EXERCISE 3-11 (20–25 minutes)

(a) ANDERSON COOPER CO.

Income Statement

For the Year Ended December 31, 2014

Revenues

Service revenue ………………………………………………

$11,590

Expenses

Salaries and wages expense …………………………..

Rent expense …………………………..……………………..

Depreciation expense ………………………………………

(b) ANDERSON COOPER CO.

Statement of Retained Earnings

For the Year Ended December 31, 2014

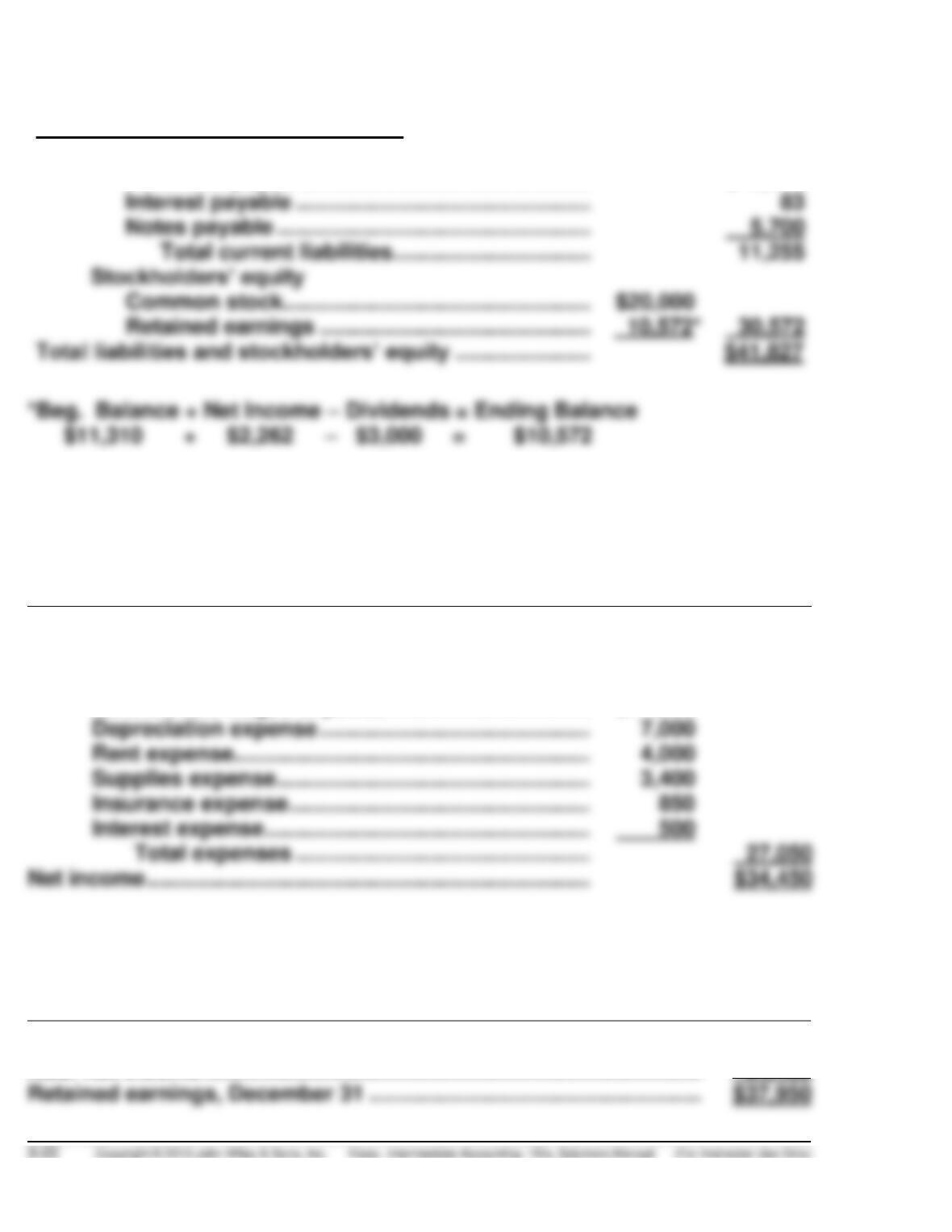

Retained earnings, January 1 …………………………………………………….

$11,310

Add: Net income ……………………………………………………………………….

(c) ANDERSON COOPER CO.

Balance Sheet

December 31, 2014

Assets

Current Assets

Cash ……………………………………………………….

$19,472

Accounts receivable …………………………………..

