PROBLEM 8-3 (Continued)

8/15

Purchases ………………………………………………………

15,840

Accounts Payable ($16,000 X .99) …………….

15,840

8/25

Purchases ………………………………………………………

Accounts Payable ($20,000 X .98) …………….

19,600

Accounts Payable …………………………………………..

15,840

Purchase Discounts Lost ………………………………..

Cash ………………………………………………………

2.

8/31

Purchase Discounts Lost ………………………………..

216

Accounts Payable

(.02 X [$12,000 – $1,200]) ………………………

216

3.

Same as part (a) (2) except:

PROBLEM 8-4

(a)

Purchases

Total Units

Sales

Total Units

April 1 (balance on hand)

100

April 5

300

April 4

400

April 12

200

April 11

300

April 27

800

April 18

200

April 28

April 30

Total units

Total units sold

Assuming costs are not computed for each withdrawal:

1. First-in, first-out.

Date of Invoice

No. Units

Unit Cost

Total Cost

2. Last-in, first-out.

Date of Invoice

No. Units

Unit Cost

Total Cost

PROBLEM 8-4 (Continued)

3. Average-cost.

Cost of Part X available.

Date of Invoice

No. Units

Unit Cost

Total Cost

April 1

100

$5.00

$ 500

April 4

400

April 26

600

(b) Assuming costs are computed for each withdrawal:

1. First-in, first out.

PROBLEM 8-4 (Continued)

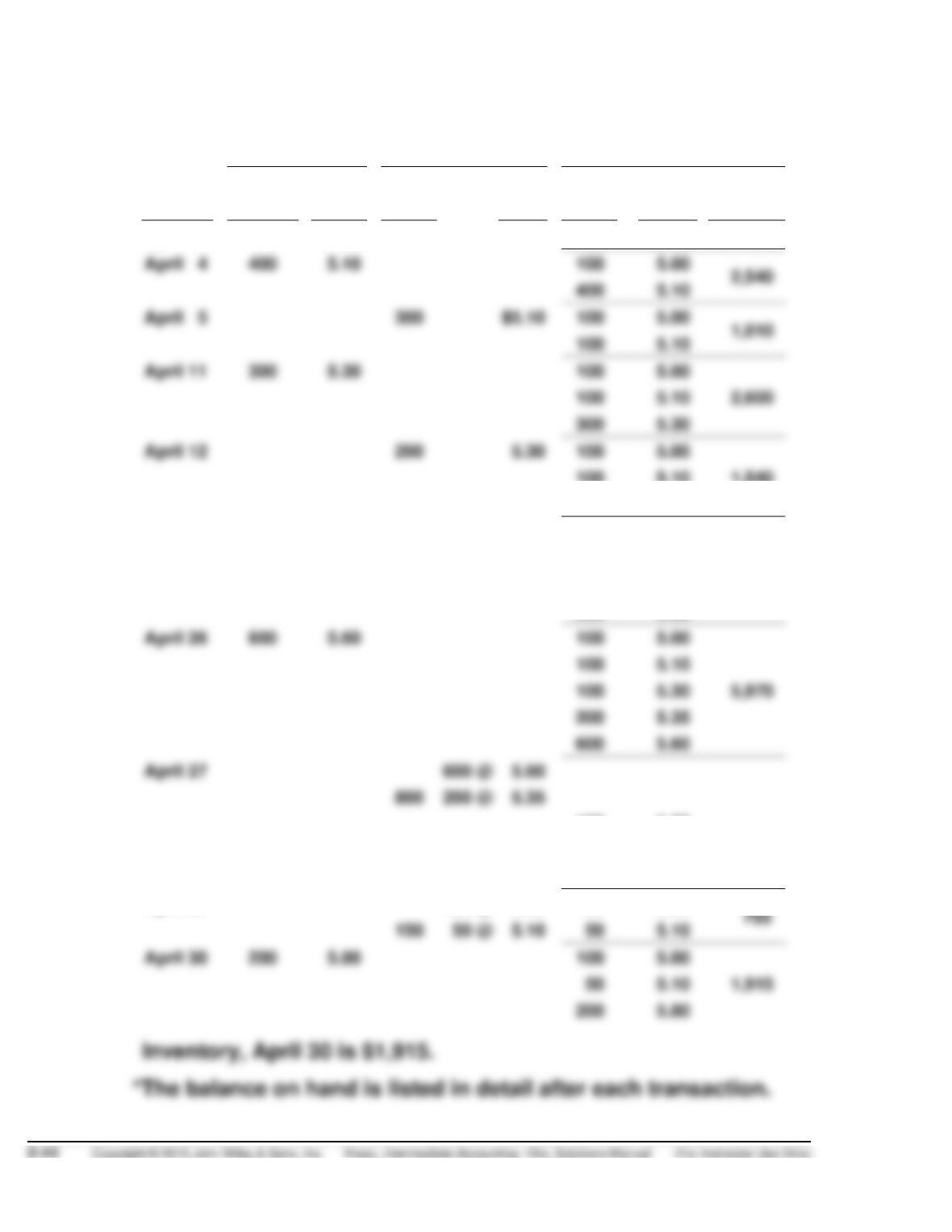

2. Last-in, first-out.

Purchased

Sold

Balance*

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost

Amount

April 1

100

$5.00

100

$5.00

$ 500

April 4

100

5.00

2,540

400

5.10

April 5

300

$5.10

100

5.00

100

5.10

April 11

100

5.00

100

5.10

2,600

300

5.30

April 12

200

100

5.00

100

5.10

1,540

100

5.30

April 18

200

5.35

100

5.00

100

5.10

2,610

100

5.30

200

5.35

April 26

100

5.00

100

5.10

100

5.30

5,970

200

5.35

600

5.60

April 27

800

100

5.00

1,540

100

5.10

100

5.30

April 28

100 @

5.30

100

5.00

150

5.10

April 30

200

100

5.00

5.10

200

5.80

PROBLEM 8-4 (Continued)

