EXERCISE 11-5 (20–25 minutes)

(a)

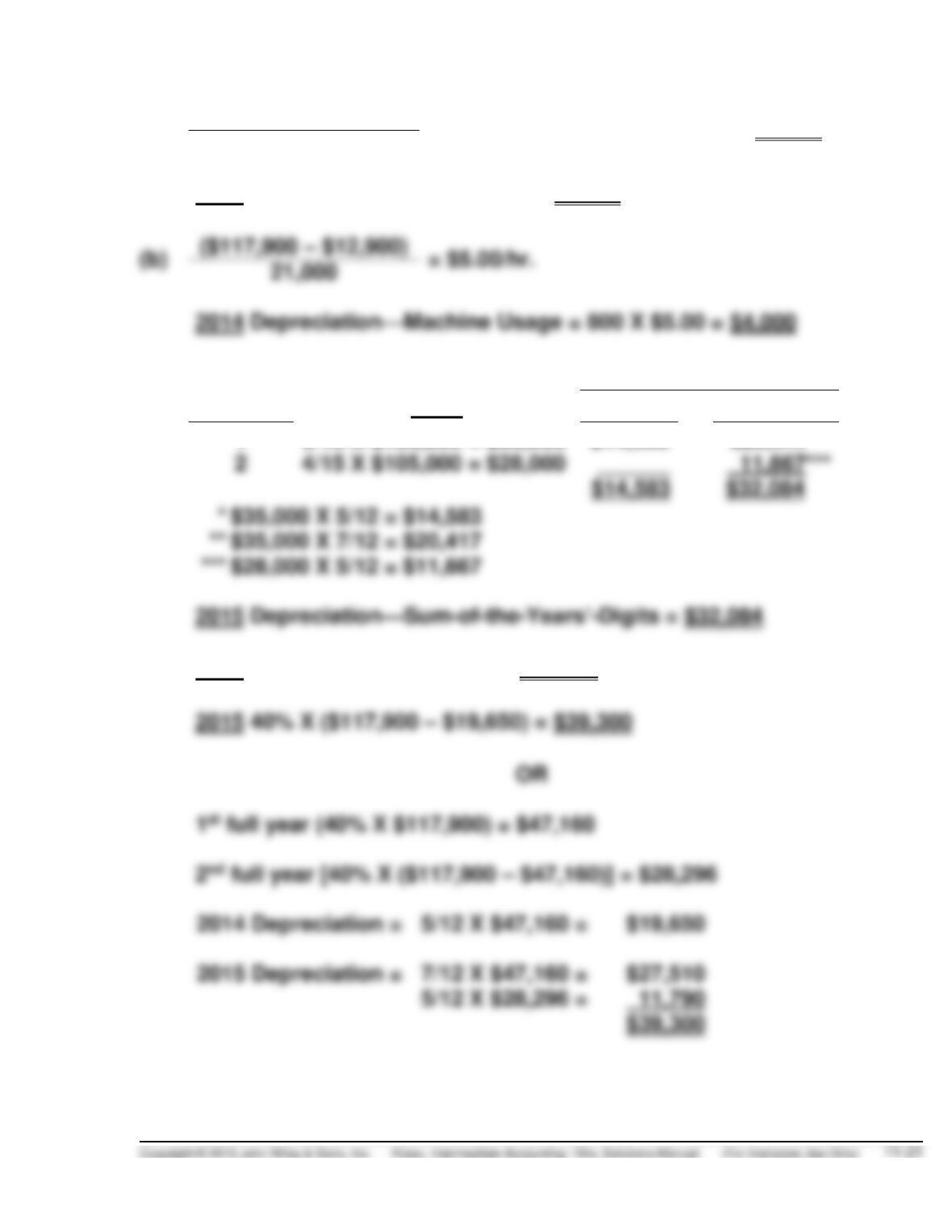

($117,900 – $12,900)

= $21,000/yr. = $21,000 X 5/12 = $8,750

5

2014 Depreciation—Straight line = $8,750

(c)

Machine

Allocated to

Year

Total

2014

2015

1

5/15 X $105,000 = $35,000

$14,583*

$20,417**

(d) 2014 40% X ($117,900) X 5/12 = $19,650

5/12 X $47,160 =

5/12 X $28,296 =

$39,300

EXERCISE 11-6 (20–30 minutes)

