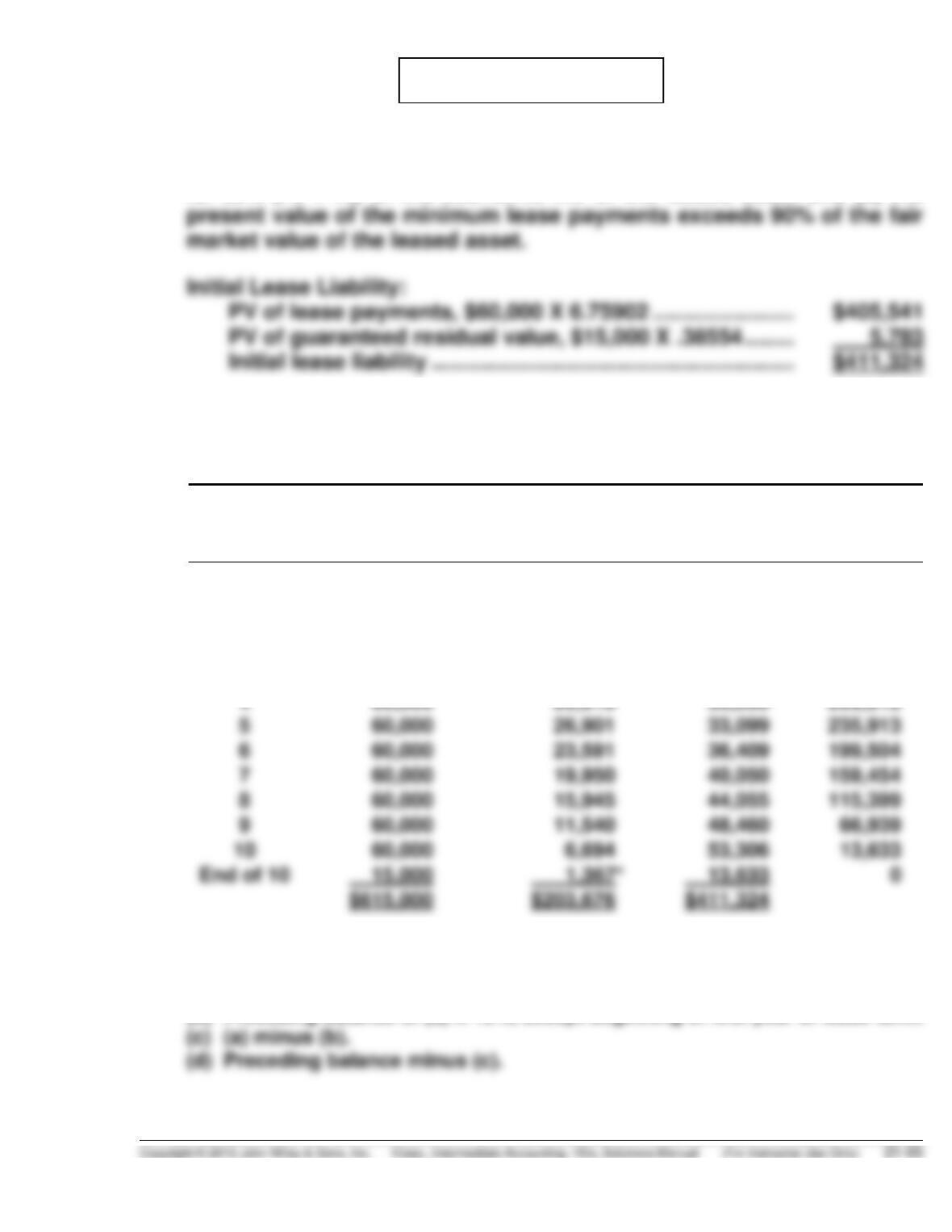

(a) The noncancelable lease is a sales-type capital lease because: (1) the

lease term is for 83% (10 ÷ 12) of the economic life of the leased asset,

1. Lease Receivable:

Present value of annual payments of $60,000

2. Sales price is the same as the present value of

minimum lease payments ………………………………………. $411,324

PROBLEM 21-13 (Continued)

(b) AMIRANTE INC. (Lessor)

Lease Amortization Schedule

(Annuity due basis, guaranteed residual value)

Beginning

of Year

Annual Lease

Payment Plus

Residual Value

Interest (10%)

on Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

(a)

(b)

(c)

(d)

Initial PV

—

—

—

$411,324

1

$ 60,000

—

$ 60,000

351,324

2

60,000

$ 35,132

24,868

326,456

3

60,000

32,646

27,354

299,102

4

269,012

5

60,000

33,099

235,913

6

199,504

7

159,454

8

60,000

44,055

115,399

9

$615,000

$411,324

*Rounding error is $4.00.

