PROFESSIONAL RESEARCH (Continued)

d. Assess the effects on an entity’s financial position of both its

45–16 All of the following are cash inflows for operating activities:

a. Cash receipts from sales of goods or services, including

receipts from collection or sale of accounts and both short–

b. Cash receipts from returns on loans, other debt instruments of

other entities, and equity securities—interest and dividends.

c. All other cash receipts that do not stem from transactions

45–17 All of the following are cash outflows for operating activities:

a. Cash payments to acquire materials for manufacture or goods

for resale, including principal payments on accounts and both

b. Cash payments to other suppliers and employees for other

goods or services.

PROFESSIONAL RESEARCH (Continued)

c. Cash payments to governments for taxes, duties, fines, and

other fees or penalties and the cash that would have been paid

for income taxes if increases in the value of equity instruments

d. Cash payments to lenders and other creditors for interest.

e. Cash payment made to settle an asset retirement obligation.

PROFESSIONAL SIMULATION

Note: This assignment is available on the Kieso website.

Financial Statements

ELLWOOD HOUSE, INC.

Statement of Cash Flows

For the Year Ended December 31, 2015

Cash flows from operating activities

Net income …………………………………………………… $42,000

Adjustments to reconcile net income to net

Cash flows from investing activities

Purchase of land (c) ……………………………………… (5,500)

Sale of investments (d)………………………………….. 15,500

Net cash provided by investing activities ……….. 10,000

Noncash investing and financing activities

Issuance of bonds for equipment …………………… $32,000

PROFESSIONAL SIMULATION (Continued)

Explanation

Dear Mr. Brauer:

Enclosed is your statement of cash flows for the year ending December 31,

2015. I would like to take this opportunity to explain the changes which

occurred in your business as a result of cash activities during 2015.

(Please refer to the attached statement of cash flows.)

The second category, cash flows from investing activities, results from

the acquisition/disposal of long-term assets including the purchase of

another entity’s debt or equity securities. Your purchase of land (item c)

as well as the sale of your investment portfolio (item d) represent your

investing activities during 2015, the purchase being a $5,500 outflow

and the sale being a $15,500 inflow.

Sincerely,

IFRS CONCEPTS AND APPLICATION

IFRS23-1

IAS 7, “Cash Flow Statements,” provides the overall IFRS requirements for

cash flow information.

IFRS23-2

As in U.S. GAAP, the statement of cash flows is a required statement for

Other similarities include: (1) Companies preparing financial statements

under IFRS must prepare a statement of cash flows as an integral part;

(2) Both IFRS and U.S. GAAP require that the statement of cash flows should

Notable differences are (1) IFRS encourages companies to disclose the

aggregate amount of cash flows that are attributable to the increase in

operating capacity separately from those cash flows that are required to

maintain operating capacity; (2) The definition of cash equivalents used in

IFRS is not the same as that used in U.S. GAAP. A major difference is that in

certain situations bank overdrafts are considered part of cash and cash

IFRS23-3

Presently, the FASB and the IASB are involved in a joint project on the

presentation and organization of information in the financial statements. The

FASB favors presentation of operating cash flows using the direct method

IFRS23-4

Examples of non-cash transactions are: (1) issuance of shares for non-cash

IFRS23-5

(a) Operating—add to net income.

(b) Financing activity.

(c) Investing activity.