(a)

2014

Straight-line

$212,000 – $12,000

= $25,000/year

8

(b)

2014

Output

$212,000 – $12,000

= $5.00/output unit

40,000

(d)

8 + 7 + 6 + 5 + 4 + 3 + 2 + 1 = 36 OR

n (n + 1)

=

8(9)

= 36

2

2

Allocated to

Sum-of-the-years’-digits

Total

2014

2015

2016

Year 1

8/36 X $200,000 =

$44,444

$11,111

$33,333

$38,889

$29,167

$33,333

8,333

(e) Double-declining balance 2015: 1/8 X 2 = 25%.

2014: 25% X $212,000 X 3/12 = $13,250

EXERCISE 11-6 (Continued)

2nd full year [25% X ($212,000 – $53,000)] = $39,750

EXERCISE 11-7 (25–35 minutes)

Methods of Depreciation

Description

Date

Purchased

Cost

Salvage

Life

Method

Accum. Depr.

to 2015

2016 Depr.

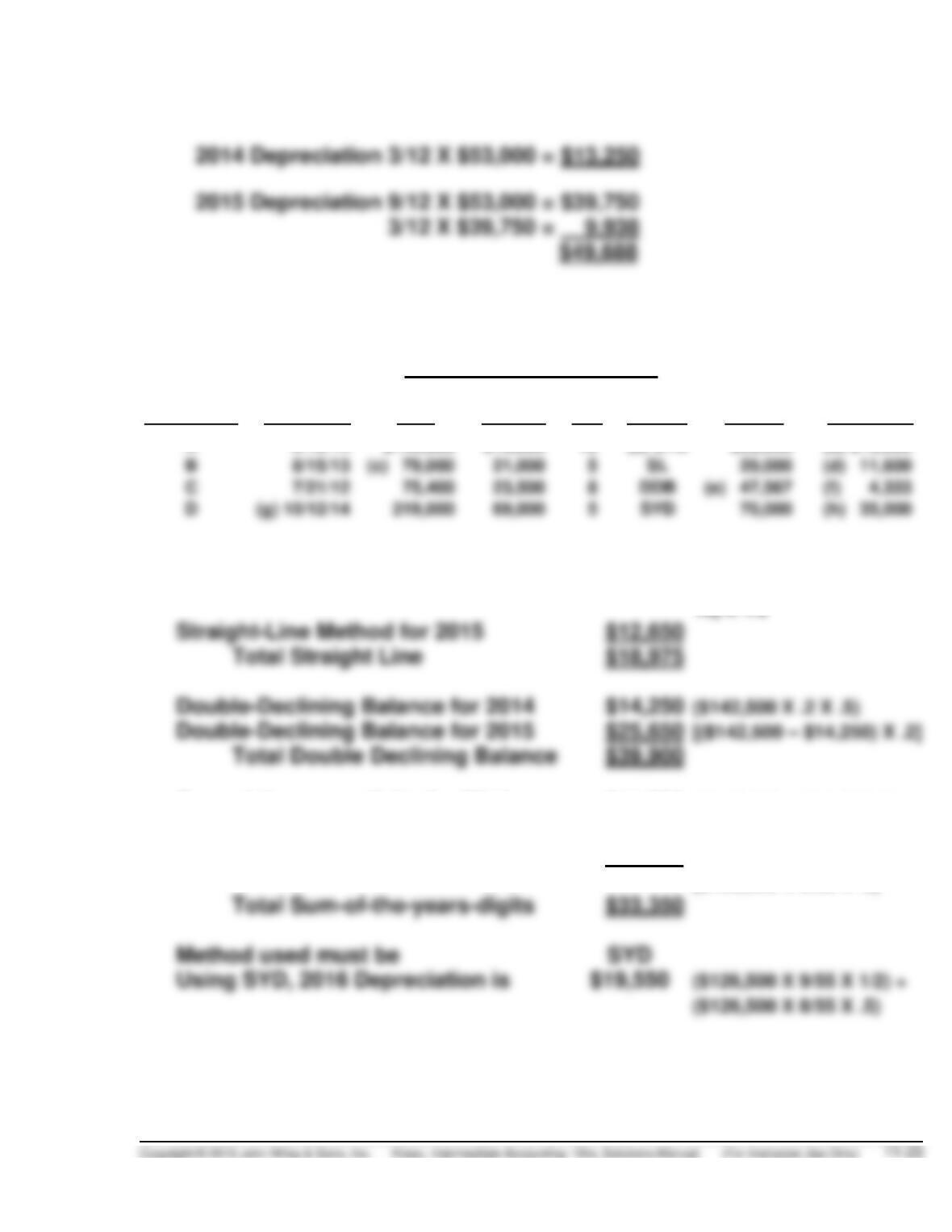

A

2/12/14

$142,500

$16,000

10

(a) SYD

$33,350

(b) $19,550

B

8/15/13

(d) 11,600

C

(e) 47,567

(f) 4,333

D

(g) 10/12/14

(h) 35,000

Machine A—Testing the methods

Straight-Line Method for 2014

$ 6,325

[($142,500 – $16,000) ÷

10] X 1/2

Sum-of-the-years-digits for 2014

$11,500

[($142,500 – $16,000) X

10/55 X .5]

Sum-of-the-years-digits for 2015

$21,850

($126,500 X 10/55 X 1/2) +

($126,500 X 9/55 X .5)

Using SYD, 2016 Depreciation is

EXERCISE 11-7 (Continued)

Machine B—Computation of the cost

Asset has been depreciated for 2 1/2 years using the straight-line

method.

Machine C—Using the double-declining balance method of depreciation

2012’s depreciation is

$ 9,425

($75,400 X .25 X .5)

2014’s depreciation is

$12,370

($75,400 – $25,919) X .25

2015’s depreciation is

$ 9,278

($75,400 – $38,289) X .25

Using DDB, 2016 Depreciation is $4,333 ($75,400 – $47,567 – $23,500)

Machine D—Computation of Year Purchased

First Half Year using SYD =

$25,000

[($219,000 – $69,000) X

