EXERCISE 5-17 (Continued)

(b) Grant Wood Corporation

Balance Sheet

December 31, 2014

Assets

Current assets …………………………………………

$296,500b

Equity investments (Long-term) ………………..

16,000

Property, plant, and equipment

Land ………………………………………………….

$ 30,000

Building ($120,000 + $27,000) ………………

$147,000

Equipment ($90,000 – $20,000) …………….

Total property, plant, and equipment …..

Liabilities and Stockholders’ Equity

Current liabilities ($150,000 + $13,000) ……………………

$163,000

Long-term liabilities

Bonds payable ($100,000 + $50,000) ………………….

150,000

Total liabilities ……………………………………………

Common stock ………………………………………………..

$180,000

Retained earnings ($44,000 + $55,000 – $30,000) ……..

Total paid-in capital and retained earnings ……..

Less: Cost of treasury stock …………………………..

11,000

Total stockholders’ equity …………………………..

b

The amount determined for current assets could be computed last and then is a

“plug” figure. That is, total liabilities and stockholders’ equity is computed because

information is available to determine this amount. Because the total assets amount is

the same as total liabilities and stockholders’ equity amount, the amount of total

EXERCISE 5-18 (25–35 minutes)

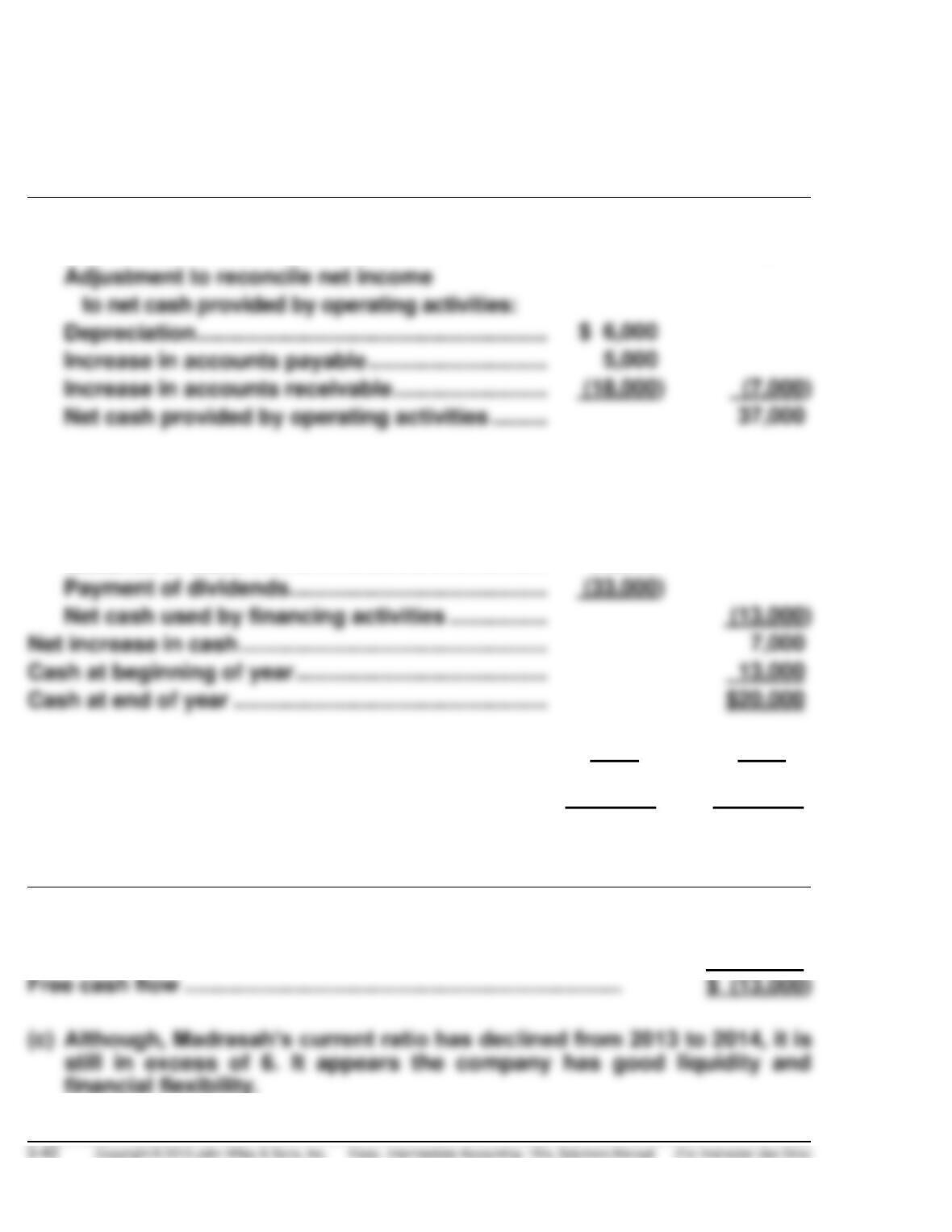

(a) Madrasah Corporation

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………………….

$44,000

Adjustment to reconcile net income

to net cash provided by operating activities:

Depreciation ……………………………………………………..

Increase in accounts payable …………………………..

Increase in accounts receivable …………………………

Net cash provided by operating activities …………..

Cash flows from Investing activities

