PROBLEM 13-7

(a)

(1)

Cash ……………………………………………………….

4,440,000

Sales Revenue (600 X $7,400) …………………………..

4,440,000

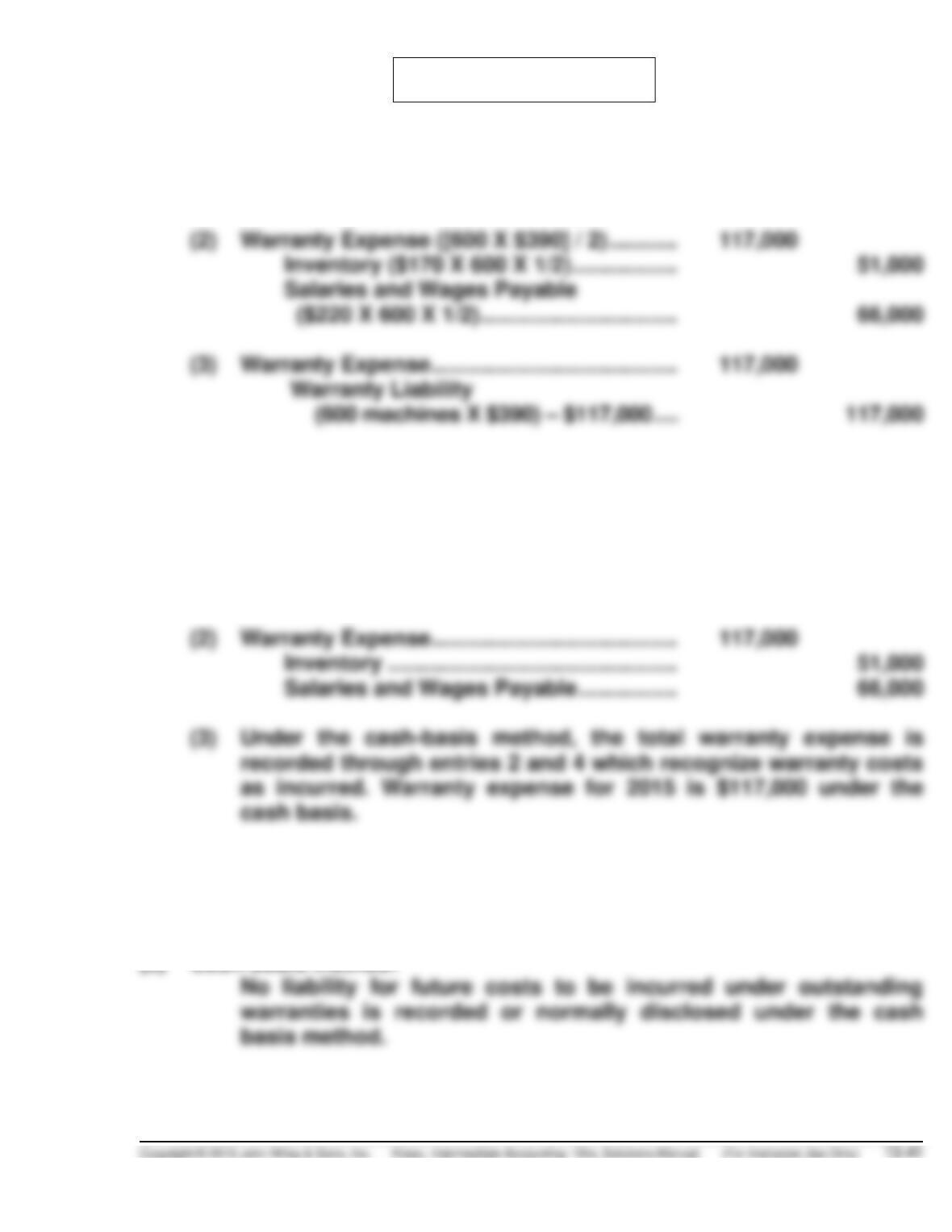

(2)

Warranty Expense ([600 X $390] / 2) ………………………….

117,000

Inventory ($170 X 600 X 1/2) …………………………..

51,000

(3)

Warranty Expense ……………………………………………………

Warranty Liability

(600 machines X $390) – $117,000 …………………….

(4)

Warranty Liability …………………………………………………….

117,000

Inventory ……………………………………………………….

51,000

Salaries and Wages Payable …………………………..

66,000

(b)

(1)

Cash ……………………………………………………….

4,440,000

Sales Revenue ………………………………………………….

4,440,000

(2)

Warranty Expense ……………………………………………………

117,000

Inventory ……………………………………………………….

51,000

Salaries and Wages Payable …………………………..

