PROBLEM 18-13 (Continued)

Balance at repossession ………….. $360*

PROBLEM 18-14

(a) 1. SAPRANO COMPANY

Schedule to Compute Cost

of Goods Sold on Installments

For 2014, 2015, and 2016

2014

2015

2016

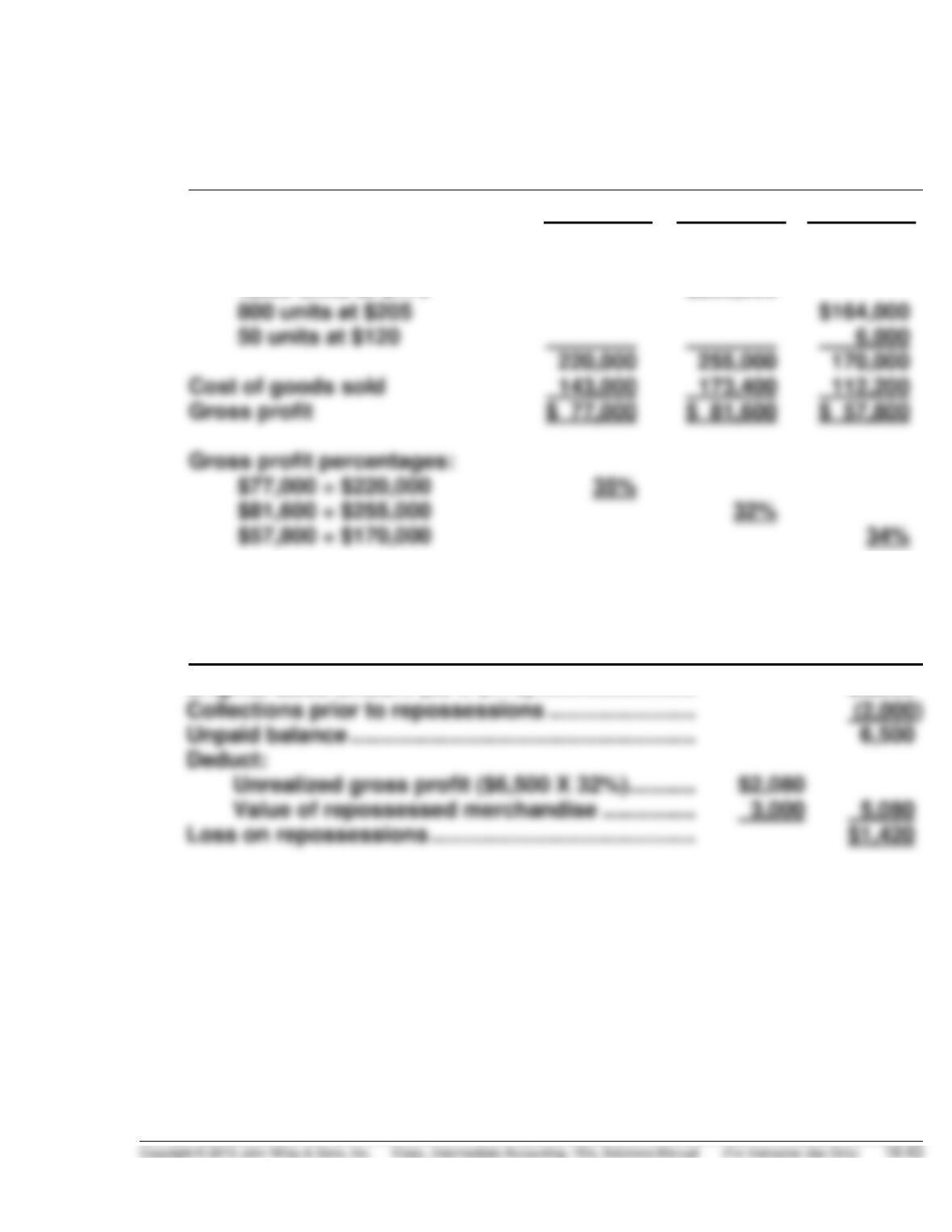

Purchases:

1,400 units at $130

($182,000

1,200 units at $112

$134,400

900 units at $136

Repossessed:

50 units at $60

Inventory at December 31:

Cost of goods sold

2. SAPRANO COMPANY

Schedule to Compute Average Unit Cost

of Goods Sold on Installments

For 2014, 2015, and 2016

2014

2015

2016

2014 ($182,000 ÷ 1,400)

$130

2016 ($125,400* ÷ 950**)

PROBLEM 18-14 (Continued)

(b) SAPRANO COMPANY

Schedule to Compute Gross Profit Percentages

For 2014, 2015, and 2016

2014

2015

2016

Sales:

1,100 units at $200

$220,000

1,500 units at $170

$255,000

800 units at $205

50 units at $120

6,000

Cost of goods sold

Gross profit

$ 77,000

$ 81,600

$ 57,800

Gross profit percentages:

$77,000 ÷ $220,000

$81,600 ÷ $255,000

$57,800 ÷ $170,000

(c) SAPRANO COMPANY

Schedule to Compute Loss on Repossessions

For 2016

Original sales amount (50 X $170) …………………….. $8,500

PROBLEM 18-14 (Continued)

(d) SAPRANO COMPANY

Schedule to Compute Net Income

From Installment Sales

For 2016

Gross profit realized on installment sales:

2016 ($34,600 X 34%) ………………………………………… $11,764

PROBLEM 18-15

(a) MONAT CONSTRUCTION COMPANY, INC.