(a) Annual lease payment required by lease contract.

(b) Preceding balance of (d) X 10%, except beginning of first year of lease term.

(c) Lessor’s journal entries:

Beginning of the Year

Lease Receivable ……………………………………………. 411,324

PROBLEM 21-13 (Continued)

Cash ………………………………………………………………… 60,000

Lease Receivable ……………………………………….. 60,000

PROBLEM 21-14

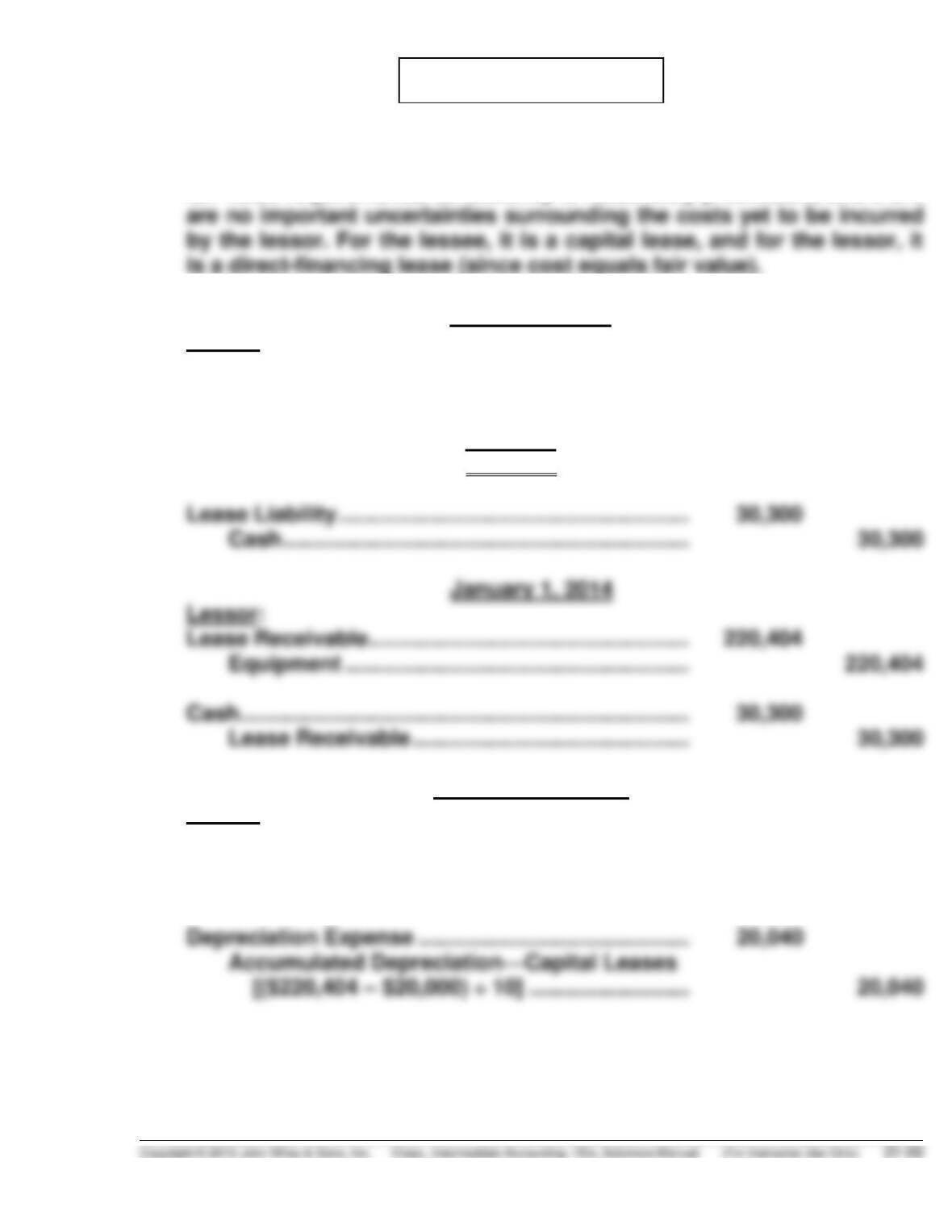

(a) The noncancelable lease is a capital lease because: (1) the lease term is

for 83% (10 ÷ 12) of the economic life of the leased asset and (2) the

(b) CHAMBERS MEDICAL (Lessee)

Lease Amortization Schedule

(Annuity-Due Basis, GRV)

Beginning

of Year

Annual Lease

Payment Plus

GRV

Interest (10%)

on Unpaid

Liability

Reduction

of Lease

Liability

Lease

Liability

(a)

(b)

(c)

(d)

Initial PV

$ 0

$ 0

$ 0

$411,324

1

60,000

0

60,000

351,324

2

60,000

35,132

24,868

326,456

3

60,000

32,646

27,354

299,102

4

30,090

269,012

5

33,099

235,913

6

60,000

23,591

36,409

199,504

7

40,050

159,454

8

44,055

115,399

9

60,000

11,540

48,460

53,306

*Rounding error is $4.