66,000

(4)

Warranty Expense ……………………………………………………

117,000

Inventory ……………………………………………………….

51,000

Salaries and Wages Payable …………………………..

66,000

(c)

Cash-basis method:

PROBLEM 13-7 (Continued)

Expense warranty accrual method:

As of 12/31/14 the balance sheet would disclose a current liability

in the amount of $117,000 for Warranty Liability.

(d)

In the case of Alvarado Company, the expense warranty accrual method

reflects properly the income resulting from operations in 2014 and 2015

PROBLEM 13-8

Inventory of Premiums ……………………………………………

60,000

Cash ………………………………………………………………

60,000

(To record purchase of 40,000 puppets at

$1.50 each)

Cash …………………………..………………………………………….

Sales Revenue ………………………………………………..

(To record sales of 480,000 boxes at

$3.75 each)

Premium Expense …………………………………………………..

34,500

Inventory of Premiums ……………………………………

[To record redemption of 115,000 coupons.

Computation: (115,000 ÷ 5) X $1.50 = $34,500]

Premium Expense …………………………………………………..

23,100

Premium Liability ……………………………………………

23,100

[To record estimated liability for premium

claims outstanding at December 31, 2015.]

Computation: Total coupons issued in 2015……………..

480,000

Total estimated redemptions (40%) ………………………….

Coupons redeemed in 2015 ……………………………………..

Estimated future redemptions …………………………..……..

Cost of estimated claims outstanding (77,000 ÷ 5) X $1.50 = $23,100

PROBLEM 13-9

(a) 2014

Inventory of Premiums …………………………..………………..

562,500

Cash ………………………………………………………………

562,500

(To record the purchase of 250,000

MP3 downloads at $2.25 each)

