*PROBLEM 14-12

(a) It is a troubled debt restructuring.

(b)

1. No entry.

Allowance for Doubtful Accounts ……………..

*Calculation of loss.

Pre-restructure carrying amount

$600,000

Present value of restructured cash flows:

(c) Losses are calculated based upon the discounted present value of

future cash flows. However, the debtor’s gain is calculated using the

*PROBLEM 14-13

(a)

On the books of Halvor Corporation:

Notes Payable ……………………………………………………….

5,000,000

Common Stock ……………………………………………….

1,700,000

Paid-in Capital in Excess of Par—

Common Stock …………………………………………..

2,000,000

Gain on Restructuring of Debt …………………………

1,300,000

Fair value of equity …………………………..

Gain on restructuring

On the books of Frontenac National Bank:

Equity Investments …………………………………………………

Allowance for Doubtful Accounts …………………………..

1,300,000

Notes Receivable …………………………..……………….

5,000,000

(b)

On the books of Halvor:

Notes Payable ……………………………………………………….

5,000,000

Land ……………………………………………………….

3,250,000

Gain on Disposal of Plant Assets …………………….

750,000

Gain on Restructuring of Debt …………………………

1,000,000

Fair value of land …………………………..

Book value of land …………………………..

Gain on disposal of

Note payable (carrying

amount) …………………………..

Gain on restructuring

On the books of Frontenac National Bank:

Land ………………………………………………………………………

Allowance for Doubtful Accounts …………………………..

Notes Receivable …………………………..……………….

*PROBLEM 14-13 (Continued)

(c)

On the books of Halvor:

No entry is needed because aggregate cash flows equal

the carrying amount.

Aggregate cash flows—principal ……………………..

$5,000,000

Carrying amount …………………………………………….

