EXERCISE 4-3 (25–35 minutes)

(a)

Total net revenue:

Sales revenue

$390,000

Less: Sales discounts

$ 7,800

Sales returns

20,200

Net sales

Dividend revenue

Rent revenue

6,500

(b)

Net income:

Total net revenue (from a)

$447,300

Expenses:

Cost of goods sold

Selling expenses

Administrative expenses

Interest expense

12,700

Total expenses

Income before income tax

Income tax

31,000

(c)

Dividends declared:

Ending retained earnings

$134,000

Beginning retained earnings

114,400

Net increase

Less: Net income

EXERCISE 4-3 (Continued)

ALTERNATE SOLUTION

Beginning retained earnings

$114,400

Add: Net income

37,300

151,700

Less: Dividends declared

Dividends declared must be $17,700

($151,700 – $134,000)

Allocation to noncontrolling interest)

$37,300 – $ $17,000 = $ 20,300

EXERCISE 4-4 (20–25 minutes)

LEROI JONES INC.

Income Statement

For Year Ended December 31, 2014

Revenues

Net sales ($1,250,000(b) – $17,000) ……………………

$1,233,000

Expenses

Cost of goods sold………………………………………….

Selling expenses …………………………………………….

Administrative expenses …………………………..

Interest expense ……………………………………………..

Total expenses ……………………………………….

Income before income tax ………………………………………..

Income tax ……………………………………………………..

63,900

Net income ……………………………………………………….

$ 149,100

EXERCISE 4-4 (Continued)

Determination of amounts

(a) Administrative expenses

=

20% of cost of good sold

=

20% of $500,000

=

$100,000

(b) Gross sales X 8%

=

administrative expenses

=

$100,000 ÷ 8%

=

$1,250,000

=

four times administrative expenses.

(operating expenses consist of selling

and administrative expenses; since

selling expenses are 4/5 of operating

expenses, selling expenses are 4

times administrative expenses.)

=

4 X $100,000

=

$400,000

Earnings per share $7.46 ($149,100 ÷ 20,000)

Note: An alternative income statement format is to show income tax part of

expenses, and not as a separate item. In this case, total expenses are

$1,083,900.

EXERCISE 4-5 (30–35 minutes)

