PROBLEM 19-5B (Continued)

(c) 2014 Income Statement

Operating loss before income taxes …………… $(140,000)

(d) 2016 Income Statement

Income before income taxes ………………………. $60,000

Income tax expense

Current ………………………………………………. $ 1,500a

Deferred …………………………………………….. 16,500 18,000

Net income ……………………………………………….. $42,000

PROBLEM 19-6B

1.

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

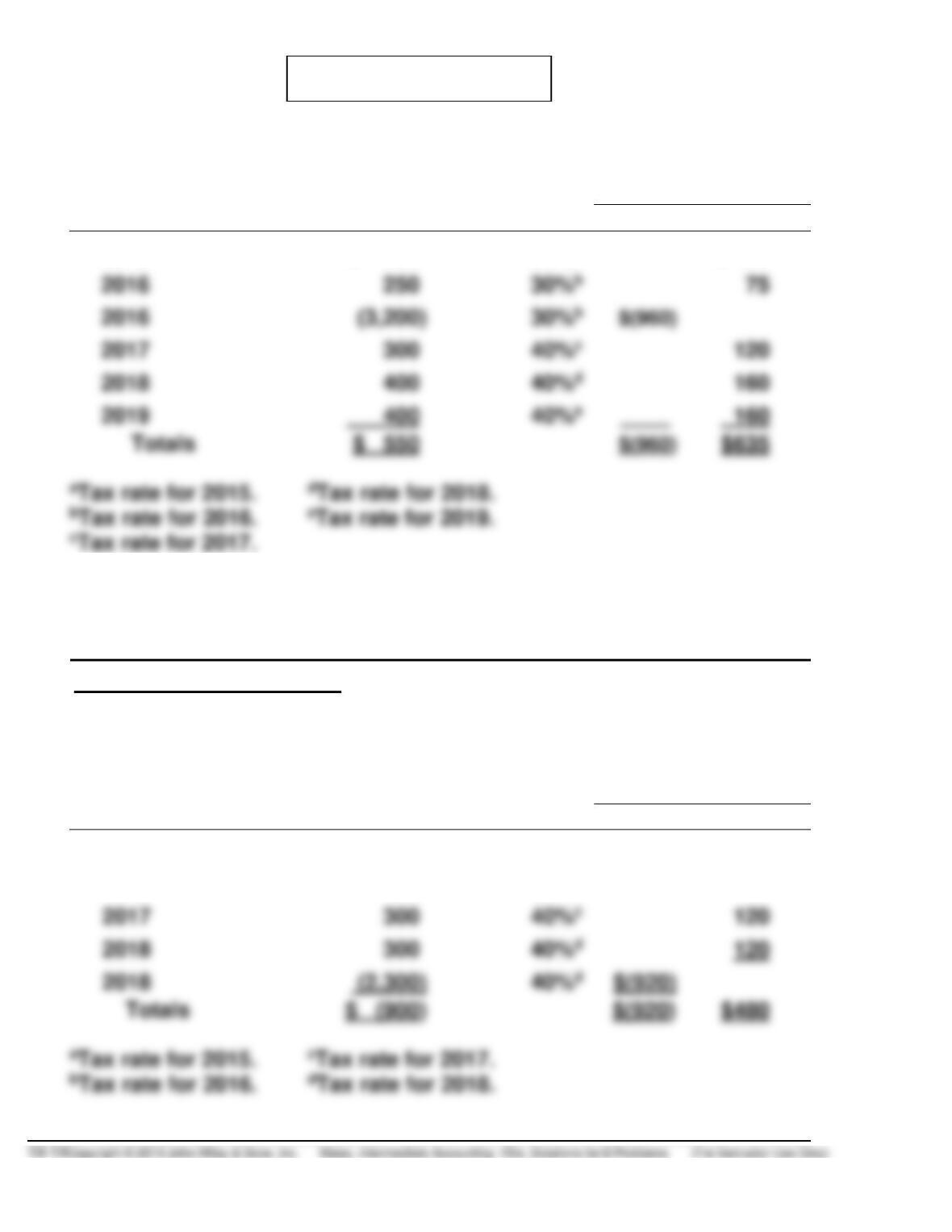

2015

$ 400

30%a

$ 120

2016

30%b

2016

30%b

2017

40%c

120

2019

400

40%e

GLIDING CO.