Purchase of equipment ……………………………………..

(17,000)

Cash flows from financing activities

Issuance of stock ……………………………………………..

20,000

Payment of dividends ………………………………………..

Net cash used by financing activities …………………

Net increase in cash ……………………………………………….

Cash at beginning of year ……………………………………….

Cash at end of year ………………………………………………..

$20,000

2014

2013

(b) Current ratio

6.3

6.73

$126,000

$101,000

$ 20,000

$ 15,000

Free Cash Flow Analysis

Net cash provided by operating activities ………………………..

$ 37,000

Less: Purchase of equipment …………………………………………

(17,000)

Pay dividends …………………………..………………………….

(33,000)

TIME AND PURPOSE OF PROBLEMS

Problem 5-1 (Time 30–35 minutes)

Problem 5-2 (Time 35–40 minutes)

Purpose—to provide the student with the opportunity to prepare a complete balance sheet, involving

dollar amounts. A unique feature of this problem is that the student must solve for the retained earnings

balance.

Problem 5-3 (Time 40–45 minutes)

Purpose—to provide an opportunity for the student to prepare a balance sheet in good form. Emphasis

Problem 5-4 (Time 40–45 minutes)

Purpose—to provide the student with the opportunity to analyze a balance sheet and correct it where

appropriate. The balance sheet as reported is incomplete, uses poor terminology, and is in error. A

challenging problem.

Problem 5-5 (Time 40–45 minutes)

Problem 5-6 (Time 35–45 minutes)

Purpose—to provide the student with an opportunity to prepare a complete statement of cash flows. A

Problem 5-7 (Time 40–50 minutes)

Purpose—to provide the student with an opportunity to prepare a balance sheet in good form and a

more complex cash flow statement.

