CA 4-7

(a) Separate Statement

Current Year

Prior Year

. . . income components . . .

Net income ………………………………………………………………….

$400,000

$410,000

Comprehensive Income Statement

Net income ………………………………………………………………….

Unrealized gains …………………………………………………………..

15,000

(b) Combined Format

. . . income components . . .

Net income …………………………………………………………………..

$400,000

$410,000

Other comprehensive income

Unrealized gains ……………………………………………………………

15,000

FINANCIAL REPORTING PROBLEM

(a) P&G uses the multiple-step income statement because it separates

operating from nonoperating activities. A multiple-step income statement

(b) P&G operates in the consumer products market. The company separates

its operations into six global segments: (sales by segment)

Fabric and Home Care, 30%

(c) P&G’s gross profit (Net Sales – Cost of Products Sold) was $41,791 million

(d) P&G probably makes a distinction between operating and nonoperating

revenue for the reasons mentioned in the solution to Part (a). By

separating out these revenue and expense items, the statement reader

can see the separate impacts of operating and financing activities.

COMPARATIVE ANALYSIS CASE

(a) Both companies are using the multiple-step format in presenting

income statement information. Companies use the multiple-step in–

come statement to recognize additional relationships related to revenues

(b) The gross profit, operating profit, and net income for these two companies

are as follows:

PepsiCo

2011

2010

2009

% Change

Net revenue ……………….

$66,504

$57,838

$43,232

53.83%

Net income …………………

Gross profit …………….

42.33%

As shown in the table above, however, Coca-Cola had greater growth

in net income from 2009 to 2011. PepsiCo reported stronger growth in

net sales over the three-year period. Both companies are doing well.

COMPARATIVE ANALYSIS CASE (Continued)

(c) Coca-Cola has reported gains on the equity transactions related to

bottling operations. PepsiCo reported gains on its equity investments.

PepsiCo provided the following disclosure for Items Affecting

Comparability:

ITEMS AFFECTING COMPARABILITY

The year-over-year comparisons of our financial results are affected

by the following items:

53rd Week

Inventory Fair Value Adjustments

In 2011, we recorded $46 million ($28 million after–tax or $0.02 per share) of

incremental costs in cost of sales related to fair value adjustments to the

Venezuela Currency Devaluation

As of the beginning of our 2010 fiscal year, we recorded a one– time $120 million

net charge related to our change to hyperinflationary accounting for our

COMPARATIVE ANALYSIS CASE (Continued)

Asset Write– Off

In 2010, we recorded a $145 million charge ($92 million after– tax or

$0.06 per share) related to a change in scope of one release in our

Foundation Contribution

In 2010, we made a $100 million ($64 million after– tax or $0.04 per share)

contribution to The PepsiCo Foundation, Inc., in order to fund charitable

and social programs over the next several years. This contribution

was recorded in corporate unallocated expenses.

Debt Repurchase

In 2010, we paid $672 million in a cash tender offer to repurchase $500 million

Non–GAAP Measures

Certain measures contained in this Annual Report are financial measures that

are adjusted for items affecting comparability (see “Items Affecting

Comparability” for a detailed list and description of each of these items), as

well as, in certain instances, adjusted for foreign currency. These measures

COMPARATIVE ANALYSIS CASE (Continued)

our ongoing performance and with how management evaluates our

operational results and trends. These measures are not, and should

not be viewed as, a substitute for U.S. GAAP reporting measures.

In the discussions of net revenue and operating profit below, effective

Servings

Since our divisions each use different measures of physical unit volume

(i.e., kilos, gallons, pounds and case sales), a common servings metric is

necessary to reflect our consolidated physical unit volume. Our

FINANCIAL STATEMENT ANALYSIS CASE 1

(a) Depending on the company chosen, student answers will vary. Given

the ready availability, the analysis for Walgreens is provided below:

Z-Score Analysis

Walgreens ($ 000,000)

2011

2010

Total Assets

$27,454

$26,275

Current Assets

$12,322

$11,922

Current Liabilities

$ 8,083

$ 7,433

Working Capital

$ 4,239

Working Capital/Assets

0.154

0.171

0.1853

Retained Earnings

$18,877

$16,848

Retained Earnings/Assets

0.688

0.641

0.9626

EBIT/Assets

0.159

0.132

0.525

0.434

Sales

$67,420

Z-Score

Z-Score

Sales/Assets

2.629

2.566

0.99

2.603

2.540

MV Equity

$31,880

$26,159

Total Liabilities

$12,607

$11,875

Liabilities

2.529

2.203

1.517

1.323

Market Price (8/31/11)

35.21

26.88

Z-Score

5.793

905.42

Total Equity

$14,847

$14,400

FINANCIAL STATEMENT ANALYSIS CASE 1 (Continued)