Balance Sheet

December 31, 2014

Other assets (noncurrent)

Deferred tax asset ($960 – $635) ………………………………… $325

2.

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

2015

$ 400

30%a

$ 120

2016

400

30%b

120

2017

40%c

120

2018

120

2018

40%d

PROBLEM 19-6B (Continued)

BOOTHILL CO.

Balance Sheet

December 31, 2014

PROBLEM 19-7B

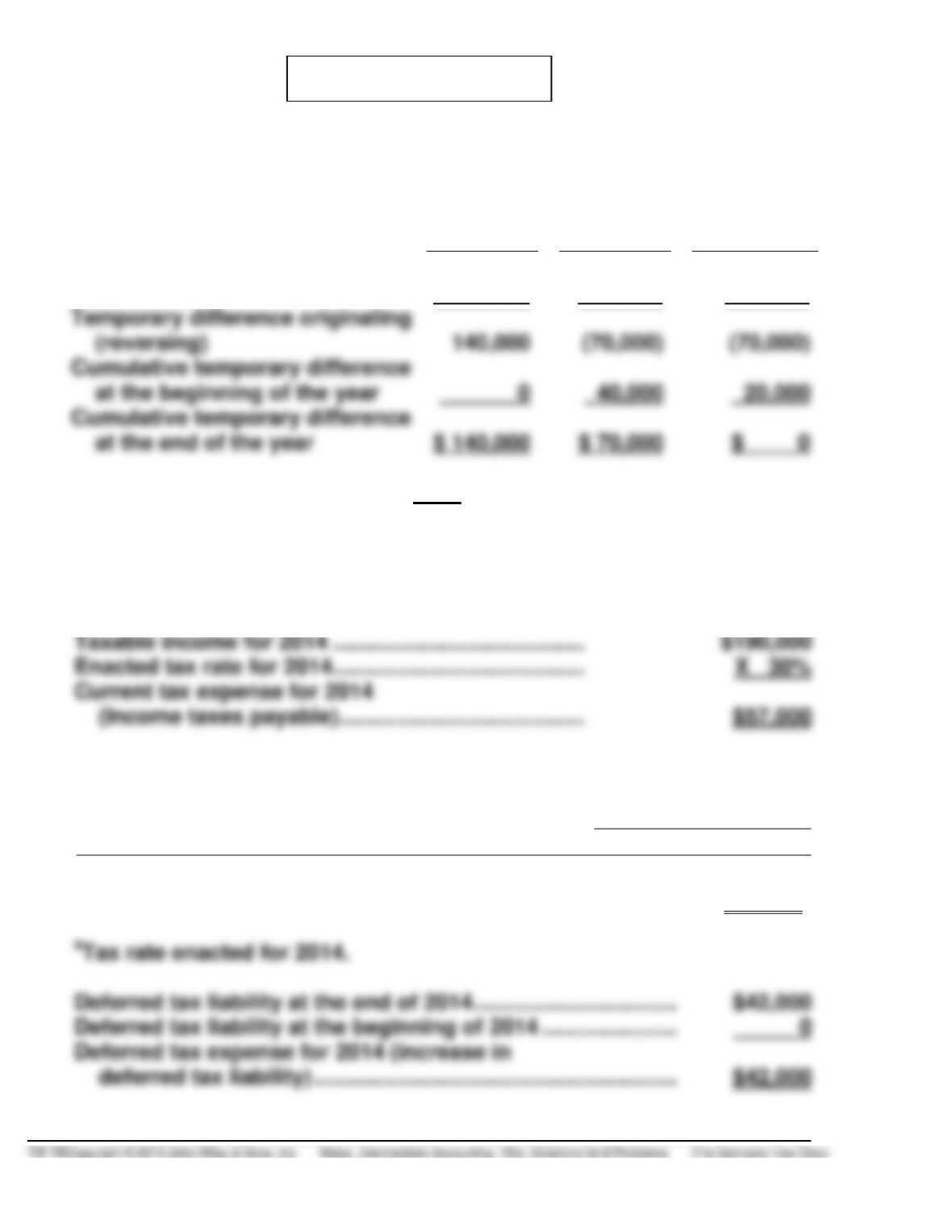

(a) Before deferred taxes can be computed, the amount of cumulative tem-

porary difference existing at the end of each year must be computed:

2014

2015

2016

Pretax financial income

$330,000

($120,000

($120,000

Taxable income

190,000

190,000

( 190,000

$ 70,000

2014

Income Tax Expense ……………………………………….. 99,000

Income Taxes Payable ………………………………. 57,000

Deferred Tax Liability ………………………………… 42,000

Temporary

Difference

Future Taxable

(Deductible)

Amounts

Tax

Rate

December 31, 2015

Deferred Tax

(Asset)

Liability

Installment Accounts

Receivable

(

$ 140,000

30%a

$42,000

PROBLEM 19-7B (Continued)

Deferred tax expense for 2014 ……………………………………….. $42,000

Current tax expense for 2014 (Income taxes payable) ……… 57,000

Income tax expense for 2014 …………………………………………. $99,000

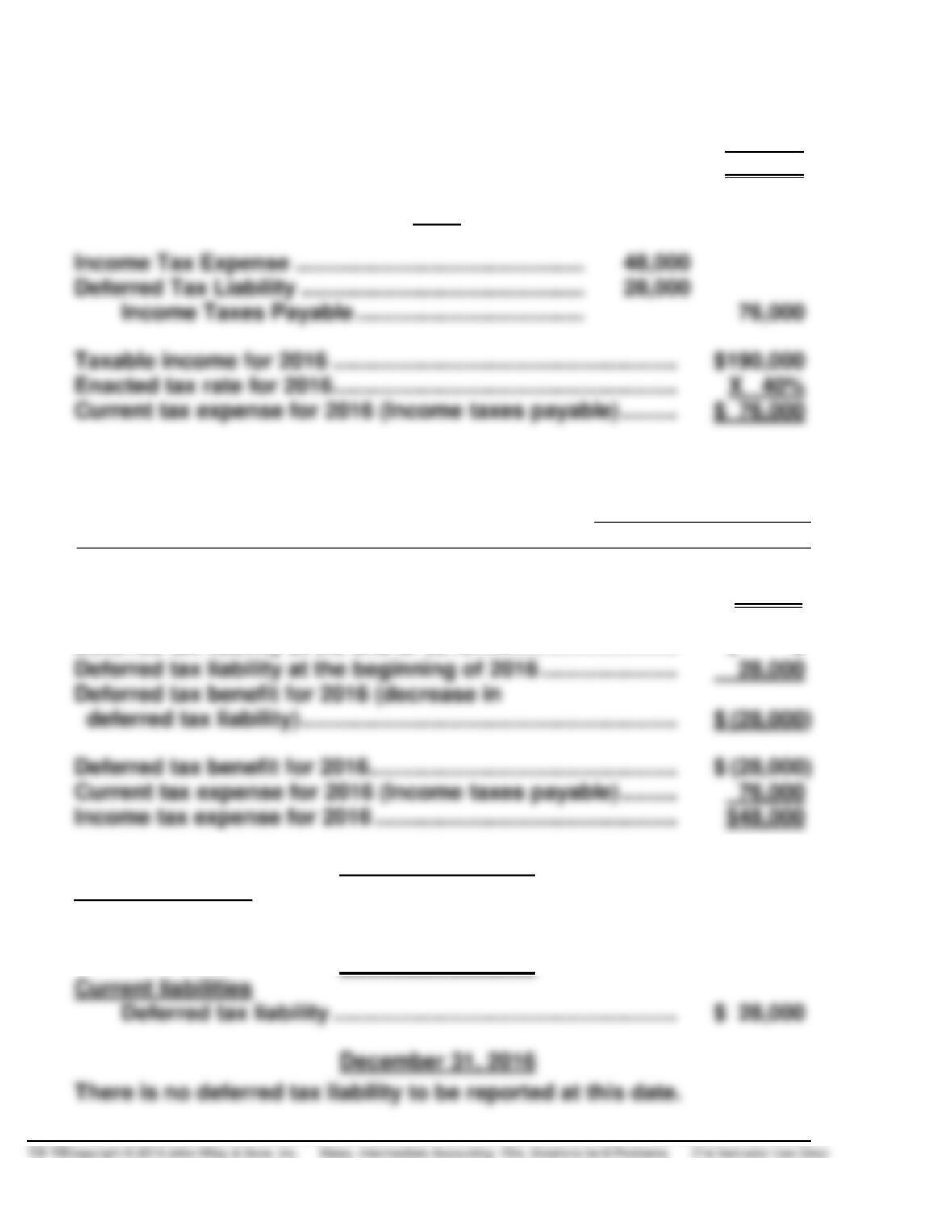

2015

Income Tax Expense ……………………………………….. 14,000

Deferred Tax Liability ………………………………… 14,000*

*Cumulative temporary difference at the end of 2014 ………… $140,000

Newly enacted tax rate for future year ……………………………. X 40%

Adjusted balance of deferred tax liability at the end

of 2014 ……………………………………………………………………… 56,000

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

December 31, 2015

Deferred Tax

(Asset)

Liability

Installment Accounts

Receivable

$70,000

40%b

$28,000

bTax rate enacted for 2015.

PROBLEM 19-7B (Continued)

Deferred tax benefit for 2015 ………………………………………….. $(28,000)

Current tax expense for 2015 (Income taxes payable) ……… 76,000

Income tax expense for 2015 …………………………………………. $48,000

2016

Temporary

Difference

Future Taxable

(Deductible)

Amounts

Tax

Rate

December 31, 2016

Deferred Tax

(Asset)

Liability

Installment Accounts

Receivable

(

$—0—

40%

$—0—

Deferred tax liability at the end of 2016 …………………………... $ 0

(b) December 31, 2014

Current liabilities

Deferred tax liability ……………………………………………….. $42,000

December 31, 2015

PROBLEM 19-7B (Continued)

