CHAPTER 11

SOLUTIONS TO B EXERCISES

E11-1B (15–20 minutes)

(a) Straight-line method depreciation for each of Years 1 through 3 =

$500,000 – $50,000

= $45,000

10

(b)

Sum-of-the-years’-digits =

10 X 11

= 55

2

(c)

Double-declining balance method

depreciation rate =

100%

X 2 = 20.00%

10

E11-2B (20–25 minutes)

(a) If there is any salvage value and the amount is unknown (as is the case

here), the cost would have to be determined by looking at the data for

E11-2B (Continued)

(b) $85,000 cost [from (a)] – $75,000 total depreciation = $10,000 salvage

value.

(e) The method that produces the lowest book value at the end of Year 3

would be the method that yields the highest accumulated depreciation at

the end of Year 3, which is DDB.

(f) The method that will yield the lowest gain (or highest loss) if the asset is

sold at the end of Year 4 is the method which will yield the highest book

value at the end of Year 4, which is the double-declining balance method

in this case.

E11-3B (15–20 minutes)

(a)

20 (20 + 1)

= 210

2

E11-3B (Continued)

(b)

100%

= 5%; 5% X 2 = 10%

20

E11-4B (15–25 minutes)

(a) $345,000 – $45,000 = $300,000; $300,000 ÷ 10 yrs. = $30,000

(d)

10 + 9 + 8 + 7 + 6 + 5 + 4 + 3 + 2 + 1 = 55 or

n(n + 1)

=

10(11)

= 55

2

2

(e)

$345,000 X 20% X 1/3 =

$23,000

[$345,000 – ($345,000 X 20%)] X 20% X 2/3 =

E11-5B (20–25 minutes)