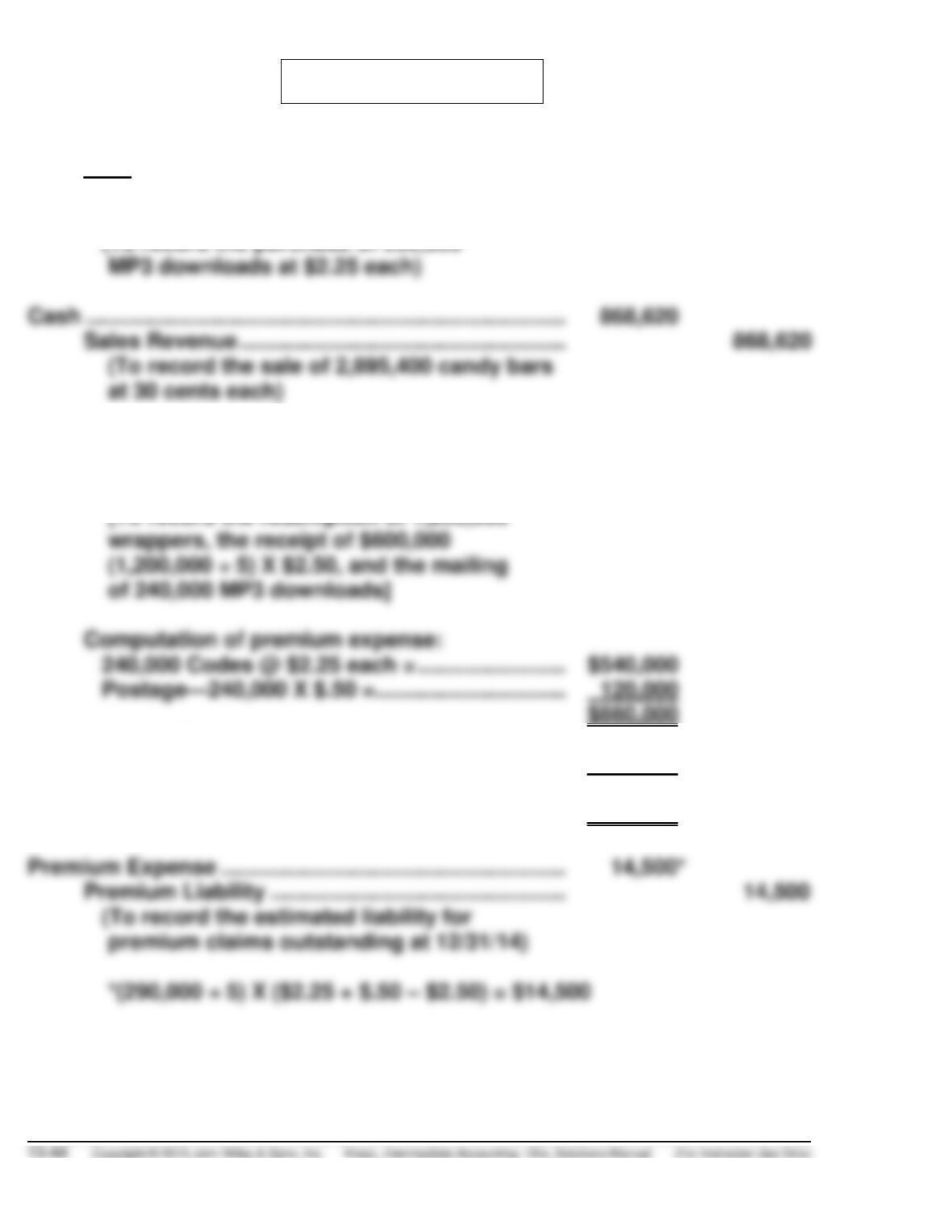

Cash ………………………………………………………………………

868,620

Sales Revenue ………………………………………………..

868,620

(To record the sale of 2,895,400 candy bars

at 30 cents each)

Cash [$600,000 – (240,000 X $.50)] …………………………..

480,000

Premium Expense …………………………………………………..

60,000

Inventory of Premiums …………………………………….

540,000

[To record the redemption of 1,200,000

wrappers, the receipt of $600,000

(1,200,000 ÷ 5) X $2.50, and the mailing

of 240,000 MP3 downloads]

240,000 Codes @ $2.25 each = ………………………

Postage—240,000 X $.50 = …………………………..

120,000

Less: Cash received—

240,000 X $2.50 …………………………………

600,000

Premium expense for MP3 downloads

issued ………………………………………………………

$ 60,000

Premium Expense …………………………………………………..

Premium Liability …………………………..……………….

(To record the estimated liability for

premium claims outstanding at 12/31/14)

PROBLEM 13-9 (Continued)