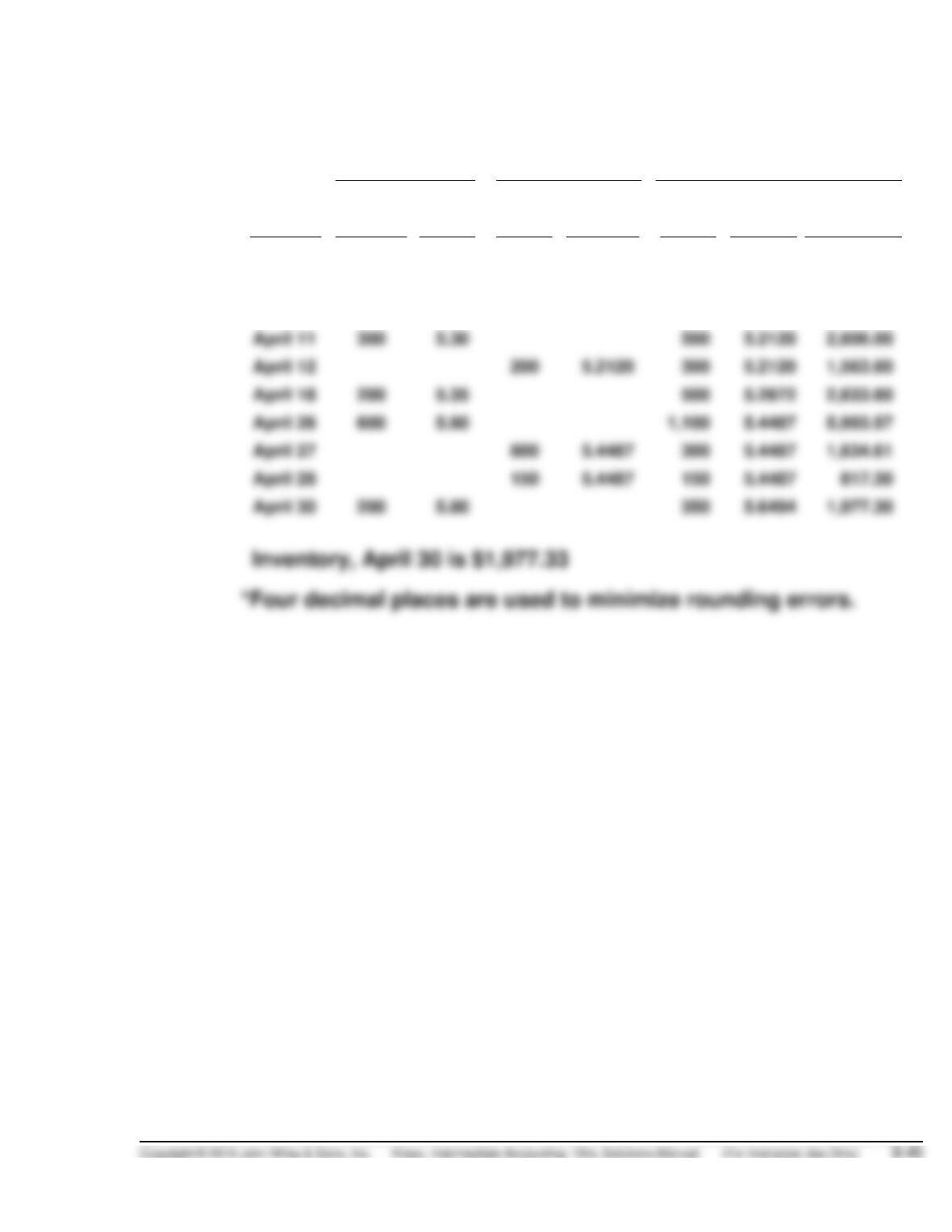

3. Average-cost.

Purchased

Sold

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost*

Amount

April 1

100

$5.00

100

$5.0000

$ 500.00

April 4

400

5.10

500

5.0800

2,540.00

April 5

300

$5.0800

200

5.0800

1,016.00

April 11

300

5.30

500

5.2120

2,606.00

April 12

200

5.2120

300

5.2120

1,563.60

April 18

200

5.35

500

5.2672

2,633.60

April 26

600

5.60

1,100

5.4487

5,993.57

April 27

800

5.4487

300

5.4487

1,634.61

April 28

150

5.4487

150

5.4487

817.30

April 30

200

5.80

350

5.6494

1,977.30

PROBLEM 8-5

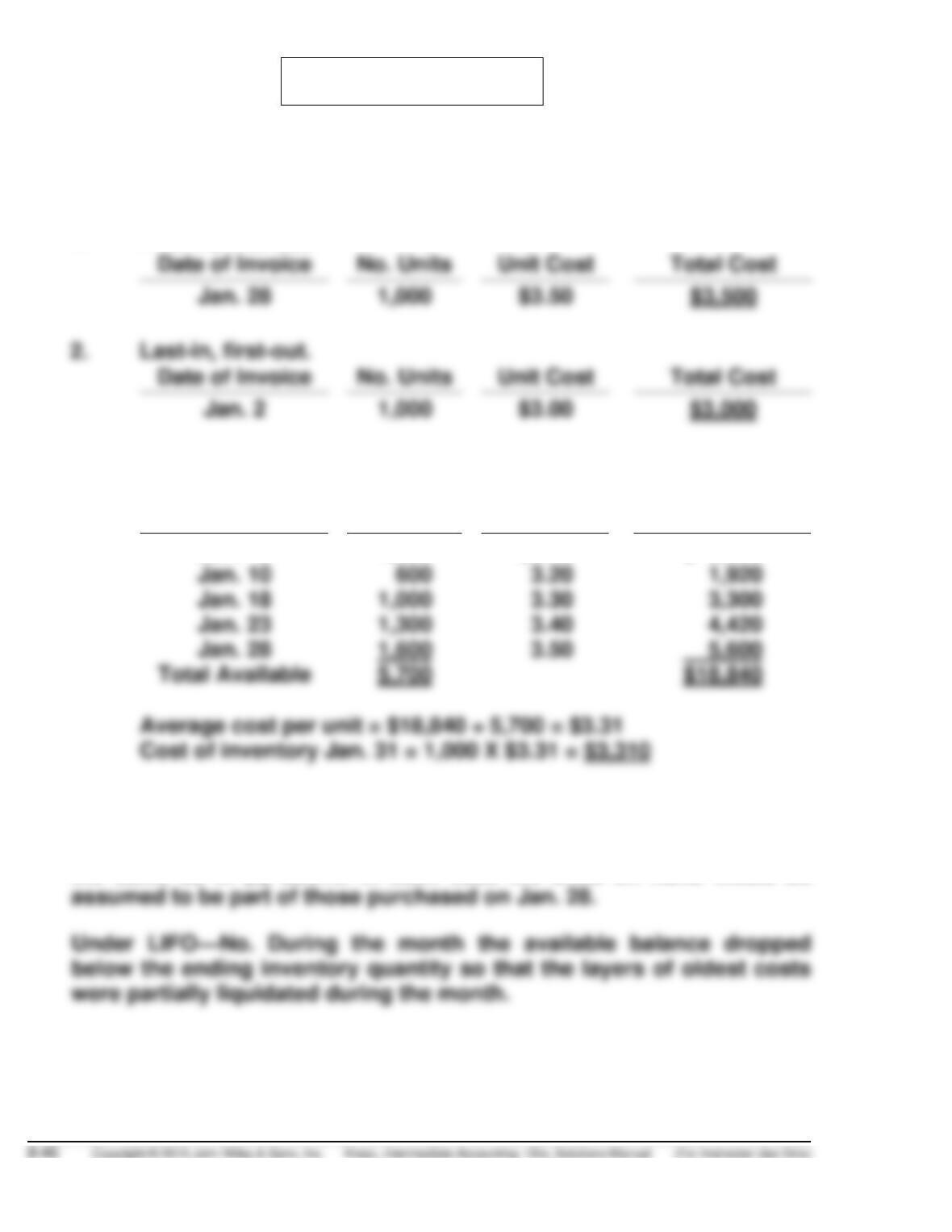

(a) Assuming costs are not computed for each withdrawal (units received,

5,700, minus units issued, 4,700, equals ending inventory at 1,000 units):

1. First-in, first-out.

Date of Invoice

No. Units

Unit Cost

Total Cost

$3.50

$3.00

3. Average-cost.

Cost of goods available:

Date of Invoice

No. Units

Unit Cost

Total Cost

Jan. 2

1,200

$3.00

$ 3,600

Jan. 23

1,300

4,420

(b) Assuming costs are computed at the time of each withdrawal:

Under FIFO—Yes. The amount shown as ending inventory would be

the same as in (a) above. In each case the units on hand would be

PROBLEM 8-5 (Continued)

Under Average-Cost—No. A new average cost would be computed

each time a withdrawal was made instead of only once for all items

purchased during the year.

The calculations to determine the inventory on this basis are given below.

2. Last-in, first-out.

Received

Issued

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost*

Amount

Jan. 2

1,200

$3.00

1,200

$3.00

$3,600

Jan. 7

700

$3.00

500

3.00

1,500

Jan. 10

600

3.20

500

3.00

600

3.20

Jan. 13

500

3.20

500

3.00

1,820

100

3.20

100

3.20

4,130

700

3.30

Jan. 20

700

3.30

100

3.20

300

3.00

200

3.00

600

Jan. 23

1,300

3.40

200

3.00

5,020

1,300

3.40

Jan. 26

800

3.40

200

3.00

500

3.40

Jan. 28

1,600

3.50

200

3.00

500

3.40

7,900

1,600

3.50

Jan. 31

1,300

3.50

200

3.00

500

3.40

3,350

300

3.50

PROBLEM 8-5 (Continued)

