ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Principles

Both methods attempt to report revenues that faithfully represent the

operations of the company so that future earnings and cash flows can be

predicted (relevance). With the percentage-of–completion method, companies

use subjective estimates (based on prior experience) of the percent

PROFESSIONAL RESEARCH

(a) See FASB ASC 605-15-15 (Predecessor Literature—FAS 48: Revenue

Recognition When Right of Return Exists)

(b) According to FASB ASC 605-15–15:

15-2 The guidance in this Subtopic applies to the following transactions:

a. Sales in which a product may be returned, whether as a

matter of contract or as a matter of existing practice, either by

the ultimate customer or by a party who resells the product to

(c) According to FASB ASC 605-15–25:

> Sales of Product when Right of Return Exists

25-1 If an entity sells its product but gives the buyer the right to return

the product, revenue from the sales transaction shall be recog–

nized at time of sale only if all of the following conditions are met:

PROFESSIONAL RESEARCH (Continued)

d. The buyer acquiring the product for resale has economic

substance apart from that provided by the seller. This condition

f. The amount of future returns can be reasonably estimated

(see paragraphs 605-15–25-3 through 25-4). Because detailed

record keeping for returns for each product line might be

(d) According to FASB ASC Codification 605-15-25:

25-3 The ability to make a reasonable estimate of the amount of future

returns depends on many factors and circumstances that will

vary from one case to the next. However, any of the following

factors may impair the ability to make a reasonable estimate:

a. The susceptibility of the product to significant external factors,

PROFESSIONAL RESEARCH (Continued)

c. Absence of historical experience with similar types of sales of

similar products, or inability to apply such experience because

PROFESSIONAL SIMULATION

Note: This assignment is available on the Kieso website.

Measurement

Computation of net income for 2015:

Revenues ………………………………………………………….. $5,500,000

Journal Entries

Construction in Process……………………………. 100,000

Materials, Cash, Payables …………………… 100,000

PROFESSIONAL SIMULATION (Continued)

Financial Statements

NOMAR INDUSTRIES, INC.

Balance Sheet

December 31, 2015

Current Assets

Accounts receivable ($230,000 – $202,500) …………………. $27,500

Explanation

Given these facts, a more appropriate revenue recognition policy would be

IFRS CONCEPTS AND APPLICATION

IFRS18-1

The general concepts and principles used for revenue recognition are

IFRS18-2

The cost-recovery method is preferable when the lack of dependable

estimates or inherent hazards cause forecasts to be doubtful.

IFRS18-3

Livesey should use the cost-recovery method. Under the cost-recovery

IFRS18-4

The percentage-of-completion method is preferable when estimates of

costs to complete and extent of progress toward completion of long-term

contracts are reasonably dependable. The percentage-of–completion method

should be used in circumstances when reasonably dependable estimates

can be made and:

(1) The contract clearly specifies the enforceable rights regarding

IFRS18-4 (Continued)

(2) The buyer can be expected to satisfy all obligations under the

contract.

