Continuing Case Solution

Chapter 19

(a)

Memorandum

To: Eric Conner and Phil Martin, CM2

From: L. Harbach

Re: Income Taxes

Date: February 4, 2013

According to GAAP (see FASB ASC 740-10-05-05), the framework for the

Temporary Differences

FASB ASC 740-10-05-7 describes the concepts of temporary differences:

A temporary difference refers to a difference between the tax basis of an asset or

liability, determined based on recognition and measurement requirements for tax

positions, and its reported amount in the financial statements that will result in

Examples of temporary differences:

(1) Accelerated depreciation for income tax and straight-line for financial

reporting can cause a temporary difference between the book and tax

value of the asset. This temporary difference is caused by the timing

Continuing Case Solution

15

(2) Revenue collected in advance and reported on the cash basis for income

tax but on the accrual basis for financial reporting can cause a temporary

Permanent Differences

Permanent differences are caused by items that (1) enter into pre-tax financial

Examples of permanent differences:

Interest received on state and municipal obligations; expenses incurred in

Continuing Case Solution

16

(b)

Memorandum

To: Eric Conner and Phil Martin, CM2

From: L. Harbach

Re: Adjusting Entry for Income Tax Expense

Date: February 4, 2013

Looking at the various business activities that the company anticipates for 2013, I

have detailed the income tax adjusting journal entry (combined) that will be

required. Below are the calculations for current and deferred income taxes; on

the next page are the individual journal entries as well as the combined journal

entry.

Current Income Tax Calculation 2013

Future Future

Deferred Tax Calculations Taxable Deductible

Amount (deferred tax liability)

Amount (Deferred Tax Asset

)

Fixed asset book value difference $30

,000

Warranty payable difference

$75,000

,500

0

0

,500

$26,250

$510,000

80,000

75,000

628,000

$219,800

Continuing Case Solution

17

Journal Entries:

Income Tax Expense

219,800

Income Tax Payable

219,800

,500

26,250

26,250

26,250

219,800

Continuing Case Solution

18

Additional Activities: Extend your accounting knowledge

(a)

Memorandum

To: Eric Conner and Phil Martin, CM2

From: L. Harbach

Re: Income Taxes

Date: February 8, 2013

Deferred tax assets are recognized for all deductible temporary differences.

These assets represent the increase in taxes refundable (saved) in future years

FASB ASC 740-10-30-5 dictates when the valuation allowance is to be used:

Reduce deferred tax assets by a valuation allowance if, based on the weight of

The ultimate decision of whether a valuation allowance account is required is up

to management. The following excerpts from the FASB Codification, list the

positive and negative evidence that must be weighed in making this decision.

The following examples of negative evidence (evidence indicating it is more likely

than not that a deferred tax asset will not be realized) are listed in FASB ASC

740-10-30-21:

Forming a conclusion that a valuation allowance is not needed is difficult when

there is negative evidence such as cumulative losses in recent years. Other

examples of negative evidence include (but are not limited to) the following:

Continuing Case Solution

FASB ASC 740-10-30-22 lists the following evidence that would support the

assertion that a deferred tax asset is more likely than not to be realized:

Examples (not prerequisites) of positive evidence that might support a conclusion

that a valuation allowance is not needed when there is negative evidence include

(but are not limited to) the following:

a. Existing contracts or firm sales backlog that will produce more than

Finally, FASB ASC 740-10-30-23 addresses the role of judgment in determining

the need for a valuation allowance:

An entity shall use judgment in considering the relative impact of negative and

positive evidence. The weight given to the potential effect of negative and positive

evidence shall be commensurate with the extent to which it can be objectively

verified. The more negative evidence that exists, the more positive evidence is

Continuing Case Solution

20

(b)