Computation of Billings on Uncompleted Contract

In Excess of Related Costs

December 31, 2014

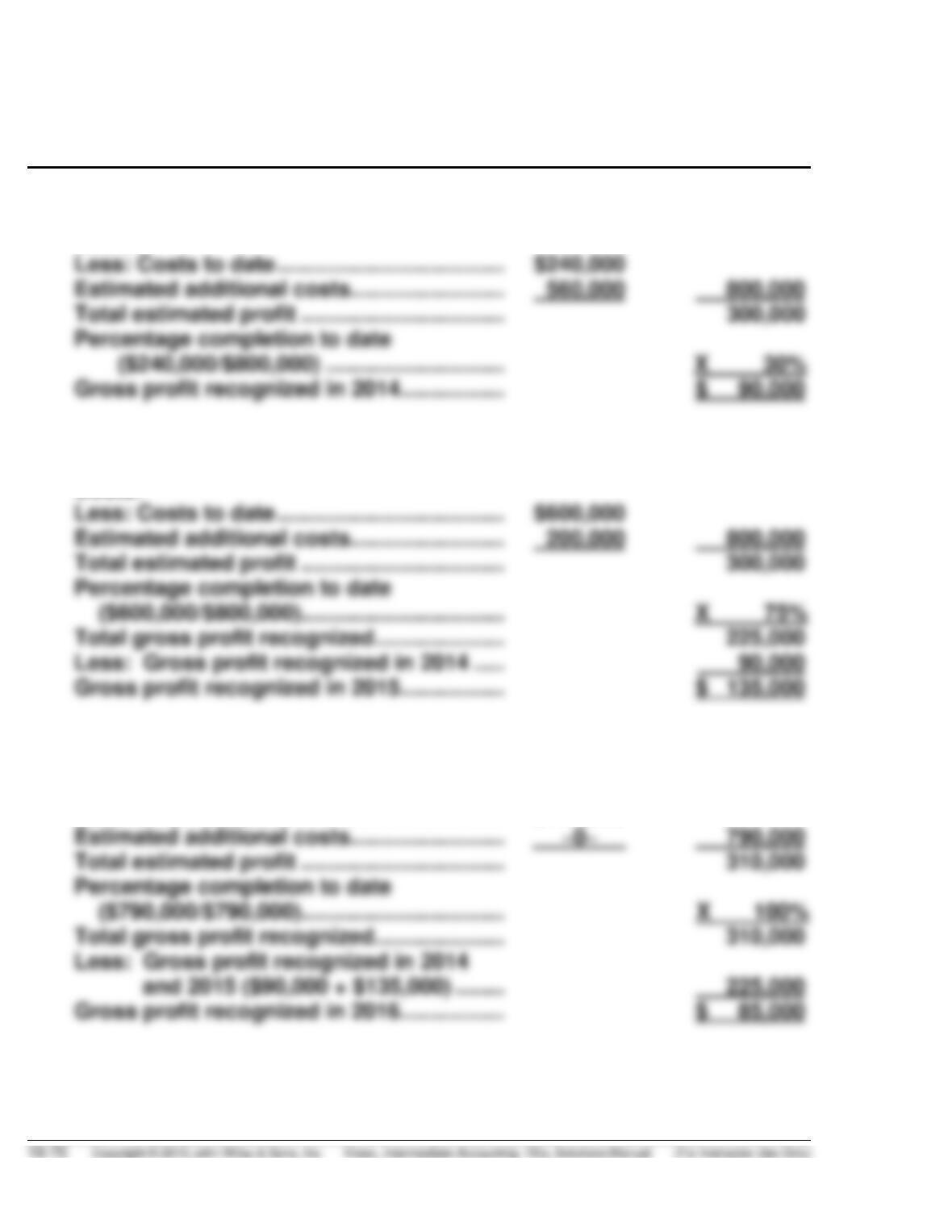

Partial billings on contract during 2014 …………………… $1,400,000

MONAT CONSTRUCTION COMPANY, INC.

Computation of Cost of Uncompleted Contract

In Excess of Related Billings

December 31, 2015

Balance, December 31, 2014—excess of

billings over costs ……………………………………………… $ (260,000)

PROBLEM 18-15 (Continued)

MONAT CONSTRUCTION COMPANY, INC.

Computation of Costs Relating to Substantially

Completed Contract in Excess of Billings

December 31, 2016

Balance, December 31, 2015—excess of costs

over billings …………………………………………………………. $ 490,000

(b) MONAT CONSTRUCTION COMPANY, INC.

Computation of Profit or Loss to be Recognized

On Uncompleted Contract

Year Ended December 31, 2014

Contract price …………………………………………. $4,400,000

Deduct contract costs:

PROBLEM 18-15 (Continued)

MONAT CONSTRUCTION COMPANY, INC.

Computation of Loss to be Recognized

On Uncompleted Contract

Year Ended December 31, 2015

Contract price ……………………………………… $4,400,000

Deduct contract costs:

MONAT CONSTRUCTION COMPANY, INC.

Computation of Loss to Be Recognized

On Substantially Completed Contract

Year Ended December 31, 2016

Contract price …………………………………………………….. $4,400,000

PROBLEM 18-16

Dear Sue:

This letter regards the revenue recognition matter which we discussed earlier.

By using a recognition method called percentage-of-completion, you will

show a profit in every year of the construction project, assuming, of course,

that no unexpected losses occur.

The completed-contract method which you use presumes that revenue

The most frequently used measure of this degree of completion is the cost–

to–cost method, which determines the percentage of a project’s completion

as the ratio of costs that have already been incurred to the total estimated

costs required in order to finish the project. This percentage is then applied

to the total contract price or gross profit to arrive at the amount of revenue

or gross profit recognized for the period.

PROBLEM 18-16 (Continued)

2014 and 2015 actually allow you to show a profit before the project has been

finished. In addition, where applicable, generally accepted accounting princi–

ples require the use of the percentage-of-completion method in preference

PROBLEM 18-16 (Continued)

Percentage-of–Completion Method

Three-Year Schedule of Gross Profit Recognition

Gross profit recognized in 2014:

Contract price ……………………………………… $1,100,000

Costs:

Gross profit recognized in 2015:

Contract price ……………………………………… $1,100,000

Costs:

Gross profit recognized in 2016:

Contract price ……………………………………… $1,100,000

Costs:

Less: Costs to date ………………………………. $790,000

PROBLEM 18-17

(a) Schedule to Compute Gross Profit for 2014

A

B

C

D

E

Estimated profit (loss):

A: ($300,000 – $320,000)

$(20,000)

B: ($350,000 – $339,000)

D: ($200,000 – $205,000)

A: (not applicable)

—

B: ($67,800 ÷ $339,000)

20%

D: (not applicable)

Gross profit (loss) recognized

$(20,000)