SOLUTIONS TO PROBLEMS

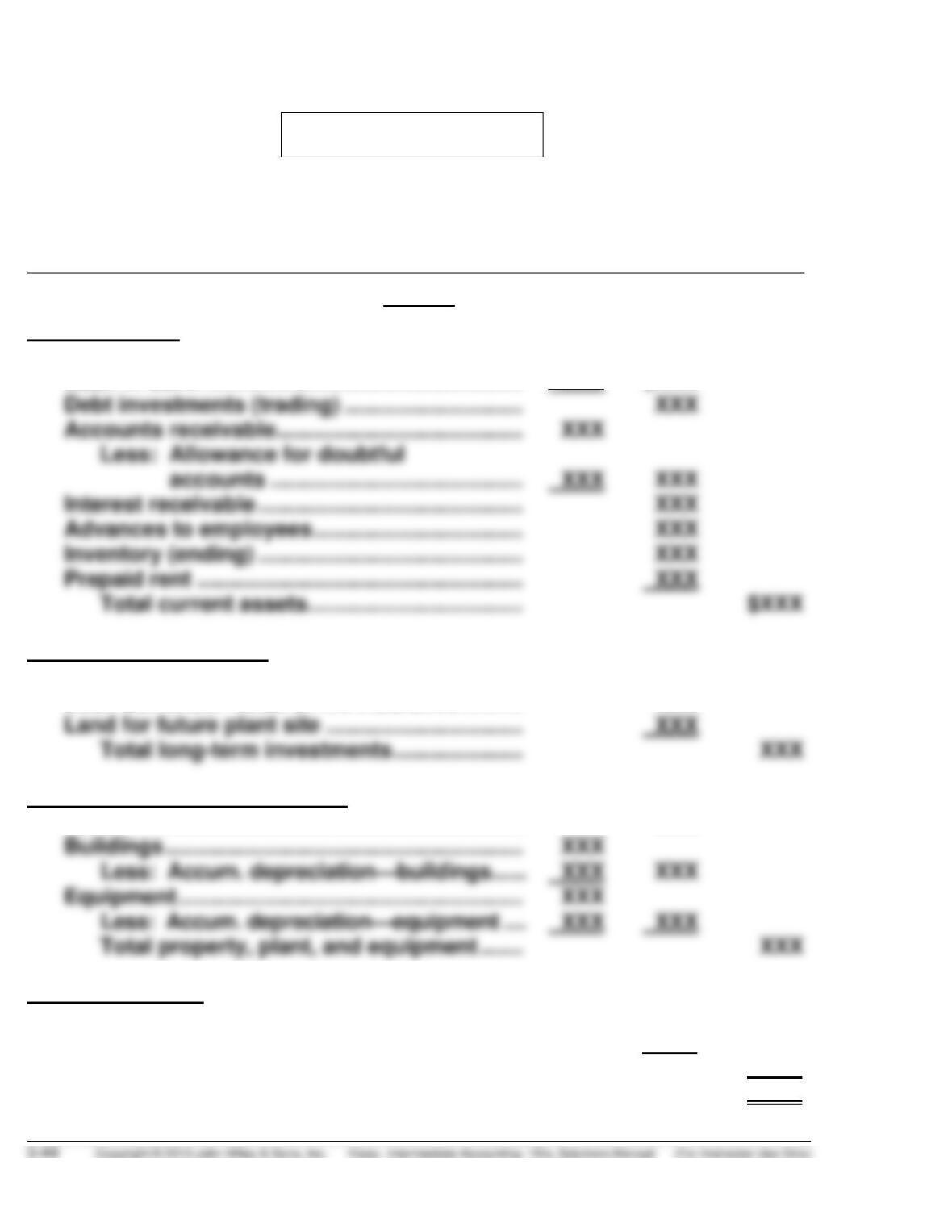

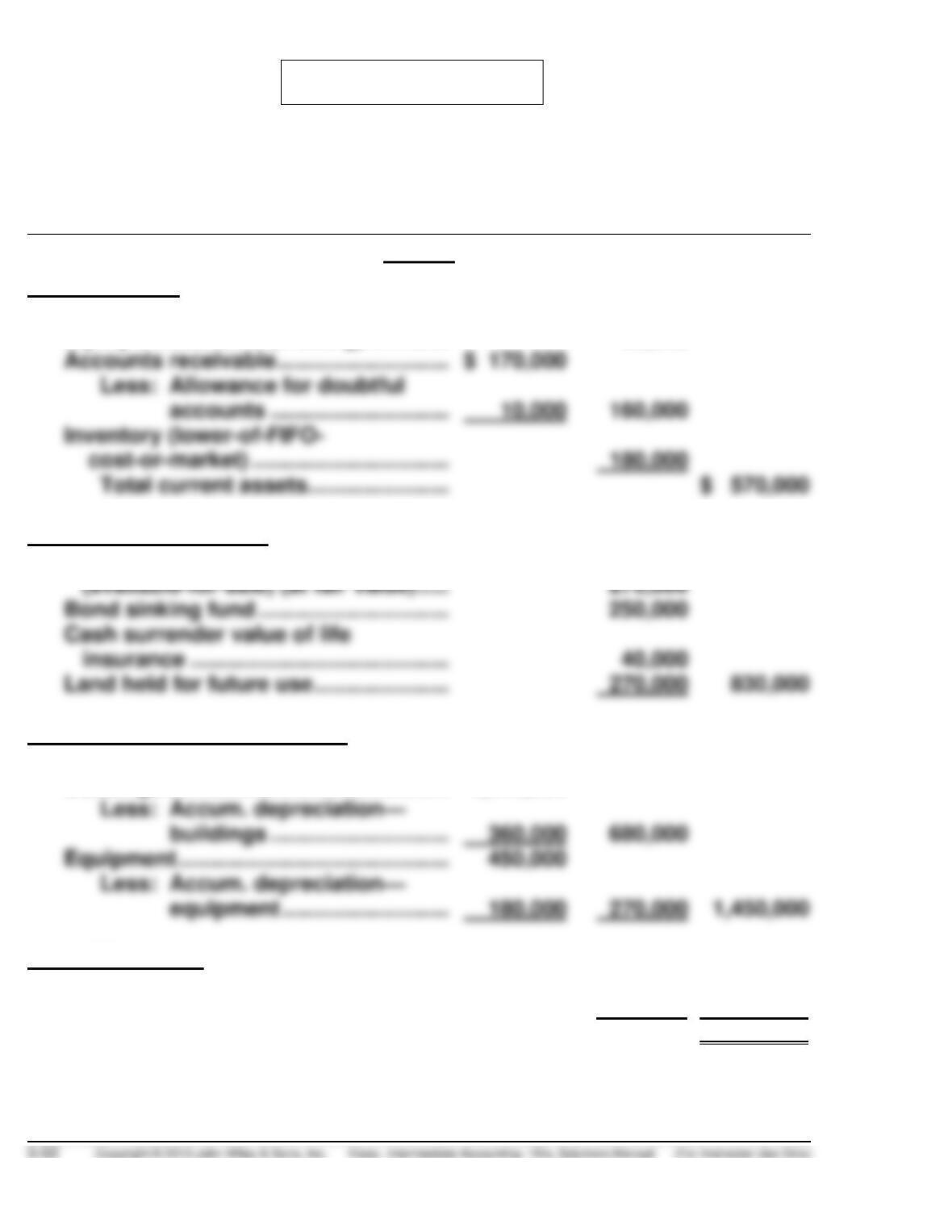

PROBLEM 5-1

COMPANY NAME

Balance Sheet

December 31, 20XX

Assets

Current assets

Cash on hand (including petty cash) ………….

$XXX

Cash in bank …………………………………………….

XXX

$XXX

Debt investments (trading) ………………………..

XXX

Accounts receivable ………………………………….

accounts …………………………………..

Interest receivable …………………………..………..

XXX

Advances to employees …………………………….

Inventory (ending) …………………………………….

XXX

Prepaid rent ……………………………………………..

XXX

Total current assets ……………………………..

Long-term investments

Bond sinking fund …………………………………….

XXX

Cash surrender value of life insurance ……….

XXX

Land for future plant site …………………………..

Total long-term investments …………………

Property, plant, and equipment

Land …………………………………………………………

XXX

Less: Accum. depreciation—buildings ……

Equipment ………………………………………………..

Less: Accum. depreciation—equipment ….

XXX

Total property, plant, and equipment …….

Intangible assets

Copyrights ……………………………………………….

XXX

Patents …………………………………………………….

XXX

Total intangible assets …………………………

XXX

Total assets ………………………………………………

$XXX

PROBLEM 5-1 (Continued)

Liabilities and Stockholders’ Equity

Current liabilities

Notes payable ………………………………………….

$XXX

Payroll taxes payable ……………………………….

XXX

Salaries and wages payable ……………………..

XXX

XXX

Unearned subscriptions revenue ………………

Total current liabilities ………………………..

Long-term debt

Bonds payable …………………………………………

$XXX

Add: Premium on bonds payable ………..

XXX

XXX

Pension liability ……………………………………….

