CHAPTER 13

Current Liabilities and Contingencies

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Concept of liabilities;

definition and classification

of current liabilities.

1, 2, 3,

4, 6, 8

1, 16

1, 2

1, 2

2.

Accounts and notes

payable; dividends payable.

7, 11

1, 2, 3

2, 16

1, 2

1, 2

3.

Short-term obligations

expected to be refinanced.

9, 10

4

3, 4

3

4.

Deposits and advance

payments.

5, 12

5

2

5.

Compensated absences

and bonuses.

13, 14, 15

5, 6, 16

6.

Collections for third parties.

16

6, 7

7, 8, 9, 16

3, 4

7.

Contingent liabilities

(General).

17, 18, 19,

20, 22

10, 11

13, 16

10, 11, 13

4, 5, 6

8.

Guaranties and warranties.

21, 23

13, 14

10, 11, 16

5, 6, 7,

12, 14

6, 7

9.

Premiums and awards

offered to customers.

24, 25

12, 15, 16

8, 9, 12, 14

Self-insurance, litigation,

claims, and assessments,

asset retirement obligations.

26, 27, 28

10, 11, 12

2, 10,

11, 13

5, 6

Presentation and analysis.

29, 30, 31

17, 18, 19

9

3

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief Exercises

Exercises

Problems

Concepts

for

Analysis

of current

liabilities.

1. Describe the

nature, type,

and valuation

1,2,3,4,7,8

1, 2, 3,

4, 5, 6

1, 2, 7

1, 2

CA13-1

3. Identify types of

employee-

related

liabilities.

13,14

7, 8, 9

5, 6, 8, 9

3, 4

account for and

disclose gain

and loss

contingencies.

5. Explain the

accounting for

different types

of loss

contingencies.

17, 18,19,

20,21, 22,

10, 11, 12, 13,

14, 15

10, 11, 12, 13,

14, 15

2, 5, 6, 7, 8,

9, 10, 11, 12,

CA13-6,

CA13-7

6. Indicate how to

present and

analyze

liabilities and

contingencies.

29,30,31

16, 17,

18, 19

9

4. Identify the

criteria used to

15,16

10, 11, 12, 13,

14, 15

13

7, 10, 11, 13

CA13-4,

CA13-5

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E13-1

Balance sheet classification of various liabilities.

Simple

10–15

E13-2

Accounts and notes payable.

Moderate

15–20

E13-3

Refinancing of short-term debt.

Simple

10–12

E13-4

Refinancing of short-term debt.

Simple

20–25

E13-5

Compensated absences.

Moderate

25–30

E13-6

Compensated absences.

Moderate

25–30

E13-7

Adjusting entry for sales tax.

Simple

E13-8

Payroll tax entries.

Simple

10–15

E13-9

Payroll tax entries.

Simple

15–20

E13-10

Warranties.

Simple

10–15

E13-11

Warranties.

Moderate

15–20

E13-12

Premium entries.

Simple

15–20

E13-13

Contingencies.

Moderate

20–30

E13-14

Asset retirement obligation.

Moderate

25–30

E13-15

Premiums.

Moderate

25–35

E13-16

Financial statement impact of liability transactions.

Moderate

30–35

E13-17

Ratio computations and discussion.

Simple

15–20

E13-18

Ratio computations and analysis.

Simple

20–25

E13-19

Ratio computations and effect of transactions.

Moderate

15–25

P13-1

Current liability entries and adjustments.

Simple

25–30

P13-2

Liability entries and adjustments.

Simple

25–35

P13-3

Payroll tax entries.

Moderate

20–30

P13-4

Payroll tax entries.

Simple

20–25

P13-5

Warranties, accrual, and cash basis.

Simple

15–20

P13-6

Extended warranties.

Simple

10–20

P13-7

Warranties, accrual, and cash basis.

Moderate

25–35

P13-8

Premium entries.

Moderate

15–25

P13-9

Premium entries and financial statement presentation.

Moderate

30–45

P13-10

Loss contingencies: entries and essay.

Simple

25–30

P13-11

Loss contingencies: entries and essays.

Moderate

35–45

P13-12

Warranties and premiums.

Moderate

20–30

P13-13

Liability errors.

Moderate

25–35

P13-14

Warranty and coupon computation.

Moderate

20–25

CA13-1

Nature of liabilities.