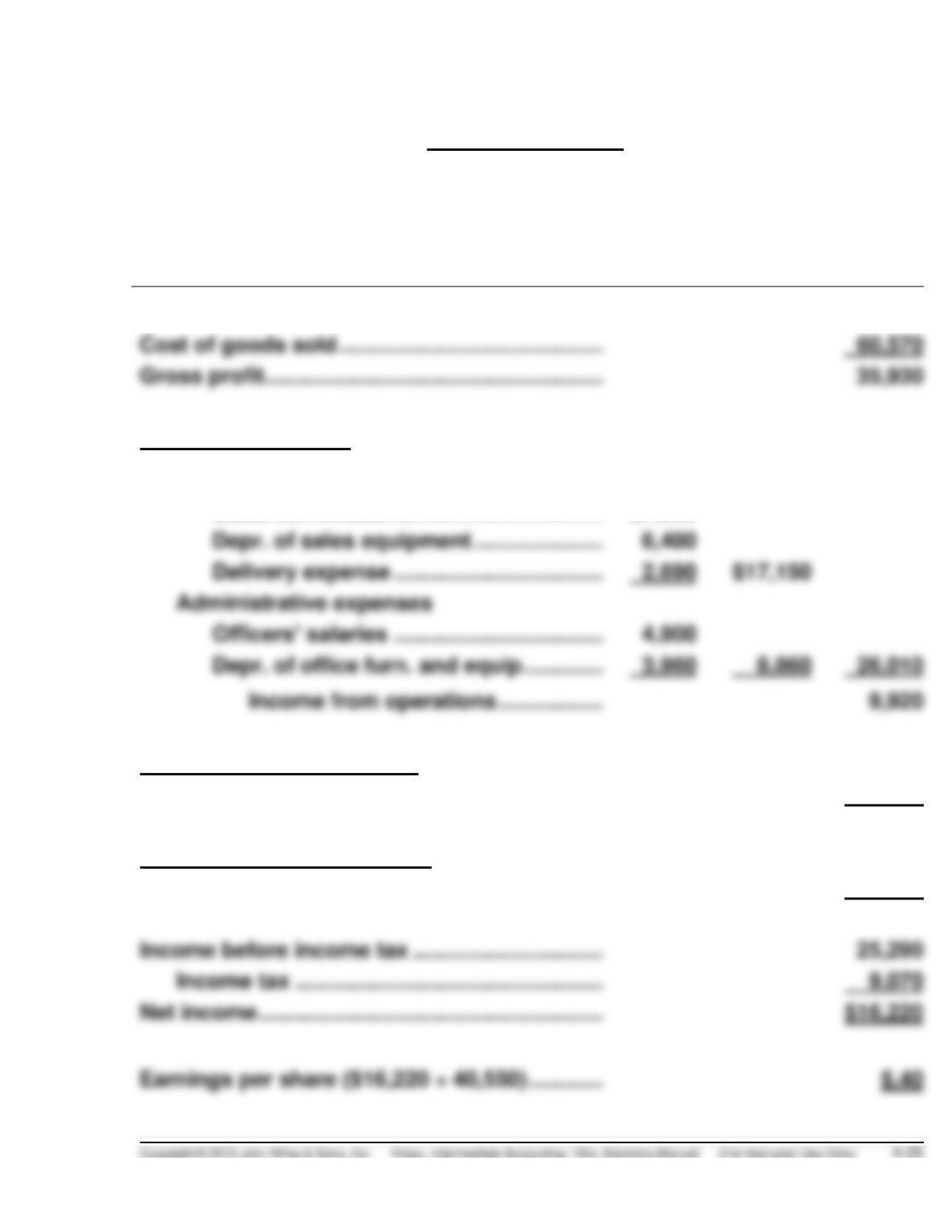

(a) Multiple-Step Form

P. BRIDE COMPANY

Income Statement

For the Year Ended December 31, 2014

(In thousands, except earnings per share)

Sales revenue ……………………………………………..

$96,500

Cost of goods sold ………………………………………

60,570

Gross profit …………………………………………………

35,930

Operating Expenses

Selling expenses

Sales commissions …………………………..

$7,980

Depr. of sales equipment …………………..

Delivery expense ………………………………

$17,150

Administrative expenses

Officers’ salaries ………………………………

Depr. of office furn. and equip. …………..

Income from operations ……………….

Other Revenues and Gains

Rent revenue …………………………………………

17,230

27,150

Other Expenses and Losses

Interest expense …………………………………….

1,860

Income before income tax …………………………..

25,290

Income tax …………………………………………….

9,070

Net income ………………………………………………….

EXERCISE 4-5 (Continued)