6,920

Prepaid rent ……………………………………………….

Total current assets ……………………………….

Property, plant, and equipment

Equipment ………………………………………………….

EXERCISE 3-11 (Continued)

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ………………………………………

$ 5,472

Interest payable …………………………………………

Notes payable ……………………………………………

Total current liabilities …………………………..

Common stock…………………………………………..

Retained earnings ……………………………………..

EXERCISE 3-12 (20–25 Minutes)

(a) SANTO DESIGN AGENCY

Income Statement

For the Year Ended December 31, 2014

Revenues

Service revenue ……………………………………………..

$61,500

Expenses

Salaries and wages expense …………………………...

$11,300

Depreciation expense ……………………………………..

Supplies expense ……………………………………………

Insurance expense ………………………………………….

Interest expense ……………………………………………..

Total expenses …………………………………………

SANTO DESIGN AGENCY

Statement of Retained Earnings

For the Year Ended December 31, 2014

Retained earnings, January 1 …………………………………………………….

$ 3,500

Add: Net income ……………………………………………………………………….

34,450

EXERCISE 3-12 (Continued)

(a) Continued SANTO DESIGN AGENCY

Balance Sheet

December 31, 2014

Assets

Cash ………………………………………………………………………..

$11,000

Accounts receivable …………………………………………………

21,500

Supplies …………………………………………………………………..

Prepaid insurance …………………………………………………….

$60,000

Less: Accumulated depreciation – equipment ………………..

Liabilities and Stockholders’ Equity

Liabilities

Notes payable ………………………………………………….

$ 5,000

Accounts payable …………………………………………….

5,000

Interest payable ……………………………………………….

150

Unearned service revenue ………………………………..

5,600

Salaries and wages payable ……………………………..

1,300

Total liabilities……………………………………………

Common stock ………………………………………………..

$10,000

Retained earnings …………………………..……………….

(b) (1) Based on interest payable at December 31, 2014, interest is $25 per

month or 0.5% of the note payable. 0.5% X 12 = 6% interest per year.

EXERCISE 3-13 (10–15 minutes)

(a)

Sales revenue ……………………………………………………….

$800,000

Less: Sales returns and allowances …………………………..

$24,000

Sales discounts ……………………………………………………….

Net sales ……………………………………………………….