EXERCISE 11-8 (20–25 minutes)

Old Machine

June 1, 2012

Purchase

$31,000

Freight

200

Installation

500

Total cost

$31,700

Annual depreciation charge: ($31,700 – $2,500) ÷ 10 = $2,920

Book value, old machine, June 1, 2016:

[$33,680 – $2,920 – ($3,140 X 3)] =

$21,340

Less: Fair value

Loss on exchange

Cost of removal

75

Total loss

$ 1,415

(Note to instructor: The above computation is done to determine whether

there is a gain or loss from the exchange of the old machine with the new

machine and to show how the cost of removal might be reported. Also, if a

New Machine

Basis of new machine

Cash paid ($35,000 – $20,000)

$15,000

Fair value of old machine

20,000

Installation cost

EXERCISE 11-9 (15–20 minutes)

(a)

Asset

Cost

Estimated

Salvage

Depreciable

Cost

Estimated

Life

Depreciation

per Year

A

$ 40,500

$ 5,500

$ 35,000

10

$ 3,500

B

33,600

4,800

28,800

9

3,200

23,500

2,500

21,000

6

3,500

Composite life = $134,700 ÷ $16,300, or 8.26 years

Composite rate = $16,300 ÷ $152,600, or approximately 10.7%

(b)

Depreciation Expense ……………………………………………..

16,300

Assets ……………………………………………………….

Accumulated Depreciation—Plant Assets ………………..

14,200

Plant Assets …………………………………………………..

EXERCISE 11-10 (10–15 minutes)

Sum-of-the-years’-digits =

8 X 9

= 36

2

Using Y to stand for the years of remaining life:

Multiplying both sides by 36:

EXERCISE 11-11 (10–15 minutes)

(a) No correcting entry is necessary because changes in estimate are

(b) Revised annual charge

Book value as of 1/1/2015 [$60,000 – ($7,000 X 5)] = $25,000

Accumulated Depreciation—Machinery ……………

EXERCISE 11-12 (20–25 minutes)

(a) 1988–1997—($2,000,000 – $60,000) ÷ 40 = $48,500/yr.