Moderate

20–25

CA13-2

Current versus noncurrent classification.

Moderate

15–20

CA13-3

Refinancing of short-term debt.

Moderate

30–40

CA13-4

Loss contingencies.

Simple

15–20

CA13-5

Loss contingency.

Simple

15–20

CA13-6

Warranties and loss contingencies.

Simple

15–20

CA13-7

Warranties.

Moderate

20–25

SOLUTIONS TO CODIFICATION EXERCISES

CE13-1

Master Glossary

(a) An asset retirement is an obligation associated with the retirement of a tangible long-lived asset.

(b) Current liabilities is used principally to designate obligations whose liquidation is reasonably

expected to require the use of existing resources properly classifiable as current assets, or the

creation of other current liabilities. See paragraphs 210–10–45-5 through 45-12.

CE13-2

According to FASB ASC 410-20-50 (Asset Retirement and Environmental Obligations):

50-1 An entity shall disclose all of the following information about its asset retirement obligations:

(a) A general description of the asset retirement obligations and the associated long-lived

assets

(c) A reconciliation of the beginning and ending aggregate carrying amount of asset retirement

obligations showing separately the changes attributable to the following components,

50-2 If the fair value of an asset retirement obligation cannot be reasonably estimated, that

fact and the reasons therefor shall be disclosed.

CE13-3

According to FASB ASC 450-10-55 (Contingencies —Implementation Guidance and Illustrations):

Depreciation

55-2 The fact that estimates are used to allocate the known cost of a depreciable asset over the pe–

riod of use by an entity does not make depreciation a contingency; the eventual expiration of the

Estimates Used in Accruals

55-3 Amounts owed for services received, such as advertising and utilities, are not contingencies

Changes in Tax Law

55-4 The possibility of a change in the tax law in some future year is not an uncertainty.

CE13-4

According to FASB ASC 710-10–25-1 (Compensation Recognition—Compensated Absences), an

employer must accrue a liability for employees’ compensation for future absences if all of the following

conditions are met:

(a) The employer’s obligation relating to employees’ rights to receive compensation for future

absences is attributable to employees’ services already rendered.

(b) The obligation relates to rights that vest or accumulate. Vested rights are those for which the

ANSWERS TO QUESTIONS

1. Current liabilities are obligations whose liquidation is reasonably expected to require use of

2. You might explain to your friend that the accounting profession at one time prepared financial

statements somewhat in accordance with the broad or loose definition of a liability submitted by the

AICPA in 1953: “Something represented by a credit balance that is or would be properly carried

forward upon a closing of books of account according to the rules or principles of accounting,

provided such credit balance is not in effect a negative balance applicable to an asset. Thus the

3. As a lender of money, the banker is interested in the priority his/her claim has on the company’s

assets relative to other claims. Close examination of the liability section and the related footnotes

4. Current liabilities are obligations whose liquidation is reasonably expected to require the use of

existing resources properly classified as current assets, or the creation of other current liabilities.

5. Unearned revenue is a liability that arises from current sales but for which some services or

products are owed to customers in the future. At the time of a sale, customers pay not only for the

delivered product, but they also pay for future products or services (e.g., another plane trip, hotel

6. Payables and receivables generally involve an interest element. Recognition of the interest element

(the cost of money as a factor of time and risk) results in valuing future payments at their current

value. The present value of a liability represents the debt exclusive of the interest factor.

Questions Chapter 13 (Continued)

7. A discount on notes payable represents the difference between the present value and the face

8. Liabilities that are due on demand (callable by the creditor) should be classified as a current

liability. Classification of the debt as current is required because it is a reasonable expectation that

9. An enterprise should exclude a short-term obligation from current liabilities only if (1) it intends to

refinance the obligation on a long-term basis, and (2) it demonstrates an ability to consummate the

refinancing.

10. The ability to consummate the refinancing may be demonstrated (i) by actually refinancing the short-

11. A cash dividend formally authorized by the board of directors would be recorded by a debit to

Retained Earnings and a credit to Dividends Payable. The Dividends Payable account should be

classified as a current liability.

12. Unearned revenue arises when a company receives cash or other assets as payment from a

customer before conveying (or even producing) the goods or performing the services which it has

committed to the customer.

Unearned revenue is assumed to represent the obligation to the customer to refund the assets

total obligation.