3. Average-cost.

Received

Issued

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost*

Amount

Jan. 2

1,200

$3.00

1,200

$3.0000

$3,600

Jan. 7

700

$3.0000

500

3.0000

1,500

Jan. 10

600

3.20

1,100

3.1091

3,420

Jan. 13

500

3.1091

600

3.1091

1,865

Jan. 18

300

1,300

3.2281

4,197

Jan. 20

1,100

3.2281

200

3.2281

646

Jan. 23

1,300

3.40

1,500

3.3773

5,066

Jan. 26

800

700

3.3773

2,364

Jan. 28

1,600

3.50

2,300

3.4626

7,964

Jan. 31

1,300

3.4626

1,000

3.4626

3,463

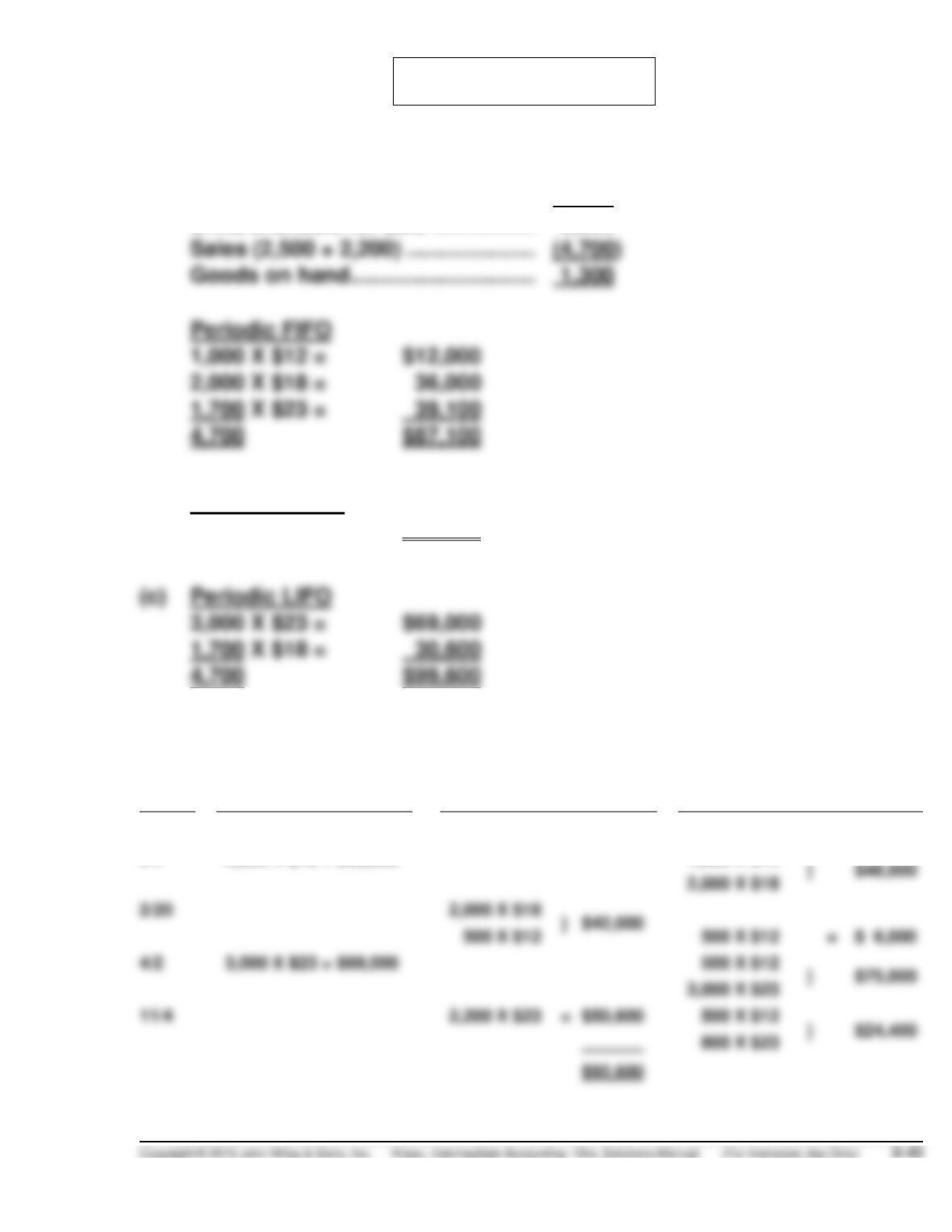

PROBLEM 8-6

(a)

Beginning inventory …………………

1,000

Purchases (2,000 + 3,000) ………….

5,000

Units available for sale ……………..

6,000

Sales (2,500 + 2,200) …………………

Goods on hand …………………………

Periodic FIFO

1,000 X $12 =

1,700 X $23 =

4,700

$87,100

(b)

Perpetual FIFO

Same as periodic:

$87,100

(c)

Periodic LIFO

3,000 X $23 =

1,700 X $18 =

4,700

$99,600

(d)

Perpetual LIFO

Date

Purchased

Sold

Balance

1/1

1,000 X $12

=

$12,000

2/4

2,000 X $18 = $36,000

1,000 X $12

2,000 X $18

2/20

2,000 X $18

500 X $12

500 X $12

=

$ 6,000

4/2

3,000 X $23 = $69,000

500 X $12

3,000 X $23

11/4

2,200 X $23

=

$50,600

500 X $12

PROBLEM 8-6 (Continued)