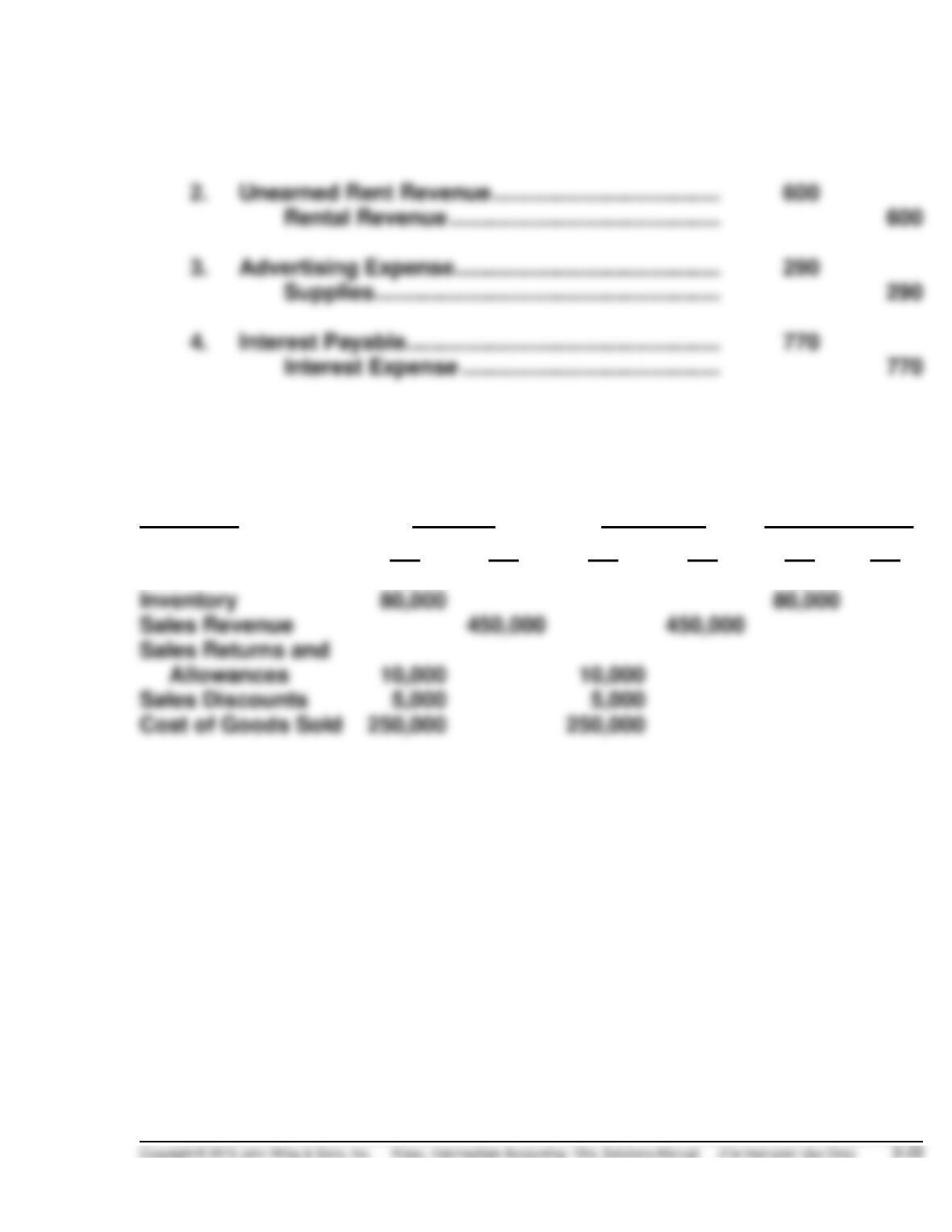

(b)

Sales ……………………………………………………………………………………

Income Summary ……………………………………………………….

Income Summary……………………………………………………….

Sales Returns and Allowances …………………………..

EXERCISE 3-14 (10–15 minutes)

Sales Revenue ……………………………………………………….

350,000

Sales Returns and Allowances …………………………..

13,000

Sales Discounts ……………………………………………………….

8,000

Income Summary ……………………………………………………….

Income Summary……………………………………………………….

Cost of Goods Sold ……………………………………………………….

Delivery Expense ……………………………………………………….

Insurance Expense ……………………………………………………….

Rent Expense ……………………………………………………….

20,000

Salaries and Wages Expense …………………………..

61,000

Income Summary……………………………………………………….

Retained Earnings ……………………………………………………….

21,000

EXERCISE 3-15 (10–15 minutes)

EXERCISE 3-16 (10–15 minutes)

Sales Revenue ……………………………………………………….

410,000

Cost of Goods Sold ……………………………………………………….

225,700

Sales Returns and Allowances …………………………..

12,000

Sales Discounts ……………………………………………………….

Selling Expenses ……………………………………………………….

Administrative Expenses ………………………………………………….

38,000

Income Tax Expense ……………………………………………………….

Income Summary ……………………………………………………….

(or)

Sales Revenue ……………………………………………………….

410,000

Income Summary ……………………………………………………….

410,000

Income Summary …………………………..…………………………..

336,700

Cost of Goods Sold ……………………………………………………….

Sales Returns and Allowances …………………………..

Sales Discounts ……………………………………………………….

Selling Expenses ……………………………………………………….

Administrative Expenses ………………………………………………….

Income Tax Expense ……………………………………………………….

Income Summary …………………………..…………………………..

Retained Earnings……………………………………………………….

Retained Earnings ……………………………………………………….

Dividends ……………………………………………………….

EXERCISE 3-17 (10–15 minutes)

J1

Date

Account Titles and Explanation

Ref.

Debit

Credit

Mar.

1

Cash

50,000

Common Stock

50,000

(Investment of cash in business)

3

Land

10,000

Buildings

22,000

Equipment

6,000

Cash

38,000

(Purchased Michelle Wie’s Golf Land)

5

Advertising Expense

1,600

Cash

1,600

(Paid for advertising)

6

Prepaid Insurance

1,480

Cash

1,480

(Paid for one-year insurance policy)

10

Equipment

2,500

Accounts Payable

2,500

(Purchased equipment on account)

18

Cash

1,200

Service Revenue

1,200

(Received cash for services performed)

25

Dividends

500

Cash

500

(Declared and paid a $500 cash dividend)

30

Salaries and Wages Expense

900

Cash

900

(Paid wages expense)

30

Accounts Payable

2,500

Cash

2,500

(Paid creditor on account)

31

Cash

750

Service Revenue

750

(Received cash for services performed)

*EXERCISE 3-18 (15–20 minutes)

Jill Accardo, M.D.