2015

Inventory of Premiums ……………………………………………

742,500

Cash ………………………………………………………………

742,500

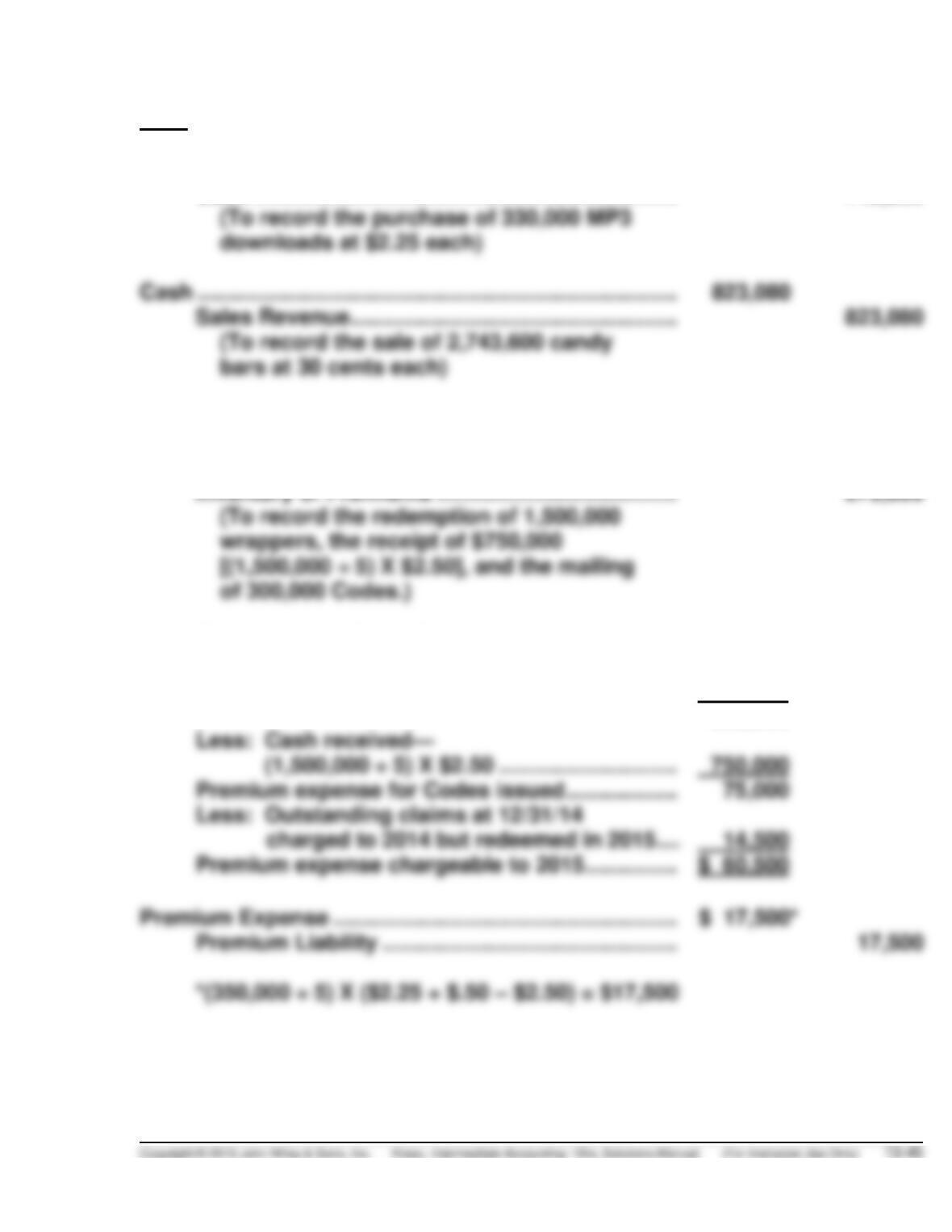

Cash …………………………..………………………………………….

823,080

Sales Revenue ………………………………………………..

(To record the sale of 2,743,600 candy

bars at 30 cents each)

Cash ($750,000 – $150,000) ……………………………………..

600,000

Premium Liability ……………………………………………………

14,500

Premium Expense …………………………………………………..

60,500

Inventory of Premiums ……………………………………

675,000

(To record the redemption of 1,500,000

wrappers, the receipt of $750,000

[(1,500,000 ÷ 5) X $2.50], and the mailing

of 300,000 Codes.)

Computation of premium expense:

300,000 Codes @ $2.25 = ………………………………

$675,000

Postage—300,000 @ $.50 = …………………………

150,000

825,000

Less: Cash received—

(1,500,000 ÷ 5) X $2.50 …………………………..

750,000

Premium expense for Codes issued …………………

75,000

Less: Outstanding claims at 12/31/14

charged to 2014 but redeemed in 2015 …….

Premium Expense …………………………………………………..

$ 17,500*

Premium Liability ……………………………………………

PROBLEM 13-9 (Continued)

(b)

Amount

Account

2014

2015

Classification

Inventory of Premiums

*

Current asset

Premium Liability

Current liability

*

$2.25 (250,000 – 240,000)