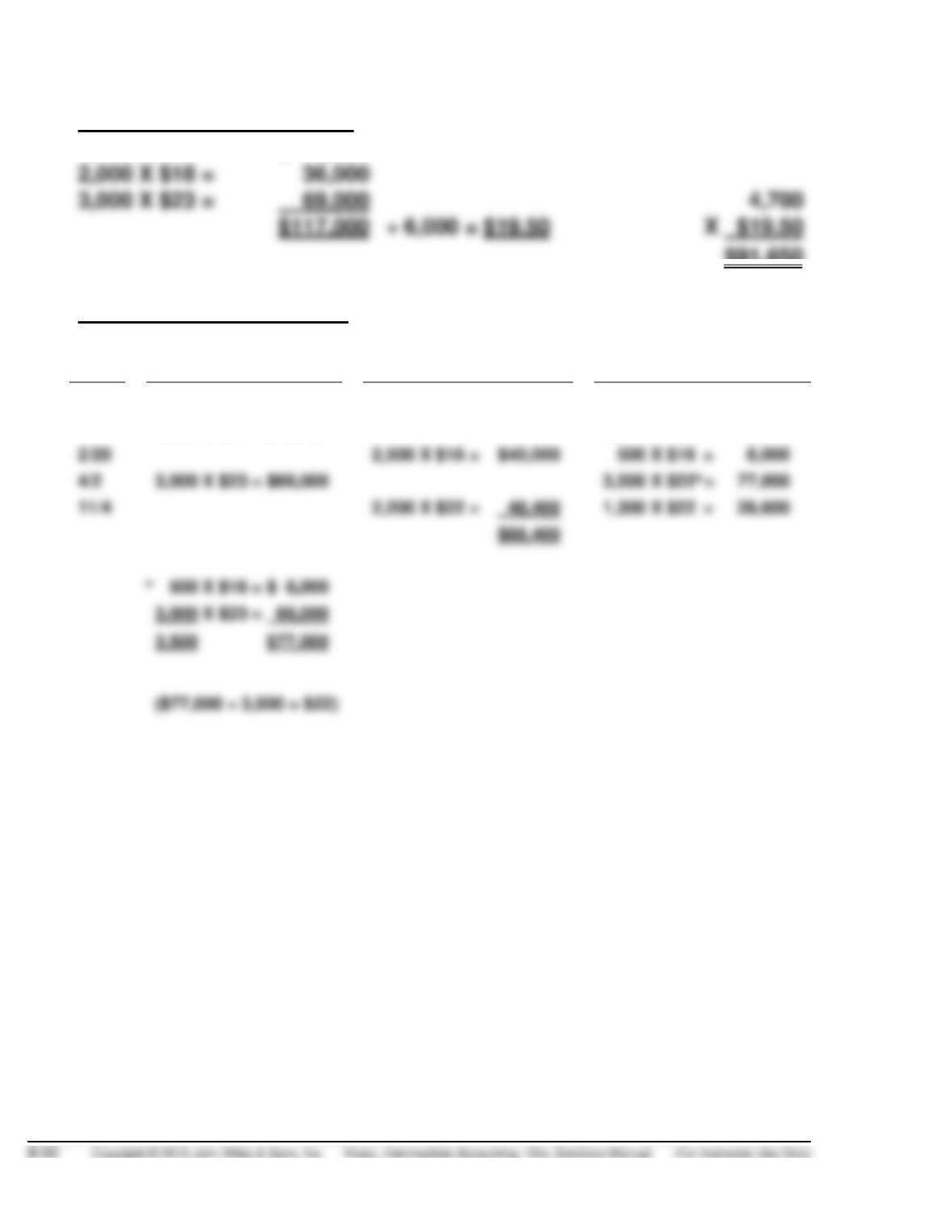

(e)

Periodic weighted-average

1,000 X $12 =

$ 12,000

2,000 X $18 =

3,000 X $23 =

69,000

$91,650

(f)

Perpetual moving average

Date

Purchased

Sold

Balance

1/1

1,000 X $12 =

$12,000

2/4

2,000 X $18 = $36,000

3,000 X $16 =

48,000

2/20

2,500 X $16 =

$40,000

500 X $16 =

8,000

4/2

3,000 X $23 = $69,000

3,500 X $22a =

77,000

11/4

2,200 X $22 =

48,400

1,300 X $22 =

28,600

$88,400

3,000 X $23 = 69,000

PROBLEM 8-7

The accounts in the 2015 financial statements which would be affected by

a change to LIFO and the new amount for each of the accounts are as

follows:

Account

New amount

for 2015

(1)

Cash

$176,400

(2)

Inventory

(3)

Retained earnings

(4)

Cost of goods sold

The calculations for both 2014 and 2015 to support the conversion to LIFO

are presented below.

Income for the Years Ended

12/31/14

12/31/15

Sales revenue

$900,000

$1,350,000

Less: Cost of goods sold

525,000

792,000

Other expenses

205,000

304,000

730,000

Income before taxes

170,000

254,000

Income taxes (40%)

68,000

101,600

Net income

Cost of Goods Sold and

Ending Inventory for the Years Ended

12/31/14

12/31/15

Beginning inventory

( 40,000 X $3.00)

$120,000

( 40,000 X $3.00)

$120,000

Purchases

(150,000 X $3.50)

525,000

(180,000 X $4.40)

792,000

Cost of goods available

645,000

912,000

Ending inventory

( 40,000 X $3.00)

( 40,000 X $3.00)

Cost of goods sold

$525,000

$792,000

Determination of Cash at

12/31/14

12/31/15

Income taxes under FIFO

$ 76,000

$116,000

Income taxes as calculated under LIFO

68,000

101,600

Increase in cash

8,000

14,400

difference

8,000

Total increase in cash

8,000

22,400

PROBLEM 8-7 (Continued)

Determination of Retained Earnings at

12/31/14

12/31/15

Net income under FIFO

$114,000

$174,000

Net income under LIFO

(102,000)

(152,400)

Reduction in retained earnings

12,000

21,600

2014 reduction

12,000

Total reduction in retained earnings

12,000

33,600

Retained earnings under FIFO

PROBLEM 8-8

(a)

1.

Ending inventory in units

Portable

6,000 + 15,000 – 14,000 =

Midsize

8,000 + 20,000 – 24,000 =

Flat-screen

3,000 + 10,000 – 6,000 =

2.

Ending inventory at current cost

Portable

7,000 X $110 =

$ 770,000

Midsize

4,000 X $300 =

1,200,000

Flat-screen

7,000 X $500 =

3,500,000

$5,470,000

3.

Ending inventory at base-year cost

Portable

7,000 X $100 =

$ 700,000

Midsize

4,000 X $250 =

1,000,000

Flat-screen

7,000 X $400 =

2,800,000

$4,500,000

4.

Price index

$5,470,000 ÷ $4,500,000 = 1.2156

5.

Ending inventory

$3,800,000 X 1.0000 =

$3,800,000

700,000* X 1.2156 =

850,920

$4,650,920

*($4,500,000 – $3,800,000 = $700,000)

6.

Cost of goods sold

Beginning inventory ………………………………………….