Conversion of Cash Basis to Accrual Basis

For the Year 2014

Excess of cash collected over cash disbursed ($142,600 –

$55,470)

$87,130

Alternate solution:

Jill Accardo, M.D.

Conversion of Income Statement Data

from Cash Basis to Accrual Basis

For the Year 2014

Cash

Adjustments

Accrual

Basis

Add

Deduct

Basis

Collections from customers:

$142,600

–Accounts receivable, Jan. 1

$9,250

+Accounts receivable, Dec. 31

$15,927

+Unearned service revenue, Jan. 1

–Unearned service revenue, Dec. 31

Disbursements for expenses:

–Accrued liabilities, Jan. 1

+Accrued liabilities, Dec. 31

+Prepaid expenses, Jan. 1

Operating expenses

Net income—cash basis

$ 87,130

Net income—accrual basis

*EXERCISE 3-19 (10–15 minutes)

(a) Wayne Rogers Corp.

Income Statement (Cash Basis)

For the Year Ended December 31,

2013

2014

Sales revenue

$295,000

$515,000

Net income

(b) Wayne Rogers Corp.

Income Statement (Accrual Basis)

For the Year Ended December 31,

2013

2014

Sales* revenue

Net income

*EXERCISE 3-20 (20–25 minutes)

(a)

Adjusting Entries:

1.

Insurance Expense ($5,280 X 5/24) …………………………..

1,100

Prepaid Insurance ……………………………………………………….

1,100

2.

Rent Revenue ($1,800 X 1/3) …………………………..

Unearned Rent Revenue …………………………..

3.

Supplies ……………………………………………………….

Advertising Expense ……………………………………………………….

4.

Interest Expense ……………………………………………………….

Interest Payable ……………………………………………………….

*EXERCISE 3-20 (Continued)

(b)

Reversing Entries:

1.

No reversing entry required.

2.

Unearned Rent Revenue ……………………………………………………….

Rental Revenue ……………………………………………………….

3.

Advertising Expense ……………………………………………………….

Supplies ……………………………………………………….

4.

Interest Payable ……………………………………………………….

Interest Expense …………………………..…………………………..

*EXERCISE 3-21 (10–15 minutes)

Accounts

Adjusted Trial

Balance

Income

Statement

Balance Sheet

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Cash

9,000

9,000

Inventory

Sales Returns and

Cost of Goods Sold

*EXERCISE 3-22 (20–25 minutes)

Ed Bradley Co.

Worksheet (partial)