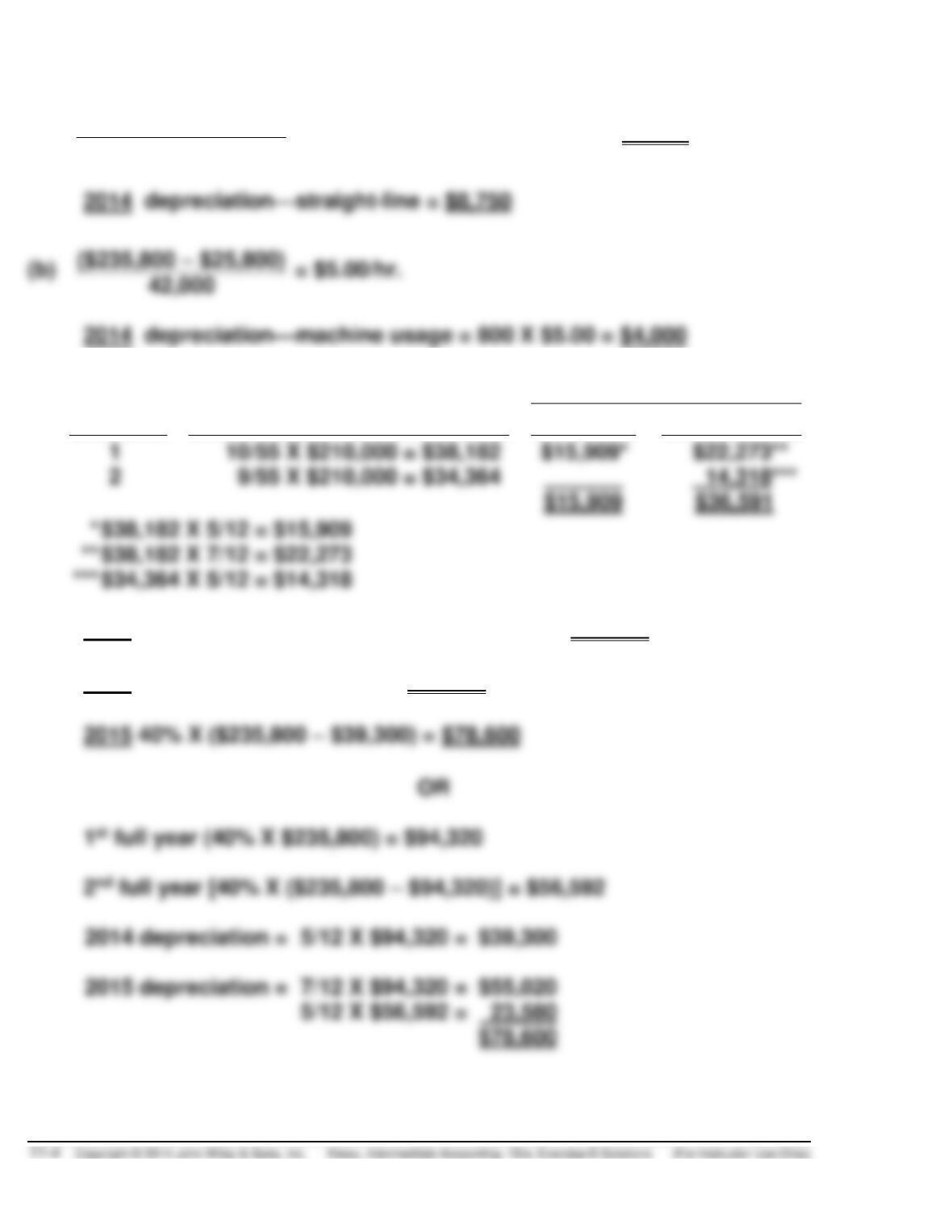

(a)

($235,800 – $25,800)

= $21,000/yr. = $21,000 X 5/12 = $8,750

10

($235,800 – $25,800)

(c)

Machine

Allocated to

Year

Total

2014

2015

2015 Depreciation—sum-of-the-years’-digits = $36,591

(d) 2014 40% X ($235,800) X 5/12 = $39,300

E11-6B (20–30 minutes)

(a)