$60,500 + $17,500

PROBLEM 13-10

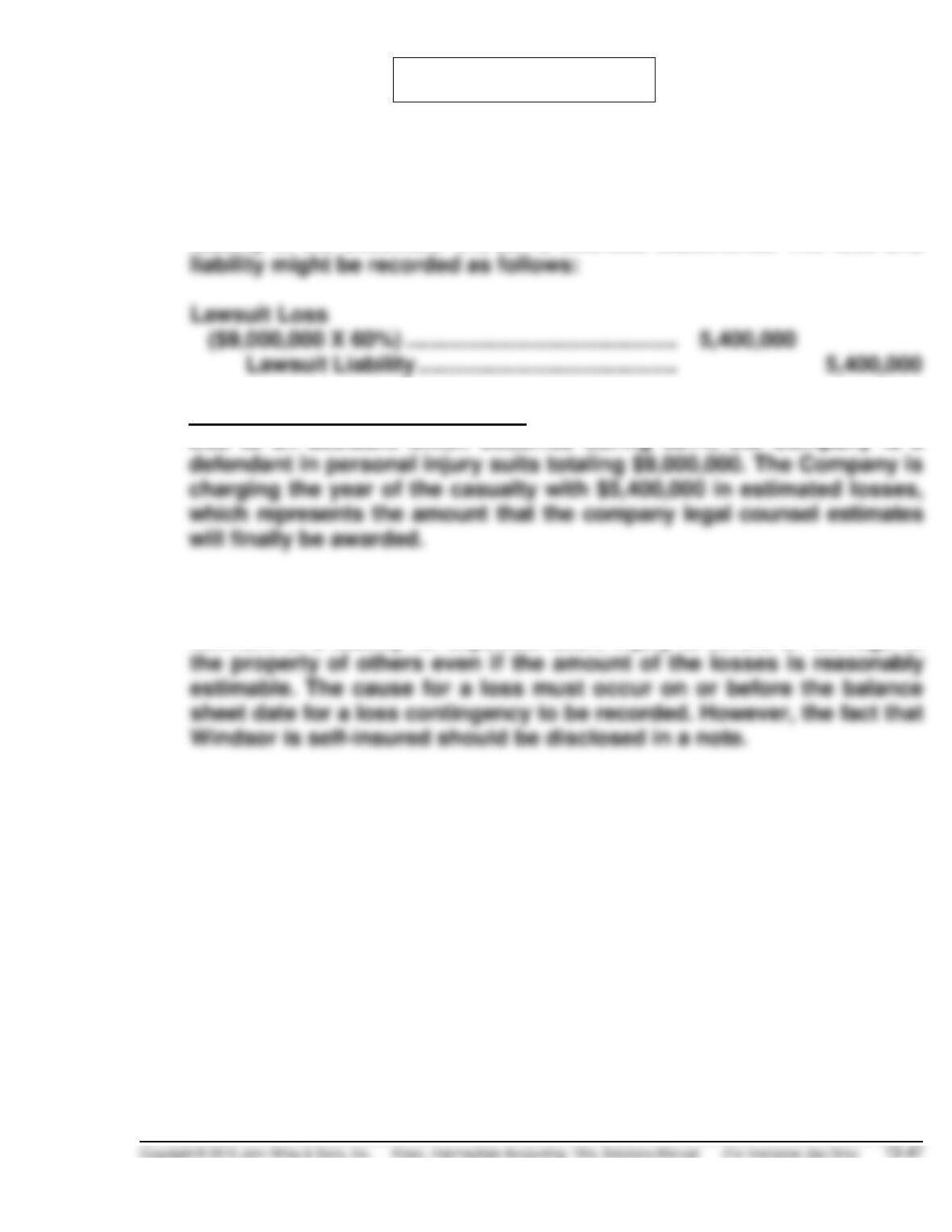

(a) Because the cause for litigation occurred before the date of the finan–

cial statements and because an unfavorable outcome is probable and

reasonably estimable, Windsor Airlines should report a loss and a

liability in the December 31, 2014, financial statements. The loss and

Note to the Financial Statements

Due to an accident which occurred during 2014, the Company is a

(b) Windsor Airlines need not establish a liability for risk of loss from lack

of insurance coverage itself. GAAP does not require or allow the estab-

lishment of a liability for expected future injury to others or damage to

PROBLEM 13-11

(a)