For the Month Ended April 30, 2014

Adjusted Trial

Balance

Income

Statement

Balance Sheet

Account Titles

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

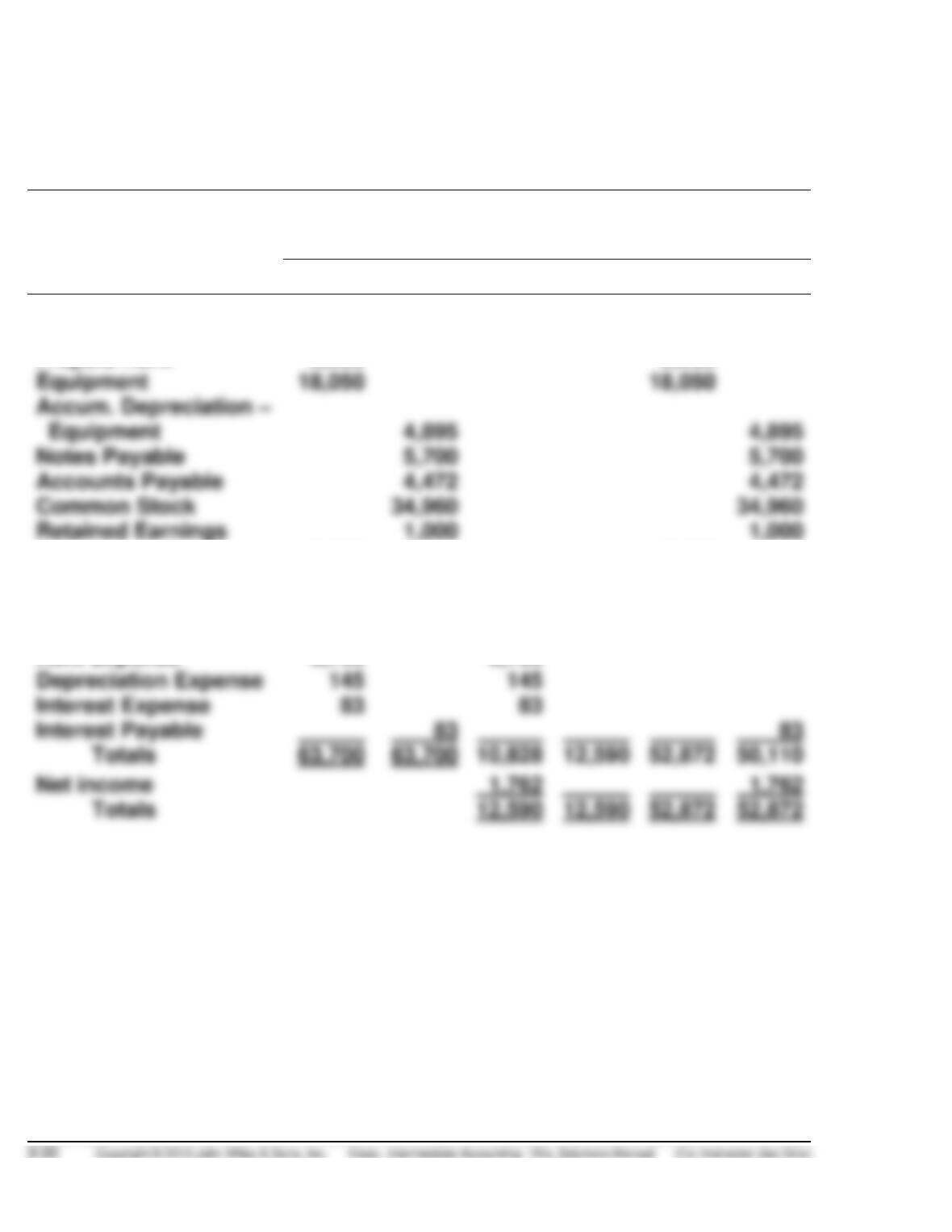

Cash

18,972

18,972

Accounts Receivable

6,920

6,920

Prepaid Rent

2,280

2,280

Notes Payable

5,700

Accounts Payable

Common Stock

34,960

34,960

Retained Earnings

1,000

Dividends

6,650

6,650

Service Revenue

12,590

12,590

Salaries and Wages

Expense

6,840

6,840

Rent Expense

3,760

3,760

Depreciation Expense

Interest Expense

Interest Payable

83

83

Net income

EXERCISE 3-22 (Continued)

Ed Bradley Co.

Balance Sheet

April 30, 2014

Assets

Current Assets

Cash ……………………………………………………….

$18,972

Accounts receivable ………………………………..

6,920

Prepaid rent …………………………………………….

Total current assets …………………………

Property, plant, and equipment

Equipment ………………………………………………

Liabilities and Stockholders’ Equity

Current liabilities

Notes payable …………………………………………

$ 5,700

Accounts payable ……………………………………

4,472

Interest payable ………………………………………

Total current liabilities …………………….

Common Stock ……………………………………….

Retained earnings …………………………..……….

*EXERCISE 3-23 (10–15 minutes)

Jurassic Park Co.

Worksheet (partial)

For Month Ended February 28, 2014

Trial

Balance

Adjustments

Adjusted

Trial Balance

Income

Statement

Balance

Sheet

Account Titles

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Supplies

1,756

(a)

1,041

715

715

(b)

7,196

Accumulated

depreciation –

The following accounts and amounts would be shown in the February

income statement:

Supplies expense $1,041

TIME AND PURPOSE OF PROBLEMS

Problem 3-1 (Time 25–35 minutes)

Purpose—to provide an opportunity for the student to post daily transactions to a “T” account ledger,

Problem 3-3 (Time 25–30 minutes)

Purpose—to provide an opportunity for the student to prepare adjusting entries. The adjusting entries

are fairly complex in nature.

Problem 3-4 (Time 40–50 minutes)

Problem 3-5 (Time 15–20 minutes)

Problem 3-6 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to prepare year-end adjusting entries from a trial

balance and related information presented. The problem also requires the student to prepare an

income statement, a balance sheet, and a statement of owners’ equity. The problem covers the basics

of the end-of-period adjusting process.

Problem 3-7 (Time 25–35 minutes)

Purpose—to provide an opportunity for the student to figure out the year-end adjusting entries that were

Problem 3-8 (Time 25–35 minutes)

Purpose—to provide an opportunity for the student to figure out the year-end adjusting entries that were

Problem 3-9 (Time 30–40 minutes)

Problem 3-10 (Time 30–35 minutes)

Purpose—to provide an opportunity for the student to prepare adjusting and closing entries from a trial

balance and related information. The student is also required to post the entries to “T” accounts.