Unearned revenues arise from the following activities:

(1) The sale by a transportation company of tickets or tokens that may be exchanged or used to

Questions Chapter 13 (Continued)

13. Compensated absences are employee absences such as vacation, illness, and holidays for which

it is expected that employees will be paid.

14. A liability should be accrued for the cost of compensated absences if all of the following conditions

are met:

(a) The employer’s obligation relating to employees’ rights to receive compensation for future

15. An employer is required to accrue a liability for “sick pay” that employees are allowed to accumu–

late and use as compensated time off even if their absence is not due to illness. An employer is

permitted but not required to accrue to liability for sick pay that employees are allowed to claim

only as a result of actual illness.

16. Employers generally withhold from each employee’s wages amounts to cover income taxes

(withholding), the employee’s share of FICA taxes, and other items such as union dues or health

17. (a) A contingency is defined as an existing condition, situation, or set of circumstances involving

18. A contingent liability should be recorded and a charge accrued to expense only if:

(a) information available prior to the issuance of the financial statements indicates that it is probable

that a liability has been incurred at the date of the financial statements, and

(b) the amount of the loss can be reasonably estimated.

19. A determinable current liability is susceptible to precise measurement because the date of payment,

the payee, and the amount of cash needed to discharge the obligation are reasonably certain. There

is nothing uncertain about (1) the fact that the obligation has been incurred and (2) the amount of the

obligation.

Questions Chapter 13 (Continued)

20. The terms probable, reasonably possible, and remote are used in GAAP to denote the chances

of a future event occurring, the result of which is a gain or loss to the enterprise. If it is probable

that a loss has been incurred at the date of the financial statements, then the liability (if reasonably

21. Under the cash-basis method, warranty costs are charged to expense in the period in which the

seller or manufacturer performs in compliance with the warranty, no liability is recorded for future

22. Under U.S. GAAP, companies may not record provisions for future operating losses. Such provi–

sions do not meet the definition of a liability, since the amount is not the result of a past transaction

23. The expense warranty approach and the sales warranty approach are both variations of the accrual

method of accounting for warranty costs. The expense warranty approach charges the estimated

future warranty costs to operating expense in the year of sale or manufacture. The sales warranty

approach defers a certain percentage of the original sales price until some future time when actual

costs are incurred or the warranty expires.

24. Southeast Airlines Inc.’s award plan is in essence a discounted ticket sale. Therefore, the full-fare

ticket should be recorded as unearned transportation revenue (liability) when sold and recognized

25. Although the accounting for this transaction has been studied, no authoritative guideline has been

developed to record this transaction. In the case of a free ticket award, AcSEC proposed that

26. An asset retirement obligation must be recognized when a company has an existing legal obligation

associated with the retirement of a long-lived asset and when the amount can be reasonably

estimated.

27. The absence of insurance does not mean that a liability has been incurred at the date of the financial

statements. Until the time that an event (loss contingency) occurs there can be no diminution in the

Questions Chapter 13 (Continued)

28. In determining whether or not to record a liability for pending litigation, the following factors must

be considered:

(a) The time period in which the underlying cause for action occurred.

29. There are several defensible recommendations for listing current liabilities: (1) in order of maturity,

(2) according to amount, (3) in order of liquidation preference. The authors’ recent review of pub–

30. The acid-test ratio and the current ratio are both measures of the short-term debt-paying ability of

the company. The acid-test ratio excludes inventories and prepaid expenses on the basis that these

31. (a) A liability for goods purchased on credit should be recorded when title passes to the purchaser.

If the terms of purchase are f.o.b. destination, title passes when the goods purchased arrive; if

f.o.b. shipping point, title passes when shipment is made by the vendor.

(b) Officers’ salaries should be recorded when they become due at the end of a pay period.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 13-1

July 1

Purchases ……………………………………………………….

60,000

Accounts Payable …………………………………………..

60,000

Freight–in ……………………………………………………….

1,200

Cash ……………………………………………………….

1,200

July 3

Accounts Payable …………………………………………………..

6,000

Purchase Returns and Allowances …………………..

6,000

July 10

Accounts Payable …………………………………………………..

54,000

Cash ($54,000 X 98%) …………………………..

52,920

Purchase Discounts ………………………………………..

1,080

BRIEF EXERCISE 13-2

11/1/14

Cash ……………………………………………………….