$5,000,000

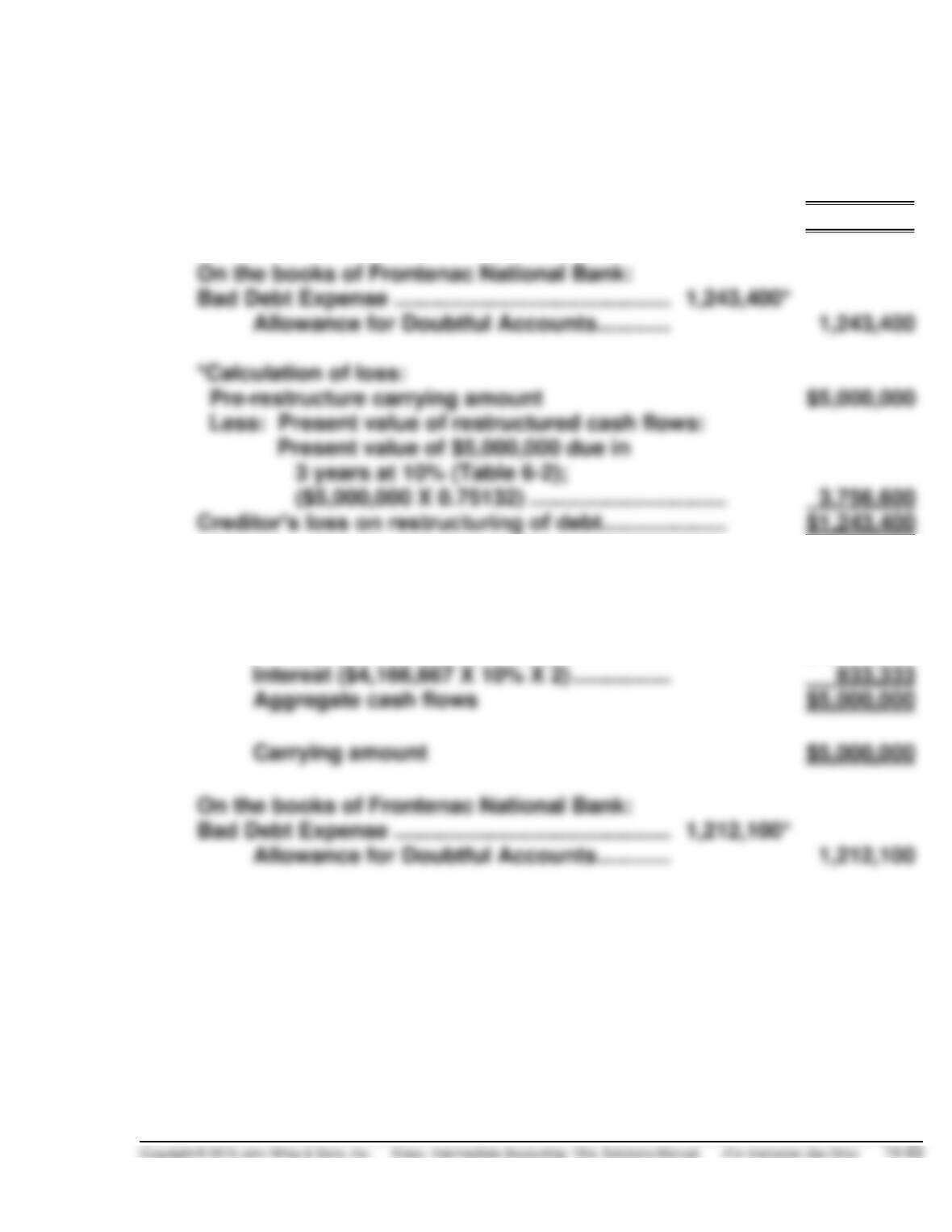

On the books of Frontenac National Bank:

Allowance for Doubtful Accounts …………………….

$5,000,000

3 years at 10% (Table 6-2);

($5,000,000 X 0.75132) …………………………..

$1,243,400

(d)

On the books of Halvor:

No entry is needed because aggregate cash flows equal

the carrying amount.

Principal ……………………………………………………….

$4,166,667

Interest ($4,166,667 X 10% X 2) ………………………..

833,333

Aggregate cash flows

$5,000,000

Carrying amount

$5,000,000

On the books of Frontenac National Bank:

Allowance for Doubtful Accounts …………………….

*PROBLEM 14-13 (Continued)

*Calculation of loss:

Pre-restructure carrying amount …………………………..

$5,000,000

Present value of restructured cash flows:

Present value of $4,166,667 due in

3 years at 10%, interest payable

annually (Table 6-2); ($4,166,667 X

.75132) ……………………………………………………….

Present value of $416,667 interest

payable annually for 3 years at 10%,

(Table 6-4); ($416,667 X 2.48685) ……………………

Less first year payment:

Present value of $416,667 interest due

in 1 year at 10% (Table 6-2);

($416,667 X .90909) …………………………..

3,787,900

*PROBLEM 14-14

Carrying amount of the debt at date of restructure, $330,000 + $33,000 =

$363,000. Total future cash flow, $300,000 + ($300,000 X .10 X 3) = $390,000.

Because the future cash flow exceeds the carrying amount of the debt, no

gain is recognized at the date of restructure.

(a) The effective-interest rate subsequent to restructure is computed by

trial and error using the assumed partial present value tables based

Therefore, the approximate effective rate is 2 5/8%.

(b) SCHEDULE OF DEBT REDUCTION

AND INTEREST EXPENSE AMORTIZATION

Date

Cash

Paid

Interest

Expense

Premium

Amortized

Carrying

Amount of

Note

12/31/14

$363,000

12/31/16

*PROBLEM 14-14 (Continued)

(c)

Calculation of loss:

Pre-restructure carrying amount …………………………..

$363,000

Present value of restructured cash flows:

Present value of $300,000 due in 3 years

at 10% , interest payable annually

(Table 6-2); ($300,000 X .75132) ……………………..

Present value of $30,000 interest payable

annually for 3 years at 10% (Table 6-4);

($30,000 X 2.48685) ………………………………………

(300,000*)

$300,000. The $1 difference is due to rounding.

Date

Cash

Received

Interest

Revenue

Change in

Carrying

Amount

Carrying

Amount of

Note

12/31/14

$300,000

12/31/15

$ 30,000a

$30,000b

$ 0

300,000c

12/31/16

12/31/17

0

12/31/18

(d)

Crocker Corp. entries:

December 31, 2014

Interest Payable ………………………………………………………

33,000

Notes Payable ………………………………………………..

33,000

December 31, 2015

Interest Expense …………………………………………………….

9,529

Notes Payable ……………………………………………………….

20,471

Cash …………………………..…………………………..

*PROBLEM 14-14 (Continued)

December 31, 2016

Interest Expense …………………………………………………….

8,991

Cash ……………………………………………………….

