CHAPTER 16

SOLUTIONS TO B EXERCISES

E16-1B (15–20 minutes)

1. Cash ($50,000,000 X 1.02) ……………………….. 51,000,000

2. Cash ……………………………………………………… 35,350,000

Bonds Payable …………………………………. 35,000,000

Premium on Bonds Payable ……………… 122,500

3. Debt Conversion Expense ………………………. 355,000

Bonds Payable ………………………………………. 60,000,000

Premium on Bonds Payable ……………………. 155,000

E16-2B (15–20 minutes)

(a) Interest Payable ($900,000 X 4/6) …………………….. 600,000

Interest Expense ($900,000 X 2/6) + $1,890 …………. 301,890

Discount on Bonds Payable ……………………… 1,890

Cash ($15,000,000 X 12% ÷ 2) ……………………. 900,000

(b) Bonds Payable ………………………………………………. 7,500,000

Discount on Bonds Payable ………………………. 221,218

E16-3B (10–20 minutes)

Conversion recorded at book value of the bonds:

Bonds Payable ……………………………………………………… 5,600,000

Premium on Bonds Payable ………………………………….. 150,000

E16-4B (15–20 minutes)

(a) Cash ……………………………………………………….. 26,500,000

Bonds Payable ………………………………….. 25,000,000

Premium on Bonds Payable ………………. 1,500,000

(b) Bonds Payable ………………………………………… 10,000,000

Schedule 1

Computation of Unamortized Premium on Bonds Converted

Premium on bonds payable on July 1, 2013 …………… $1,500,000

Schedule 2

Computation of Common Stock Resulting from Conversion

Number of shares convertible on January 1, 2013: Number of bonds

($25,000,000 ÷ $1,000) ……………………………………………. 25,000

Number of shares for each bond ………………………… X 10 250,000

E16-5B (10–20 minutes)

Interest Expense …………………………………………………… 153,395

Discount on Bonds Payable

[$110,050 ÷ 162 = $679; $679 X 5] ………………… 3,395

E16-6B (25–35 minutes)

(a) December 31, 2013

Bond Interest Expense …………………………………….. 56,667

(b) January 1, 2014

Bonds Payable ………………………………………………… 400,000

Premium on Bonds Payable ……………………………… 34,667

E16-6B (Continued)

(c) May 31, 2014

Bond Interest Expense …………………………………….. 18,889

Premium on Bonds Payable ……………………………… 1,111

Bond Interest Payable

(d) June 30, 2014

Bond Interest Expense …………………………………….. 11,333

Premium on Bonds Payable ……………………………… 667**

Bond Interest Payable ………………………………………. 20,000

Cash …………………………………………………………. 32,000*

E16-7B (10–15 minutes)

(a) Basic formulas:

Value of bonds without warrants

X Issue price = Value assigned to bonds

Value of bonds without warrants

+ Value of warrants

Value of bonds without warrants

Cash ……………………………………………………………….. 825,000

Discount on Bonds Payable ………………………………

(b) When the warrants are nondetachable, separate recognition is not given

to the warrants. The accounting treatment parallels that given convertible

debt because the debt and equity element cannot be separated.

E16-8B (10–15 minutes)