Total long-term liabilities …………………….

Total liabilities ……………………………………

Stockholders’ equity

Capital stock

Preferred stock (description) ……………….

XXX

Common stock (description) ……………….

XXX

XXX

Total paid-in capital …………………………….

XXX

Retained earnings ……………………………………

Less: Treasury stock ……………………………….

Total stockholders’ equity …………………..

Paid-in capital in excess of par –

PROBLEM 5-2

MONTOYA, INC.

Balance Sheet

December 31, 2014

Assets

Current assets

Cash …………………………………………….

$ 360,000

Equity investments (trading) ………….

121,000

Notes receivable …………………………..

445,700

Income taxes receivable ………………..

Inventory ………………………………………

239,800

Prepaid expenses ………………………….

Total current assets ………………….

$1,352,050

Property, plant, and equipment

Land ……………………………………………..

480,000

Equipment …………………………………….

Intangible assets

Goodwill ……………………………………….

125,000

Total assets ……………………………..

$4,504,850

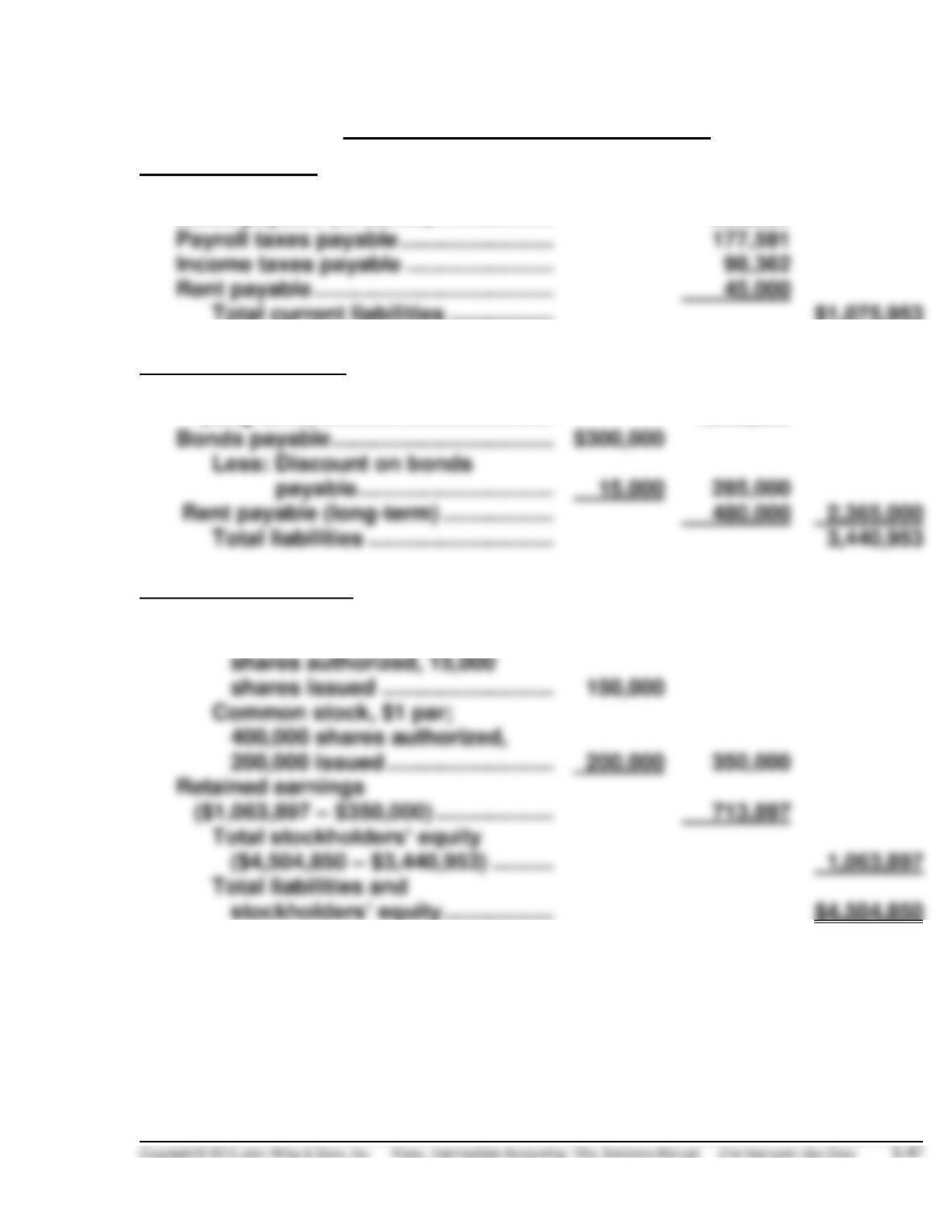

PROBLEM 5-2 (Continued)

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………..

$ 490,000

Notes payable (to banks) …………………

265,000

Payroll taxes payable ………………………

Income taxes payable ……………………..

Rent payable …………………………………..

Total current liabilities ……………….

$1,075,953

Long-term liabilities

Notes payable