Time and Purpose of Problems (Continued)

*Problem 3-11 (Time 35–40 minutes)

Purpose—to provide an opportunity for the student to prepare and compare (a) cash basis and accrual-

basis income statements, (b) cash-basis and accrual-basis balance sheets, and (c) to discuss the

weaknesses of cash basis accounting.

*Problem 3-12 (Time 40–50 minutes)

SOLUTIONS TO PROBLEMS

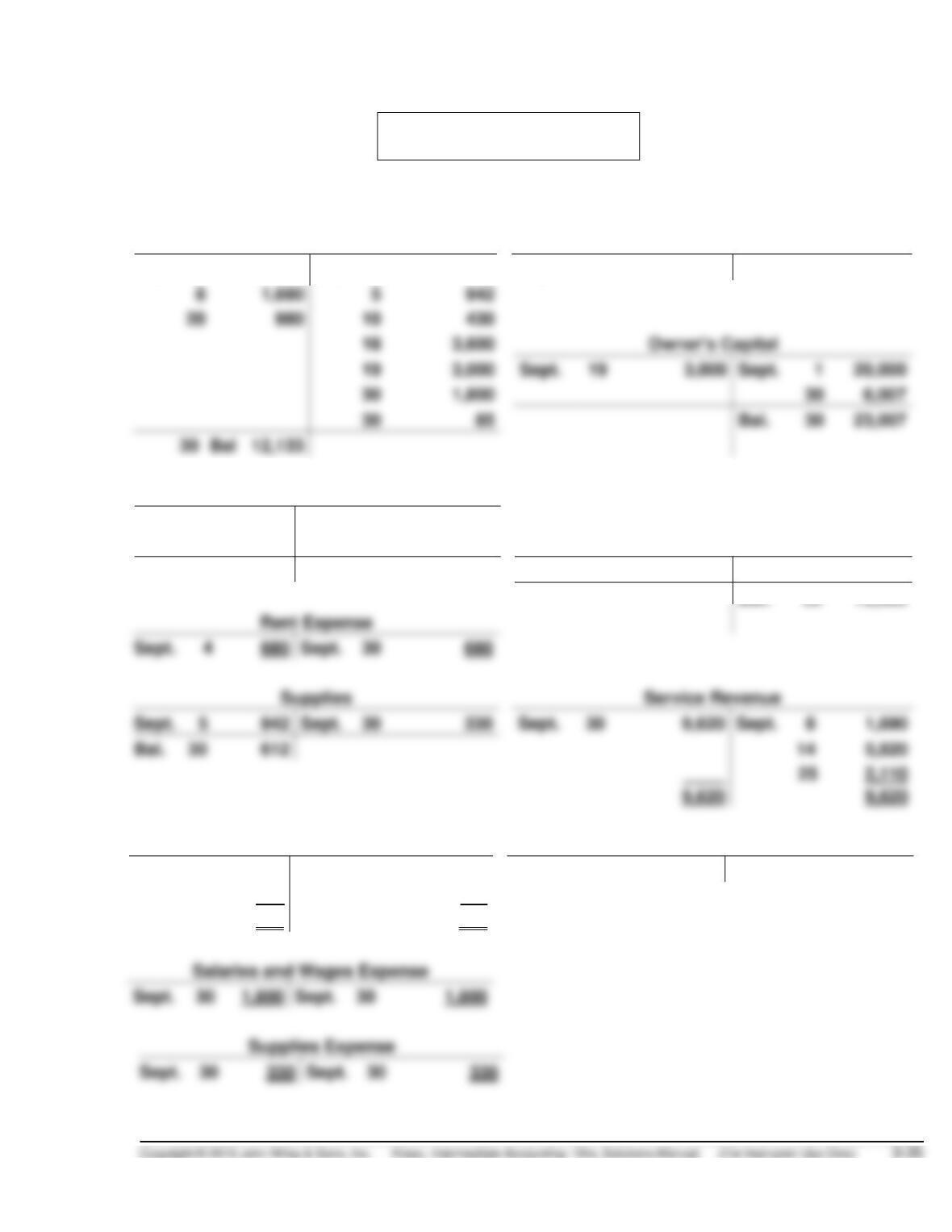

PROBLEM 3-1

(a) (Explanations are omitted.) and (d)

Cash

Equipment

Sept.