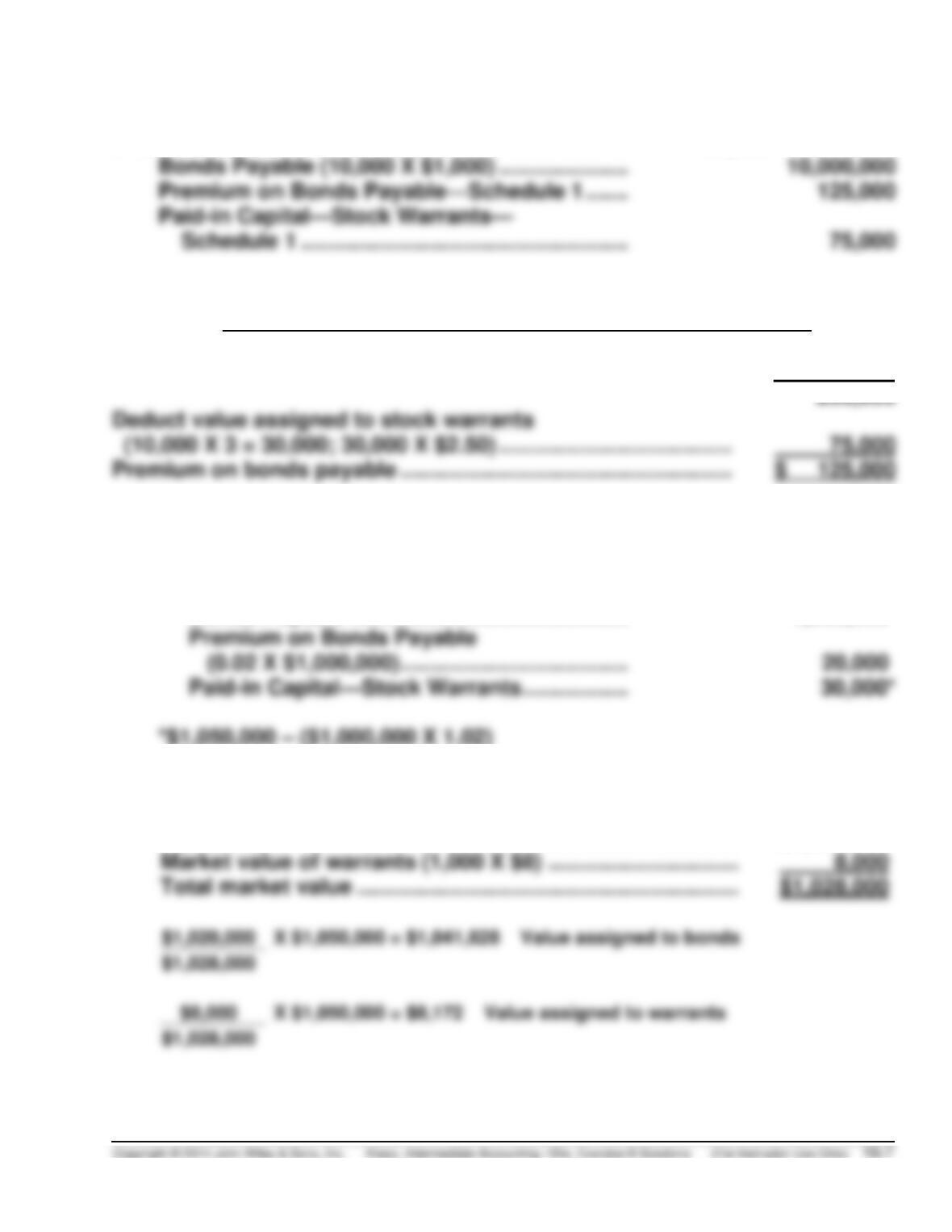

Cash …………………………..……………………………………. 10,135,000

Unamortized Bond Issue Costs …………………………. 65,000

Schedule 1

Premium on Bonds Payable and Value of Stock Warrants

Sales price (10,000 X $1,020) ……………………………………………. $10,200,000

Face value of bonds ………………………………………………………… 10,000,000

E16-9B (10–15 minutes)

(a) Cash ($1,000,000 X 1.05) …………………………….. 1,050,000

Bonds Payable ……………………………………… 1,000,000

*$1,050,000 – ($1,000,000 X 1.02)

(b) Market value of bonds without warrants

($1,000,000 X .1.02) ………………………………………………….. $1,020,000

E16-9B (Continued)

Cash ………………………………………………………… 1,050,000

E16-10B (15–25 minutes)

7/1/14 No entry on adoption of plan

1/1/15 No entry (total compensation cost is $660,000)

12/31/15 Compensation Expense ……………………….. 220,000

Paid-in Capital—Stock Options …………….. 220,000

[To record compensation expense

for 2015 (1/3 X $660,000)]

12/31/16 Compensation Expense ……………………….. 220,000

Paid-in Capital in Excess of Par …….. 7,160,000

(Note: The market price of the stock has no relevance in the prior entry and

the following one.)

E16-11B (15–25 minutes)

1/1/14 No entry – total compensation expense is $1,250,000

7/1/14 No entry – compensation total is now only $1,150,000

E16-12B (15–25 minutes)

7/1/13 No entry

12/31/13 Compensation Expense ……………………….. 87,500

Paid-in Capital—Stock Options

($350,000 X 1/2 X 1/2) ……………….. 87,500

E16-12B (Continued)

7/1/15 Cash (35,000 X $58) …………………………..….. 2,030,000

Paid-in Capital—Stock Options ……………… 245,000*

E16-13B (10–15 minutes)

