CHAPTER 22

SOLUTIONS TO B EXERCISES

E22-1B (10–15 minutes)

(a) The net income to be reported in 2014, using the retrospective approach,

would be computed as follows:

E22-2B (10–15 minutes)

(a) Retained earnings …………………………………….. 40,000*

Inventory …………………………………………… 40,000

E22-3B (10–15 minutes)

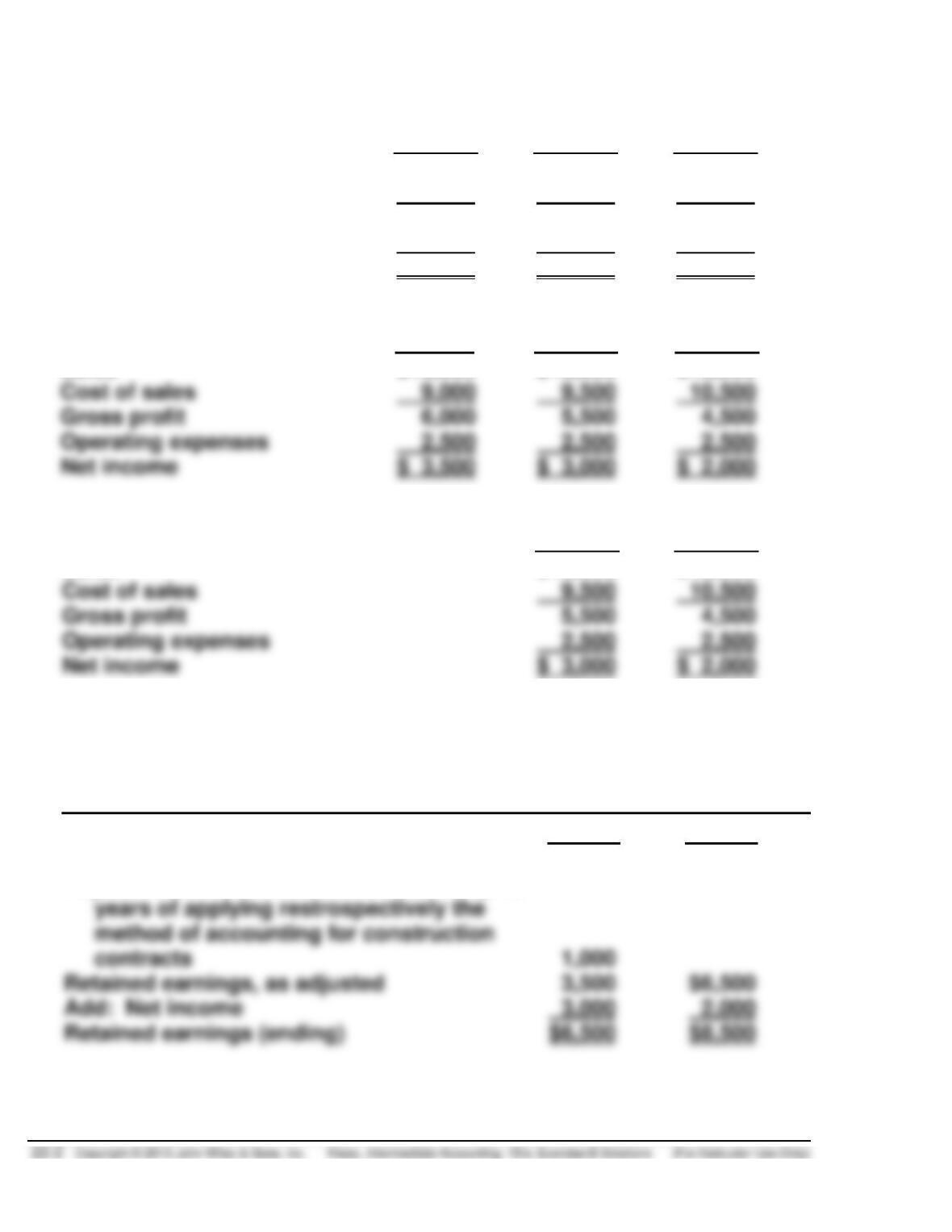

(a) LIFO:

2012 2013 2014

Sales $15,000 $15,000 $15,000

Cost of sales 10,000 10,500 11,000

Gross profit 5,000 4,500 4,000

Operating expenses 2,500 2,500 2,500

Net income $ 2,500 $ 2,000 $ 1,500

Average-cost:

2012 2013 2014

Sales $15,000 $15,000 $15,000

(b) Average-cost:

2013 2014

Sales $15,000 $15,000

(c) KYTO ELECTRONICS

Retained Earnings Statement

For the Year Ended December 31

2013 2014

Retained earnings, as reported $2,500

Adjustment for the cumulative effect on prior

E22-3B (Continued)

(d) On January 1, 2014, the Company elected to change its method of valuing

its inventory to the average-cost method; in all prior years inventory was

2014 2013

LIFO Average Difference LIFO Average Difference

Balance Sheet:

Inventory $3,500 $6,000 $2,500 $3,000 $5,000 $2,000

Retained

earnings 6,000 8,500 2,500 4,500 6,500 2,000

E22-4B (10–15 minutes)

(a) $60,000

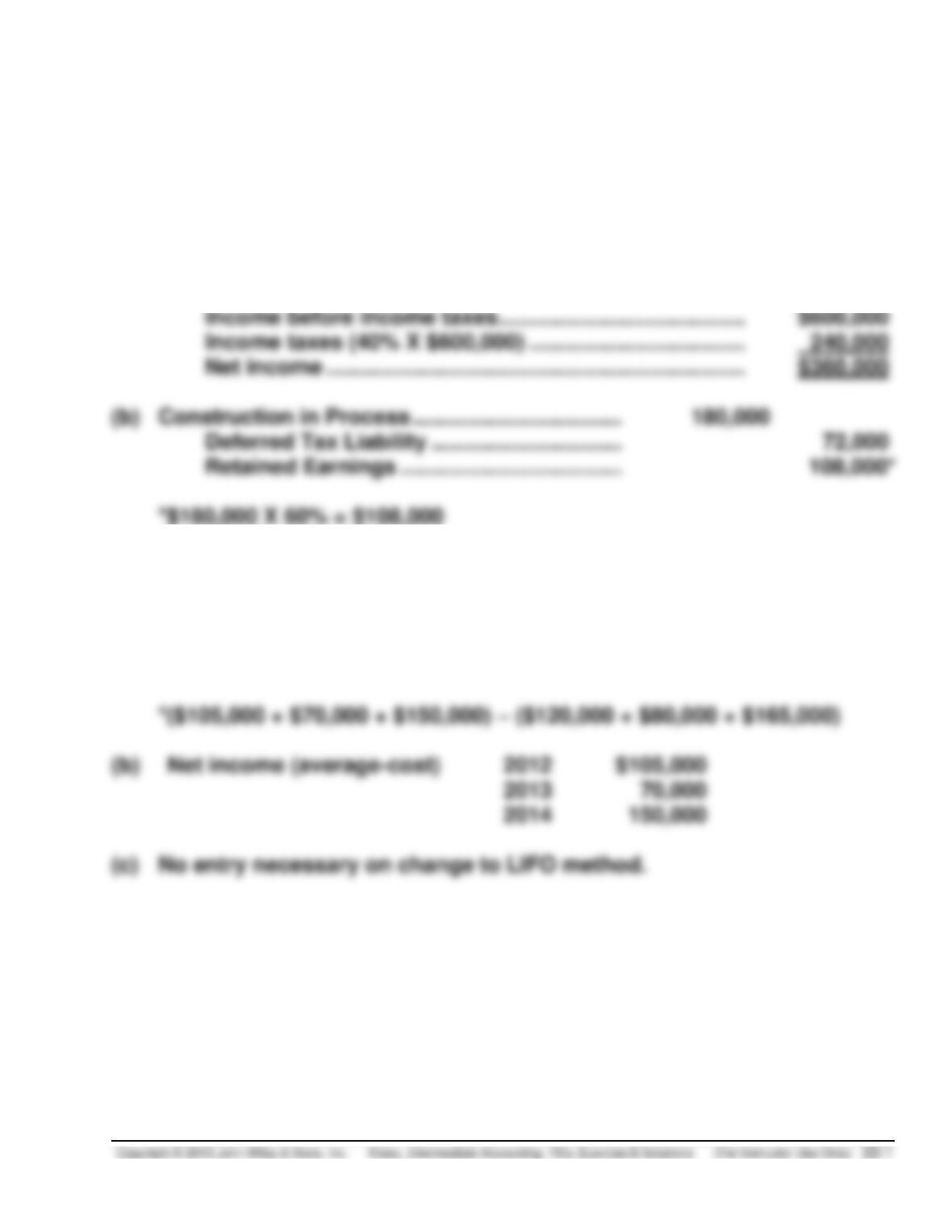

E22-5B (30–35 minutes)

(a) MARVEL INC.

Income Statement

For the Year Ended

2014

2013

Sales ………………………………………………………..

$10,000

$10,000

Cost of goods sold ……………………………………

5,600

5,500

Operating expenses

1,500

1,500

Income before profit sharing ……………….

Profit sharing expense ………………………………

Net income …………………………………………

(b) The profit sharing expense reflects an indirect effect of the change in

accounting principle. Indirect effects from periods before the change are

recorded in the year of the change. In this case, profit sharing expense

recorded in 2014 is composed of:

(c) Retained Earnings Statement

2014

Retained earnings, January 1, as reported ………………… $25,000

E22-6B (30–35 minutes)