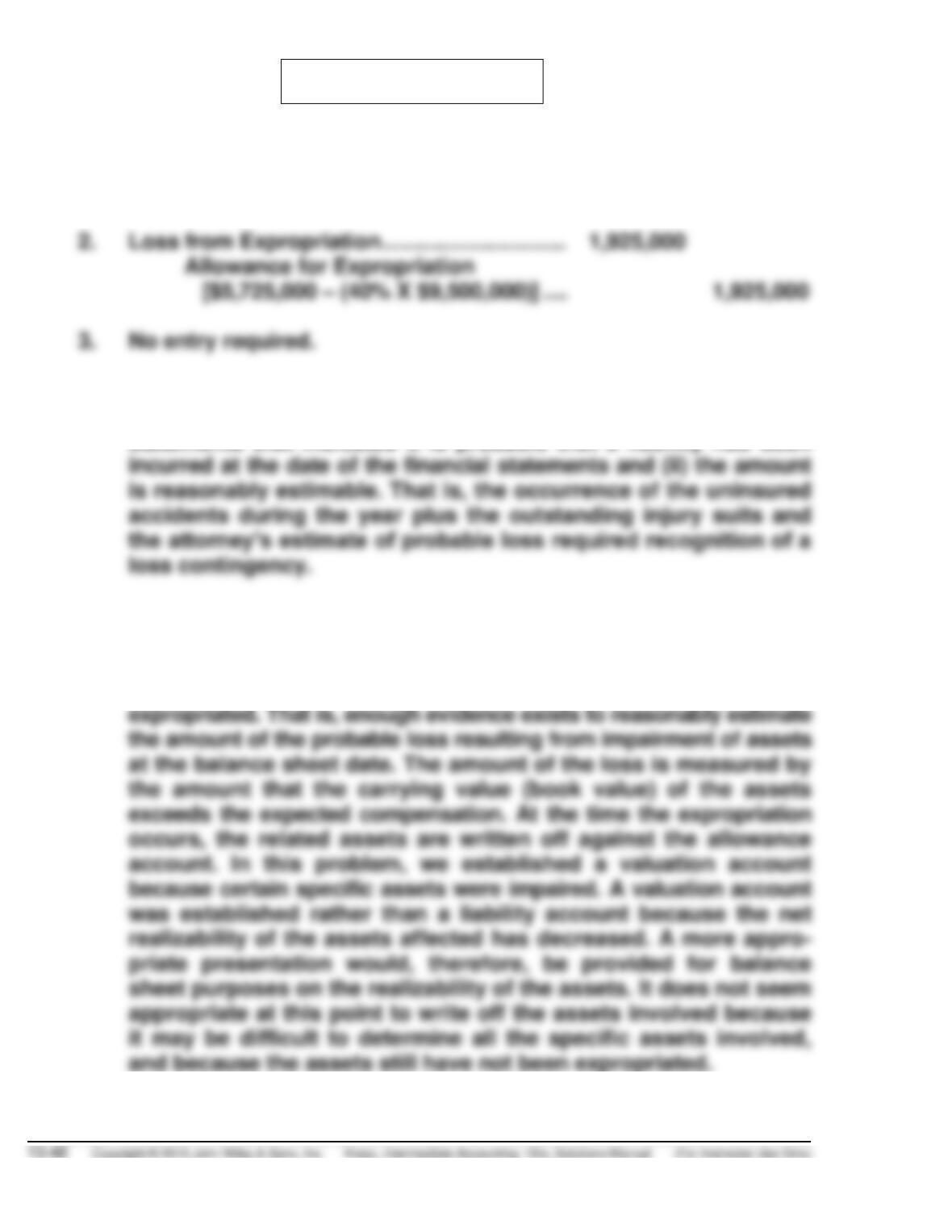

1.

Lawsuit Loss ……………………………………………………….

250,000

Lawsuit Liability ……………………………………………..

250,000

2.

Loss from Expropriation …………………………..

Allowance for Expropriation

No entry required.

(b)

1.

A loss and a liability have been recorded in the first case because

(i) information is available prior to the issuance of the financial

statements that indicates it is probable that a liability had been

2.

An entry to record a loss and establish an allowance due to threat

of expropriation is necessary because the expropriation is imminent

as evidenced by the foreign government’s communicated intent

to expropriate and the prior settlements for properties already

PROBLEM 13-11 (Continued)

3.

Even though Polska’s chemical product division is uninsurable

due to high risk and has sustained repeated losses in the past, as

of the balance sheet date no assets have been impaired or liabili–

ties incurred nor is an amount reasonably estimable. Therefore,

this situation does not satisfy the criteria for recognition of a loss

PROBLEM 13-12

(a)

Sales of musical instruments and sound equipment ……….

$5,700,000

Estimated warranty cost ………………………………………………..

X .02

Warranty expense for 2014 …………………………………….