40,000

Notes Payable …………………………..…………………….

40,000

12/31/14

Interest Expense ……………………………………………………..

Interest Payable

($40,000 X 9% X 2/12) …………………………..

2/1/15

Notes Payable ……………………………………………………….

40,000

Interest Payable ………………………………………………………

Interest Expense ……………………………………………………..

Cash

[($40,000 X 9% X 3/12) + $40,000] …………………..

40,900

BRIEF EXERCISE 13-3

11/1/14

Cash ………………………………………………………………………

60,000

Discount on Notes Payable …………………………..

1,350

Notes Payable ………………………………………………..

61,350

12/31/14

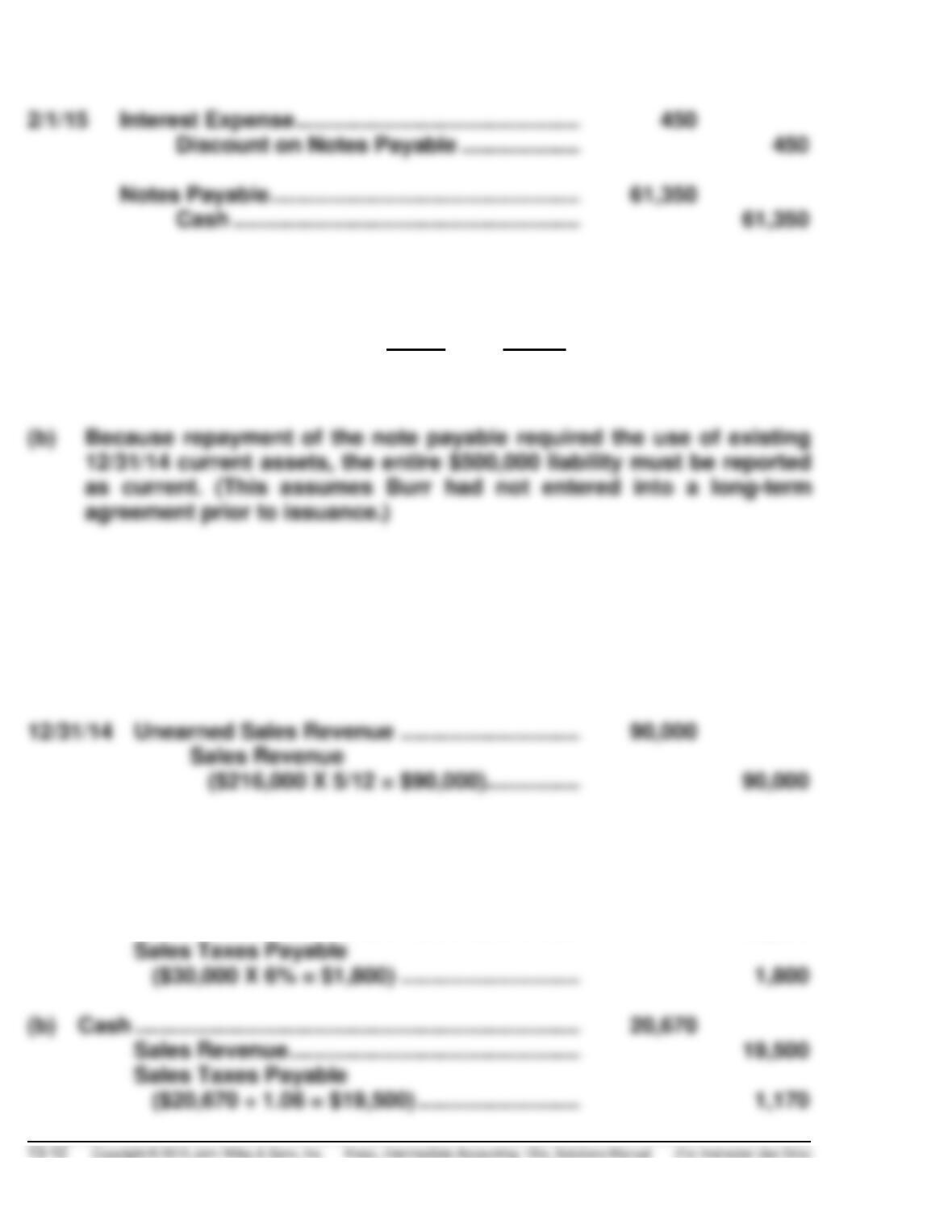

Interest Expense …………………………………………………….

