PROBLEM 19-6

1.

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

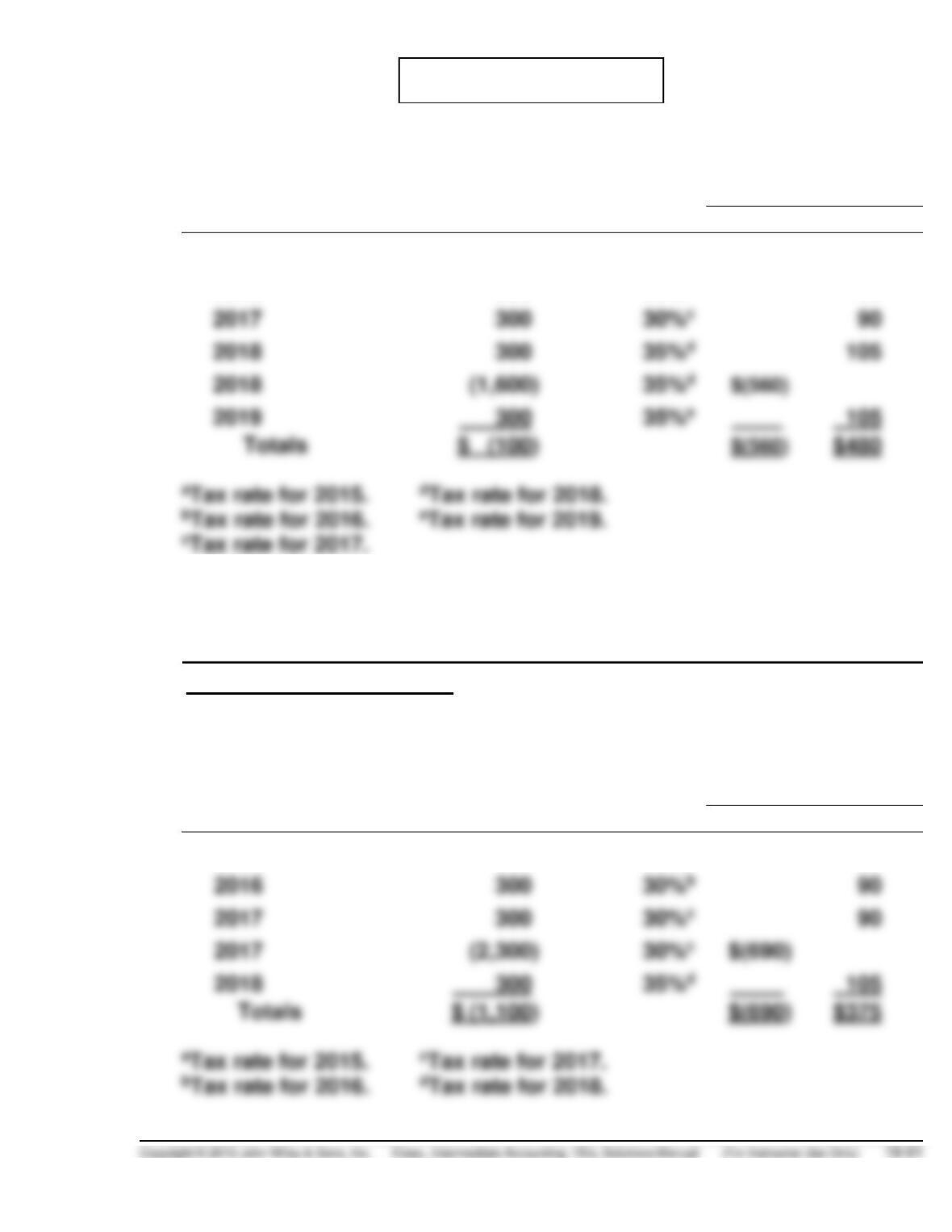

2015

$ 300

30%a

$ 90

2016

300

30%b

90

2017

300

30%c

90

2018

300

35%d

2018

2019

300

35%e

MOONEY CO.

Balance Sheet

December 31, 2014

Other assets (noncurrent)

Deferred tax asset ($560 – $480) ………………………………… $80

2.

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

2015

$ 300

30%a

$ 90

2016

300

30%b

90

2017

300

30%c

90

2017

30%c

2018

300

35%d

PROBLEM 19-6 (Continued)

ROESCH CO.