Schedule to Compute Unbilled Contract Costs

and Recognized Profit and Billings

in Excess of Costs and Recognized Profit

Costs and

Estimated Profits

or Losses

Related

Billings

Costs and

Estimated Profits

in Excess of Billings

Billings in Excess

of Costs and Estimated

Profits

A

$228,000a

$200,000

$ 28,000

D

PROBLEM 18-17 (Continued)

(b) Partial Income Statement

Revenue from long-term contracts …………………………………. $925,622*

Costs of construction

($252,500 + $67,800 + $186,000 + $120,122 + $190,000) …. 816,422

Gross profit …………………………………………………………………… $109,200

*A: $300,000 X ($248,000 ÷ $320,000) = $232,500

Partial Balance Sheet

Current assets:

Accounts receivable

($830,000 – $765,000) ………………………….. $ 65,000

Project

Costs

Profit/(loss)

Construction

in Process

Billings

A

$248,000

$(20,000)

$228,000

$200,000

E

38,000)

PROBLEM 18-17 (Continued)

(c) Schedule to Compute Gross Profit for 2014

A

B

C

D

E

A: ($300,000 – $320,000)

$(20,000)

B: Not completed

Schedule to Compute Unbilled Contract Costs

and Billings in Excess of Costs

Costs and

Recognized Profits

or Losses

Related

Billings

Costs and

Recognized Losses

in Excess of Billings

Billings in Excess

of Costs

A

a$228,000a

$200,000

$ 28,000

(d) The principal advantage of the completed-contract method is that it

reports revenue based on the final results and not on estimates made

throughout the construction period. However, the disadvantage of

using this method is that for contracts which extend more than one

PROBLEM 18-17 (Continued)

On the other hand, the percentage-of-completion method does recog-

nize revenue and gross profit before the completion of a project. If Buhl

can determine reliable estimates of its progress and meets the other

conditions for this method, Buhl can recognize revenues as the work

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 18-1 (Time 20–30 minutes)

Purpose—to provide a situation that requires an examination and application of the earning and

realization elements of three revenue recognition methods. The three business situations require the

computation of revenue to be recognized.

CA 18-2 (Time 35–45 minutes)

Purpose—to provide the student with an understanding of the conceptual merits of recognizing revenue

CA 18-3 (Time 25–30 minutes)

Purpose—to provide the student with an understanding of the conceptual factors underlying the

CA 18-4 (Time 30–35 minutes)

Purpose—to provide the student with an understanding of the criteria and applications utilized in the

CA 18-5 (Time 35–45 minutes)

Purpose—to provide the student an opportunity to explain how a magazine publisher should recognize

subscription revenue. The case is complicated by a 25% return rate and a premium offered to

subscribers. The effect on the current ratio must be discussed.

CA 18-6 (Time 20–25 minutes)

Purpose—to provide the student an opportunity to discuss the theoretical justification for use of the

CA 18-7 (Time 20–25 minutes)

Purpose—to provide the student an ethical situation related to the recognition of revenue from

membership fees.

*CA 18-8 (Time 35–45 minutes)

Purpose—to provide the student with an understanding of the accounting treatment accorded franchis–

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 18-1

(a) Definitions and descriptions of each of the three noted revenue recognition methods, and an

indication as to whether they are in accordance with generally accepted accounting principles

(GAAP), are presented below.

1. The completion-of-production method allows revenue to be recognized when production

is complete even though a sale has not yet been made. The circumstances that justify

revenue recognition at this point are:

2. The percentage-of-completion method is used on long-term projects and the following

conditions must exist for its use:

• A firm contract price with a high probability of collection.

3. The installment-sales method allows revenue to be recognized when cash is collected

rather than at the point of sale. Due, in part, to improved credit procedures that increase the

(b) The revenue to be recognized in the fiscal year ended November 30, 2014, for each of the three

companies is as calculated and presented below:

1. Farber Mining would recognize as revenue the market value of metals mined during the

year.