(d) Revised annual depreciation

Building

Book value: ($2,000,000 – $1,358,000*)

$642,000

Salvage value

60,000

582,000

Annual depreciation

$ 18,188

EXERCISE 11-12 (Continued)

Addition

Book value: ($500,000 – $288,000**)

$ 212,000

Less: Salvage value

20,000

192,000

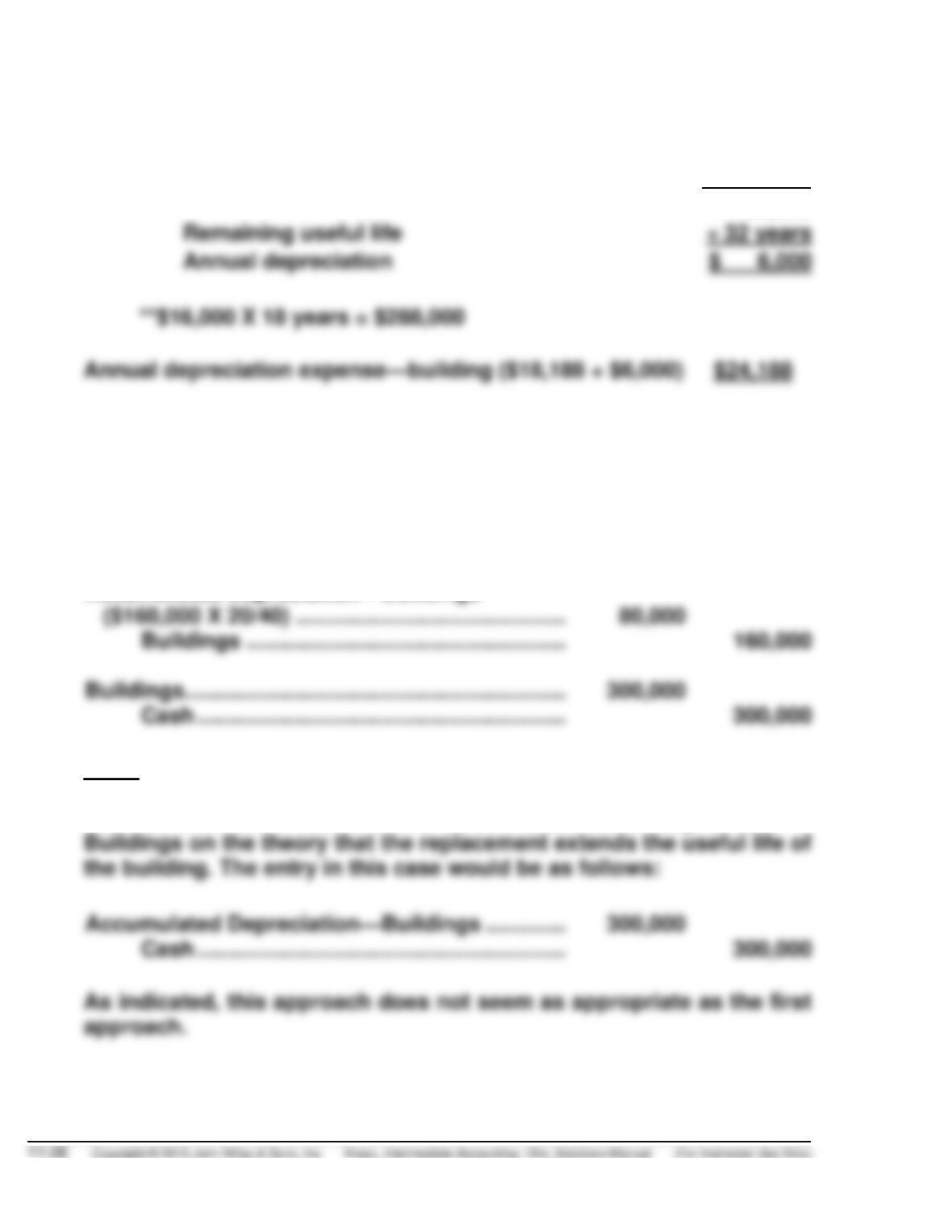

Remaining useful life

Annual depreciation

EXERCISE 11-13 (15–20 minutes)

(a) $2,200,000 ÷ 40 = $55,000

(b)

Loss on Disposal of Plant Assets …………………………..

80,000

Accumulated Depreciation—Buildings

Cash ……………………………………………………….

Note: The most appropriate entry would be to remove the old roof and

record a loss on disposal, because the cost of the old roof is given.

Another alternative would be to debit Accumulated Depreciation—

Cash ……………………………………………………….