1

20,000

Sept.

4

680

Sept.

2

17,280

5

10

18

19

Sept.

19

Sept.

1

30

30

6,007

30

Bal.

30

30

Bal

12,133

Accounts Receivable

Sept.

14

5,820

Sept.

20

980

25

2,110

Accounts Payable

Bal.

30

6,950

Sept.

18

3,600

Sept.

2

17,280

Bal.

30

13,680

Rent Expense

Sept.

30

Sept.

5

942

Sept.

30

330

Sept.

30

9,620

Sept.

1,690

Bal.

30

25

2,110

Office Expense

Accumulated Depreciation—Equipment

Sept.

10

430

Sept.

30

515

Sept.

30

288

30

85

515

515

Salaries and Wages Expense

Sept.

1,800

Sept.

30

PROBLEM 3-1 (Continued)

Depreciation Expense

Income Summary

Sept.

30

288

Sept.

30

288

Sept.

30

680

Sept.

30

9,620

30

515

30

330

30

288

(b) YASUNARI KAWABATA, D.D.S.

Trial Balance

September 30

Debit

Credit

Cash …………………………………………………………………………….

$12,133

Accounts Receivable …………………………………………………….

6,950

Supplies ……………………………………………………………………….

612

Equipment ……………………………………………………….

17,280

Accumulated Depreciation—Equipment …………………………

Accounts Payable ……………………………………………………….

Service Revenue ……………………………………………………….

Rent Expense …………………………..…………………………..

680

Office Expense ……………………………………………………….

Salaries and Wages Expense …………………………………………

1,800

Supplies Expense …………………………..…………………………..

330

Depreciation Expense ……………………………………………………

PROBLEM 3-1 (Continued)

(c) YASUNARI KAWABATA, D.D.S.

Income Statement

For the Month of September

Service revenue …………………………..…………………………..

$9,620

Expenses:

Salaries and wages expense…………………………

$1,800

Rent expense ………………………………………………

Supplies expense ………………………………………..

Depreciation expense …………………………..

Office expense …………………………………………….

Total expenses…………………………………………

YASUNARI KAWABATA, D.D.S.

Statement of Owners’ Equity

For the Month of September

Owner’s capital September 1 ……………………………………………..

$20,000

Add: Net income ……………………………………………………………..

Less: Withdrawal by owner ……………………………………………….

YASUNARI KAWABATA, D.D.S.

Balance Sheet

As of September 30

Assets

Liabilities and Owners’ Equity

Cash …………………………..

$12,133

Accounts payable ………………..

$13,680

Accounts receivable ……….

Supplies …………………………

Equipment. …………………….

PROBLEM 3-1 (Continued)

(d) YASUNARI KAWABATA, D.D.S.

Post-Closing Trial Balance

September 30

Debit

Credit

Cash …………………………..…………………………..

$12,133

Accounts Receivable ………………………………………

6,950

Accumulated Depreciation—Equipment …………..

PROBLEM 3-2

(a)

Dec. 31

Accounts Receivable ……………………………………………………….

3,500

Service Revenue ……………………………………………………….

3,500

31

Unearned Service Revenue …………………………..

1,400

Service Revenue ……………………………………………………….

1,400

31

Supplies Expense ……………………………………………………….

5,400

5,400

31

Depreciation Expense ……………………………………………………….

5,000

Accumulated Depreciation—

Equipment ……………………………………………………….

5,000

31

Interest Expense ……………………………………………………….

Interest Payable ……………………………………………………….

31

Insurance Expense ……………………………………………………….

Prepaid Insurance ……………………………………………………….

31

Salaries and Wages Expense …………………………..

1,300

Salaries and Wages Payable …………………………..

(b) MASON ADVERTISING AGENCY

Income Statement

For the Year Ended December 31, 2014

Revenues

Service revenue …………………………..………………….

$63,500

Expenses

Salaries and wages expense …………………………..

$11,300

Depreciation expense …………………………..

Rent expense ………………………………………………….

Insurance expense …………………………..

Interest expense ……………………………………………..

500

Total expenses…………………………..