CA 18-1 (Continued)

2. Enyart Paperbacks would recognize revenue of $5,600,000, calculated as follows.

Sales in fiscal 2014 ………………………………. $7,000,000

Less: Estimated sales returns

3. Glesen Protection Devices would recognize revenue of $5,000,000. Revenue to be recog-

CA 18-2

(a) The point of sale is the most widely used basis for the timing of revenue recognition because in

most cases it provides the degree of objective evidence accountants consider necessary to reliably

measure periodic business income. In other words, sales transactions with outsiders represent

(b) 1. Though it is recognized that revenue is earned throughout the entire production process,

generally it is not feasible to measure revenue on the basis of operating activity. It is not

feasible because of the absence of suitable criteria for consistently and objectively arriving

at a periodic determination of the amount of revenue to recognize.

2. To criticize the sales basis as not being sufficiently conservative because accounts receiv–

able do not represent disposable funds, it is necessary to assume that the collection of

CA 18-2 (Continued)

factor in the earnings process and substitutes for it the administrative function of managing

and collecting receivables. In other words, the investment of funds in receivables should be

regarded as a policy designed to increase total revenues, properly recognized at the point

of sale, and the cost of managing receivables (e.g., bad debts and collection costs) should

(c) 1. During production. This basis of recognizing revenue is frequently used by firms whose

major source of revenue is long-term construction projects. For these firms the point of sale

is far less significant to the earnings process than is production activity because the sale is

assured under the contract (except of course where performance is not substantially in

accordance with the contract terms).

To defer revenue recognition until the completion of long-term construction projects could

2. When cash is received. The most common application of this basis for the timing of

revenue recognition is in connection with installment-sales contracts. Its use is justified on

the grounds that, due to the length of the collection period, increased risks of default, and

CA 18-3

(a) Most merchandising concerns deal in finished products and would recognize revenue at the point

of sale. This is often identified as the moment when the title legally passes from seller to purchaser.

At the point of sale, there is an arm’s-length transaction to objectively measure the amount of

revenue to be recognized. With accounting theory based heavily on objective measurement, it is

logical that point-of-sale transaction revenue recognition would be used by many firms, especially

merchandising concerns.

Other advantages of point-of-sale timing for revenue recognition include the following:

1. It is a discernible event (as contrasted to the accretion concept).

(b) For service-type transactions, revenue is generally recognized on the basis of the seller’s perform-

ance of the transaction with performance being the execution of a defined act or acts or the passage

of time. Service-type firms may select from recommended methods to recognize revenue:

(1) specific performance method, (2) completed performance method, (3) proportional performance

method, and (4) collection method.

(c) Revenue is sometimes recognized at completion of the production activity, or after the point of

sale. The recognition of revenue at completion of production is justified only if certain conditions

are present. The necessary conditions are that there must be a relatively stable market for the

product, marketing costs must be nominal, and the units must be homogeneous. These three

necessary conditions are not often present except in the case of certain precious metals and

agricultural products. In these situations it has been considered appropriate to recognize revenue

at the completion of production.

CA 18-4

(a) Income results from economic activity in which one entity furnishes goods or services to another.

To warrant revenue recognition, the earnings process must be substantially complete and there

must be a change in net assets that is capable of being objectively measured. Normally, this

involves an arm’s-length exchange transaction with a party external to the entity. The existence

and terms of the transaction may be defined by operation of law, by established trade practice, or

may be stipulated in a contract.

(b) Griseta & Dubel Inc., in effect, is a merchandising firm which collects cash (for merchandise

credits) far in advance of furnishing the goods. In addition, since the data indicate that about

5 percent of the credits sold will never be redeemed, it also has revenue from this source unless

these credits are redeemed. Griseta & Dubel’s revenues from these two sources could be recog–

nized on one of three major bases. First, all revenue could be recognized when the credits are

be to recognize the revenue from the never–to–be–redeemed credits on a passage-of-time basis.

The principal expense, merchandise premium costs, should be matched with the revenue. If all

revenue is recognized when credits are sold, an accrual of the cost of the future premium

redemptions would be necessary. In such a case, when credit redemptions and related premium

issuances occurred, the costs of the premiums would be charged to the accrued liability account.

On the other hand, if credit sales were treated as an advance, the deferred revenue would be

recognized and the matching cost of the premiums issued would be recognized with the revenue

at the time of redemption.