EXERCISE 11-13 (Continued)

(c) No entry necessary.

(d) (Assume the cost of the old roof is removed)

Buildings ($2,200,000 – $160,000 + $300,000)

$2,340,000

Less: Accumulated Depreciation

($55,000 X 20 – $80,000)

1,020,000

1,320,000

Remaining useful life

÷ 25 years

(Assume the cost of the new roof is debited to

Accumulated Depreciation—Equipment)

Book value of the building prior to the replacement of

roof $2,200,000 – ($55,000 X 20) =

$1,100,000

Cost of new roof

$1,400,000

Remaining useful life

EXERCISE 11-14 (20–25 minutes)

(a)

Maintenance and Repairs Expense ………………………….

500

Equipment ……………………………………………………..

500

(b)

The proper ending balance in the asset account is:

January 1 balance

$134,750

Add: New equipment:

Purchases

Freight

700

Installation

Less: Cost of equipment sold

23,000

December 31 balance

EXERCISE 11-14 (Continued)

(2) Sum-of-the-years’-digits: 10 + 9 + 8 + 7 + 6 + 5 + 4 + 3 + 2 + 1 = 55

OR

n(n + 1)

=

10(11)

= 55

2

2

EXERCISE 11-15 (25–35 minutes)

(a)

2009

2010–2015

Incl.

2016

Total

(1)

$192,000 – $16,800 = $175,200

$175,200 ÷ 12 = $14,600

per yr. ($40 per day)

2010–2015 Include. (6 X $14,600)

68/365 of $14,600 =

$ 2,720

(2)

0

87,600

14,600

102,200

(3)

14,600

87,600

0

102,200

(4)

7,300

87,600

7,300

102,200

(5)

4/12 of $14,600

87,600

3/12 of $14,600

3,650

96,117

(6)

0

0

87,600

(b) The most accurate distribution of cost is given by methods 1 and 5 if

it is assumed that straight-line is satisfactory. Reasonable accuracy

EXERCISE 11-16 (10–15 minutes)

(a)

December 31, 2014

Loss on Impairment ………………………………………………..

3,200,000

Accumulated Depreciation—Equipment …………..

3,200,000

Cost

$9,000,000

Less: Accumulated depreciation

Carrying amount

Less: Fair value

Loss on impairment

(b)

December 31, 2015

Depreciation Expense ……………………………………………..

1,200,000

Accumulated Depreciation—Equipment …………..

1,200,000

New carrying amount

Useful life

Depreciation per year

(c) No entry necessary. Restoration of any impairment loss is not permitted.

EXERCISE 11-17 (15–20 minutes)

(a)

Loss on Impairment ………………………………………………..

3,220,000

Accumulated Depreciation—Equipment …………..

3,220,000

Cost

$9,000,000

Accumulated depreciation

1,000,000

Less: Fair value

Plus: Cost of disposal

EXERCISE 11-17 (Continued)

(b) No entry necessary. Depreciation is not taken on assets intended to

be sold.

Recovery of Loss from Impairment ………………….

500,000

Less: Cost of disposal

Less: Carrying amount

Recovery of loss on impairment

EXERCISE 11-18 (15–20 minutes)

(a)

December 31, 2014

Loss on Impairment ………………………………………………..

270,000

Accumulated Depreciation—Equipment …………..

270,000

Cost

Less: Accumulated depreciation

Less: Fair value

Loss on impairment

(b) It may be reported in the other expenses and losses section or it may

be highlighted as an unusual item in a separate section. It is not

reported as an extraordinary item.

(d) Management first had to determine whether there was an impairment.

To evaluate this step, management does a recoverability test. The

recoverability test estimates the future cash flows expected from use

EXERCISE 11-19 (15–20 minutes)

(a)

Depreciation Expense:

$84,000

= $2,800 per year

30 years

(b) Cost of Timber Sold: $9,000,000 – $1,800,000 = $7,200,000

$7,200,000 + $100,000 = $7,300,000

($7,300,000 ÷ 5,000,000 bd. ft.) X 900,000 bd. ft. = $1,314,000

EXERCISE 11-20 (10–15 minutes)

Cost per barrel of oil:

Initial payment =

$500,000

=

$2.00

250,000

Rental =

=

Premium = 5% of $55 =

Reconditioning of land =

=

.12

EXERCISE 11-21 (15–20 minutes)

(a) $1,300 – $300 = $1,000 per acre for timber

X 850,000 bd. ft. =

8,000 bd. ft. X 7,000 acres

X 850,000 bd. ft. = $106,250.