(long-term) ………………………………….

1,600,000

Bonds payable ………………………………..

Rent payable (long-term) ………………..

Total liabilities …………………………..

Stockholders’ equity

Capital stock

Preferred stock, $10 par; 20,000

PROBLEM 5-3

EASTWOOD COMPANY

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ………………………………………………..

$ 41,000

Accounts receivable ………………………….

$163,500

Inventory (LIFO cost)…………………………

Prepaid insurance …………………………..

Total current assets ……………………..

Long-term investments

Equity investments

($120,000 have been pledged as

security for notes payable)—

at fair value ……………………………………

339,000

Property, plant, and equipment

Cost of uncompleted plant facilities

Equipment ………………………………………..

Intangible assets

Patents (less $4,000 amortization) ……..

36,000

Total assets …………………………………

$1,154,200

PROBLEM 5-3 (Continued)

Liabilities and Stockholders’ Equity

Current liabilities

Notes payable (secured by

investments of $120,000) ………………..

$ 94,000

Accounts payable …………………………...

Accrued liabilities …………………………...

Total current liabilities ……………….

Long-term liabilities

8% bonds payable, due

January 1, 2025 …………………………….

200,000

Less: Discount on bonds payable……

Total liabilities …………………………..

Stockholders’ equity

Common stock

Retained earnings …………………………..