BRIEF EXERCISE 13-3 (Continued)

Discount on Notes Payable …………………………..

Notes Payable ……………………………………………………….

Cash ……………………………………………………….

BRIEF EXERCISE 13-4

(a) Since both criteria are met (intent and ability), none of the $500,000

would be reported as a current liability. The entire amount would be

reported as a long-term liability.

BRIEF EXERCISE 13-5

8/1/14

Cash ……………………………………………………….

216,000

Unearned Sales Revenue

(12,000 X $18) ………………………………………………

216,000

Unearned Sales Revenue …………………………..

Sales Revenue

($216,000 X 5/12 = $90,000) …………………………..

90,000

BRIEF EXERCISE 13-6

(a)

Accounts Receivable ………………………………………………

31,800

Sales Revenue ………………………………………………..

30,000

Sales Taxes Payable

($30,000 X 6% = $1,800) …………………………..

(b)

Cash ………………………………………………………………………

Sales Revenue ………………………………………………..

BRIEF EXERCISE 13-7

Salaries and Wages Expense …………………………………..

24,000

FICA Taxes Payable ………………………………………..

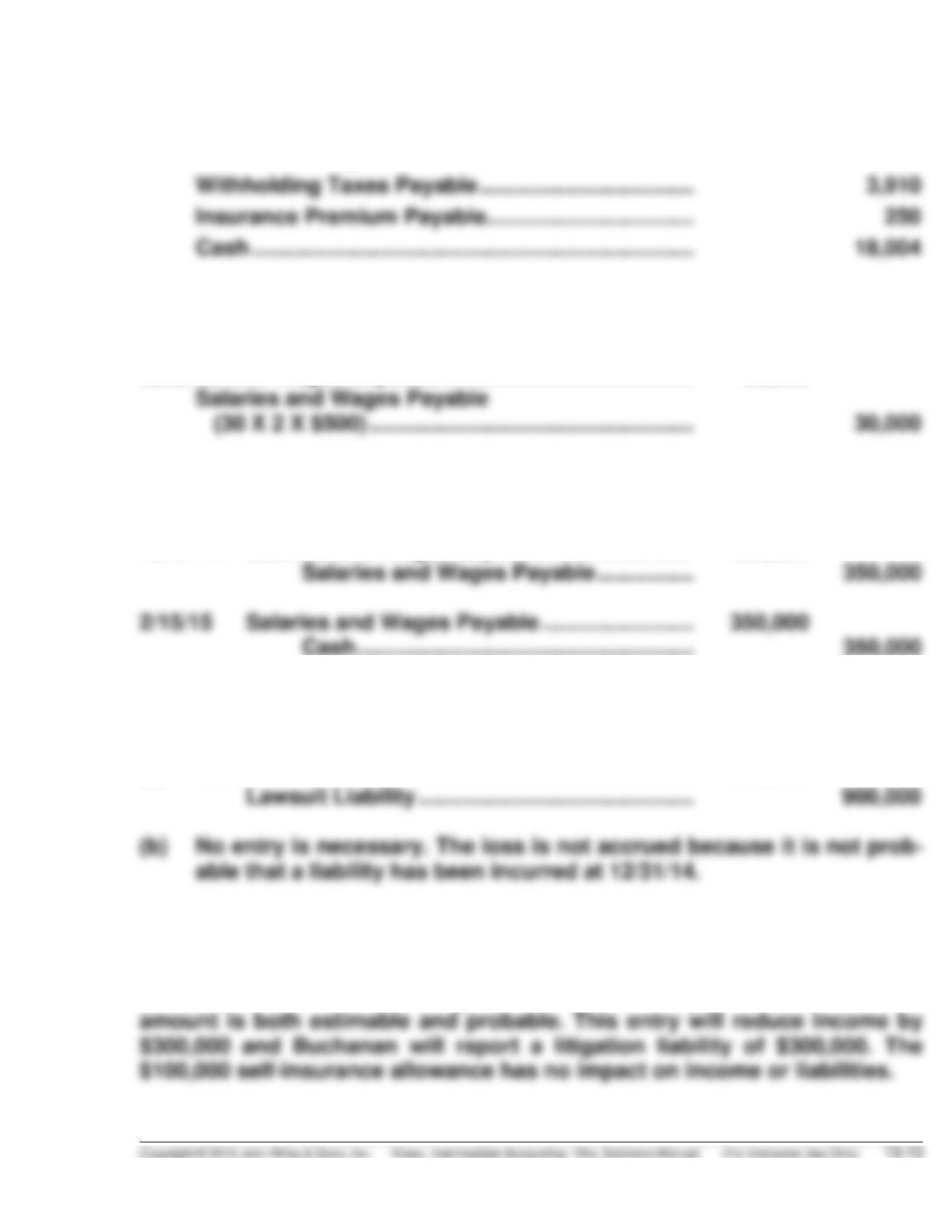

1,836

Withholding Taxes Payable ……………………………..

3,910

Insurance Premium Payable …………………………….

Cash ………………………………………………………………

BRIEF EXERCISE 13-8

Salaries and Wages Expense …………………………………..

30,000

Salaries and Wages Payable

(30 X 2 X $500) ……………………………………………..

BRIEF EXERCISE 13-9

12/31/14

Salaries and Wages Expense …………………………..

350,000

Salaries and Wages Payable …………………………..

2/15/15

Salaries and Wages Payable …………………………..

350,000

Cash ……………………………………………………….

BRIEF EXERCISE 13-10

(a)

Lawsuit Loss ……………………………………………………….

900,000

Lawsuit Liability ……………………………………………..

BRIEF EXERCISE 13-11

Buchanan should record a litigation accrual on the patent case, since the

BRIEF EXERCISE 13-12

Oil Platform …………………………………………………………….

450,000

Asset Retirement Obligation …………………………..

450,000

BRIEF EXERCISE 13-13

2014

Warranty Expense …………………………………………………..

70,000

Inventory ……………………………………………………….

Warranty Expense …………………………………………………..

Warranty Liability ……………………………………………………

BRIEF EXERCISE 13-14