IFRS23-6

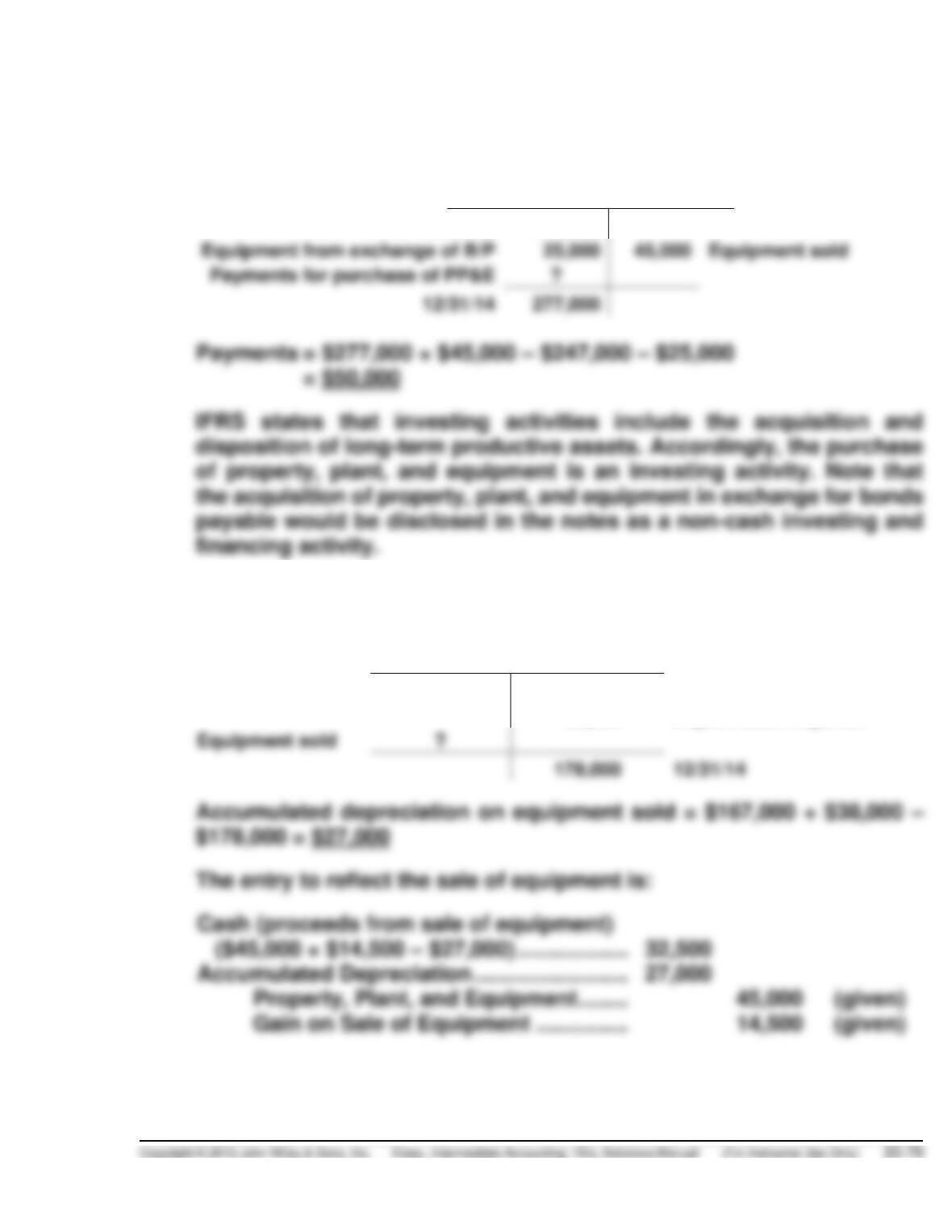

(a) The solution can be determined through use of a T-account for

Property, Plant, and Equipment.

Property, Plant & Equipment

12/31/13

247,000

Equipment sold

12/31/14

277,000

(b) The solution can be determined through use of a T-account for Accu-

mulated Depreciation.

Accumulated Depreciation

167,000

12/31/13

38,000

Depreciation expense

Equipment sold

178,000

12/31/14

IFRS23-6 (Continued)

The proceeds from the sale of equipment of $32,500 are considered

(c) The cash dividends paid can be determined by analyzing T-accounts

for Retained Earnings and Dividends Payable.

Retained Earnings

91,000

12/31/13

Dividends declared

31,000

Net income

12/31/14

12/31/13

18,000

Dividends declared

12/31/14

Financing activities include all cash flows involving liabilities and equity

other than operating items. Payment of cash dividends is thus a

financing activity.

(d) The redemption of bonds payable amount is determined by setting up

a T-account for Bonds Payable.

46,000

12/31/13

25,000

Issuance of B/P for PP&E

Redemption of B/P

49,000

12/31/14

IFRS23-6 (Continued)

IFRS23-7

DINGEL CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income………………………………………………….. $14,750(a)

Adjustments to reconcile net income to net

cash provided by operating activities:

Cash flows from investing activities

Sale of equity investments …………………………... 4,700

Sale of equipment ……………………………………….. 2,500

Purchase of equipment (cash) ……………………… (20,000)

Proceeds from flood damage to building ………. 32,000

Net cash provided by investing activities ……… 19,200

IFRS23-7 (Continued)

Supplemental disclosures of cash flow information:

Cash paid during the year for:

Non-cash investing and financing activities:*

Retired note payable by issuing ordinary shares …. $10,000

Supporting Computations:

(a) Ending retained earnings ……………………………………. $20,750

Beginning retained earnings ………………………………. (6,000)

Net income ……………………………………………………. $14,750

(c) Cost …………………………………………………………………… $29,750

Accumulated depreciation …………………………………… (6,000)

Book value …………………………………………………………. 23,750

Proceeds from insurance …………………………………….. (32,000)

Gain from flood damage …………………………………. ($ 8,250)

IFRS23-8

(a) According to IAS 7, “Information about the cash flows of an entity is

useful in providing users of financial statements with a basis to

assess the ability of the entity to generate cash and cash equivalents

and the needs of the entity to utilise those cash flows. The economic

(b) According to paragraph 10, “The statement of cash flows shall report

cash flows during the period classified by operating, investing and

financing activities.” Further, paragraph 11 states “An entity presents

(c) According to paragraph 14, “Cash flows from operating activities are

primarily derived from the principal revenue-producing activities of

the entity. Therefore, they generally result from the transactions and

other events that enter into the determination of profit or loss. Examples

of cash flows from operating activities are:

(a) cash receipts from the sale of goods and the rendering of services;

IFRS23-9

(a) M&S uses the indirect method to compute and report net cash

(b) The most significant item in the investing activities section is the

£564.3 million that M&S spent on “property, plant and equipment.” The

most significant item in the financing activities section is redemption

of medium-term notes (£307.6 million).