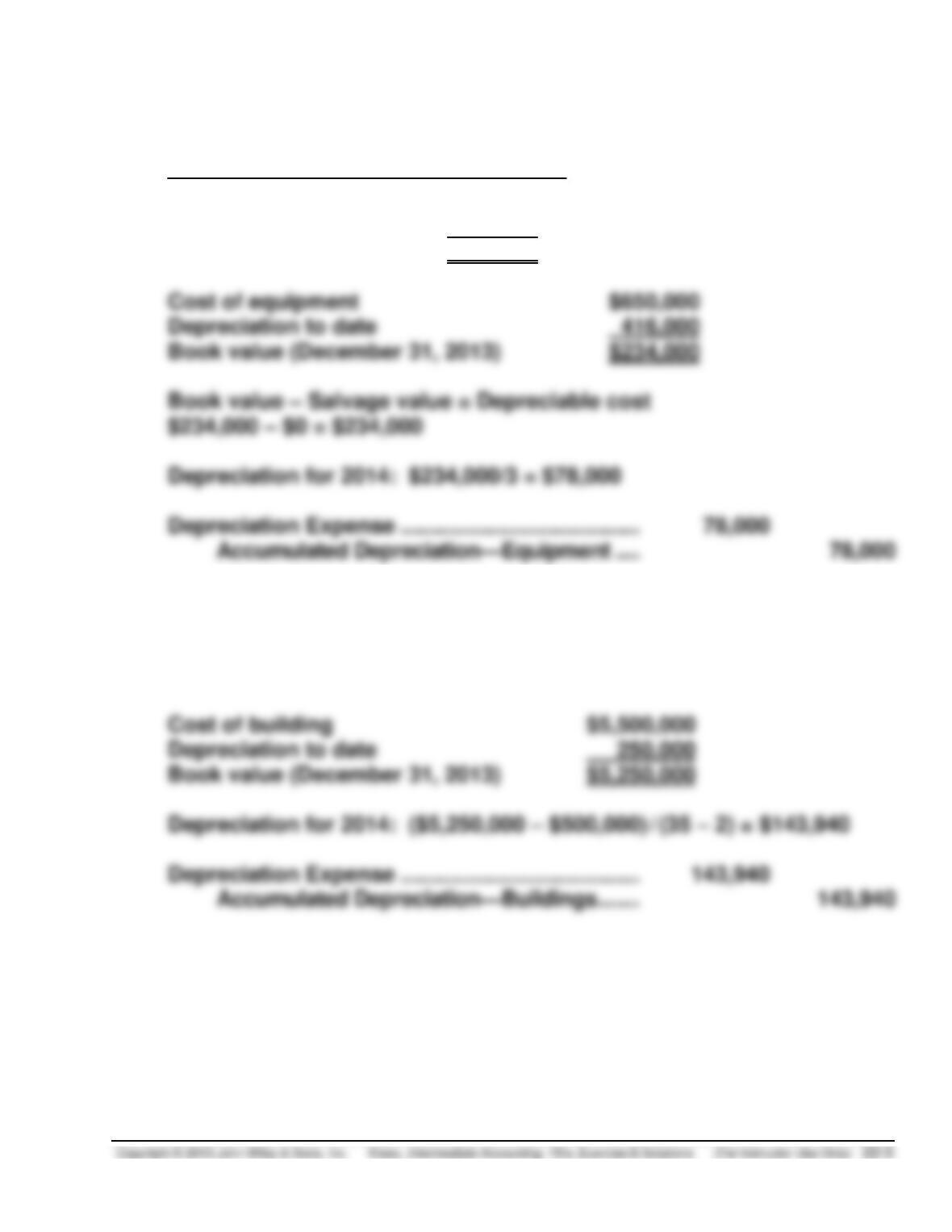

(a) Depreciation to date on equipment:

Double-declining balance depreciation

2012 (40% X $650,000) $260,000

2013 (40% X $390,000) 156,000

$416,000

(b) Depreciation to date on building:

($5,500,000 – $500,000)/40 years = $125,000 per year

$125,000 X 2 = $250,000 depreciation to date

E22-7B (25–35 minutes)