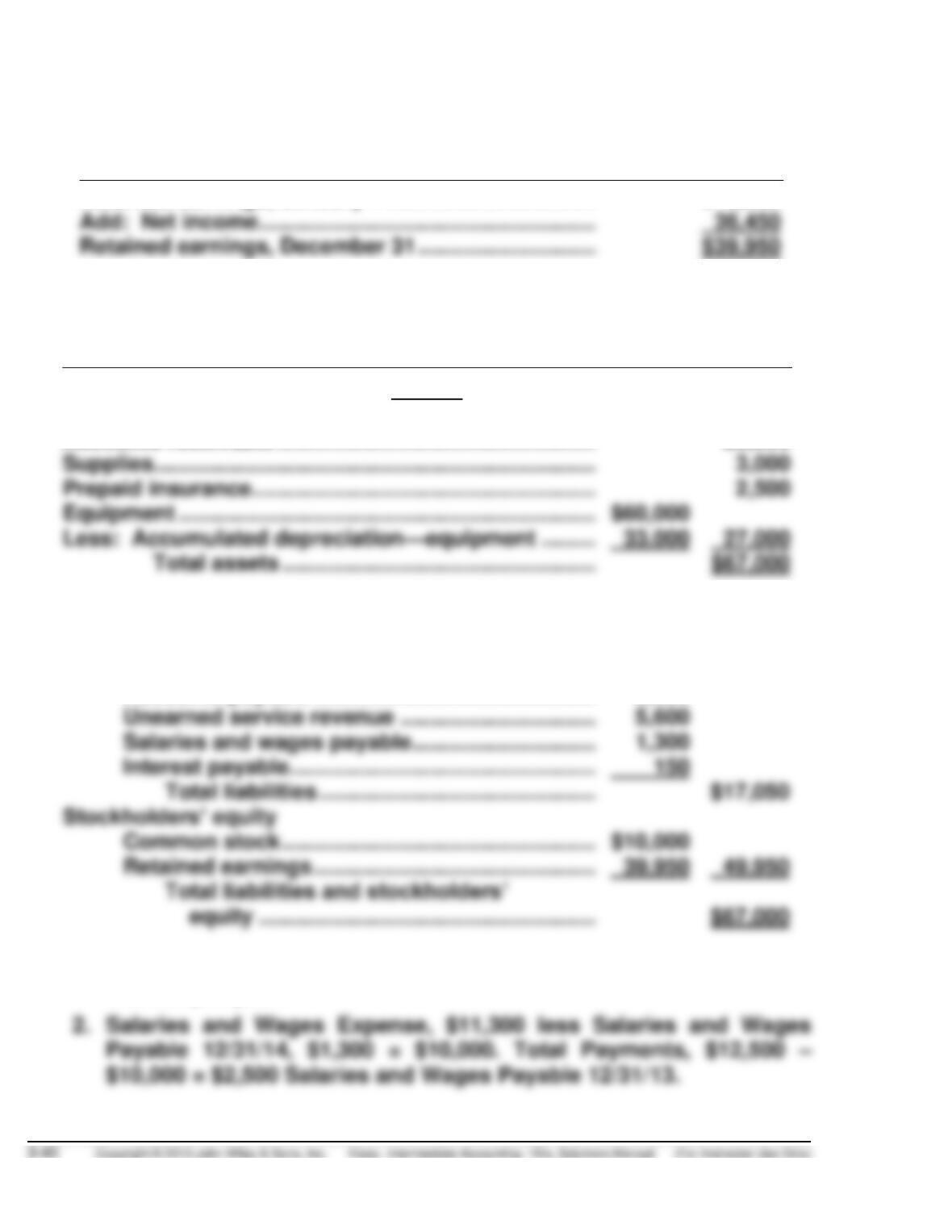

PROBLEM 3-2 (Continued)

MASON ADVERTISING AGENCY

Statement of Retained Earnings

For the Year Ended December 31, 2014

Retained earnings, January 1 ……………………………………………………

$ 3,500

Add: Net income……………………………………………………….

MASON ADVERTISING AGENCY

Balance Sheet

December 31, 2014

Assets

Cash ………………………………………………………………………..

$11,000

Accounts receivable …………………………………………………

23,500

Supplies …………………………………………………………………..

Prepaid insurance …………………………………………………….

Equipment ……………………………………………………………….

$60,000

Less: Accumulated depreciation—equipment …………..

Liabilities and Stockholders’ Equity

Liabilities

Notes payable………………………………………………….

$ 5,000

Accounts payable ……………………………………………

5,000

Unearned service revenue …………………………..

5,600

Salaries and wages payable …………………………..

1,300

Interest payable ……………………………………………….

Total liabilities …………………………………………..

Common stock …………………………..……………………

Retained earnings ……………………………………………

(c) 1. Interest is $50 per month or 1% of the note payable. 1% X 12 = 12%

interest per year.