$ 114,000

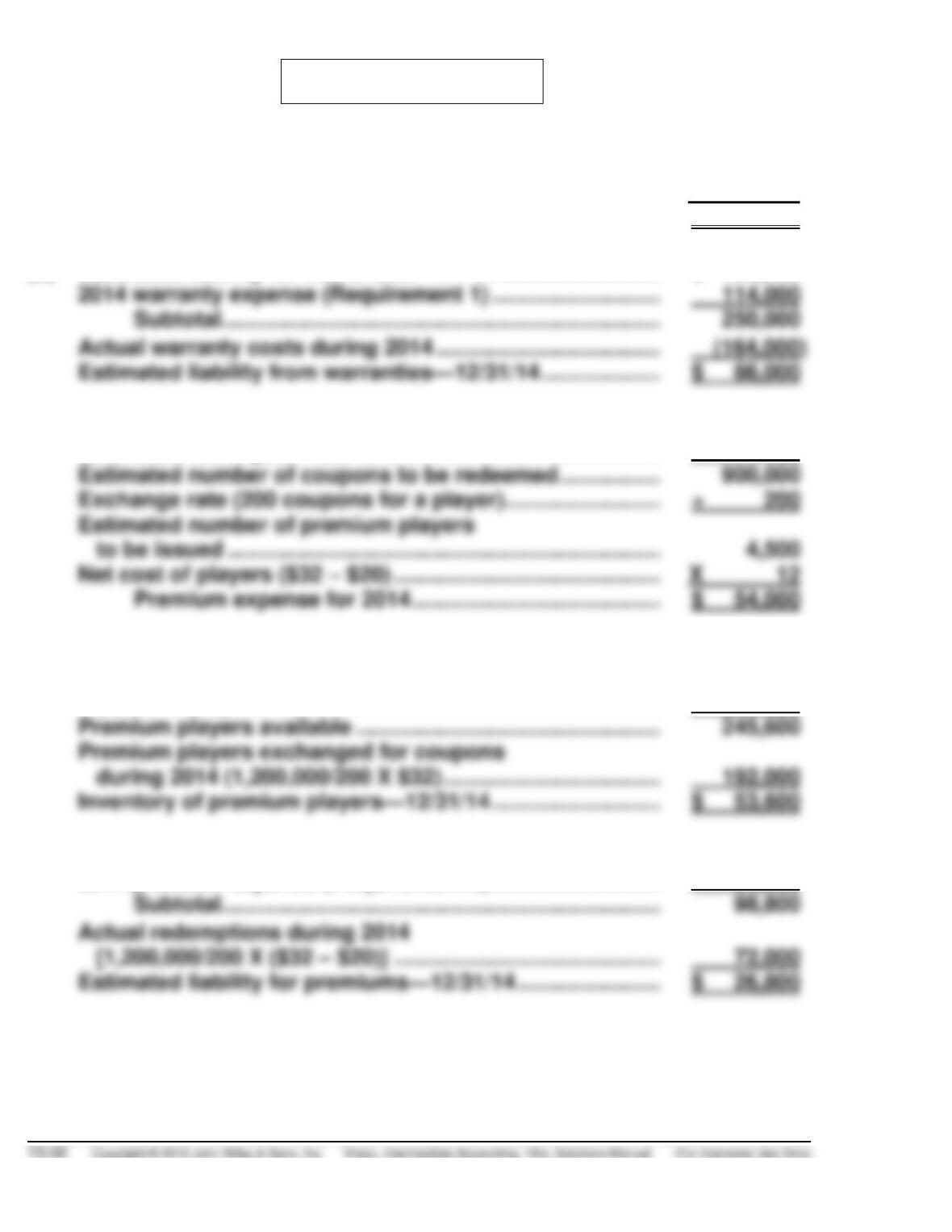

(b)

Estimated liability for warranties—1/1/14 ………………………..

$ 136,000

114,000

Subtotal ………………………………………………………………..

Actual warranty costs during 2014 …………………………………

Estimated liability from warranties—12/31/14 ………………….

$ 86,000

(c)

Coupons issued (1 coupon/$1 sale) ……………………………….

1,500,000

Estimated redemption rate …………………………………………….

.60

Estimated number of coupons to be redeemed ……………….

Exchange rate (200 coupons for a player) ……………………….

÷ 200

Estimated number of premium players

to be issued ……………………………………………………………….

Net cost of players ($32 – $20) ……………………………………….

X 12

Premium expense for 2014 …………………………………….

$ 54,000

(d)

Inventory of premium players—1/1/14 …………………………..

$ 37,600

Premium players purchased during 2014

(6,500 X $32) ………………………………………………………………

208,000

Premium players available …………………………………………….

Premium players exchanged for coupons

192,000

Inventory of premium players—12/31/14 …………………………

$ 53,600

(e)

Estimated liability for premiums—1/1/14 …………………………

$ 44,800

2014 premium expense (Requirement 3) …………………………

54,000

Subtotal ………………………………………………………………..

Actual redemptions during 2014

[1,200,000/200 X ($32 – $20)] ……………………………………….

72,000

Estimated liability for premiums—12/31/14 ……………………..

$ 26,800

PROBLEM 13-13

1. Memo prepared by:

Date:

Millay Corporation

December 31, 2014

Recognition of Warranty Expense

During June of this year, the client began the manufacture and sale of a

new line of dishwasher. Sales of 120,000 dishwashers during this period

amounted to $60,000,000. These dishwashers were sold under a one-year

warranty, and the client estimates warranty costs to be $25 per appliance.

Because Millay accounts for warranties on the accrual basis, it must recog-

nize the entire $3,000,000 as warranty expense in the year of sale. The client

should have made the following journal entries:

(a) Cash ………………………………………………………….. 60,000,000

Sales Revenue (120,000 X $500) ………….. 60,000,000

(To record sale of 120,000 dishwashers)

2. Memo prepared by:

Date:

Millay Corporation

December 31, 2014

Loss Contingency from Violation

Of EPA Regulations

I contacted the client’s counsel via a routine attorney letter, asking for

Although the litigation is pending, Sondgeroth believes that the suit will

probably be lost. A reasonable estimate of clean up costs and fines is

$2,750,000. The client neither disclosed nor accrued this loss in the finan–

cial statements.

3. Memo prepared by:

Date:

Millay Corporation

December 31, 2014

Loss Contingency on

Patent Infringement Litigation

In answer to my attorney letter requesting information about any possible

litigation associated with the client, Morgan Sondgeroth informed me that

the client is in the middle of a patent infringement suit with Megan Drabek

PROBLEM 13-14

1. Estimated warranty costs:

On 2013 sales $ 800,000 X .10 …………………………..

$ 80,000

On 2014 sales $1,100,000 X .10 …………………………..

110,000

On 2015 sales $1,200,000 X .10 …………………………..

Total estimated costs …………………………………

310,000

Total warranty expenditures ……………………….

85,700*

2.

Computation of liability for premium claims outstanding:

Unredeemed coupons for 2014

($9,000 – $8,000) ……………………………………………..

($30,000 X .40) ………………………………………………..