Depreciation for 2014 using double-declining balance method of depreciation

= $160,000 X 50% = $80,000

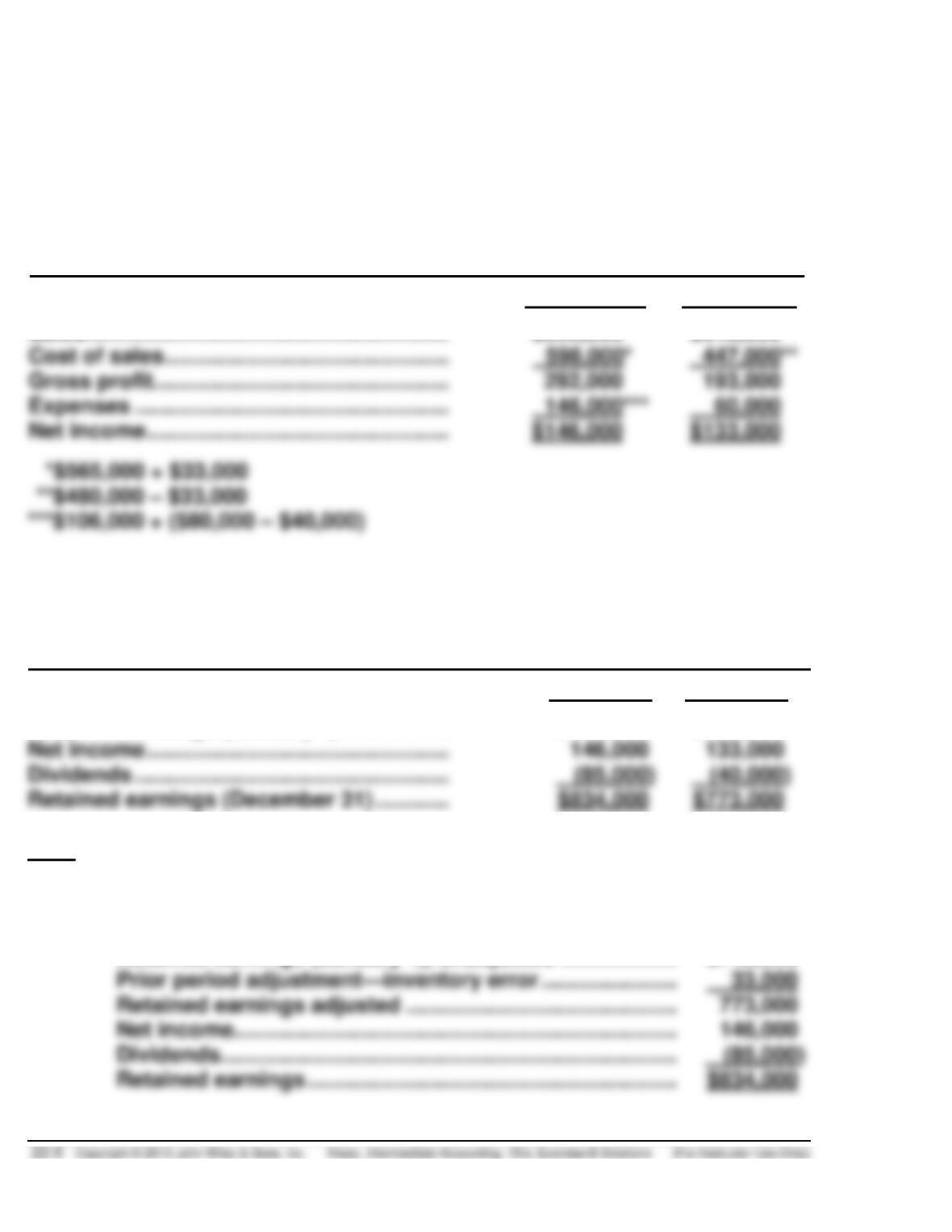

TITAN COMPANY

Comparative Income Statements

For the Years 2014 and 2013

2014

$890,000

2013

$640,000

Sales …………………………………………………..

Expenses ……………………………………………

TITAN COMPANY

Statement of Retained Earnings

For the Years 2014 and 2013

Retained earnings (January 1) ……………..

2014

$773,000

2013

$680,000

Dividends ……………………………………………

Note:

Another acceptable presentation for the retained earnings statement for 2014

is:

Retained earnings (January 1), unadjusted ………………. $740,000

E22-8B (5–10 minutes)

1. a 6. b

E22-9B (15–20 minutes)

December 31, 2014

Retained Earnings ($250,000 X 1/5) ………………………… 50,000

Accumulated Depreciation—Equipment ………….. 50,000

(To correct for the omission of depreciation

expense in 2013)

E22-10B (20–25 minutes)

Computation of 2015 depreciation expense on the building:

Cost of building …………………………………………………………… $2,500,000

E22-10B (Continued)

Computation of 2015 depreciation expense on the equipment:

Cost of equipment ……………………………………………………….. $300,000

E22-11B (10–15 minutes)

(a) No entry necessary.

(b) Depreciation Expense ………………………………………. 135,000*

Accumulated Depreciation—Equipment ……… 135,000

*Original cost $1,000,000

E22-12B (20–25 minutes)

(a) Depreciation Expense …………………………………….. 200,000*

Accumulated Depreciation ……………………….. 200,000

*Original cost $600,000

(b)

2015

2014

Income before depreciation expense……….