(e)

Bad Debt Expense ………………………………………………….

Allowance for Doubtful Accounts …………………….

Cash ………………………………………………………………………

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 14-1 (Time 25–30 minutes)

Purpose—to provide the student with some familiarity with the economic theory which relates to the

CA 14-2 (Time 15–25 minutes)

Purpose—this case includes discussions of the determination of the selling price of bonds, presentation

of items related to bonds on the balance sheet and the income statement, whether discount amor-

tization increases or decreases, and how an early retirement of bonds should be reported on the income

statement.

CA 14-3 (Time 20–25 minutes)

Part I—Purpose—to provide the student with an understanding of the significance of the difference

CA 14-4 (Time 20–30 minutes)

Purpose—the student is asked to explain project financing arrangements, take-or-pay contracts, off-

CA 14-5 (Time 20–30 minutes)

Purpose—to provide the student with an opportunity to examine the ethical issues related to the issue

of bonds.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 14-1

(a) 1. This is a common balance sheet presentation and has the advantage of being familiar to users

2. This presentation indicates the dual nature of the bond obligations. There is an obligation to

make periodic payments of $55,000 and an obligation to pay the $1,000,000 at maturity. The

3. This presentation shows the total liability which is incurred in a bond issue, but it ignores the

time value of money. This would be a fair presentation of the bond obligations only if the

effective-interest rate were zero.

(b) When an entity issues interest-bearing bonds, it normally accepts two types of obligations: (1) to

pay interest at regular intervals and (2) to pay the principal at maturity. The investors who

purchase Nichols Company bonds expect to receive $55,000 each January 1 and July 1 through

Another way of viewing this is that the $1,085,800 is the amount which, if invested at an annual

interest rate of 10% compounded semiannually, would allow withdrawals of $55,000 every six

months from July 1, 2014 through January 1, 2034 and $1,000,000 on January 1, 2034.

Even when bonds are issued at their maturity value, the price paid coincides with the maturity

value because the coupon rate is equal to the effective rate. If the bonds had been issued at their

maturity value, the $1,000,000 would be the present value of future interest and principal pay-

ments discounted at an annual rate of 11% compounded semiannually.

CA 14-1 (Continued)

2. The effective-interest rate at January 1, 2014 is the market rate to Nichols Company for long-

term borrowing. This rate gives a discounted value for the bond obligations, which is the

amount that could be invested at January 1, 2014 at the market rate of interest. This

investment would provide the sums needed to pay the recurring interest obligation plus the

(d) Using a current yield rate produces a current value, that is, the amount which could currently be

invested to produce the desired payments. When the current yield rate is lower than the rate at the

issue date (or than at the previous valuation date), the liabilities for principal and interest would

CA 14-2

(a) 1. The selling price of the bonds would be the present value of all of the expected net future cash

2. Immediately after the bond issue is sold, the current asset, cash, would be increased by the

proceeds from the sale of the bond issue. A noncurrent liability, bonds payable, would be

(b) The following items related to the bond issue would be included in Sealy’s 2014 income statement:

1. Interest expense would be included for ten months (March 1, 2014, to December 31, 2014) at

an effective-interest rate (yield) of 11 percent. This is composed of the nominal interest of

2. Interest expense (or bond issue expense) would be included for ten months of amortization of

bond issue costs (March 1, 2014 to December 31, 2014). Bond issue costs should be amor-

(c) The amount of bond discount amortization would be lower in the second year of the life of the

bond issue. The effective-interest method of amortization uses a uniform interest rate based upon

a changing carrying value which results in increasing amortization each year when there is a bond

discount.

CA 14-2 (Continued)

CA 14-3

Part I.

(a) The effective-interest method of amortization of bond discount or premium applies a constant

interest rate to the carrying value of the debt. The straight-line method applies a constant dollar

(b) Before the effective-interest method of amortization can be used, the effective yield or interest rate

of the bond must be computed. The effective yield rate is the interest rate that will discount the two

components of the debt instrument to the amount received at issuance. The two components in

the value of a bond are the present value of the principal amount due at the end of the bond term

and the present value of the annuity represented by the periodic interest payments during the life

of the bond. Interest expense using the effective interest method is based upon the effective yield

or interest rate multiplied by the carrying value of the bond (par value adjusted for unamortized

premium or discount). The amount of amortization is the difference between recognized interest

expense and the interest actually paid (par value multiplied by the nominal rate). When a premium

Part II.