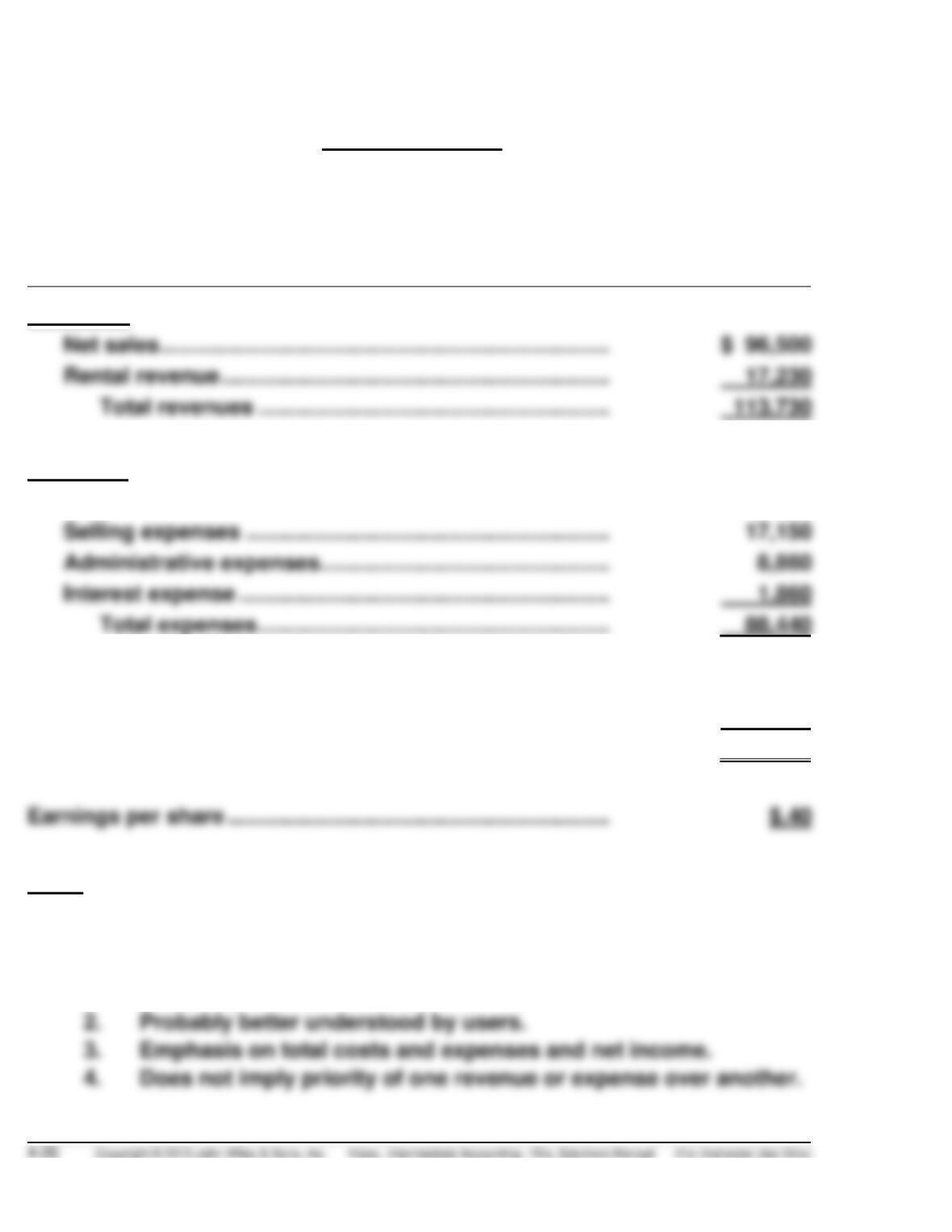

(b) Single-Step Form

P. BRIDE COMPANY

Income Statement

For the Year Ended December 31, 2014

(In thousands, except earnings per share)

Revenues

Net sales ………………………………………………………………….

$ 96,500

Rental revenue …………………………..…………………………..

17,230

Total revenues ……………………………………………………

Expenses

Cost of goods sold …………………………………………………..

60,570

Selling expenses ……………………………………………………..

17,150

Administrative expenses…………………………………………..

Interest expense ………………………………………………………

1,860

Total expenses ……………………………………………………

88,440

Income before income tax ……………………………………………..

25,290

Income tax …………………………………………………………………….

9,070

Net income ………………………………………………………………

$ 16,220

Earnings per share ……………………………………………………….

Note: An alternative income statement format for the single-step form is to

show income tax a part of expenses, and not as a separate item.

(c) Single-step:

1. Simplicity and conciseness.

EXERCISE 4-5 (Continued)

Multiple-step:

1. Provides more information through segregation of operating and

nonoperating items.

EXERCISE 4-6 (30–35 minutes)

MARIA CONCHITA ALONZO CORP.

Income Statement

For the Year Ended December 31, 2014

Sales Revenue

Sales revenue …………………………………………………..

$1,380,000

Less: Sales returns and allowances …………………..

Sales discounts ………………………………………

195,000

Net sales ………………………………………………………….

Cost of goods sold ……………………………………………

621,000

Gross profit on sales …………………………..…………………

Operating Expenses

Selling expenses ……………………………………………

194,000

Administrative and general expenses ……………..

291,000

Income from operations………………………………………….