$760,000

$560,000

Income taxes …………………………………………

$336,000

E22-13B (10–15 minutes)

(a) The net income to be reported in 2015, using the retrospective approach,

would be computed as follows:

E22-14B (20–35 minutes)

(a) Inventory ………………………………………………………… 38,000

Retained Earnings …………………………………….. 38,000*

(b) Inventory ………………………………………………………… 40,000

Retained Earnings …………………………………….. 40,000*

E22-15B (15–20 minutes)

1. Goodwill …………………………………………………………. 20,000

Retained Earnings …………………………………….. 10,000

Amortization Expense ……………………………….. 10,000

E22-15B (Continued)

4. Depreciation Expense ………………………………………. 4,800

E22-16B (10–15 minutes)

1. Insurance Expense…………………………………………… 2,500

Prepaid Insurance……………………………………… 2,500

E22-17B (10–15 minutes)

Inventory ……………………………………………………………….. 73,600

Retained Earnings ……………………………………………. 44,100

Computations:

Effect on retained earnings

over (under) statement

Understatement of 2014 ending inventory …….

($(73,600)

Understatement of 2013 depreciation …………..

E22-18B (25–30 minutes)

(a) Effect of errors on 2015 net income: $106,500 overstatement

Computations:

Effect on 2015

net income over

(under) statement

Overstatement of 2013 ending inventory …………….

($ 0

(b) No effect on 2015 working capital as inventory error corrected itself.

(c) Effect of errors on retained earnings: $21,500 overstatement

Computations:

Effect on retained

earnings over

(under) statement

Overstatement of 2013 ending inventory …………

$ 0

E22-19B (20–25 minutes)

(a) 1. Supplies on Hand ……………………………………….. 6,500

Supplies Expense ………………………………… 6,500

2. Salary and Wages Expense …………………………. 4,000

Accrued Salaries and Wages ………………… 4,000

6. Accumulated Depreciation ($75,000 – $7,000) .. 68,000

Depreciation Expense ………………………….. 68,000

7. Accumulated Depreciation ………………………….. 45,000

Retained Earnings ……………………………….. 45,000

(b) 1. Supplies on Hand ……………………………………….. 6,500

Retained Earnings ……………………………….. 6,500

E22-19B (Continued)

5. Retained Earnings ($36,000 ÷ 2) …………………… 18,000

Prepaid Rent ……………………………………….. 18,000

(c)(1) Books have not been closed

6. Accumulated Depreciation ………………………….. 68,000

(c)(2) Books have been closed

6. Accumulated Depreciation ………………………….. 68,000

E22-20B (20–25 minutes)

2014

2015

Income before tax ……………………………………………..

$650,000

$521,800

Corrections:

Adjustment to interest income* …………………….

615

646

Sales erroneously included in 2015 income …..

Overstatement of 2014 ending inventory ……….

*Interest income for 2014 and 2015 was computed as follows:

Book Value of Bonds

Stated Interest

Effective Interest

2014

$92,300

$4,000

$4,615**

2015

92,915

4,000

4,646*

**$92,300 X 5%

Difference between effective interest at 5% and stated interest (4%):

E22-21B (10–15 minutes)

2014

2015

(1)

(3)

(5)

Over–

Under-

No

Over–

Under-

No

*E22-22B (25–30 minutes)

Because GEO has a 30% interest in Graphic Corp. as of 7/1/15, it is necessary

to first adjust the investment in Graphic to the equity method in prior periods.

The following schedule provides this information:

12/31/14

6/30/15

Dividends received ………………………………………………

Adjustment …………………………………………………………

Note: Goodwill is not amortized.

A computation of the ending balance in the investment account of Graphic

Corp. can now be made as follows:

Investment in Graphic Corp. 1/1/14 ……………………………… $2,700,000

*E22-23B (15–20 minutes)

(a) Prior to January 1, 2015, EchoLab Inc. carried the investment in Quiet

Inc. under the equity method of accounting, as evidenced from the

entries in the investment account. Use of the equity method was

appropriate because EchoLab’s interest in Quiet exceeded 20%.