(a)

Cash ………………………………………………………………………

1,980,000

Unearned Warranty Revenue

(20,000 X $99) ………………………………………………

1,980,000

(b)

Warranty Expense …………………………………………………..

Inventory ……………………………………………………….

(c)

Unearned Warranty Revenue …………………………..

Warranty Revenue

($1,980,000 X 180/1,080*) …………………………..

BRIEF EXERCISE 13-15

Premium Expense …………………………………………………….

96,000

Premium Liability ……………………………………………..

96,000*

*UPC codes expected to be sent in (30% X 1,200,000) …

360,000

UPC codes already redeemed …………………………………..

(240,000 ÷ 3) X ($1.10 + $0.60 – $0.50) ……………………..

SOLUTIONS TO EXERCISES

EXERCISE 13-1 (10–15 minutes)

(a) Current liability.

(b) Current liability.

(c) Current liability or long-term liability depending on term of warranty.

(d) Current liability.

(e) Current liability.

EXERCISE 13-2 (15–20 minutes)

(a)

Sept. 1

Purchases ……………………………………………………….

50,000

Accounts Payable …………………………..

50,000

Oct. 1

Accounts Payable …………………………………………………..

50,000

Notes Payable …………………………..

50,000

Oct. 1

Cash ……………………………………………………….

50,000

Discount on Notes Payable …………………………..

Notes Payable …………………………..

(b)

Dec. 31

Interest Expense …………………………………………………….

1,000

Interest Payable …………………………..

1,000

($50,000 X 8% X 3/12)

Dec. 31

Interest Expense …………………………………………………….

1,000

($4,000 X 3/12)

EXERCISE 13-2 (Continued)

(c)

(1)

Notes payable

$50,000

Interest payable

(2)

Notes payable

Less discount ($4,000 – $1,000)

EXERCISE 13-3 (10–12 minutes)

Hattie McDaniel Company

Partial Balance Sheet

December 31, 2014

Current liabilities:

Notes payable (Note 1)

Long-term debt:

Notes payable refinanced in February 2015 (Note 1)

950,000

Note 1.

Short-term debt refinanced. As of December 31, 2014, the company

had notes payable totaling $1,200,000 due on February 2, 2015. These

OR

Current liabilities:

Notes payable (Note 1)

$250,000

Short-term debt expected to be refinanced (Note 1)

950,000

(Same footnote as above.)