$ 3,800,000

Purchases

Cost of goods available …………………………………….

Ending inventory ………………………………………………

PROBLEM 8-8 (Continued)

7.

Gross profit

Sales revenue

(6,000 X $600)] …………………………………………………….

$15,420,000

Cost of goods sold …………………………………………………

(b)

1.

Ending inventory at current cost restated to base cost

Portable

$ 770,000 ÷ 1.10a =

$ 700,000

a. $110 ÷ $100

b. $300 ÷ $250

c. $500 ÷ $400

2.

Ending inventory

Portable

$ 600,000 X 1.00 =

$ 600,000

100,000 X 1.10 =

Midsize

Flat-screen

2,000,000

3.

Cost of good sold

Cost of good available …………………………………………

$16,450,000

Ending inventory …………………………………………………

(4,910,000)

Cost of goods sold …………………………………………

$11,540,000

4.

Gross profit

Sales revenue ……………………………………………………..

$15,420,000

Cost of goods sold ………………………………………………

PROBLEM 8-9

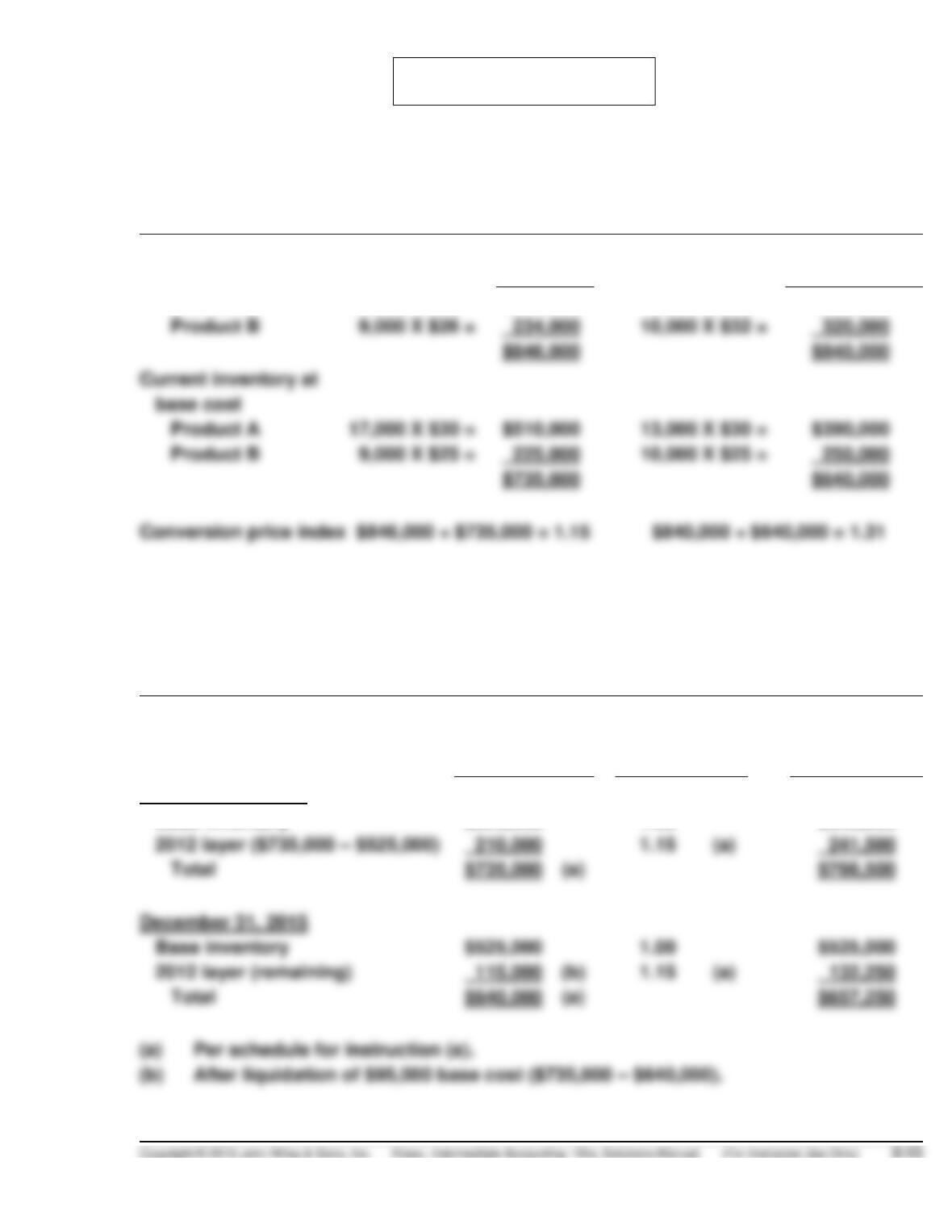

(a) BONANZA WHOLESALERS INC.

Computation of Internal Conversion Price Index

for Inventory Pool No. 1 Double Extension Method

Current inventory at

current-year cost

2014

2015

Product A

17,000 X $36 =

$612,000

13,000 X $40 =

$520,000

Product B

base cost

Product A

17,000 X $30 =

Product B

(b) BONANZA WHOLESALERS INC.