IFRS18-5

Under the cost-recovery method, revenue is recognized up to the amount

IFRS18-6

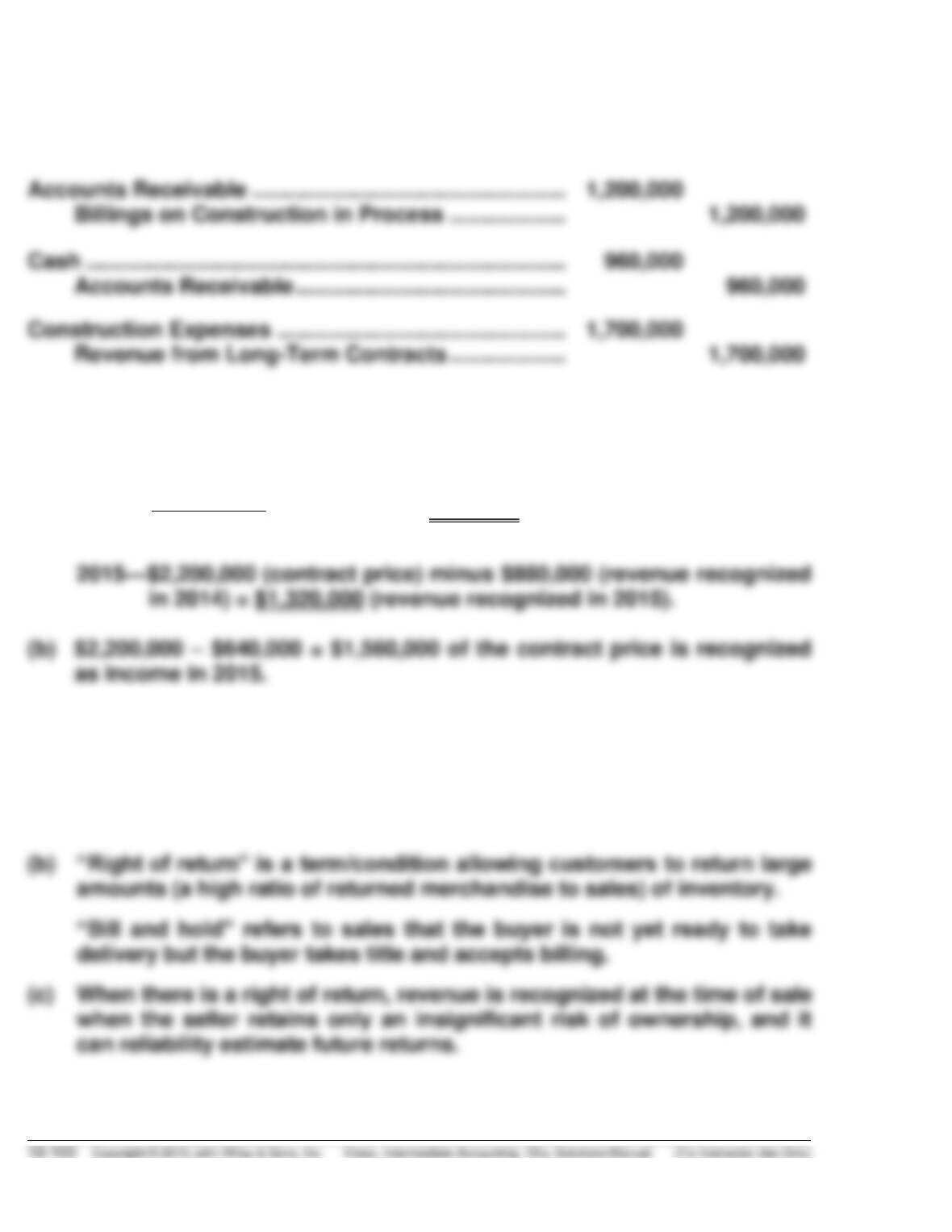

Construction in Process …………………………………… 1,700,000

Materials, Cash, Payables ………………………….. 1,700,000

IFRS18-7

Construction in Process ………………………………………. 1,700,000

Materials, Cash, Payables. …………………………….. 1,700,000

IFRS18-8

(a)

2014—

$640,000

X $2,200,000 = $880,000

$1,600,000

IFRS18-9

(a) IAS 18, paragraphs 15-19 addresses revenue recognition when right of

return exists.

IFRS18-9 (Continued)

(d) An entity does not recognise revenue if it retains significant risks of

ownership. Examples of situations in which the entity may retain the

significant risks and rewards of ownership are:

1. the entity retains an obligation for unsatisfactory performance not

covered by normal warranties.

(e) The seller recognises revenue when the buyer takes title, provided:

1. it is probable that delivery will be made;

2. the item is on hand, identified and ready for delivery to the buyer at

IFRS18-10

(a) 2012 Revenues: £9,934.3 million.

IFRS18-10 (Continued)

(c) Revenue comprises sales of goods to customers outside the Group

less an appropriate deduction for actual and expected returns,

(d) Accruals for sales returns and loyalty scheme redemptions are

estimated on the basis of historical returns and redemptions and these