2014

Straight-line

$250,000 – $50,000

= $25,000/year

8

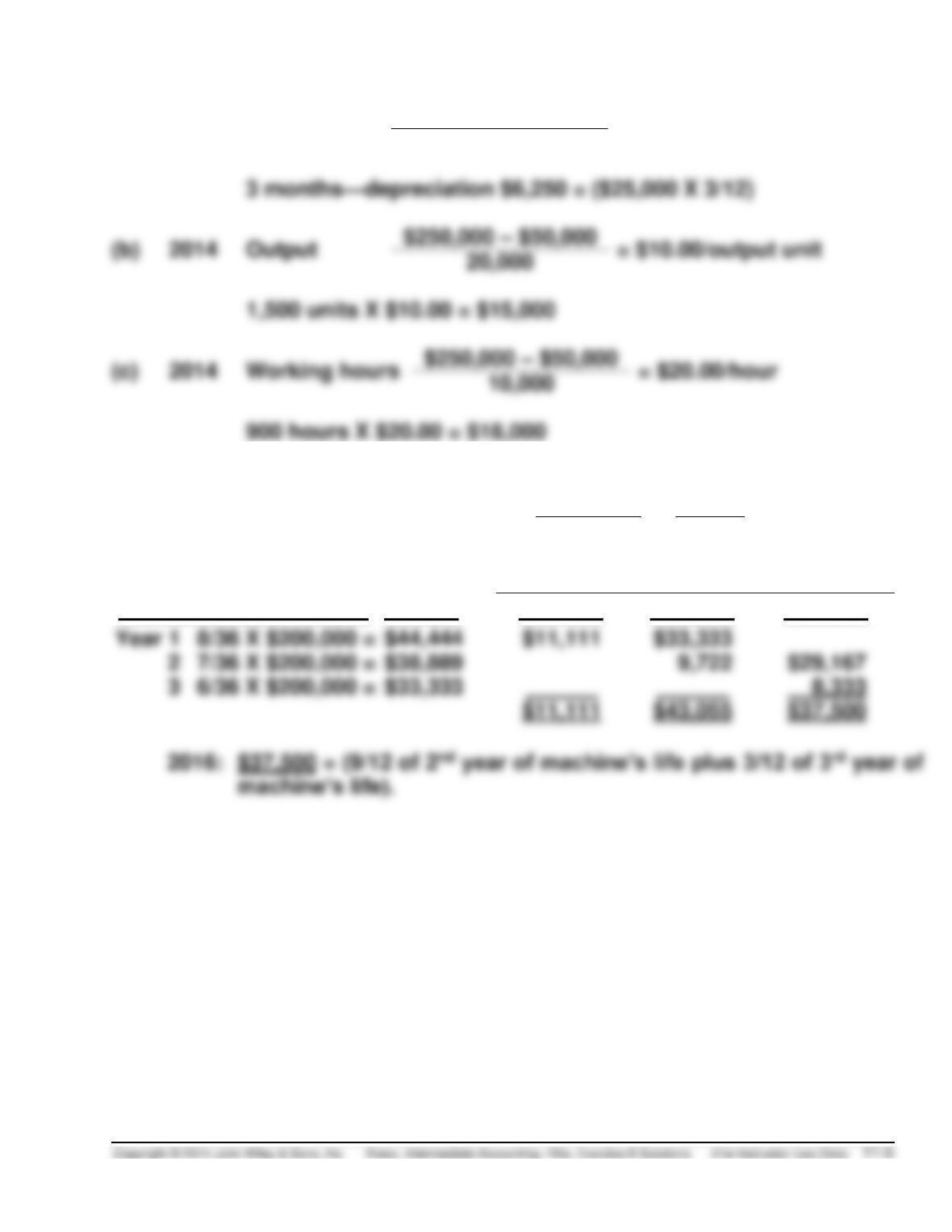

3 months—depreciation $6,250 = ($25,000 X 3/12)

(b)

2014

Output

$250,000 – $50,000

= $10.00/output unit

1,500 units X $10.00 = $15,000

900 hours X $20.00 = $18,000

(d)

8 + 7 + 6 + 5 + 4 + 3 + 2 + 1 = 36 or

n (n + 1)

=

8(9)

= 36

2

2

Allocated to

Sum-of-the-years’-digits

Total

2014

2015

2016

7/36 X $200,000 =

6/36 X $200,000 =

E11-6B (Continued)

(e) Double-declining balance 2005: 1/8 X 2 = 25%

2014: 25% X $250,000 X 3/12 = $15,625

OR

1st full year (25% X $250,000) = $62,500

E11-7B (25–35 minutes)

Methods of Depreciation

Description

Date

Purchased

Cost

Salvage

Life

Method

Accum. Depr.

to 2014

2015 Depr.

A

7/10/09

$216,000

$36,000

6

(a)

$105,000

(b) $

C

E11-7B (Continued)

Machine A—Testing the methods

(a) Straight-Line Method for 2011

$ 15,000

[($216,000 – $36,000) ÷

6] X 1/2

Straight-Line Method for 2012-14

$ 90,000

[($216,000 – $36,000) ÷

6] X 3

($216,000 X .333 X .5)

($180,000 X .333)

($120,000 X .333

Sum-of-the-Years-Digits for 2011

$ 25,714

[($216,000 – $36,000) X

6/21 X .5]

Sum-of-the-Years-Digits for 2012

$ 47,143

($180,000 X 5/21 X 1/2)

Sum-of-the-Years-Digits for 2013

$ 38,571

($180,000 X 5/21 X 1/2) +

($180,000 X 4/21 X 1/2)

($180,000 X 3/21 X 1/2)

($180,000 X 6/21 X 1/2) +

(b) Using SL, 2015 Depreciation is

$30,000

($216,000 – 36,000)/6

Machine B—Computation of the cost

(c) Asset has been depreciated for 1 1/2 years using the SYD method.

E11-7B (Continued)

(d) Using SYD, 2015 Depreciation is $23,333.

Sum-of-the-Years-Digits for 2015

$23,333

($100,000 X 4/15 X 1/2) +

($100,000 X 3/15 X 1/2)

(f) Using SL, 2015 Depreciation is $20,500

Thus the asset must have been purchased on February 12, 2014

$47,360

Machine D—Computation of Year Purchased

E11-8B (20–25 minutes)

Old Machine

October 1, 2010

Purchase…………………………………

$68,000

Freight ……………………………………

300

Installation ………………………………

E11-8B (Continued)

Book value, old machine, October 1, 2016:

[$76,000 – $19,500 – ($7,500 X 3)] = ……………………….

