CA 24-8 (Continued)

2. The company’s revenue and expenses would be reported as follows on its quarterly report

prepared for the first quarter of the 2014–2015 fiscal year:

Sales revenue ………………………………………………………………………………. $60,000,000

Cost of goods sold ………………………………………………………………………… 36,000,000

beyond the interim period in which the expenditure is made.

(b) The financial information to be disclosed to its stockholders in its quarterly reports as a minimum

include:

1. Sales revenue or gross revenues, provision for income taxes, extraordinary items and net

income.

CA 24-9

(a) Acceptable. The use of estimated gross profit rates to determine the cost of goods sold is accept-

able for interim reporting purposes as long as the method and rates utilized are reasonable. The

(c) Acceptable. Any loss in inventory value should be reported when the decline occurs. Any re–

coveries of the losses on the same inventory in later periods should be recognized as gains in the

later interim periods of the same fiscal year. However, the gains should not exceed the previously

recorded losses.

CA 24-9 (Continued)

(e) Acceptable. The annual audit fee is an expense which benefits the company’s entire year. Com-

panies are encouraged to make quarterly estimates of these items that usually result in year–end

adjustments. Therefore, this expense can be prorated over the four quarters.

(f) Not acceptable. Revenue from products sold should be recognized as earned during the interim

CA 24-10

(a) Arguments for requiring published forecasts:

1. Investment decisions are based on future expectations; therefore, information about the

(b) The purpose of a safe harbor rule is to provide protection to an enterprise that presents an

(c) An enterprise’s concerns about preparing a forecast are as follows:

1. No one can foretell the future. Therefore forecasts, while conveying an impression of precision

about the future, will inevitably be wrong.

CA 24-11

(a) The controller notes that the financial vice president is misrepresenting the financial condition of

the company by suggesting that the company has become more efficient when, in fact, the

(c) The favorable media release enhances the current stockholders’ position, as well as boosting the

image of management. Such publicity may well contribute to an increased stock price. Future inves–

tors and stockholders are harmed because the media release depicts a misleading perspective

on the financial condition of the company.

CA 24-11 (Continued)

(d) The controller is responsible for both the accuracy and the clarity of financial reporting. If the media

CA 24-12

(a) The ethical issues involved are profitability, long-term versus short-term performance, and integrity

of financial reporting.

(b) Form should not dictate substance. The bonds should be issued when the company needs the

should not delay issuance.

*CA 24-13

FINANCIAL REPORTING PROBLEM

(a) Proctor & Gamble (P&G) commented on the following items in its note

on accounting policies:

Nature of operations Cash flow presentation

Basis of presentation Cash equivalents

(b) P&G reported information for the following segments:

1. Beauty

2. Grooming

The fabric care and home care segment is the largest in net sales and

COMPARATIVE ANALYSIS CASE

THE COCA-COLA COMPANY VERSUS PEPSICO, INC.

(a) 1. Coca-Cola commented on the following list of items in its note on

accounting policies:

The Coca-Cola Company and Subsidiaries (Note 1)

• Description of Business

• Basis of Presentation

• Principles of Consolidation

• Cash Equivalents

• Short-term Investments

• Investments in Equity and Debt Securities

• Trade Accounts Receivable

• Inventories

• Derivative Instruments

2. PepsiCo commented on the following list of items in its note on

accounting policies:

PepsiCo, Inc. and Subsidiaries

Note 2—Our Significant Accounting Policies

COMPARATIVE ANALYSIS CASE (Continued)

Cash Equivalents

Software Costs

Commitments and Contingencies

Research and Development

Other Significant Accounting Policies

Recent Accounting Pronouncements

(b) Coca-Cola divided its operations into seven operating segments:

(c) Coca–Cola’s independent auditors are Ernst & Young LLP, while PepsiCo’s

independent auditors are KPMG LLP.

*FINANCIAL STATEMENT ANALYSIS CASE

RNA INC.

(a) The calculation of selected financial ratios for RNA for the fiscal year

2015 is as follows:

Times interest earned

=

Income before income taxes

and interest expense

Interest expense

*FINANCIAL STATEMENT ANALYSIS CASE (Continued)

Asset turnover

=

Net sales

Average total assets

=

Inventory turnover

=

=

(b) The analytical use of each of the six ratios presented above and what

investors can learn about RNA’s financial stability and operating

efficiency are presented below.

Current ratio

• Measures the ability to meet short-term obligations using short-

term assets.

Acid-test ratio

• Measures the ability to meet short-term debt using the most liquid

assets.

*FINANCIAL STATEMENT ANALYSIS CASE (Continued)

Times interest earned

• Measures the ability to meet interest commitments from current

Profit margin on sales

• Measures the net income generated by each dollar of sales. It pro–

Asset turnover

• Measures the efficiency of resource use; i.e., the ability to generate

sales through the use of assets.