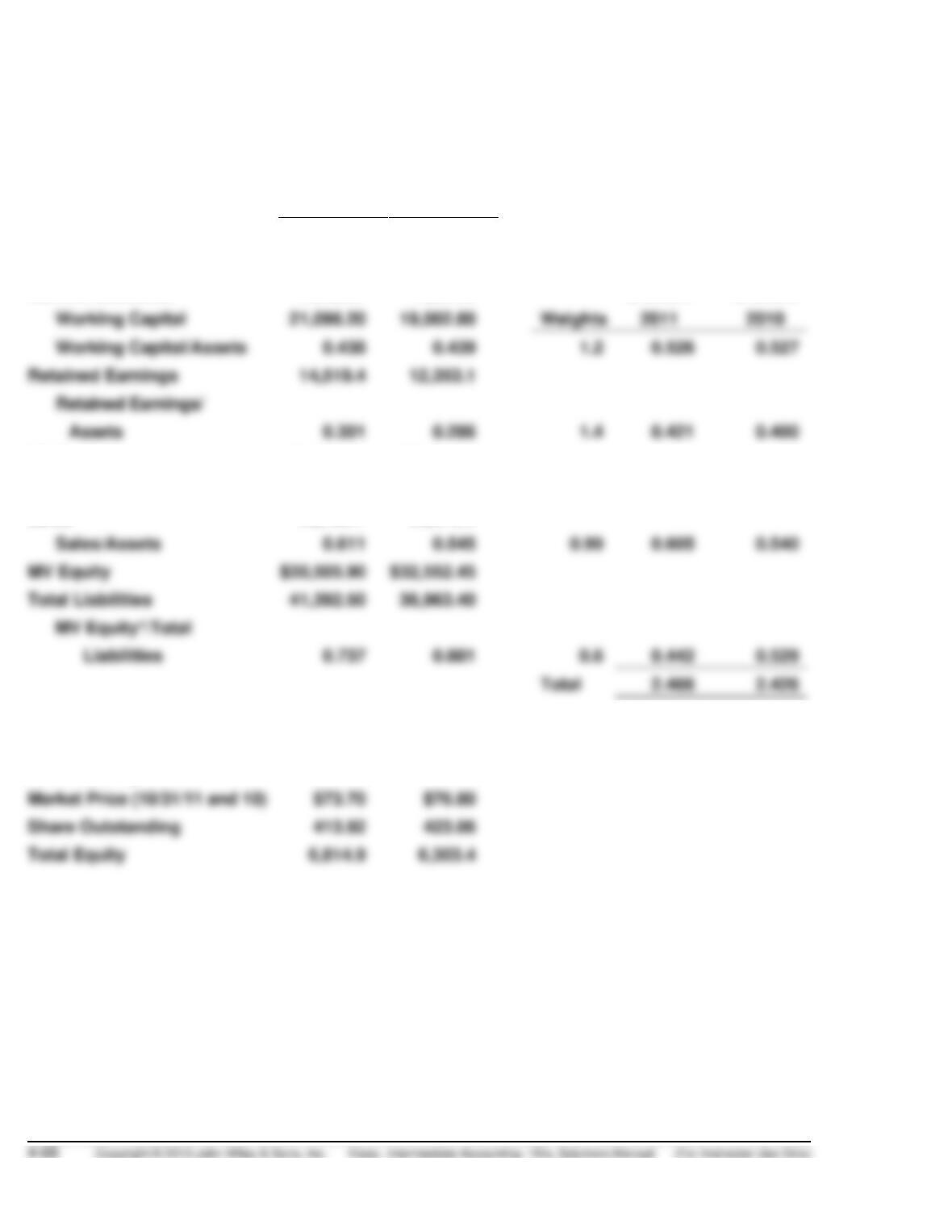

Deere & Co. ($ 000,000)

Oct. 31,

2011

Oct. 31,

2010

Total Assets

48,207.4

43,266.8

Current Assets

38,816.7

33,366.8

Current Liabilities

17,720.5

14,364.0

2011

Working Capital

21,096.20

19,002.80

Weights

Working Capital/Assets

0.438

0.439

1.2

0.527

Retained Earnings

14,519.4

12,353.1

Retained Earnings/

Assets

1.4

0.421

0.400

Z-Score

Z-Score

EBIT

$6,904.80

$5,661.90

EBIT/Assets

0.143

0.131

3.3

0.472

0.432

Sales

29,466.1

23,573.2

Sales/Assets

0.611

0.545

MV Equity

Total Liabilities

41,392.50

36,963.40

Total

2.426

*Market price X Shares

Outstanding

Market Price (10/31/11 and 10)

Share Outstanding

Total Equity

FINANCIAL STATEMENT ANALYSIS CASE 1 (Continued)

(b) Walgreens’ Z-score in 2011 has increased but is still well above the

cutoff score for companies that are unlikely to fail. The company has

improved on just about all components of the Z-score.

FINANCIAL STATEMENT ANALYSIS CASE 2

Earnings (loss) per common share

Earnings from continuing operations

($97,700,000 ÷ 177,636,000) ……………………………………….

$0.55

Discontinued operations………………………………………………….

Extraordinary items ……………………………………………………….

FINANCIAL STATEMENT ANALYSIS CASE 3

(a) Assumptions and estimates related to items such as bad debt expense,

warranties, or the useful lives or residual values for fixed assets could

result in income being overstated.

(b) See the table below.