$34,000

Fair value ……………………………………………………………….

Loss on exchange ………………………………………………….

Cost of removal ………………………………………………………

75

(Note to instructor: The above computation is done to determine whether

there is a gain or loss from the exchange of the old machine with the new

New Machine

Basis of new machine

Cash paid ($86,000 – $22,000) ………

$64,000

Fair value of old machine …………….

Installation cost ………………………….

Depreciation for the year beginning October 1, 2016 = ($89,000 – $10,000) ÷ 10

= $7,900.

E11-9B (15–20 minutes)

(a)

Asset

Cost

Estimated

Salvage

Depreciable

Cost

Estimated

Life

Depreciation

per Year

A

$121,500

$16,500

$105,000

10

$10,500

B

100,800

14,400

86,400

9

9,600

C

108,000

10,800

97,200

9

D

4,500

52,500

7

7,500

E

70,500

7,500

63,000

6

$53,700

E11-9B (Continued)

(b)

Depreciation Expense—Plant Assets ………………………..

48,900

Accumulated Depreciation—Plant

Assets …………………………………………………………

(c)

Cash ……………………………………………………………………….

14,400

Accumulated Depreciation—Plant Assets ………………….

42,600

Plant Assets …………………………………………………..

E11-10B (10–15 minutes)

Sum-of-the-years’-digits =

8 X 9

= 36

2

E11-11B (10–15 minutes)

(a) No correcting entry is necessary because changes in estimate are

handled in the current and prospective periods.

(b) Revised annual charge:

Book value as of 1/1/2015 [$100,000 – ($8,000 X 5)] = $60,000

E11-12B (20–25 minutes)

(a) 1995–2001—($4,000,000 – $200,000) ÷ 40 = $95,000/yr.

(c) No adjusting entry required.

(d) Revised annual depreciation

Building

Book value: ($4,000,000 – $1,995,000*) …………..

Salvage value ………………………………………………..

Remaining useful life …………………………………….

Annual depreciation ………………………………………

Addition

Book value: ($1,500,000 – $647,500**)…………….

$852,500

Salvage value ………………………………………………..

20,000

832,500

Remaining useful life …………………………………….