Inventory turnover

• Measures how quickly inventory is sold, as well as how effectively

investment in inventory is used. It also provides a basis for deter–

*FINANCIAL STATEMENT ANALYSIS CASE (Continued)

(c) Limitations of ratio analysis include:

• Difficulty making comparisons among firms in the same industry

ACCOUNTING, ANALYSIS, AND PRINCIPLES

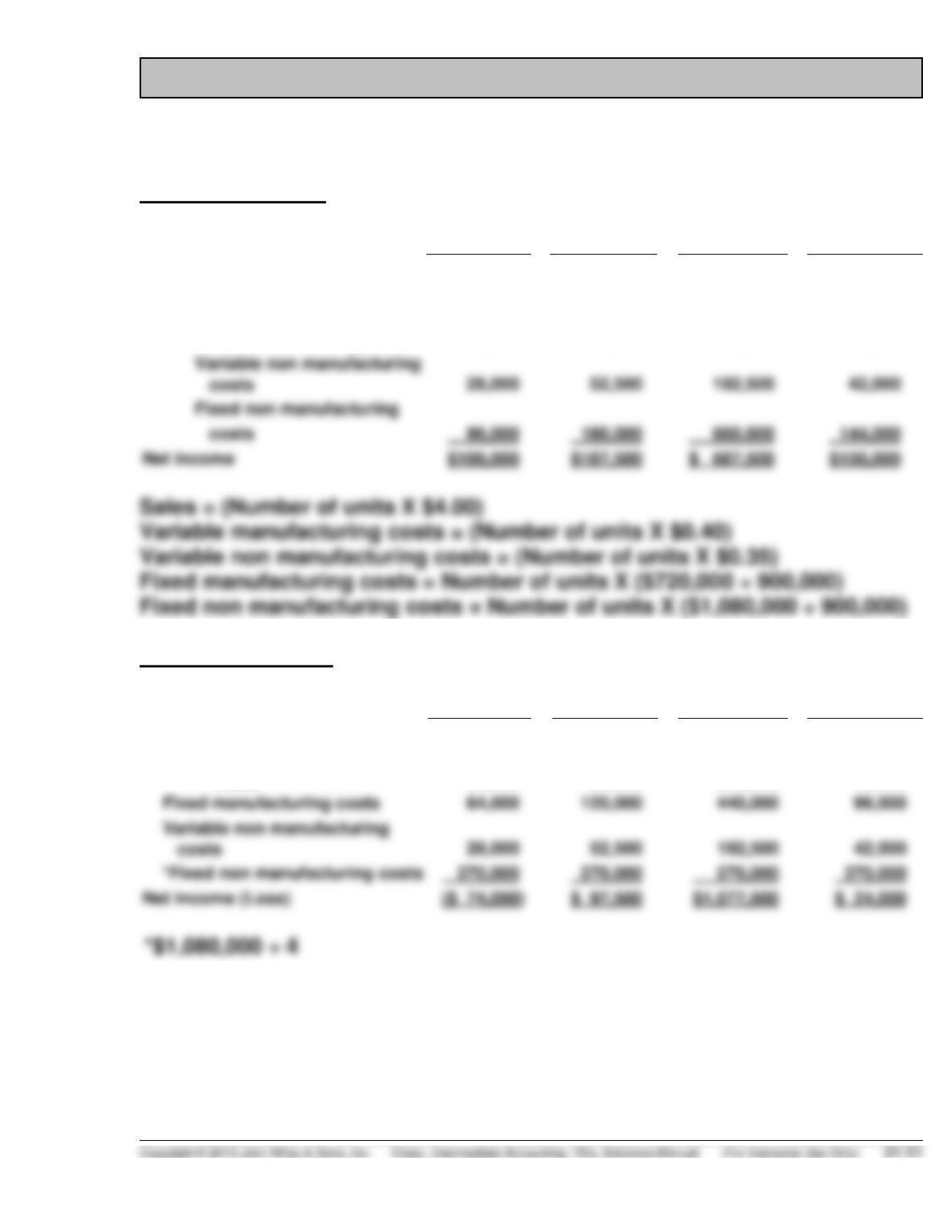

Accounting

Integral Approach

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Sales

$320,000

$600,000

$2,200,000

$480,000

Less: Variable manufacturing

costs

32,000

60,000

220,000

48,000

Fixed manufacturing costs

64,000

120,000

440,000

96,000

Net income

$ 687,500

Discrete Approach

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Sales

$320,000

$600,000

$2,200,000

$480,000

Less: Variable manufacturing

costs

32,000

60,000

220,000

48,000

Fixed manufacturing costs

120,000

Variable non manufacturing

costs

28,000

52,500

192,500

42,000

*Fixed non manufacturing costs

270,000

270,000

Net income (Loss)