Balance Sheet

December 31, 2014

PROBLEM 19-7

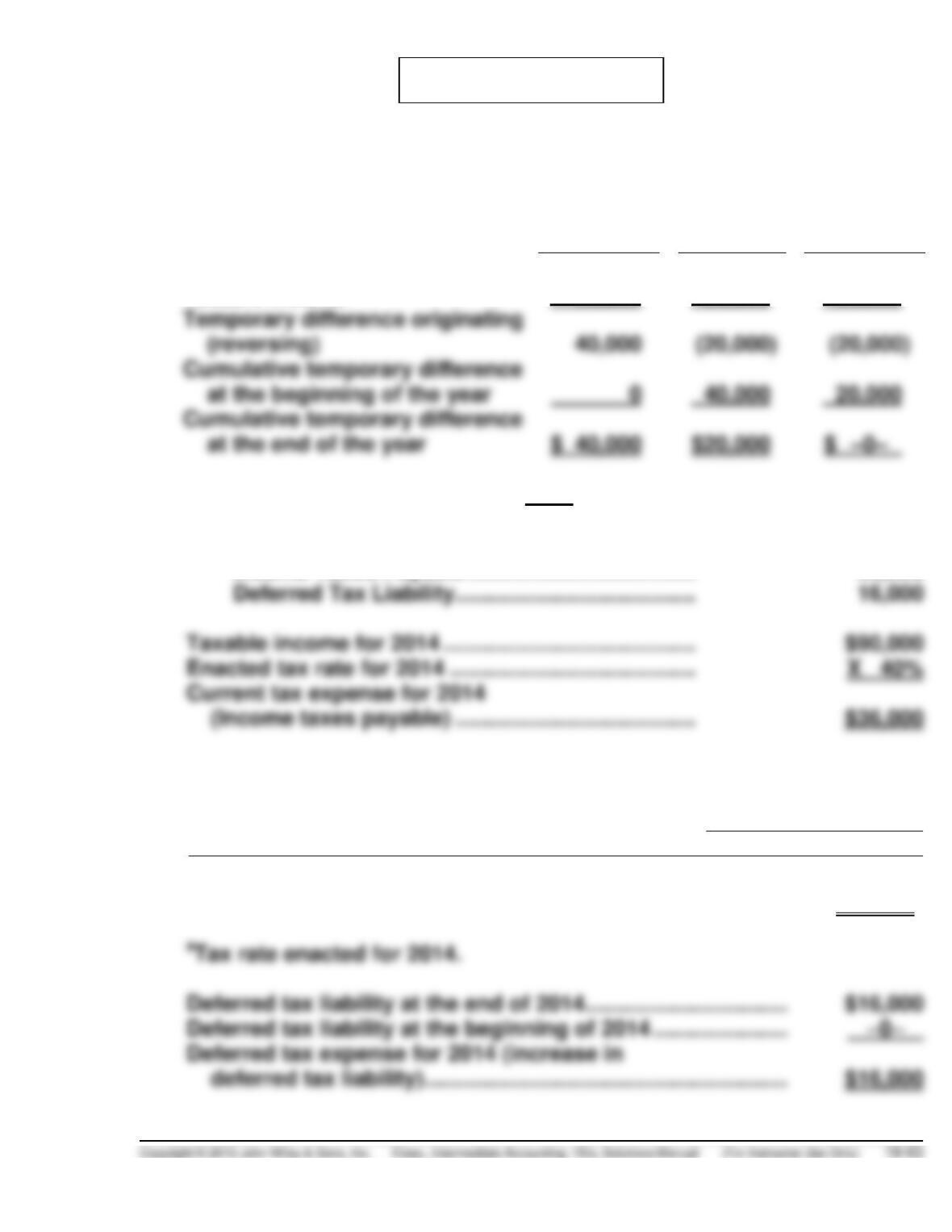

(a) Before deferred taxes can be computed, the amount of cumulative tem–

porary difference existing at the end of each year must be computed:

2014

2015

2016

Pretax financial income

$130,000

($70,000

($70,000

Taxable income

90,000

( 90,000

( 90,000

2014

Income Tax Expense ……………………………………….. 52,000

Income Taxes Payable ………………………………. 36,000

Temporary

Difference

Future Taxable

(Deductible)

Amounts

Tax

Rate

December 31, 2015

Deferred Tax

(Asset)