(a) Annual lease payment required by lease contract.

(b) Preceding balance of (d) X 10%, except beginning of first year of lease term.

PROBLEM 21-14 (Continued)

(c) Lessee’s journal entries:

Beginning of the Year

Leased Equipment …………………………………………. 411,324

Lease Liability …………………………………………. 411,324

End of the Year

Interest Expense ……………………………………………. 35,132

Interest Payable ………………………………………. 35,132

(To record accrual of annual interest on

lease obligation)

PROBLEM 21-15

Memorandum Prepared by: (Your Initials)

Date:

HOCKNEY, INC.

December 31, 2014

Reclassification of Leased Auto

As a Capital Lease

While performing a routine inspection of the client’s garage, I found a used

automobile which was not listed among the company’s assets in the

equipment subsidiary ledger. I asked Stacy Reeder, plant manager, about

I advised the client to capitalize this lease at the present value of its minimum

lease payments: $10,731 (the present value of the monthly payments), plus

$809 (the present value of the guaranteed residual). The following journal

entry was suggested:

PROBLEM 21-15 (Continued)

Finally, this vehicle must be depreciated over its lease term. Using straight–

PROBLEM 21-16

(a) The lease agreement satisfies both the 75% of useful life and 90% of

fair value requirements, collectibility is reasonably predictable, and there

(b) January 1, 2014

Lessee:

Leased Equipment ………………………………………….. 220,404

Lease Liability ………………………………………….. 220,404

($30,300 X 6.99525 = $211,956)

($20,000 X .42241 = 8,448)

= $220,404)

December 31, 2014

Lessee:

Interest Expense …………………………………………….. 17,109

Interest Payable

[($220,404 – $30,300) X .09] ……………………. 17,109

PROBLEM 21-16 (Continued)

December 31, 2014

Lessor:

Interest Receivable …………………………………………… 17,109

Interest Revenue ………………………………………… 17,109

(c) (1) and (2) are both $211,956, as the lessee has no obligation to pay the

residual value.

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 21-1 (Time 15–25 minutes)

Purpose—to provide the student with an understanding of the theoretical reasons for requiring certain

CA 21-2 (Time 25–35 minutes)

Purpose—to provide an understanding of the factors underlying the accounting for a leasing arrangement

from the point of view of both the lessee and lessor. The student is required to determine the classifica–

tion of this leasing arrangement, the appropriate accounting treatment which should be accorded this

lease, and the financial statement disclosure requirements for both the lessee and lessor.

CA 21-3 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of the classification of three leases. The student

CA 21-4 (Time 15–25 minutes)

CA 21-5 (Time 30–35 minutes)

Purpose—to provide the student with a lease situation containing a bargain-purchase option and both

CA 21-6 (Time 20–25 minutes)

Purpose—to provide the student with a lease arrangement with a bargain-purchase option in order to

examine the ethical issues of lease accounting.

*CA 21-7 (Time 15–25 minutes)

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 21-1

(b) Evans should account for this lease at its inception as an asset and an obligation at an amount

should be the machine’s fair value.

(c) Evans will incur interest expense equal to the interest rate used to capitalize the lease at its

inception multiplied by the appropriate net carrying value of the liability at the beginning of the

period.

(d) The asset recorded under the capital lease and the accumulated depreciation should be classified

on Evans’ December 31, 2014, balance sheet as noncurrent and should be separately identified

CA 21-2

(2) Since the given facts state that Sylvan (lessee) does not have access to information that

would enable determination of Breton Leasing Corporation’s (lessor) implicit rate for this

(3) The amount recorded as an asset on Sylvan’s books should be shown in the fixed assets

section of the balance sheet as “Leased Equipment” or another similar title. Of course, at

the same time as the asset is recorded, a corresponding liability (“Lease Liability” or similar

CA 21-2 (Continued)

(4) For this lease, Sylvan must disclose the future minimum lease payments in the aggregate

(b) (1) Based on the given facts, Breton has entered into a direct-financing lease. There is no

dealer or manufacturer profit included in the transaction, the discounted present value of the

(2) Breton should record a Lease Receivable for the present value of the minimum lease

payments and the present value of the residual value. It should also remove the machine

from the books by a credit to the applicable asset account.