Annual depreciation ………………………………………

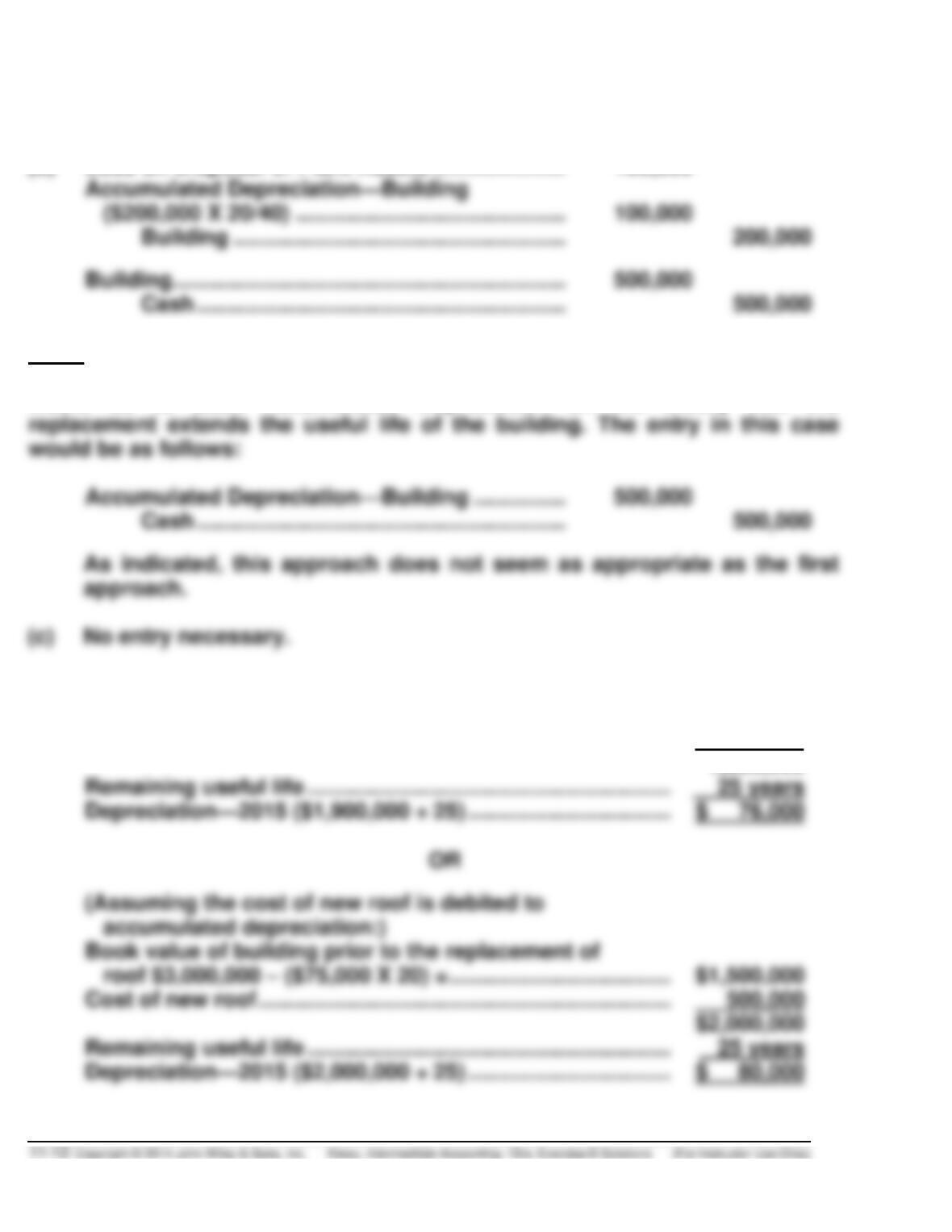

E11-13B (15–20 minutes)

(a) $3,000,000 ÷ 40 = $75,000

(b)

Loss on Disposal of Plant Assets …………………………….

100,000

Accumulated Depreciation—Building

($200,000 X 20/40) ………………………………………………..

100,000

500,000

Cash …………………………..………………………………….

Accumulated Depreciation—Building ………………………

500,000

Cash …………………………..………………………………….

Note: The most appropriate entry would be to remove the old roof and record

a loss on disposal, because the cost of old roof is given. Another alternative

would be to debit Accumulated Depreciation on the theory that the

(d) (Assuming the cost of old roof is removed:)

Building ($3,000,000 – $200,000 + $500,000) ………………….

$3,300,000

Accumulated Depreciation ($75,000 X 20 – $100,000) …….

1,400,000

1,900,000

Remaining useful life …………………………………………………..

accumulated depreciation:)

roof $3,000,000 – ($75,000 X 20) = ………………………………

$1,500,000

Cost of new roof ………………………………………………………….

500,000

$2,000,000

Remaining useful life …………………………………………………..

E11-14B (20–25 minutes)

(a)

Repair Expense……………………………………………………….

1,250

Equipment ………………………………………………………

1,250

(b)

The proper ending balance in the asset account is:

January 1 balance ……………………………….

$212,000

Add: New equipment:

Purchases ……………………………………..

Freight …………………………………………..

Installation …………………………..………..

Less: Cost of equipment sold ……………..

December 31 balance …………………………..

8/55 X $192,000 = ……………………………………………….

For equipment purchased in 2015: 10/55 X $84,500 = …..

Total …………………………………………………………………

(1) Straight-line: $276,500 ÷ 10 = $27,650

E11-15B (25–35 minutes)

(a)

2010

2011–2015

Incl.

2016

Total

1.

$300,000 – $25,000 = $275,000

$275,000 ÷ 10 = $27,500 per yr.

$169,973

3.

8/12 of $27,500

6/12 of $27,500

(b) The most accurate distribution of cost is given by methods 1 and 5 if it is

assumed that straight-line depreciation is satisfactory. Reasonable

E11-16B (10–15 minutes)

(a)

December 31, 2014

Loss on Impairment ………………………………………………..