Liability

Installment Accounts

Receivable

(

$ 40,000

40%a

$16,000

PROBLEM 19-7 (Continued)

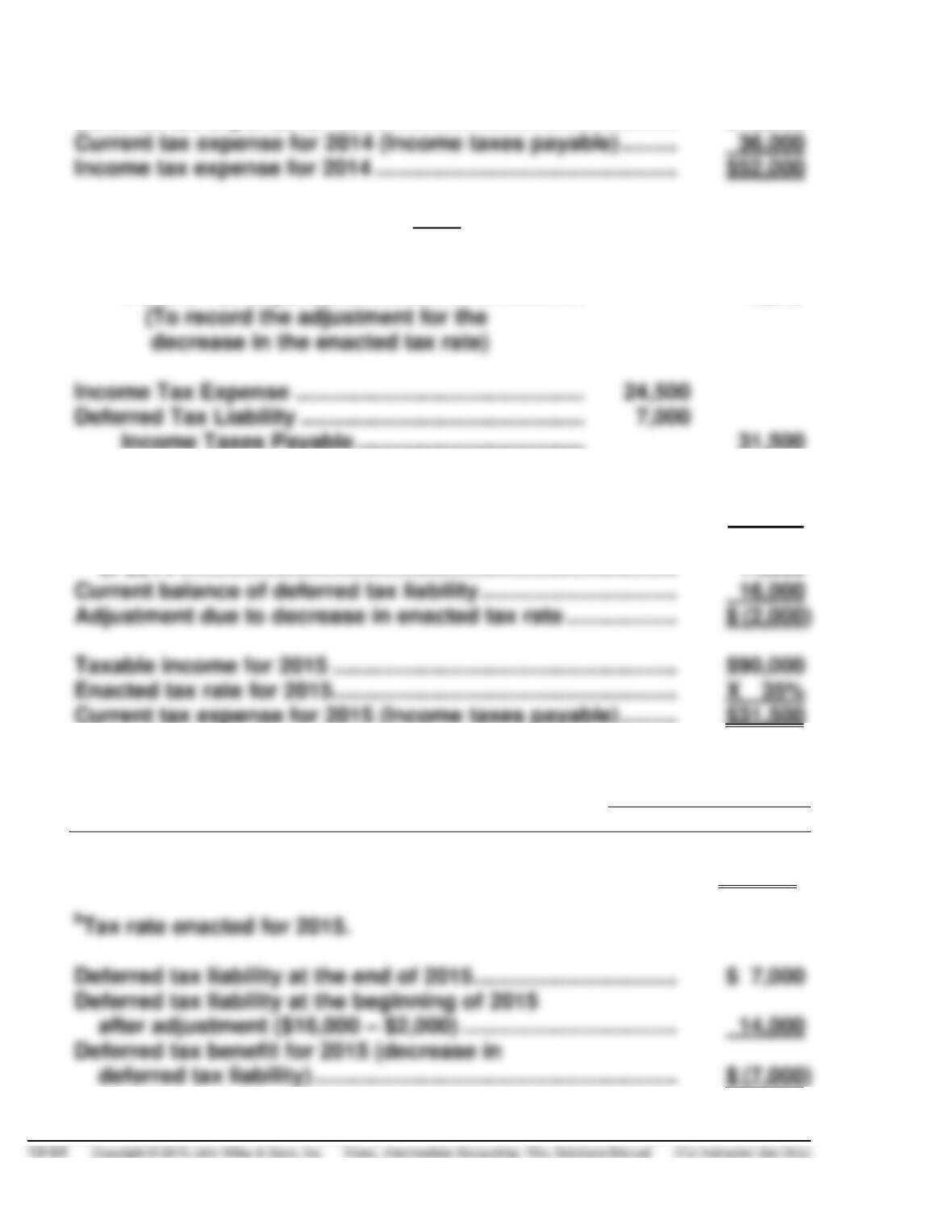

Deferred tax expense for 2014 ……………………………………….. $16,000

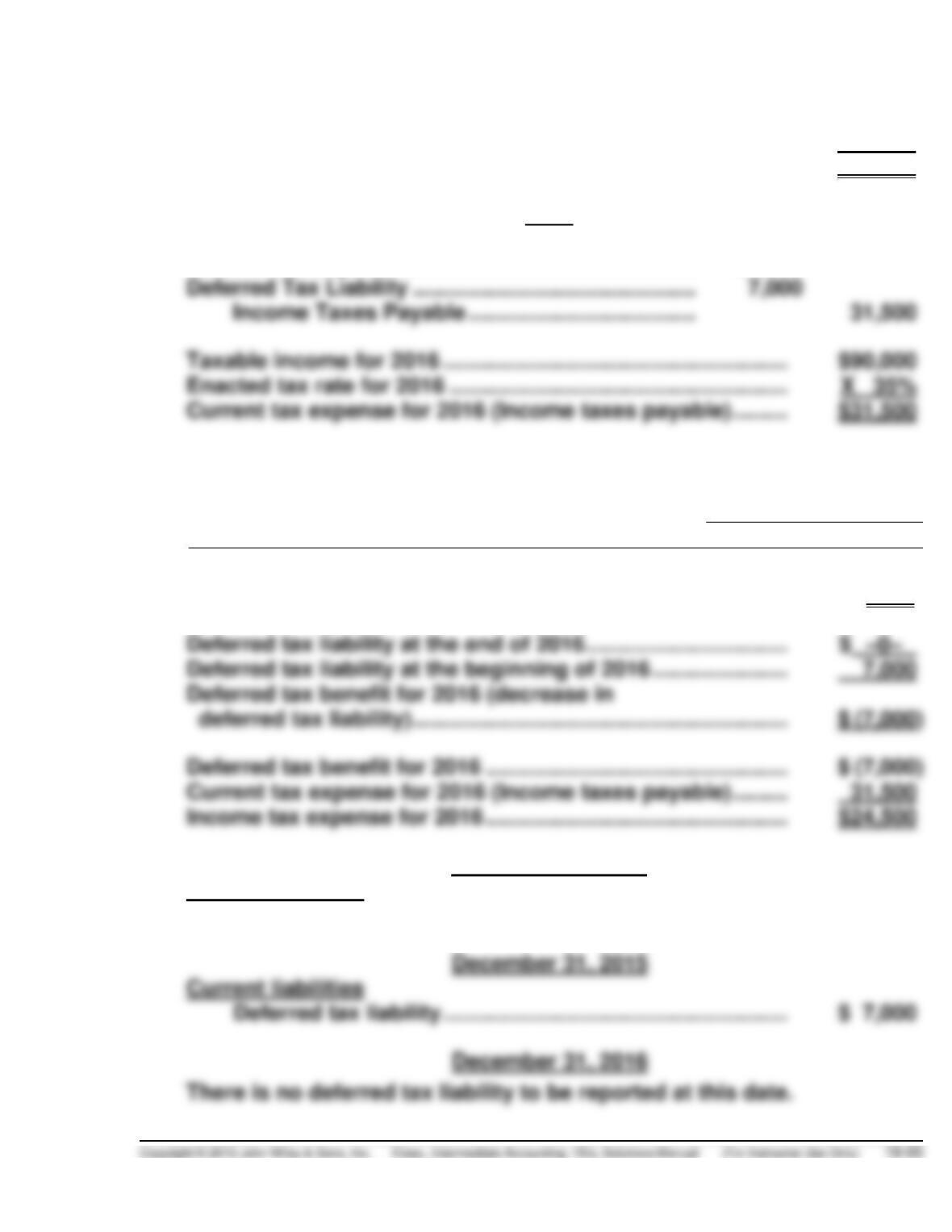

2015

Deferred Tax Liability ………………………………………. 2,000

Income Tax Expense …………………………………. 2,000*

Income Taxes Payable ………………………………. 31,500

*Cumulative temporary difference at the end of 2014 ………… $40,000

Newly enacted tax rate for future year ……………………………. X 35%

Adjusted balance of deferred tax liability at the end

of 2014 ……………………………………………………………………… 14,000

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

December 31, 2015

Deferred Tax

(Asset)

Liability

Installment Accounts

Receivable

$20,000

35%b

$ 7,000

PROBLEM 19-7 (Continued)

Deferred tax benefit for 2015 …………………………………………. $ (7,000)

Current tax expense for 2015 (Income taxes payable) ……… 31,500

Income tax expense for 2015 …………………………………………. $24,500

2016

Income Tax Expense ……………………………………….. 24,500

Temporary

Difference

Future Taxable

(Deductible)

Amounts

Tax

Rate

December 31, 2016

Deferred Tax

(Asset)

Liability

Installment Accounts

Receivable

(

$–0–

30%

$–0–

(b) December 31, 2014

Current liabilities

Deferred tax liability ……………………………………………….. $16,000

PROBLEM 19-7 (Continued)

(c) 2014

Income before income taxes ………………………………… $130,000

2015

Income before income taxes ………………………………… $70,000

2016

Income before income taxes ………………………………… $70,000

PROBLEM 19-8

(a)

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

$(60,000)*

40%

$(24,000)

*(Computation shown on next page.)