(a) 1. Gain or loss to be amortized over the remaining life of old debt. The basic argument

supporting this method is that if refunding is done to obtain debt at a lower cash outlay (interest

cost), then the gain or loss is truly a cost of obtaining the reduction in cash outlay. As such, the

2. Gain or loss to be amortized over the life of the new debt instrument. This argument states

that the gain or loss from early extinguishment of debt actually affects the cost of obtaining a new

debt instrument. However, this method asserts that the effect should be matched with the

CA 14-3 (Continued)

3. Gain or loss recognized in the period of extinguishment. Proponents of this method state

that the early extinguishment of debt to be refunded actually does not differ from other types of

extinguishment of debt where the consensus is that any gain or loss from the transaction

should be recognized in full in current net earnings. The early extinguishment of the debt is

prompted for the same reason that other debt instruments are extinguished, namely, that the

(b) The immediate recognition principle is the only acceptable method of reflecting gains or losses on

the early extinguishment of debt, and these amounts, if material, must be reflected as ordinary

gains and losses.

CA 14-4

(a) Such financing arrangements arise when (1) two or more entities form another entity to construct

an operating plant that will be used by both parties; (2) the new entity borrows funds to construct

the project and repays the debt from the proceeds received from the project; and (3) payment of

the debt is guaranteed by the companies that formed the new entity.

(b) In some cases, project financing arrangements become more formalized through the use of take-

(d) Accounting for purchase commitments is unsettled and controversial. Some argue that these

contracts should be reported as assets and liabilities at the time the contract is signed; others

believe that our present recognition at the delivery date is most appropriate. FASB Concepts

Statement No. 6 states that

“a purchase commitment involves both an item that might be recorded as

an asset and an item that might be recorded as a liability. That is, it involves

CA 14-4 (Continued)

According to current practice, Ryan does not record an asset relating to the future purchase

commitment. However, if the dollar amount involved is material, the details of the contract should

(e) Off-balance-sheet financing is an attempt to borrow monies in such a way that the obligations

are not recorded in a company’s balance sheet. The reasons for off-balance-sheet financing are

many. First, many believe that removing debt or otherwise keeping it from the balance sheet

Note to instructor: Additional discussion of these type arrangements is presented in Appendix 17B

related to variable interest entities.

CA 14-5

(a) The stakeholders in the Wichita case are:

Donald Lennon, president, founder, and majority stockholder.

(b) The ethical issues:

The desires of the majority stockholder (Donald Lennon) versus the desires of the minority stock-

holders (Nina Friendly and others).

(c) The rationale provided by the student will be more important than the specific position because

this is a borderline case with no right answer.

FINANCIAL REPORTING PROBLEM

(a) According to the Short-Term and Long-Term Debt note (Note 4),

Long-term debt maturities during the next five fiscal

(b) (Amounts in $millions)

1. Working capital = Current assets less current liabilities.

($5,323) = $21,970 – $27,293

2.

Acid-test ratio =

Cash + investments + net receivables

Current liabilities

Current liabilities

While it appears P&G has a fairly weak liquidity position. The current

ratio is below 1. The acid-test ratio is significantly below 1, possibly

due to a slowing economy. However, P&G’s high current liabilities

could reflect a cheap form of financing.

The other ratio analysis below provides P&G’s additional insight into

financial position in 2011.

FINANCIAL REPORTING PROBLEM (Continued)

Inventory turnover =

Cost of goods sold

Average inventory

Current cash debt

coverage =

Net cash provided by operating activities

Average current liabilities

$27,293 + $24,282

$70,353 + $66,733

Debt to assets =

$70,353

= 0.51 (.52 in 2010)

$138,354

Time interest earned =

Income before income taxes and interest expense

Interest expense

$15,189 + $831

In total, and with comparison to analysis in 2010, P&G has an

improving liquidity and solvency position.

COMPARATIVE ANALYSIS CASE

(a) Debt to asset ratio:

Coca-Cola $48,053/$79,974 = 60%

PepsiCo $51,983/$72,882 = 71%

Times interest earned ratio:

(b)

Carrying Value

Fair Value

Coca-Cola

$15,697

$16,360

PepsiCo

23,117

29,800

The fair value will vary from the historical cost carrying value due to

changes in interest rates.

(c) 1. Lower interest rates may be available in foreign countries.