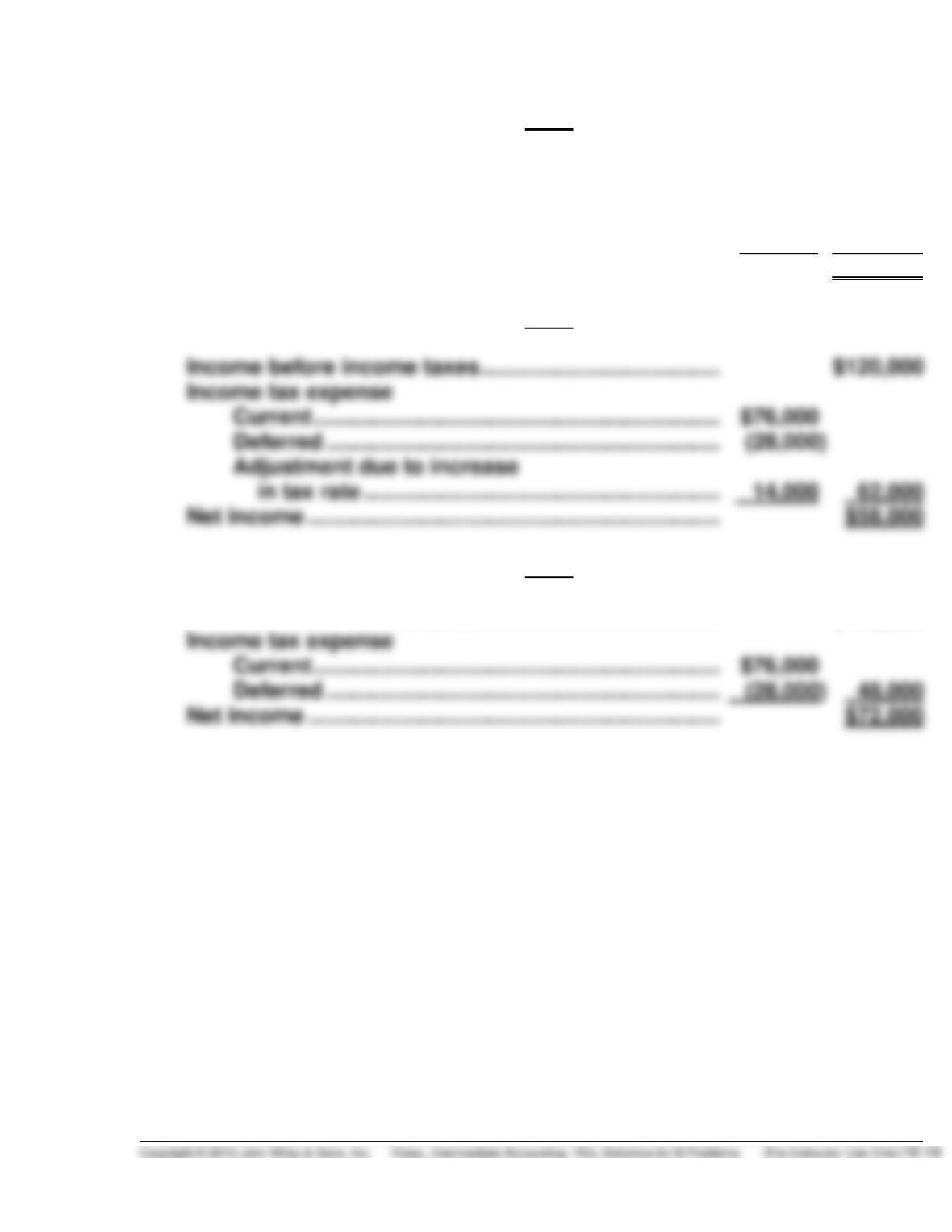

(c) 2014

Income before income taxes ………………………………… $330,000

Income tax expense

Current ………………………………………………………… $57,000

Deferred ………………………………………………………. 42,000 99,000

Net income …………………………………………………………. $231,000

2015

2016

Income before income taxes ………………………………… $120,000

PROBLEM 19-8B

(a)

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

$(32,000)*

30%

$(9,600)

(b) Income Tax Expense …………………………………….. 71,400

Deferred Tax Asset ……………………………………….. 9,600

Income Taxes Payable ……………………………. 81,000

$81,000 taxes due for 2014 ÷ 30% 2014 tax rate = $270,000 taxable

income for 2014.

(c) Income before income taxes ………………………….. $238,000a

Income tax expense

Current ………………………………………………….. $81,000

Deferred ………………………………………………… (9,600) 71,400

PROBLEM 19-8 (Continued)

Book Depreciation

Tax Depreciation

bDifference

2014

$64,000

$ 32,000*

($ 32,000

2015

64,000

64,000

0

2016

2017

2018

2019

( (32,000)

($ 0

(d)

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

$ (32,000)

30%

$(9,600)

(60,000)

Temporary

Difference

Resulting Deferred Tax

Related Balance

Sheet Account

Classification

(Asset)

Liability

Depreciation

$(9,600)

Plant Assets

Noncurrent

Unearned Rent

Current

Unearned rent

Noncurrent

Current assets

Deferred tax asset …………………………..……………………… $18,000