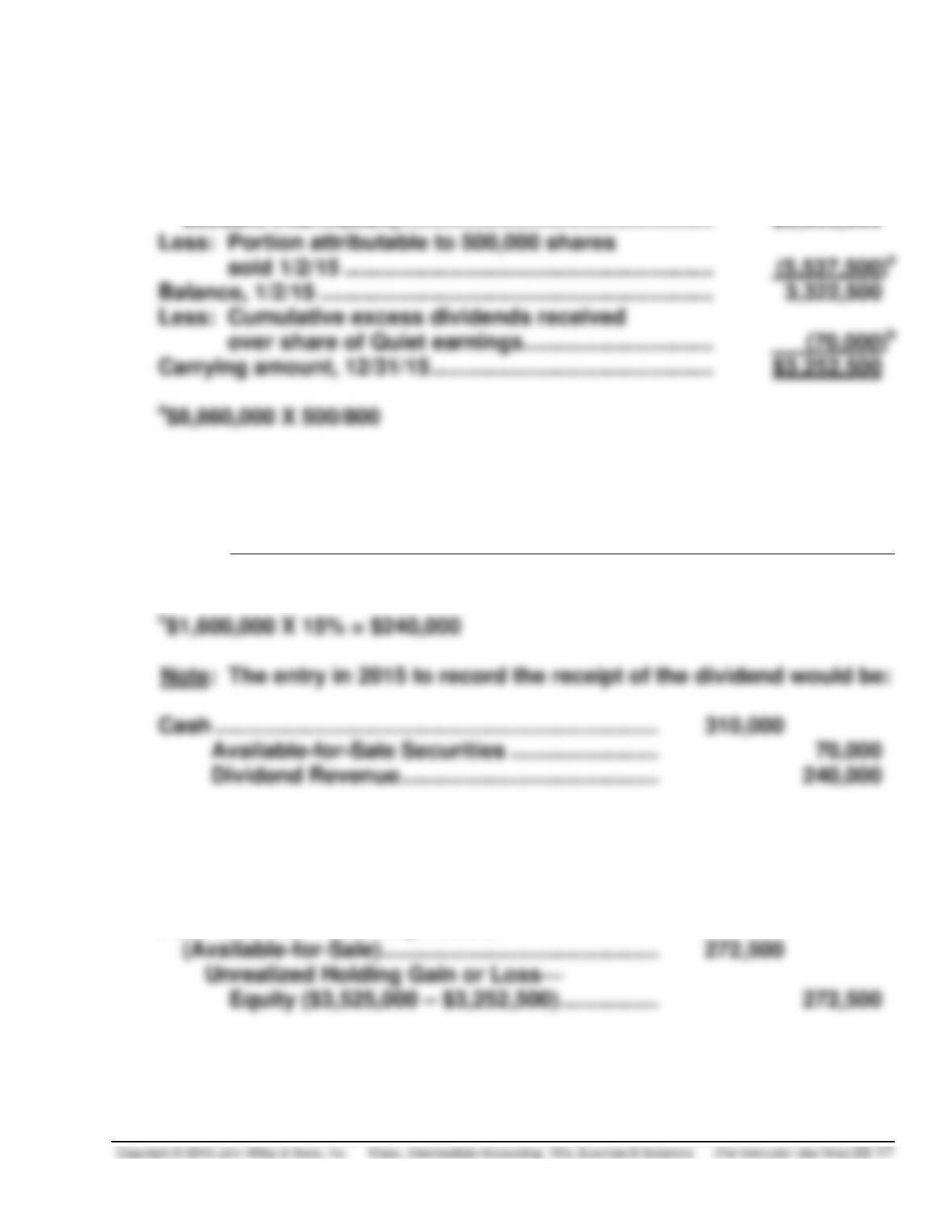

*E22-23B (Continued)

(b) The carrying amount of the investment in Quiet as of December 31, 2015,

would be computed as follows:

Carrying amount, 12/31/14 (from the given

account information) …………………………………………… $8,860,000

bComputation of excess dividends received over share of earnings:

Dividends

Received

Share of Quiet. Co.

Income

Excess Dividends Received

Over Share of Earnings

2015

$310,000

$240,000c

$(70,000)

(c) The entry to recognize the excess of fair value over the carrying amount

of the securities is as follows:

December 31, 2015

Securities Fair Value Adjustment