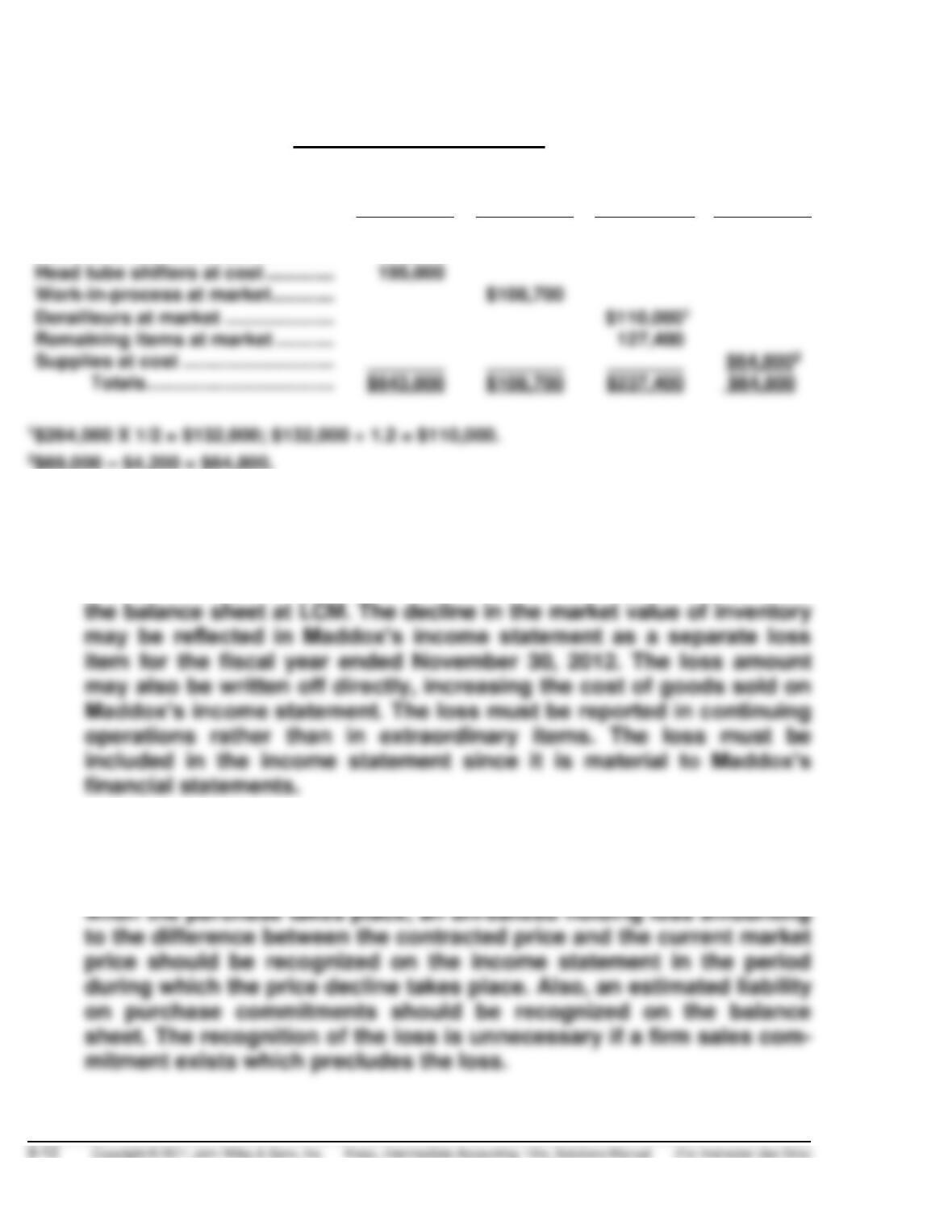

PROBLEM 9-9 (Continued)

Supporting Calculations

Finished

Goods

Work-in–

Process

Raw

Materials

Factory

Supplies

Down tube shifters at market ……..

$266,000

Bar end shifters at cost ……………..

182,000

Head tube shifters at cost ………….

195,000

$108,700

Derailleurs at market …………………

Remaining items at market ………..

Supplies at cost ………………………..