Computation of Inventory Amounts

Under Dollar-Value LIFO Method for Inventory Pool No. 1

at December 31, 2014 and 2015

Current

Inventory at

base cost

Conversion

price index

Inventory at

LIFO cost

December 31, 2014

Base inventory

$525,000

1.00

$525,000

2012 layer ($735,000 – $525,000)

(a)

December 31, 2015

Base inventory

2012 layer (remaining)

(a)

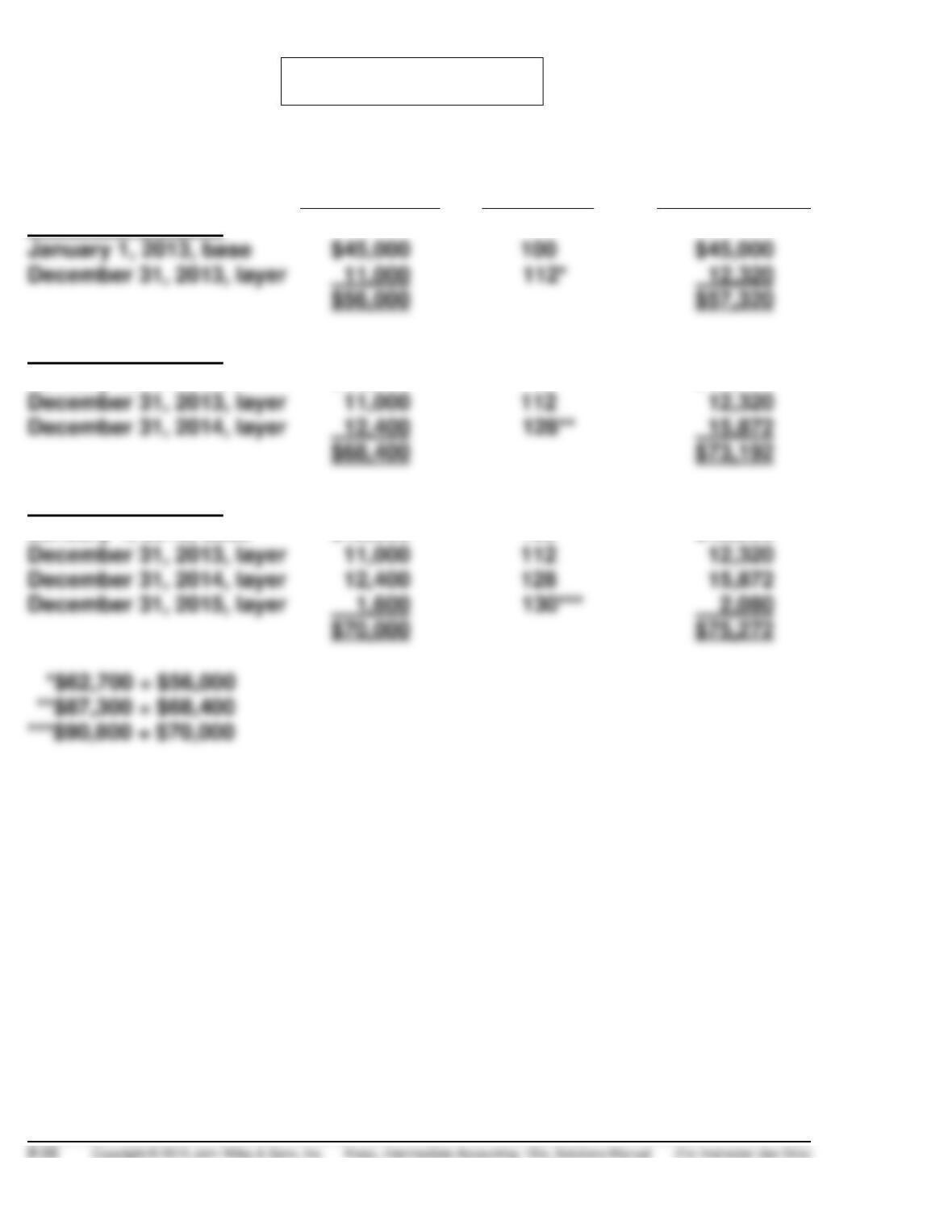

PROBLEM 8-10

Base-Year

Cost

Index %

Dollar-Value

LIFO

December 31, 2013

January 1, 2013, base

$45,000

100

$45,000

December 31, 2013, layer

December 31, 2014

January 1, 2013, base

$45,000

100

$45,000

December 31, 2013, layer

112

December 31, 2014, layer

December 31, 2015

January 1, 2013, base

$45,000

100

$45,000

December 31, 2013, layer

112

December 31, 2014, layer

128

December 31, 2015, layer

1,600

2,080

*$62,700 ÷ $56,000

***$90,800 ÷ $70,000

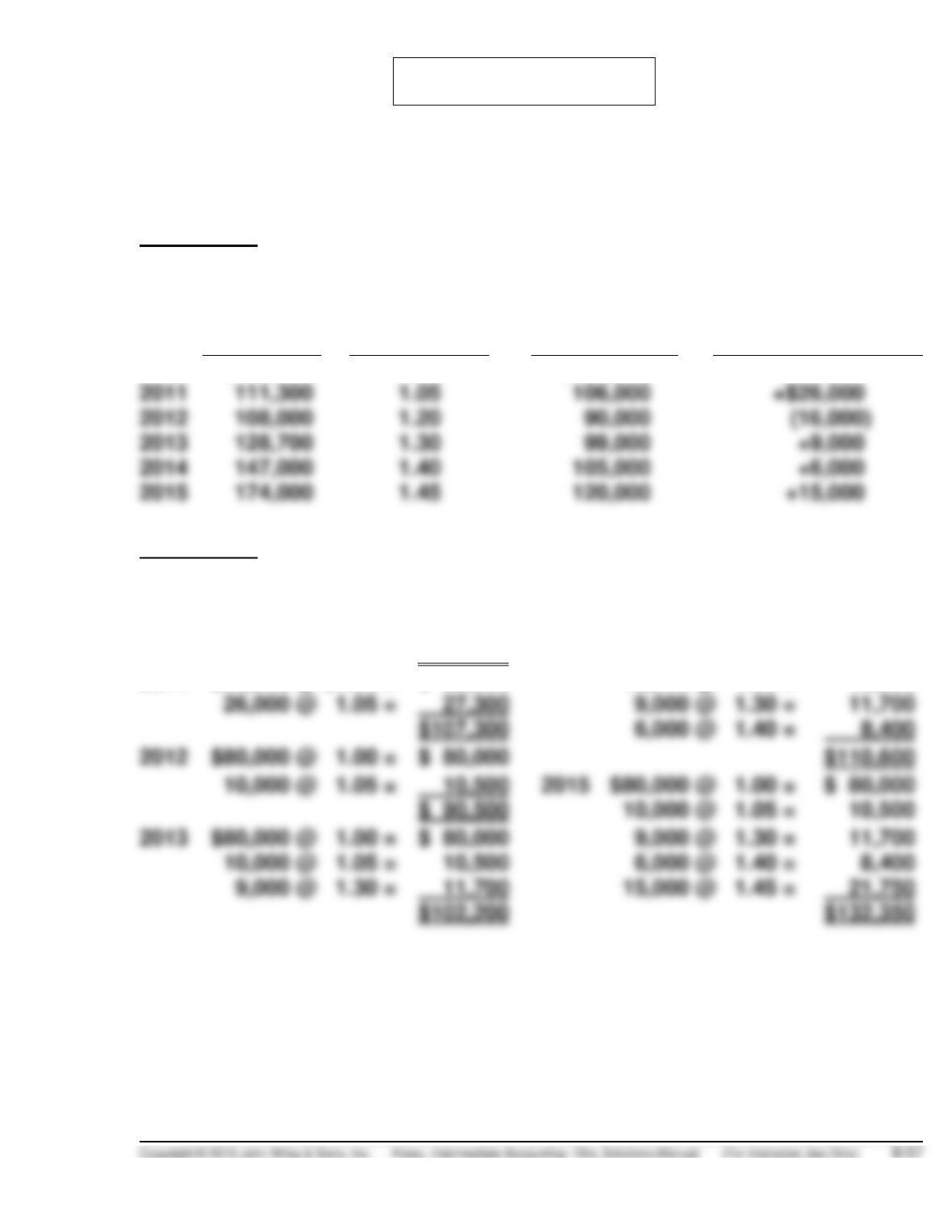

PROBLEM 8-11

(a)

Schedule A

A

B

C

D

Current $

Price Index

Base-Year $

Change from

Prior Year

2010

$ 80,000

1.00

$ 80,000

—

2011

1.05

2012

2013

1.30

99,000

2014

1.40

2015

Schedule B

Ending Inventory-Dollar-Value LIFO:

2010

$ 80,000

2014

$80,000 @ $1.00 =

$ 80,000

2011

$80,000 @ $1.00 =

$ 80,000

10,000 @ 1.05 =

10,500

27,300

9,000 @ 1.30 =

10,500

2015

$80,000 @ 1.00 =

$ 80,000

2013

$80,000 @ 1.00 =

$ 80,000

9,000 @ 1.30 =

11,700

6,000 @ 1.40 =

9,000 @ 1.30 =

11,700

21,750

PROBLEM 8-11 (Continued)

(b)

To: Richardson Company

From: Accounting Student

Subject: Dollar-Value LIFO Pool Accounting

Dollar-value LIFO is an inventory method which values groups or “pools”

of inventory in layers of costs. It assumes that any goods sold during a

given period were taken from the most recently acquired group of goods in

stock and, consequently, any goods remaining in inventory are assumed to

be the oldest goods, valued at the oldest prices.

However, inflation distorts any cost of purchases made in subsequent years.

To counteract the effect of inflation, this method measures the incremental

change in each year’s ending inventory in terms of the first year’s (base