(c) Forda should capitalize the cost of $70,000 ($20 X 3,500 trees) and

adjust the depletion the next time the timber is harvested.

EXERCISE 11-22 (15–20 minutes)

Depletion base: $1,190,000 + $90,000 – $100,000 + $200,000 = $1,380,000

EXERCISE 11-23 (15–20 minutes)

(a)

$970,000 + $170,000 + $40,000* – $100,000

= .09 depletion per unit

12,000,000

EXERCISE 11-24 (15–25 minutes)

(a) Asset turnover:

$528.4

= .6159 times

$858 + $857.9

2

(a) Return on assets:

(c) The asset turnover times the profit margin on sales provides the rate

of return on assets computed for Tootsie Roll as follows:

*EXERCISE 11-25 (20–25 minutes)

2014

2015

(a)

Revenues

$200,000

$200,000

Operating expenses (excluding depreciation)

130,000

130,000

Depreciation [($27,000 – $6,000) ÷ 7]

3,000

3,000

Income before income taxes

2014

2015

(b)

Revenues

$200,000

$200,000

Operating expenses (excluding depreciation)

130,000

130,000

Depreciation*

5,400

8,640

Taxable income

(c) Book purposes ($27,000 – $6,000) $21,000

Tax purposes (entire cost of asset) $27,000

(d) Differences will occur for the following reasons:

*EXERCISE 11-26 (15–20 minutes)

(a) (1) ($31,000 – $1,000) X 1/10 X 10/12 = $2,500 depreciation expense

for book purposes.

*EXERCISE 11-26 (Continued)

(b) (1) $31,000 X 20% X 10/12 = $5,167 depreciation expense for book

purposes.

(c) Differences will occur for the following reasons:

1. half-year convention used for tax purposes.

TIME AND PURPOSE OF PROBLEMS

Problem 11-1 (Time 25–30 minutes)

Purpose—to provide the student with an opportunity to compute depreciation expense using a number

Problem 11-2 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to compute depreciation expense using the

Problem 11-3 (Time 40–50 minutes)

Purpose—to provide the student with an opportunity to compute depreciation expense using a number

Problem 11-4 (Time 45–60 minutes)

Purpose—to provide the student with an opportunity to correct the improper accounting for Semitrucks

and determine the proper depreciation expense. The student is required to compute separately the

errors arising in determining or entering depreciation or in recording transactions affecting Semitrucks.

Problem 11-5 (Time 25–30 minutes)

Purpose—to provide the student with a problem involving the computation of estimated depletion and

Problem 11-6 (Time 25–30 minutes)

Problem 11-7 (Time 25–35 minutes)

Purpose—to provide the student with a problem involving depletion and depreciation computations.

Problem 11-8 (Time 25–35 minutes)

Purpose—to provide the student with a comprehensive problem related to property, plant, and

equipment. The student must determine depreciable bases for assets, including capitalized interest,

and prepare depreciation entries using various methods of depreciation.

Problem 11-9 (Time 15–25 minutes)

Problem 11-10 (Time 45–60 minutes)

Purpose—to provide the student with an opportunity to solve a complex problem involving a number of

Time and Purpose of Problems (Continued)

Problem 11-11 (Time 30–35 minutes)

Purpose—to provide the student with the opportunity to solve a moderate problem involving a machinery

*Problem 11-12 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to compute depreciation expense using a number

of different depreciation methods. The purpose of computing the depreciation expense is to determine

SOLUTIONS TO PROBLEMS

PROBLEM 11-1

(a) 1. Depreciation Base Computation:

Purchase price………………………….

$85,000

Less: Purchase discount (2%) ……

1,700

Installation ……………………………….

3,800

Less: Salvage value …………………

2. Sum-of-the-years’-digits for 2015

Machine Year

Total

Depreciation

2014

2015

1

8/36 X $86,400 =

$19,200

$12,800*

$ 6,400**

2

7/36 X $86,400 =

$16,800

3. Double-declining-balance for 2014

($87,900 X 25% X 2/3) = $14,650

(b) An activity method.