(b) The decline in the market value of inventory below cost may be

reported using one or two alternate methods, the direct write-down of

inventory (cost-of-goods-sold method) or the (loss method). An

allowance may be used under either method to report inventory on

(c) Purchase contracts for which a firm price has been established should

be disclosed on the financial statements of the buyer. If the contract

price is greater than the current market price and a loss is expected

PROBLEM 9-10

(a) Schedule A

Item

On Hand

Quantity

Replacement

Cost/Unit

NRV

(Ceiling)

NRV—

Normal

Profit

(Floor)

Designated

Market

Cost

Lower-of–

Cost-or–

Market

A

B

C

D

E

Schedule B

Item

Cost

Lower-of-Cost-or-Market

Difference

A

1,100 X $7.50 = $8,250

1,100 X $7.50 = $8,250

None

1,000 X $5.60 = $5,600

D

1,000 X $3.80 = $3,800

1,000 X $3.80 = $3,800

None

1,400 X $6.40 = $8,960

$950

(b) Cost of Goods Sold ……………………………………………………….

950

Allowance to Reduce Inventory to Market …………………

950

or

Loss Due to Market Decline of Inventory …………………………

Allowance to Reduce Inventory to Market …………………

950

PROBLEM 9-10 (Continued)

(c)

To: Greg Forda, Clerk

From: Accounting Manager

Date: January 14, 2013

Subject: Instructions on determining lower-of-cost-or-market for inven-

tory valuation

This memo responds to your questions regarding our use of lower-of-cost-

or-market for inventory valuation. Simply put, value inventory at whichever

is the lower: the actual cost or the market value of the inventory at the time

of valuation.

The term market, on the other hand, is more complicated. As you have

already noticed, this value could be the inventory’s replacement cost, its

net realizable value (selling price minus any estimated costs to complete

and sell), or its net realizable value less a normal profit margin. The

profession requires that the middle value of the three above costs be

chosen as the “designated market value.” This designated market value is

then compared to the actual cost in determining the lower–of-cost-or–

market.

PROBLEM 9-10 (Continued)

Proceed in the same way, always choosing the middle value among replace-

After you have aggregated the total lower-of-cost-or-market for all items,

you will be likely to have a loss on inventory which must be accounted for.

In our example, the loss is $950. You can journalize this loss in one of two

ways:

Cost of Goods Sold ………………………………………………………

950

Allowance to Reduce Inventory to Market ………………

950

Loss Due to Market Decline of Inventory ……………………….

950

Allowance to Reduce Inventory to Market ………………

950

Schedule A

Item

On Hand

Quantity

Replacement

Cost/Unit

NRV

Ceiling

NRV—

Normal

Profit

(Floor)

Designated

Market

Cost

Lower-of–

Cost-or–

Market

A

1,100

$8.40

$9.00

$7.20

$8.40

$7.50

$7.50

Schedule B

Item

Cost

Lower-of-Cost-or-Market

Difference

A

1,100 X $7.50 = $8,250

1,100 X $7.50 = $8,250

None

B

800 X $8.20 = $6,560

800 X $7.90 = $6,320

C

1,000 X $5.60 = $5,600

1,000 X $5.45 = $5,450

D

1,000 X $3.80 = $3,800

1,000 X $3.80 = $3,800

None

E

1,400 X $6.40 = $8,960

1,400 X $6.00 = $8,400

$950

*PROBLEM 9-11

(a)

Cost

Retail

Inventory, January 1 …………………..

$ 30,000

$ 43,000

Purchases ………………………………….

104,800

155,000

Purchase returns ………………………..

(2,800)

(4,000)

Totals ………………………………..

132,000

194,000

Add: Net markups

Markups …………………………...

$ 9,200

Markup cancellations …………

(3,200)

6,000

Totals ………………………………..

$132,000

200,000

Deduct: Net markdowns

Markdowns ………………………..

$ 10,500

Markdown cancellations ……..

4,000

Sales price of goods available …….

196,000

Sales ………………………………………….

$154,000

Sales returns and allowances ……..

Ending inventory at retail ……………

Inventory at lower-of-cost-or–

market (66% X $50,000) …………….

$ 33,000

(b)

Ending inventory at retail at January 1 price level

($59,400 ÷ 1.08) …………………………………………………………

$ 55,000

Less beginning inventory at retail ………………………………..

43,000

Inventory increment at retail, January 1 price level ………..

$ 12,000

($12,000 X 1.08) ………………………………………………………...