2,400,000

Accumulated Depreciation—Equipment ……………….

2,400,000

Cost

$6,750,000

Accumulated depreciation

750,000

Carrying amount

Fair value

Loss in impairment

E11-16B (Continued)

(b)

December 31, 2015

Depreciation Expense ……………………………………………..

900,000

Accumulated Depreciation—Equipment ……………….

900,000

New carrying amount

$3,600,000

Useful life

Depreciation per year

(c) No entry necessary. Restoration of any impairment loss is not permitted.

E11-17B (15–20 minutes)

(a)

Loss on Impairment ………………………………………………..

2,415,000

Accumulated Depreciation—Equipment ……………..

2,415,000

Cost

$6,750,000

Accumulated depreciation

750,000

Carrying amount

Less: Fair value

Plus: Cost of disposal

15,000

Loss on impairment

(b) No entry necessary. Depreciation not taken on assets intended to be sold.

(c)

Accumulated Depreciation—Equipment ……………………

375,000

Recovery of Loss on Impairment ……………………..

375,000

Fair value………………………………………………………………..

Less: Cost of disposal ……………………………………………

Carrying amount ……………………………………………………..

E11-18B (15–20 minutes)

(a)

December 31, 2014

Loss on Impairment ………………………………………………..

300,000

Accumulated Depreciation—Equipment ……………….

300,000

Cost

$1,200,000

Accumulated depreciation

300,000

Carrying amount

Fair value

600,000

(b) It may be reported in the “Other expenses and losses” section, or it may

be highlighted as an unusual item in a separate section. It is not

reported as an extraordinary item.

(c) No entry necessary. Restoration of any impairment loss is not permitted.

(d) Management first had to determine whether there was an impairment. To

E11-19B (15–20 minutes)

(a)

Depreciation expense:

$90,000

= $3,000 per year

30 years

Cost of timber sold: $2,000 – $500 = $1,500

Note: The spraying costs as well as the costs to maintain the fire lanes and

roads are expensed each period and are not part of the depletion base.

E11-20B (10–15 minutes)

Cost per barrel of oil:

Initial payment =

$1,200,000

=

$2.40

500,000

Rental =

=

E11-21B (15–20 minutes)

(a) $1,500 – $500 = $1,000 per acre for timber

$1,000 X 8,000 acres

X 1,000,000 bd. ft. =

5,000 bd. ft. X 8,000 acres

X 1,000,000 bd. ft. = $200,000

40,000,000 bd. ft.

40,000,000 bd. ft.

E11-22B (15–20 minutes)

Depletion base: $2,000,000 + $200,000 – $300,000 + $500,000 = $2,400,000

Depletion rate: $2,400,000 ÷ 50,000 = $48/ton

E11-23B (15–20 minutes)

(a)

$5,000,000 + $1,000,000 + $400,000* – $800,000

= $112 depletion per ton

50,000

= 1.932 times

E11-24B (15–20 minutes)

(a) Asset turnover ratio:

E11-24B (Continued)

(c) Profit margin on sales:

$138

= 4.89%

$2,820

X

Asset Turnover

X

*E11-25B (20–25 minutes)

2015

2014

(a)

Revenues …………………………..………………………..

$600,000

$600,000

Operating expenses (excluding depreciation)…

440,000

440,000

Depreciation [($54,000 – $6,000) ÷ 6] ………………

8,000

8,000

Income before income taxes ………………………….

$152,000

$152,000

2015

2014

(b)

Revenues …………………………..………………………..

$600,000

Operating expenses (excluding depreciation)…

Depreciation* ……………………………………………….

Taxable income …………………………………………….

$149,200

(c) Book purposes ($54,000 – $6,000) $48,000

Tax purposes (entire cost of asset) $54,000

*E11-26B (15–20 minutes)

(a) 1. ($21,000 – $1,000) X 1/8 X 6/12 = $1,250 depreciation expense for

book purposes.

2. $21,000 X 1/5 X 1/2 = $2,100 depreciation for tax purposes.