(b) Income Tax Expense …………………………………….. 106,000

Deferred Tax Asset ……………………………………….. 24,000

Income Taxes Payable ……………………………. 130,000

(c) Income before income taxes ………………………….. $265,000a

Income tax expense

Current ………………………………………………….. $130,000

Deferred ………………………………………………… (24,000) 106,000

PROBLEM 19-8 (Continued)

Book Depreciation

Tax Depreciation

bDifference

2014

$120,000

$ 60,000*

($ 60,000

2015

120,000

120,000

0

2016

2017

2018

2019

0

( (60,000)

Totals

$600,000

($ 0

(d)

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

$ (60,000)

40%

$(24,000)

40%

(75,000)

40%

$(210,000)

Temporary

Difference

Resulting Deferred Tax

Related Balance

Sheet Account

Classification

(Asset)

Liability

Depreciation

$(24,000)

Plant Assets

Noncurrent

Unearned Rent

Current

Unearned rent

Noncurrent

$(84,000)

Current assets

Deferred tax asset …………………………..……………………… $30,000

PROBLEM 19-8 (Continued)

(e) Income Tax Expense ………………………………………. 44,000

Deferred Tax Asset …………………………………………. 60,000

Income Taxes Payable ……………………………… 104,000

Deferred tax benefit for 2015 …………………………………………. $ (60,000)

Current tax expense for 2015 (Income taxes payable) ……… 104,000

Income tax expense for 2015 …………………………………………. $ 44,000

(f) Income before income taxes ……………………………. $110,000d

Income tax expense

Current ……………………………………………………. $104,000

PROBLEM 19-9

(a) Pretax financial income …………………………………………………. $100,000

Permanent differences:

Fine for pollution ……………………………………………………. 3,500

(b)

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Warranty costs

$ (5,000)

40%

$(2,000)

Construction profits

40%

Depreciation

40%

Totals

$(2,000)

(c) Income Tax Expense ……………………………………….. 40,800

Deferred Tax Asset ………………………………………….. 2,000

Deferred Tax Liability ………………………………… 18,000

Income Taxes Payable ………………………………. 24,800

PROBLEM 19-9 (Continued)

Deferred tax asset at the end of 2015 ……………………………… $ 2,000

Deferred tax asset at the beginning of 2015 ……………………. –0–

Deferred tax benefit for 2015 …………………………………………. $ (2,000)

(d) Income before income taxes ……………………………. $100,000

Income tax expense

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 19-1 (Time 15–20 minutes)

CA 19-2 (Time 20–25 minutes)

CA 19-3 (Time 20–25 minutes)

Purpose—to develop an understanding of temporary and permanent differences. The student is

required to explain the nature of four differences and to explain why each is a permanent or temporary

difference. Two of the four situations are challenging. Also, the nature of and the classification of deferred

tax accounts are examined.

CA 19-4 (Time 20–25 minutes)

Purpose—to develop an understanding of deferred taxes and balance sheet disclosure. This case has

CA 19-5 (Time 20–25 minutes)

CA 19-6 (Time 20–25 minutes)

Purpose—to develop an understanding of the concept of future taxable amounts and future deductible

CA 19-7 (Time 20–25 minutes)

Purpose—to provide the student an opportunity to examine the income effects of deferred taxes,

including ethical issues.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 19-1

(a) The objectives in accounting for income taxes are:

(b) To implement the objectives, the following basic principles are applied in accounting for income

taxes at the date of the financial statements:

1. A current tax liability or asset is recognized for the estimated taxes payable or refundable

benefits that, based on available evidence, are not expected to be realized.