$ 12,960

Beginning inventory at cost …………………………………………

$ 30,000

Inventory increment at cost at June 30 price level

Ending inventory at dollar-value LIFO cost ……………………

*PROBLEM 9-12

(a) The retail method is appropriate in businesses that sell many different

items at relatively low unit costs and that have a large volume of

(b) Becker Department Stores’ ending inventory value, at cost, is $83,000,

calculated as follows:

Cost

Retail

Beginning inventory ………………………………

$ 68,000

$100,000

Purchases ……………………………………………..

$255,000

$400,000

Net markups ………………………………….

50,000

Net markdowns ……………………………..

(110,000)

Goods available …………………………………….

440,000

Estimated ending inventory at retail ………..

$120,000

Beginning inventory layer ………………………

$ 68,000

$100,000

Incremental increase

20,000

At cost ($20,000 X 75%) ………………….

15,000

*PROBLEM 9-12 (Continued)

(c) The estimated shortage amount, at retail, for Becker Department Stores

is $5,000 calculated as follows:

(d) When using the retail inventory method, the four expenses and allow-

ances noted are treated in the following manner:

1. Freight costs are added to the cost of purchases.

2. Purchase returns and allowances are considered as reductions

*PROBLEM 9-13

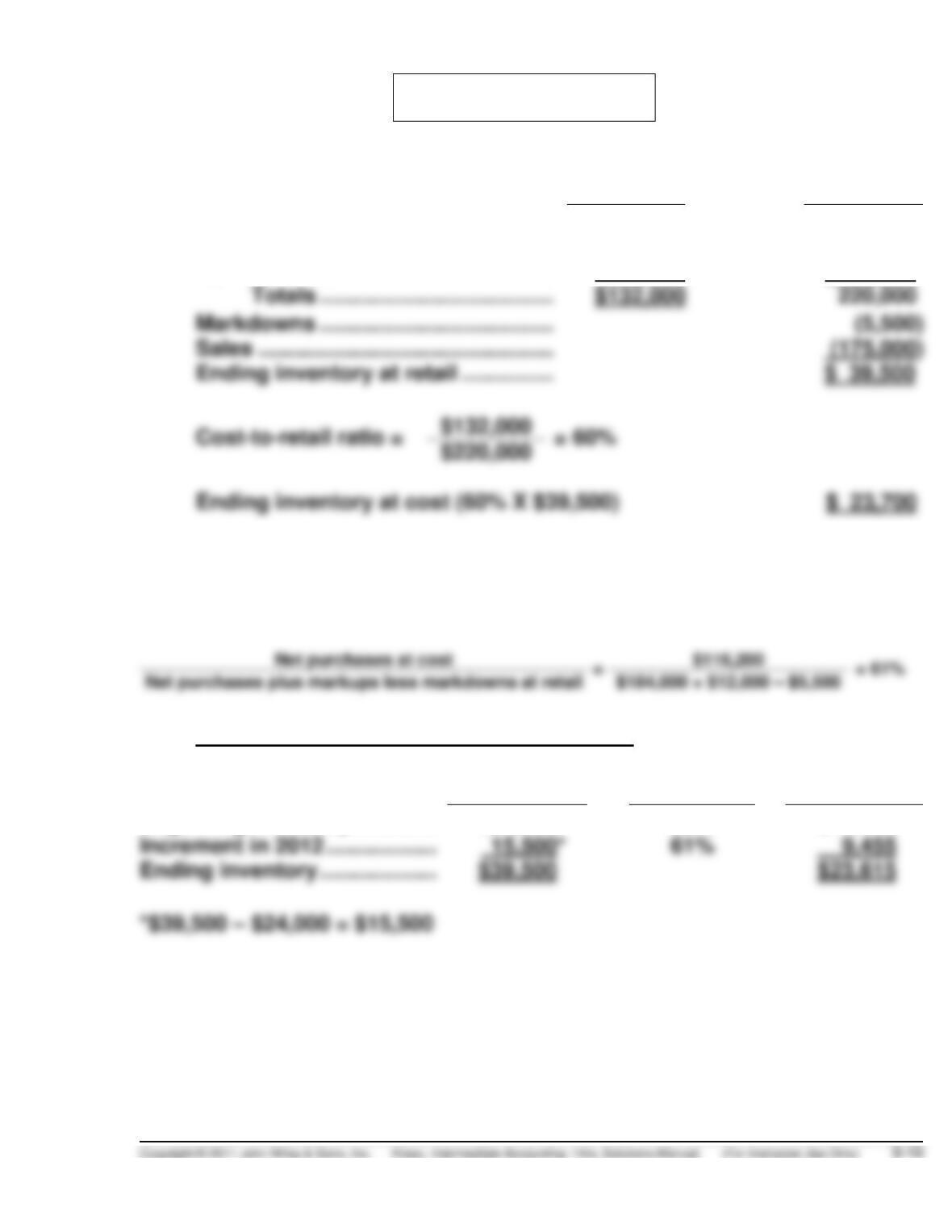

(a)