(3) During the life of the lease, Breton will record payments received as a reduction in the

receivable. Interest is recognized as interest revenue by applying the implicit interest rate to

(4) Breton must make the following disclosures with respect to this lease:

(a) The components of the lease receivable in direct-financing leases, which are (1) the

CA 21-3

(a) A lease should be classified as a capital lease when it transfers substantially all of the benefits

and risks inherent to the ownership of property by meeting any one of the four criteria established

CA 21-3 (Continued)

(b) For Lease L, Santiago Company should record as a liability at the inception of the lease an

amount equal to the present value at the beginning of the lease term of the minimum lease

payments during the lease term. This amount excludes that portion of the payments representing

(c) For Lease L, Santiago Company should allocate each minimum lease payment between a reduc–

tion of the liability and interest expense so as to produce a constant periodic rate of interest on

the remaining balance of the liability.

CA 21-4

Part 1

(a) A lessee would account for a capital lease as an asset and a liability at the inception of the lease.

Rental payments during the year would be allocated between a reduction in the liability and

interest expense. The asset would be amortized in a manner consistent with the lessee’s normal

Part 2

(a) The lease receivable in the lease is the same for both a sales-type and a direct-financing lease.

The lease receivable is the present value of the minimum lease payments (net of amounts, if any,

included therein for executory costs such as maintenance, taxes, and insurance to be paid by the

CA 21-4 (Continued)

(c) In a sales-type lease, the excess of the sales price over the carrying amount of the leased

CA 21-5

(a) The appropriate amount for the leased aircraft on Albertsen Corporation’s balance sheet after the

lease is signed is $1,000,000, the fair value of the plane. In this case, fair value is less than the

present value of the net rental payments plus purchase option ($1,022,226). When this occurs,

the asset is recorded at the fair value.

(b) The leased aircraft will be reflected on Albertsen Corporation’s balance sheet as follows:

Noncurrent assets

Leased equipment …………………………………………………………………….. $1,000,000

Less: Accumulated depreciation—capital leases …………………………….. 61,667

$ 938,333

Note A

The company leases a Viking turboprop aircraft under a capital lease. The lease runs until

December 31, 2023. The annual lease payment is paid in advance on January 1 and amounts to

$141,780, of which $4,000 is for insurance and property taxes. The aircraft is being depreciated on

CA 21-5 (Continued)

Computations

Depreciation expense:

Capitalized amount ……………………………………………………….…. $1,000,000

CA 21-6

(a) The ethical issues are fairness and integrity of financial reporting versus profits and possibly

misleading financial statements. On one hand, if Buchanan can substantiate her position, it is

(b) If Buchanan has no particular expertise in copier technology, she has no rational case for her

suggestion. If she has expertise, then her suggestion may be rational and would not be merely a

means to manipulate the balance sheet to avoid recording a liability.

further research regarding copier technology before reaching a decision.

*CA 21-7

(a) The economic effect of a long-term capital lease on the lessee is similar to that of an installment

purchase. Such a lease transfers substantially all of the benefits and risks incident to the ownership

of property to the lessee. Therefore, the lease should be capitalized.

(b) (1) Perriman should account for the sale portion of the sale-leaseback transaction at January 1,

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 21–77

*CA 21-7 (Continued)

(2) Perriman should account for the leaseback portion of the sale-leaseback transaction at

January 1, 2014, by recording both an asset and a liability at an amount equal to the

(c) The deferred gain should be amortized over the lease term or life of the asset, whichever is

appropriate. During the first year of the lease, the amortization will be an amount proportionate to

FINANCIAL REPORTING PROBLEM

(a) In P&G’s Management’s Discussion and Analysis (under Contractual

Commitments), both capital leases and operating leases are disclosed.

(c) P&G disclosed future minimum rental commitments under noncancelable

operating leases in excess of one year as of June 30, 2011, of:

2012—$264 million

COMPARATIVE ANALYSIS CASE

(a) Southwest uses both capital leases and long-term operating leases.

Southwest primarily leases aircraft and terminal space.

(c) Future minimum commitments under noncancelable leases are set forth

below (in millions):

Capital

Operating

2012 …………………………………………….

$6

$ 640

2014 …………………………………………….

(d) At year-end 2011, the present value of minimum lease payments under

(e) The details of rental expense are set forth below:

2011

2010

2009