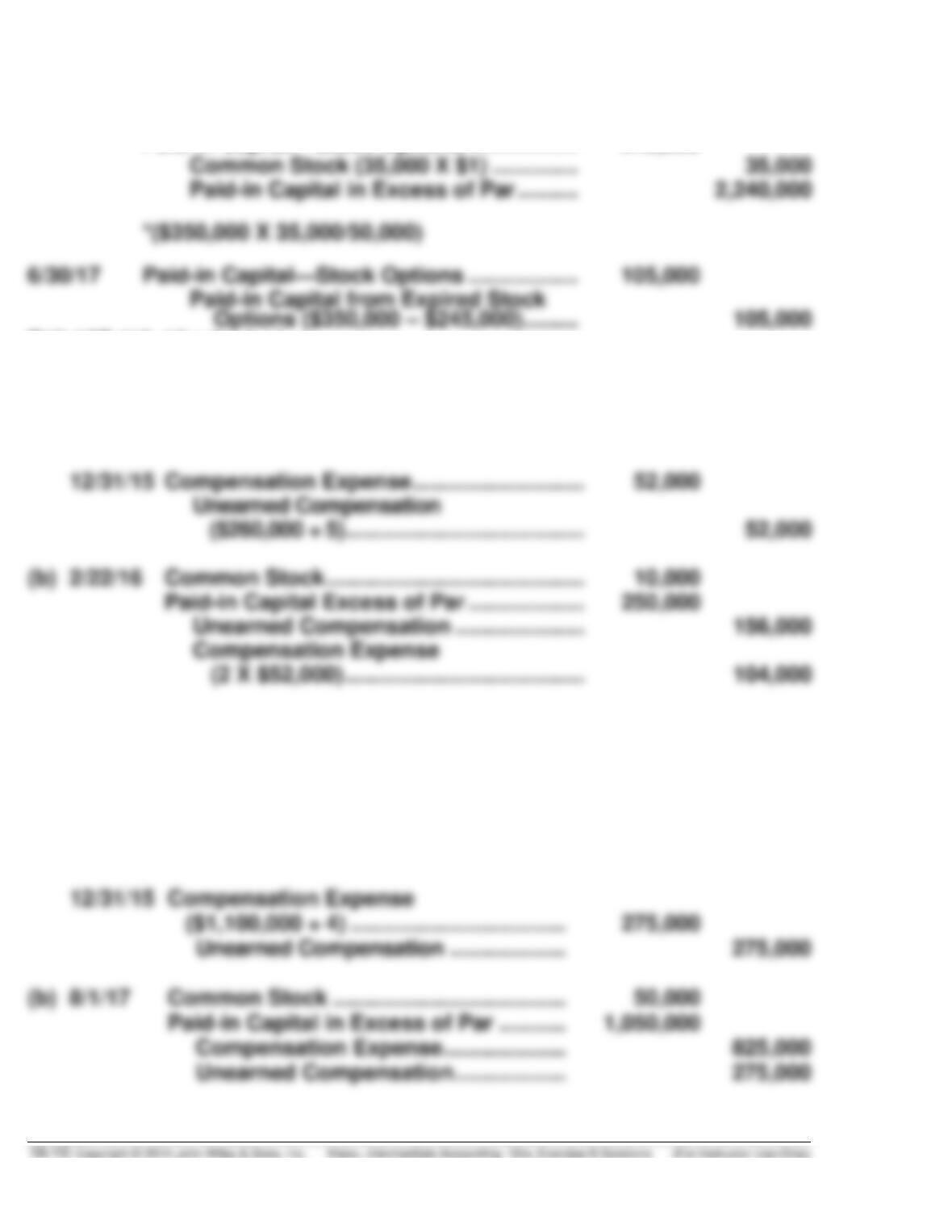

(a) 1/1/14 Unearned Compensation …………………….. 260,000

Common Stock (10,000 X $1) …………… 10,000

Paid-in Capital Excess of Par ………….. 250,000

E16-14B (10–15 minutes)

(a) 1/1/14 Unearned Compensation …………………. 1,100,000

Common Stock ($1 X 50,000) ……….. 50,000

Paid-in Capital in Excess of Par ……. 1,050,000

E16-15B (15–25 minutes)

(a) 10,000,000 shares:

2012 weighted-average number of shares

previously computed ………………………………………. 5,000,000

Retroactive adjustment for stock split ……………………………. X 2

11,500,000

(c) 14,950,000 shares:

2013 weighted average number of shares

previously computed ………………………………………….. 11,500,000

Retroactive adjustment for stock dividend ……………………… X 1.30

14,950,000

15,600,000

E16-16B (10–15 minutes)

(a)

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

Beginning balance

Jan. 1–Mar. 1

2,650,000

1.2 X 2.0

2/12

1,060,000

Issued shares

Mar. 1–Apr. 1

2,900,000

1.2 X 2.0

1/12

580,000

Reacquired shares

Apr. 1–Jul. 1

2,700,000

1.2 X 2.0

3/12

1,620,000

Stock dividend

Jul. 1–Sep. 1

3,240,000

2/12

Reissued shares

Sep. 1–Oct. 1

3,480,000

1/12

580,000

Stock split

Oct. 1–Dec. 31

6,960,000

3/12

1,740,000