Cost

Retail

Inventory (beginning) ………………….

$ 15,800

$ 24,000

Purchases ………………………………….

116,200

184,000

Markups …………………………………….

12,000

Totals ………………………………..

Markdowns ………………………………..

Sales …………………………………………

Ending inventory at retail ……………

Ending inventory at cost (60% X $39,500)

$ 23,700

(b)

Ending inventory for 2012 under the LIFO method:

The cost-to-retail ratio for 2012 can be computed as follows:

December 31, 2012, inventory at LIFO cost:

Retail

Ratio

LIFO Cost

Beginning inventory …………..

$24,000

59%

$14,160

Increment in 2012 ………………

Ending inventory ……………….

*PROBLEM 9-14

(a) DAVENPORT DEPARTMENT STORE

COMPUTATION OF COST

OF DECEMBER 31, 2011, INVENTORY

BASED ON THE CONVENTIONAL RETAIL METHOD

At Cost

At Retail

Beginning inventory, January 1, 2011 …………..

$ 29,800

$ 56,000

Add (deduct) transactions affecting cost ratio:

Gross purchases ………………………………..

Purchase returns ……………………………….

Purchase discounts …………………………...

Freight-in …………………………………………..

Net markups ………………………………………

Totals …………………………..………………

$347,200

620,000

Add (deduct) other retail transactions not

considered in computation of cost ratio:

Gross sales ……………………………………….

(551,000)

Sales returns ……………………………………..

Net markdowns ………………………………….

Employee discounts …………………………..

Totals …………………………..………………

Inventory, December 31, 2011:

At retail ……………………………………………..

$ 63,000

At cost ($63,000 X 56%*) ……………………..

$ 35,280

*Ratio of cost-to-retail = $347,200 ÷ $620,000

= 56%

*PROBLEM 9-14 (Continued)

(b) COMPUTATION OF COST

OF DECEMBER 31, 2011 INVENTORY

UNDER THE LIFO RETAIL METHOD

Cost

Retail

Totals used in computing cost ratio under

conventional retail method (part a) …………….

$347,200

$620,000

Exclude beginning inventory ……………………….

29,800

56,000

Net purchases …………………………………………….

Deduct net markdowns ………………………………..

12,000

Totals used on computing cost ratio under

Cost ratio under LIFO retail method

($317,400 ÷ $552,000) ………………………………..

Inventory, December 31, 2011:

At Cost under LIFO retail method

*PROBLEM 9-14 (Continued)

(c) COMPUTATION OF 2012 AND 2013

YEAR-END INVENTORIES

UNDER THE DOLLAR-VALUE LIFO METHOD

Computation of retail values on the basis of January 1, 2012, price levels

Cost

Retail

2012:

Inventory at end of year (given) ……………….

$75,600

Inventory at end of year stated in terms

of January 1, 2012 prices

($75,600 ÷ 105%) ………………………………….

January 1, 2012 inventory base (given)

cost ratio of 55.5% ($33,300 ÷ $60,000) ….

Increment in inventory:

In terms of January 1, 2012 prices ……………

$12,000

$12,600

$12,600 ………………………………………………..

December 1, 2012 inventory at LIFO cost …………..

2013:

Inventory at end of year (given) ………………

$62,640

Inventory at end of year stated in terms

of January 1, 2013 prices

($62,640 ÷ 108%) …………………………………

$58,000

December 31, 2013 inventory at LIFO

ratio) X $58,000 ……………………………………

$60,000 Retail

(Note to instructor: Because the retail inventory stated in terms of January 1,

2012 prices at December 31, 2012, $58,000, has fallen below the January 1,

2013 inventory base at retail, $60,000, under the LIFO theory the 2013 layer