EXERCISE 13-4 (20–25 minutes)

KATE HOLMES COMPANY

Partial Balance Sheet

December 31, 2014

Current liabilities:

Notes payable (Note 1)

$3,400,000*

Long-term debt:

Note 1.

Under a financing agreement with Gotham State Bank the Company may

borrow up to 60% of the gross amount of its accounts receivable at an

EXERCISE 13-5 (25–30 minutes)

(a)

2013

To accrue expense and liability for vacations

Salaries and Wages Expense ………………………

7,200

Salaries and Wages Payable ……………….

7,200

(1)

To accrue the expense and liability for sick pay

Salaries and Wages Expense ………………………

(2)

Salaries and Wages Expense ………………

To record payment for compensated time when used by employees

Salaries and Wages Payable ……………………….

(3)

Cash ………………………………………………….

2,880

2014

To accrue the expense and liability for vacations

Salaries and Wages Expense ……………………..

7,920

Salaries and Wages Payable ………………

7,920

(4)

To accrue the expense and liability for sick pay

Salaries and Wages Expense ……………………..

4,752

Salaries and Wages Payable ………………

4,752

(5)

To record vacation time paid

Salaries and Wages Expense ……………………..

Salaries and Wages Payable ………………………

6,480

(6)

Cash …………………………………………………

(7)

To record sick leave paid

Salaries and Wages Expense ……………………..

Salaries and Wages Payable ………………………

(8)

Cash …………………………………………………

3,960

(9)

EXERCISE 13-5 (Continued)

(1)

9 employees X $10.00/hr. X 8 hrs./day X 10 days =

$7,200

(2)

9 employees X $10.00/hr. X 8 hrs./day X 6 days =

$4,320

(3)

9 employees X $10.00/hr. X 8 hrs./day X 4 days =

$2,880

(4)

9 employees X $11.00/hr. X 8 hrs./day X 10 days =

$7,920

(5)

9 employees X $11.00/hr. X 8 hrs./day X 6 days =

$4,752

(6)

9 employees X $10.00/hr. X 8 hrs./day X 9 days =

$6,480

(7)

9 employees X $11.00/hr. X 8 hrs./day X 9 days =

$7,128

(8)

9 employees X $10.00/hr. X 8 hrs./day X (6–4) days =

$1,440

9 employees X $11.00/hr. X 8 hrs./day X (5–2) days =

= $3,816

(9)

9 employees X $11.00/hr. X 8 hrs./day X 5 days =

Note: Vacation days and sick days are paid at the employee’s current wage.

Also, if employees earn vacation pay at different pay rates, a consistent pattern

(b) Accrued liability at year-end:

2013

2014

Vacation

Wages

Payable

Sick Pay

Wages

Payable

Vacation

Wages

Payable

Sick Pay

Wages

Payable

Jan. 1 balance

$ 0

$ 0

$7,200

$1,440

+ accrued

Dec. 31 balance

(1)

$1,440

(2)

(3)

$2,376

(4)

(1)

9 employees X $10.00/hr. X 8 hrs./day X 10 days =

$7,200

(2)

9 employees X $10.00/hr. X 8 hrs./day X (6–4) days =

$1,440

9 employees X $11.00/hr. X 8 hrs./day X 10 days =

$8,640

EXERCISE 13-6 (25–30 minutes)

(a)

2013

To accrue the expense and liability for vacations

Salaries and Wages Expense…………….

7,740

(1)

Salaries and Wages Payable ……..

7,740

To record sick leave paid

Salaries and Wages Expense…………….

2,880

(2)

Cash ………………………………………..

To record vacation time paid

No entry, since no vacation days were used.

2014

To accrue the expense and liability for vacations

Salaries and Wages Expense…………….

8,352

(3)

Salaries and Wages Payable ……..

8,352

To record sick leave paid

Salaries and Wages Expense…………….

3,960

(4)

Cash ………………………………………..

To record vacation time paid

Salaries and Wage Expense ……………..

Salaries and Wages Payable ……………..

6,966

(5)

Cash ………………………………………..

7,128

(6)

(1) 9 employees X $10.75/hr. X 8 hrs./day X 10 days = $7,740

(2) 9 employees X $10.00/hr. X 8 hrs./day X 4 days = $2,880