Memorandum

To: Eric Conner and Phil Martin, CM2

From: L. Harbach

Re: Earnings Management

Date: February 8, 2013

Some managers take the opportunity to manage earnings by creating a valuation

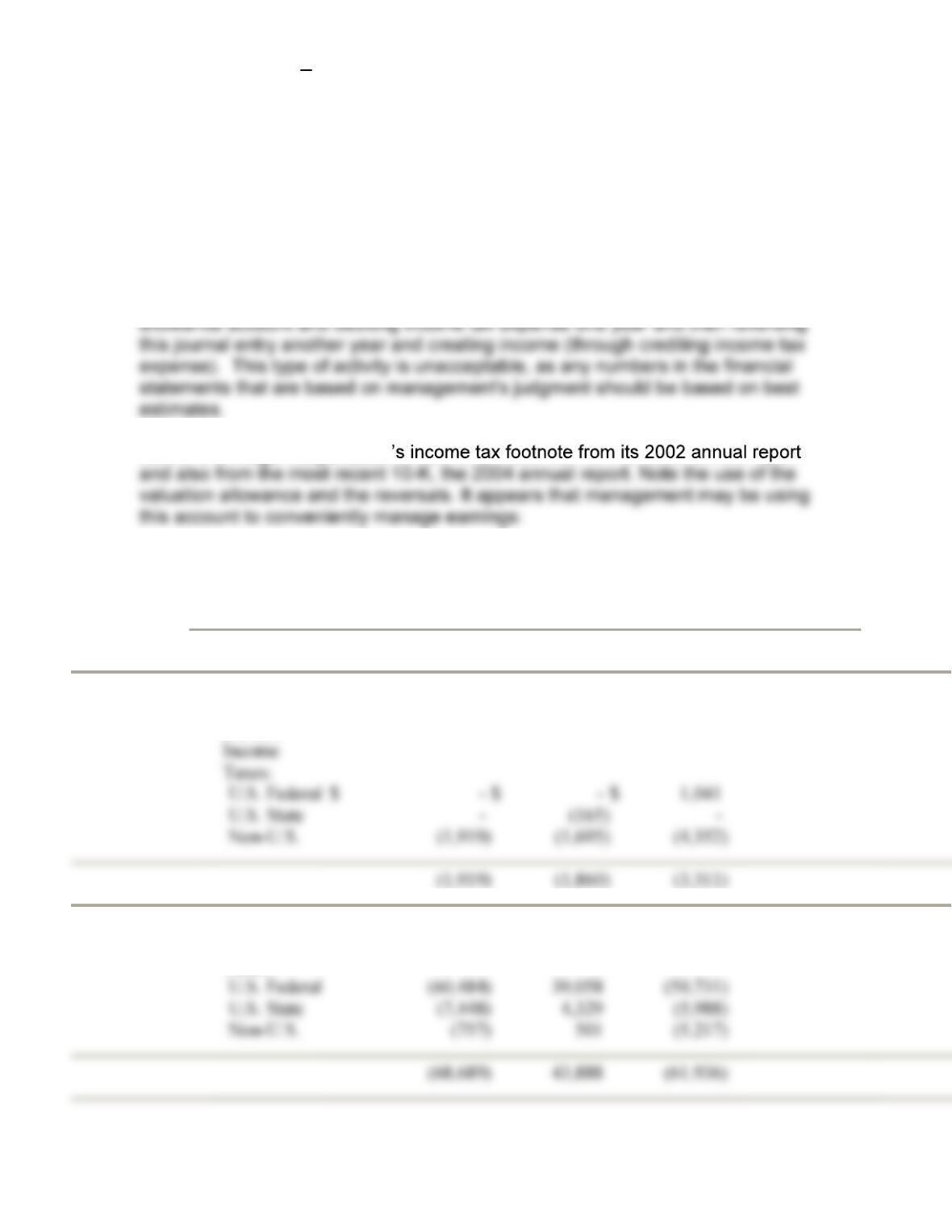

Below is Iomega Corporation

The income tax benefit (provision) consisted of the following:

Years Ended December 31,

2002

2001

2000

(In thousands)

Current

Taxes:

U.S. Federal

$

–

$

–

$

1,041

–

)

)

2

)

(1,919

)

(1,860

)

(3,311

)

Deferred

Income

Taxes:

U.S. Federal

(60,484

)

39,058

(50,731

)

U.S. State

)

4,329

)

(68,689

)

43,888

(61,936

)

Continuing Case Solution

21

Total current

and deferred

Benefit

(provision)

for income

taxes

$ (41,170

)

$ 12,846

$ 7,312

Years Ended December 31,

2004 2003

(In thousands)

Current

Income Taxes:

U.S.

State

$

(878

) $ (833

)

)

)

)

)

Federal

20,167

14,495

Non-

U.S.

(3,

865

)

(3,178

)

18,692

20,332

)

)

)

Continuing Case Solution

22

Total current

and deferred

income taxes

16,268

18,437

(c) There is substantial judgment is determining income tax expense because

much of the expense is based on deferred tax assets and liabilities created from

temporary differences. The time when these temporary differences reverse is

evaluated for future benefits.

> Statement of Financial Position Related Disclosures

50-2 The components of the net deferred tax liability or asset recognized in an entity’s

statement of financial position shall be disclosed as follows:

Continuing Case Solution

23

50-3 An entity shall disclose both of the following:

a. The amounts and expiration dates of operating loss and tax credit

> Income Statement Related Disclosures

50-9 The significant components of income tax expense attributable to continuing

operations for each year presented shall be disclosed in the financial statements or notes

thereto. Those components would include, for example:

effects of other components

g.

Adjustments of a deferred tax liability or asset for enacted changes in tax laws

or rates or a change in the tax status of the entity

h. Adjustments of the beginning-of-the-year balance of a valuation allowance

because of a change in circumstances that causes a change in judgment about the

>

Income Tax Expense Compared to Statutory Expectations

24

50-11 The reported amount of income tax expense may differ from an expected

amount based on statutory rates. The following guidance establishes the disclosure

requirements for such situations and differs for public and nonpublic entities.

There are additional disclosure requirements for public entities (FASB ASC 740-10-50-