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 13-1 (Time 20–25 minutes)

Purpose—to provide the student with the opportunity to define a liability, to distinguish between current

and long-term liabilities, and to explain accrued liabilities. The student must also describe how liabilities

are valued, explain why notes payable are usually reported first in the current liabilities section, and to

indicate the items that may comprise “compensation to employees.”

CA 13-2 (Time 15–20 minutes)

CA 13-3 (Time 30–40 minutes)

Purpose—to provide the student with a comprehensive case covering refinancing of short-term debt.

CA 13-4 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to comment on the proper treatment in the

CA 13-5 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to specify the conditions by which a loss

CA 13-6 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to discuss how product warranty costs and the fact

that a company is being sued should be reported.

CA 13-7 (Time 20–25 minutes)

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 13-1

(a) A liability is defined as “probable future sacrifices of economic benefits arising from present

obligations of a particular entity to transfer assets or provide services to other entities in the future

as a result of past transactions or events.” In other words, it is an obligation to transfer some type

of resource in the future as a result of a past transaction.

(d) Theoretically, liabilities should be measured by the present value of the future outlay of cash

required to liquidate them. But in practice, current liabilities are usually recorded in accounting

records and reported in financial statements at their maturity value. Because of the short time

periods involved—frequently less than one year—the difference between the present value of a

current liability and the maturity value is not large. The slight overstatement of liabilities that results

from carrying current liabilities at maturity value is accepted on the grounds it is immaterial.

CA 13-2

1. Since the notes payable are due in less than one year from the balance sheet date, they would

generally be reported as a current liability. The only situation in which this short-term obligation

could possibly be excluded from current liabilities is if Rodriguez Corp. intends to refinance it. For

those notes to qualify for exclusion from current liabilities, the company must meet the following

criteria:

(1) It must intend to refinance the obligation on a long-term basis, and

CA 13-2 (Continued)

2. Generally, deposits from customers would be classified as a current liability. However, the

classification of deposits as current or noncurrent depends on the time involved between the date

3. Salaries and wages payable is an accrued liability which in almost all circumstances would be

reported as a current liability (could not be excluded).

CA 13-3

(This case requires some research of FASB Codification.)

(a) No. GAAP indicates that refinancing a short-term obligation on a long-term basis means either replacing

it with a long-term obligation or with equity securities, or renewing, extending, or replacing it with

(b) Yes. The events described will have an impact on the financial statements. Since Dumars Corpo-

ration refinanced the long-term debt maturing in March 2015 in a manner that meets the conditions

set forth in GAAP that obligation should be excluded from current liabilities. The $10,000,000

(c) No. since Dumars Corporation refinanced the long-term debt maturing in March 2015 in a manner

that meets the conditions set forth in GAAP that obligation should be excluded from current liabilities.

(d) (1) No. The $10,000,000 should be shown under the caption of either “Long–Term Debt,” “Interim

Debt,” “Short–Term Debt Expected to Be Refinanced,” or “Intermediate Debt.”

CA 13-4

Because the casualty occurred subsequent to the balance sheet date, it does not meet the criteria of a

loss contingency; that is, an asset had not been impaired or a liability incurred at the date of the

balance sheet. Therefore, a loss contingency should not be accrued by a charge to expense due to the

CA 13-5

(a) Two conditions must exist before a loss contingency is recorded:

1. Information available prior to the issuance of the financial statements indicates that it is

probable that a liability has been incurred at the date of the financial statements.

2. The amount of the loss can be reasonably estimated.

(b) When some amount within the range appears at the time to be a better estimate than any other

CA 13-6

Part 1. For Product Grey, the estimated product warranty costs should be accrued by a charge to

expense and a credit to a liability because both of the following conditions were met:

1. It is probable that a liability has been incurred based on past experience.

2. The amount of the loss can be reasonably estimated as 1% of sales.

Part 2. The probable judgment ($1,000,000) should be accrued by a charge to expense and a credit to

a liability because both of the following conditions were met:

1. It is probable that a liability has been incurred because Constantine’s lawyer states that it is

probable that Constantine will lose the suit.

CA 13-6 (Continued)

Constantine should disclose in its financial statements or notes the following:

CA 13-7

(a) No, Hamilton should not follow his owner’s directive if his (Hamilton’s) original estimates are

reasonable.

(b) Rich Clothing Store benefits in lower rental expense. The Dotson Company is harmed because the

FINANCIAL REPORTING PROBLEM

(a) P&G’s short-term borrowings were $9,981 at June 30, 2011. (in

$ millions)

SHORT-TERM DEBT

(In millions)

2011

Commercial paper

Total short-term debt

(b) 1. Working capital = Current assets less current liabilities.

($5,323) = ($21,970 – $27,293)

While P&G’s current and acid-test ratios are below one, this may not

indicate a weak liquidity position. Many large companies carry relatively