(c) The procedures for the annual computation of deferred income taxes are as follows:

1. Identify: (1) the types and amounts of existing temporary differences and (2) the nature and

amount of each type of operating loss and tax credit carryforward and the remaining length

CA 19-2

(a) The following basic principles are applied in accounting for income taxes at the date of the

financial statements:

1. A current tax liability or asset is recognized for the estimated taxes payable or refundable

(b) Dexter should do the following in accounting for the temporary differences.

1. Identify the types and amounts of existing temporary differences. The depreciation policies

give rise to a temporary difference that will result in net future taxable amounts (because

CA 19-2 (Continued)

(c) Deferred tax accounts are reported on the balance sheet as assets and liabilities. They should be

classified in a net current and a net noncurrent amount. An individual deferred tax liability or

asset is classified as current or noncurrent based on the classification of the related asset or

CA 19-3

(a) 1. Temporary difference. The full estimated three years of warranty costs reduce the current

year’s pretax financial income, but will reduce taxable income in varying amounts each

respective year, as paid. Assuming the estimate as to each warranty is valid, the total

2. Temporary difference. The difference between the tax basis and the reported amount (book

basis) of the depreciable property will result in taxable or deductible amounts in future years

when the reported amount of the asset is recovered (through use or sale of the asset);

hence, it is a temporary difference.

3. Temporary difference and permanent difference. The investor’s share of earnings of an

investee (other than subsidiaries and corporate joint ventures) accounted for by the equity

method is included in pretax financial income while only 20% of dividends received from

CA 19-3 (Continued)

4. Temporary difference. For financial reporting purposes, any gain experienced in an

involuntary conversion of a nonmonetary asset to a monetary asset must be recognized in

the period of conversion. For tax purposes, this gain may be deferred if the total proceeds

are reinvested in replacement property within a certain period of time. When such a gain is

CA 19-4

Part A.

(a) Deferred income taxes are reported in the financial statements when temporary differences exist

at the balance sheet date. Deferred taxes are never reported for permanent differences.

The tax consequences of most events recognized in the financial statements for a year are

(b) 1. Gross profit on installment sales—Deferred income taxes would be recognized when gross

profit on installment sales is included in pretax financial income in the year of sale and

included in taxable income when later collected.

2. Revenues on long-term construction contracts—Deferred income taxes would be recog–

CA 19-4 (Continued)

Part B.

Deferred income taxes related to a noncurrent asset or liability would be classified as a noncurrent item

in the balance sheet. Deferred income taxes are related to an asset or liability if reduction of the asset

or liability causes the underlying temporary difference to reverse.

CA 19-5

(a) The 45% tax rate would be used in computing the deferred tax liability at December 31, 2014, if a

net operating loss (an NOL) is expected in 2015 that is to be carried back to 2014 (the enacted

tax rate is 45% in 2014). (See discussion below.)

Discussion:

In determining the future tax consequences of temporary differences, it is helpful to prepare a schedule

which shows in which future years existing temporary differences will result in taxable or deductible

amounts. The appropriate enacted tax rate is applied to these future taxable and deductible amounts.

CA 19-5 (Continued)

For future taxable amounts:

1. If taxable income is expected in the year that a future taxable amount is scheduled, use the

For future deductible amounts:

1. If taxable income is expected in the year that a future deductible amount is scheduled, use the

CA 19-6

(a) Future taxable amounts increase taxable income relative to pretax financial income in the future

due to temporary differences existing at the balance sheet date. Future deductible amounts decrease

tax consequences attributable to the future deductible amounts scheduled.

(b) The carryback and carryforward provisions will affect the amounts to be reported for the resulting

deferred tax asset and deferred tax liability.

In computing deferred tax account balances to be reported at a balance sheet date, the appropri-

For future taxable amounts:

1. If taxable income is expected in the year that a future taxable amount is scheduled, use the

calculate the related deferred tax liability.

For future deductible amounts:

1. If taxable income is expected in the year that a future deductible amount is scheduled, use

CA 19-7

(a) To realize a sizable deferred tax liability, Acme must have used an accelerated depreciation

method for tax purposes while using straight-line depreciation for its financial statements. Once

the temporary difference reversed, taxable income would exceed financial accounting income.

(b) The deferral of income taxes means that due to temporary differences caused by the difference

in financial accounting principles and tax laws, a company will be able to defer paying its income

(c) The primary stakeholders who could be harmed by Acme’s income tax practice are the federal

(d) As a CPA, Stephanie is obligated to uphold objectivity and integrity in the practice of financial

its income taxes which should not be considered unethical.