year’s) costs. This is done by adjusting subsequent cost layers, through

the use of a price index, to the base year’s inventory costs. Only after this

adjustment can the new layer be valued at current-year prices.

PROBLEM 8-11 (Continued)

1. Refer to Schedule A. To express each year’s ending inventory (Column A)

in terms of base-year costs, simply divide the ending inventory by the

2. Next, compute the difference between the previous and the current

3. Finally, express this increment in current-year terms. For the second

year, this computation is straightforward: the base-year ending inven-

Be careful with this last step in subsequent years. Notice that, in 2012, the

change from the previous year is –$16,000, which causes the 2011 layer to

be eroded during the period. Thus, the 2012 ending inventory is valued at

the original base-year cost $80,000 plus the remainder valued at the 2011

price index, $10,000 times 1.05. See 2012 computation on Schedule B.

These instructions should help you implement dollar-value LIFO in your

inventory valuation.

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 8-1 (Time 15–20 minutes)

CA 8-2 (Time 15–25 minutes)

Purpose—to provide the student with four questions about the carrying value of inventory. These

questions must be answered and defended with rationale. The topics are shipping terms, freight–in,

weighted-average cost vs. FIFO, and consigned goods.

CA 8-3 (Time 25–35 minutes)

Purpose—to provide a number of difficult financial reporting transactions involving inventories. This case

CA 8-4 (Time 15–25 minutes)

CA 8-5 (Time 20–25 minutes)

Purpose—to provide a broad overview to students as to why inventories must be included in the

CA 8-6 (Time 15–20 minutes)

CA 8-7 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to discuss the cost flow assumptions of average

cost, FIFO, and LIFO. Student is also required to distinguish between weighted-average and moving-

average and discuss the effect of LIFO on the B/S and I/S in a period of rising prices.

CA 8-8 (Time 25–30 minutes)

Purpose—to provide the student with the opportunity to discuss the differences between traditional

CA 8-9 (Time 25–30 minutes)