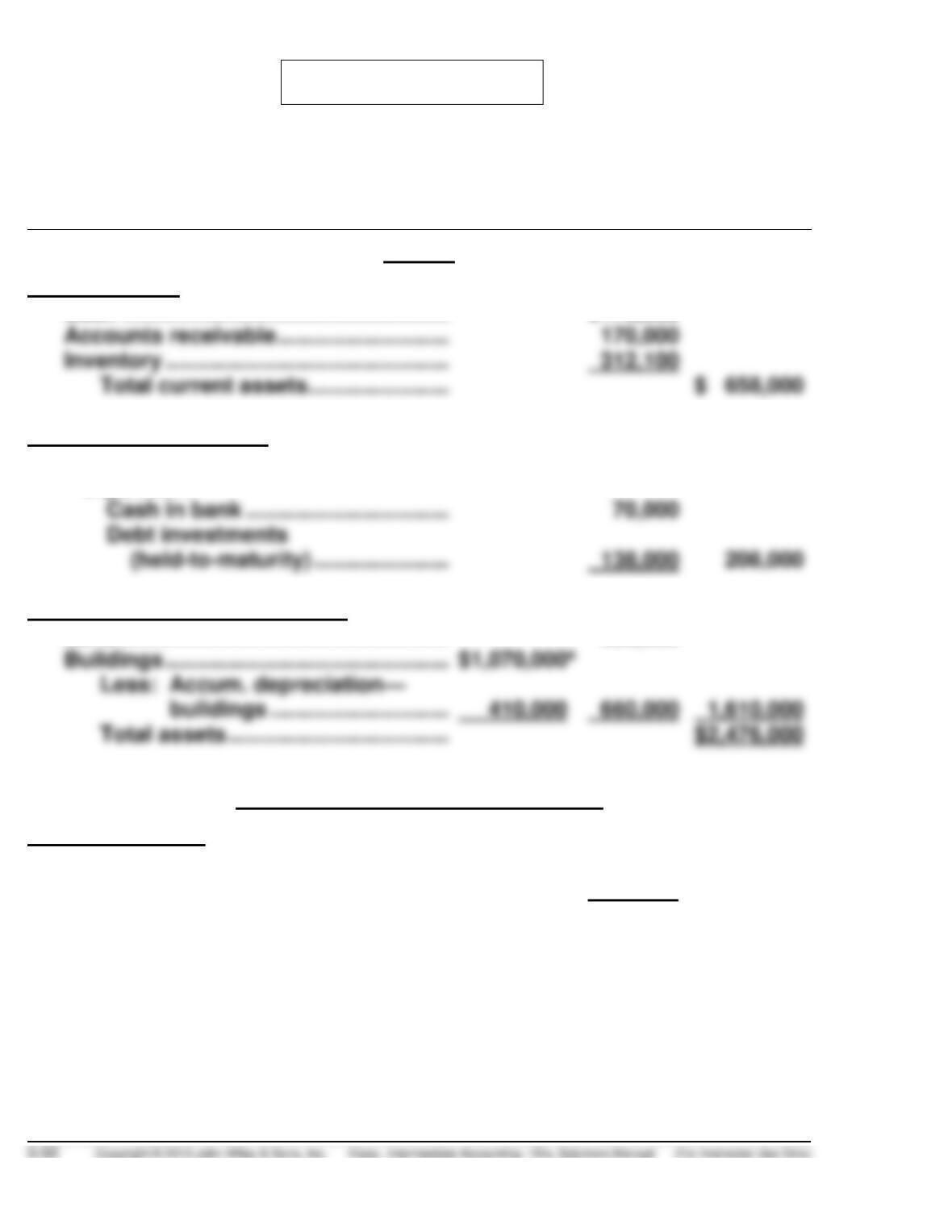

PROBLEM 5-4

KISHWAUKEE CORPORATION

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ……………………………………………….

$175,900

Accounts receivable …………………………

Inventory …………………………………………

Total current assets …………………….

Long-term investments

Assets allocated to trustee for

expansion:

Cash in bank ……………………………..

Debt investments

(held-to-maturity) ……………………

Property, plant, and equipment

Land ………………………………………………..

950,000

Buildings …………………………………………

Less: Accum. depreciation—

Total assets ………………………………..

Liabilities and Stockholders’ Equity

Current liabilities

Notes payable—current installment ……

$100,000

Income taxes payable……………………….

75,000

Total current liabilities ………………..

$ 175,000

PROBLEM 5-4 (Continued)

Long-term liabilities

Notes payable …………………………………..

500,000b

Total liabilities ……………………………..

675,000

Stockholders’ equity

Retained earnings ……………………………..

Common stock, no par; 1,000,000

a$1,640,000 – $570,000 (to eliminate the excess of appraisal value over cost

from the Buildings account. Note that the appreciation capital account is

also deleted).

Note: As an alternate presentation, the cash restricted for plant expansion

would be added to the general cash account and then subtracted. The

amount reported in the investments section would not change.

PROBLEM 5-5

SARGENT CORPORATION

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ……………………………………………….

$150,000

Equity investments (Trading) ……………

80,000

Accounts receivable …………………………

Total current assets …………………….

Long-term investments

Bond sinking fund …………………………..

Land held for future use ……………………

270,000

Equity investments

Property, plant, and equipment

Land ………………………………………………..

500,000

Buildings …………………………………………

1,040,000

Less: Accum. depreciation—

Equipment ……………………………………….

Intangible assets

Franchise ………………………………………..

165,000

Goodwill ………………………………………….

100,000

265,000

Total assets ………………………………..

$3,115,000

PROBLEM 5-5 (Continued)

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………..

$ 140,000

Notes payable …………………………………..

Income taxes payable ……………………….

Unearned rent revenue ……………………..

5,000

Total current liabilities ………………….