PROBLEM 19-8B (Continued)

(e) Income Tax Expense ……………………………………… 60,000

Deferred Tax Asset ………………………………………… 36,000

Income Taxes Payable …………………………….. 96,000

Deferred tax asset at the end of 2015 ……………………………… $ 45,600

Deferred tax asset at the beginning of 2015 ……………………. 9,600

Deferred tax benefit for 2015 (increase in

deferred tax asset) …………………………………………………….. $ (36,000)

(f) Income before income taxes ……………………………. $200,000d

Income tax expense

Current ……………………………………………………. $96,000

Deferred ………………………………………………….. (36,000) 60,000

Net income …………………………………………………….. $140,000

PROBLEM 19-9B

(a) Pretax financial income …………………………………………………. $250,000

Permanent differences:

Fine for pollution ……………………………………………………. 4,000

Taxable income …………………………………………………………….. $169,000

(b)

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Warranty costs

$ (16,000)

35%

$(5,600)

Construction profits

35%

Depreciation

35%

Totals

$(5,600)

(c) Income Tax Expense ……………………………………….. 88,200

Deferred Tax Asset …………………………..……………… 5,600

Deferred Tax Liability ………………………………… 34,650

Income Taxes Payable ………………………………. 59,150

PROBLEM 19-9B (Continued)

Deferred tax asset at the end of 2015 ……………………………… $ 5,600

Deferred tax asset at the beginning of 2015 ……………………. 0

Deferred tax benefit for 2015 ………………………………………….. $ (5,600)