Long-term liabilities

Notes payable …………………………………..

120,000

7% bonds payable, due 2022 …………….

Less: Discount on bonds payable ……..

960,000

Total liabilities …………………………..

Stockholders’ equity

Capital stock

Preferred stock, no par value;

200,000 shares authorized,

70,000 issued and outstanding ………

450,000

Paid-in capital in excess of par—

($10.00 – $1.00)] ………………………….

Retained earnings …………………………..

320,000

Total stockholders’ equity …………….

PROBLEM 5-6

(a) LANSBURY INC.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………………..

$32,000

Depreciation expense ………………………………

Net cash provided by operating activities ………

Adjustments to reconcile net income to

Cash flows from investing activities

Sale of investments ………………………………………

15,000

Purchase of land …………………………………………..

(18,000)

Net cash used by investing activities …………….

(3,000)

Cash flows from financing activities

Issuance of common stock …………………………...

Retirement of notes payable ………………………….

Payment of cash dividends …………………………..

(8,200)

Net cash used by financing activities …………….

Net increase in cash …………………………………………..

Cash at beginning of year …………………………………..

PROBLEM 5-6 (Continued)

(b) LANSBURY INC.

Balance Sheet

December 31, 2014

Assets

Liabilities and Stockholders’ Equity

Cash

$32,000

Accounts payable

$30,000

Equity

Bonds payable

(5)

Accounts

Notes payable

(1) $32,000 – ($15,000 – $3,400)

(2) $81,000 – $11,000

(c) Cash flow information is useful for assessing the amount, timing, and

uncertainty of future cash flows. For example, by showing the specific

inflows and outflows from operating activities, investing activities,

and financing activities, the user has a better understanding of the

PROBLEM 5-6 (Continued)

An analysis of Lansbury’s free cash flow indicates it is negative as shown

below:

Free Cash Flow Analysis

Net cash provided by operating activities …………………………

$19,200

Its current cash debt coverage is 0.64 to 1

$19,200

$30,000

and its cash debt

PROBLEM 5-7

(a) AERO INC.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………………….

$35,000

Depreciation expense ……………………………….

Loss on sale of investments ………………………

Increase in accounts receivable

Net cash provided by operating activities ………..

Adjustments to reconcile net income to

Cash flows from investing activities

Sale of investments ………………………………………..

27,000

Purchase of land ……………………………………………

(38,000)

Net cash used by investing activities ………………

(11,000)

Cash flows from financing activities

Issuance of common stock……………………………..

30,000

Payment of cash dividends …………………………..

Net cash provided by financing activities ………..

20,000

Net increase in cash …………………………………………….

50,200

Cash at beginning of year …………………………………….

20,000

PROBLEM 5-7 (Continued)

(b) AERO INC.

Balance Sheet

December 31, 2014

Assets

Liabilities and Stockholders’ Equity

Cash

$ 70,200

Accounts payable

$ 40,000

(1)

Retained earnings

(5)

(1) $81,000 – $12,000

(c) An analysis of Aero’s free cash flow indicates it is negative as shown

below:

Free Cash Flow Analysis

Net cash provided by operating activities …………………………

$41,200

Dividends ……………………………………………………………..

PROBLEM 5-7 (Continued)

Its current cash debt coverage is 1.18 to 1

$41,200

$35,000*

.

Overall, it appears

(d) This type of information is useful for assessing the amount, timing,

and uncertainty of future cash flows. For example, by showing the

specific inflows and outflows from operating activities, investing

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 5-1 (Time 20–25 minutes)

Purpose—to provide a varied number of financial transactions and then determine how each of these

CA 5-2 (Time 30–35 minutes)

Purpose—to present the asset section of a partial balance sheet that must be analyzed to assess its

deficiencies. Items such as improper classifications, terminology, and disclosure must be considered.

CA 5-3 (Time 20–25 minutes)

CA 5-4 (Time 20–25 minutes)

Purpose—to present the student an ethical issue related to the presentation of balance sheet

information. The reporting involves “net presentation” of property, plant and equipment.

CA 5-5 (Time 40–50 minutes)