EXERCISE 4-6 (Continued)

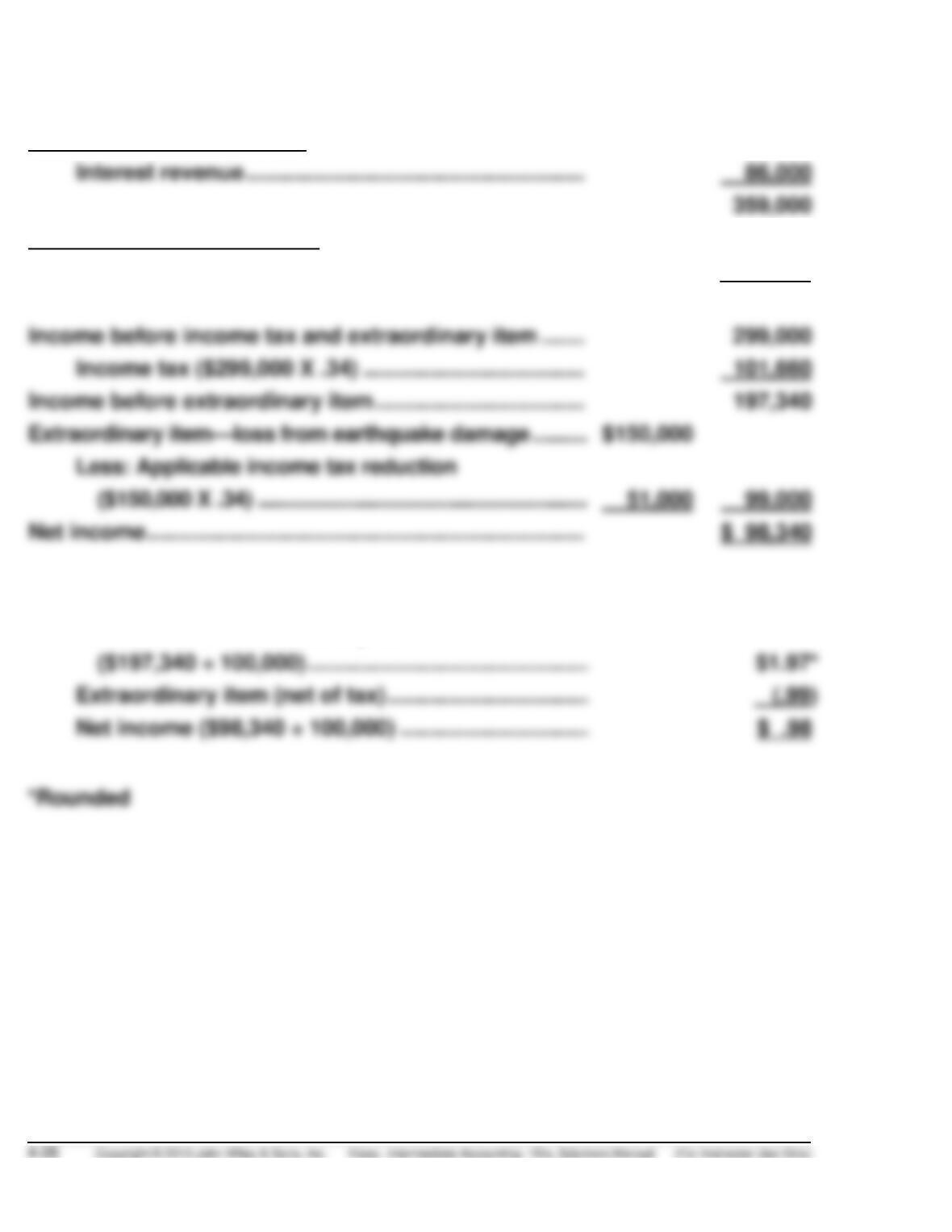

Other Revenues and Gains

Interest revenue ……………………………………………….

86,000

Other Expenses and Losses

Interest expense ………………………………………………

60,000

Income before income tax and extraordinary item …….

Income tax ($299,000 X .34) ………………………………

Income before extraordinary item …………………………....

Extraordinary item—loss from earthquake damage ……….

($150,000 X .34) …………………………………………………..

99,000

Net income ……………………………………………………………..

$ 98,340

Per share of common stock:

Extraordinary item (net of tax) …………………………….

Income before extraordinary item

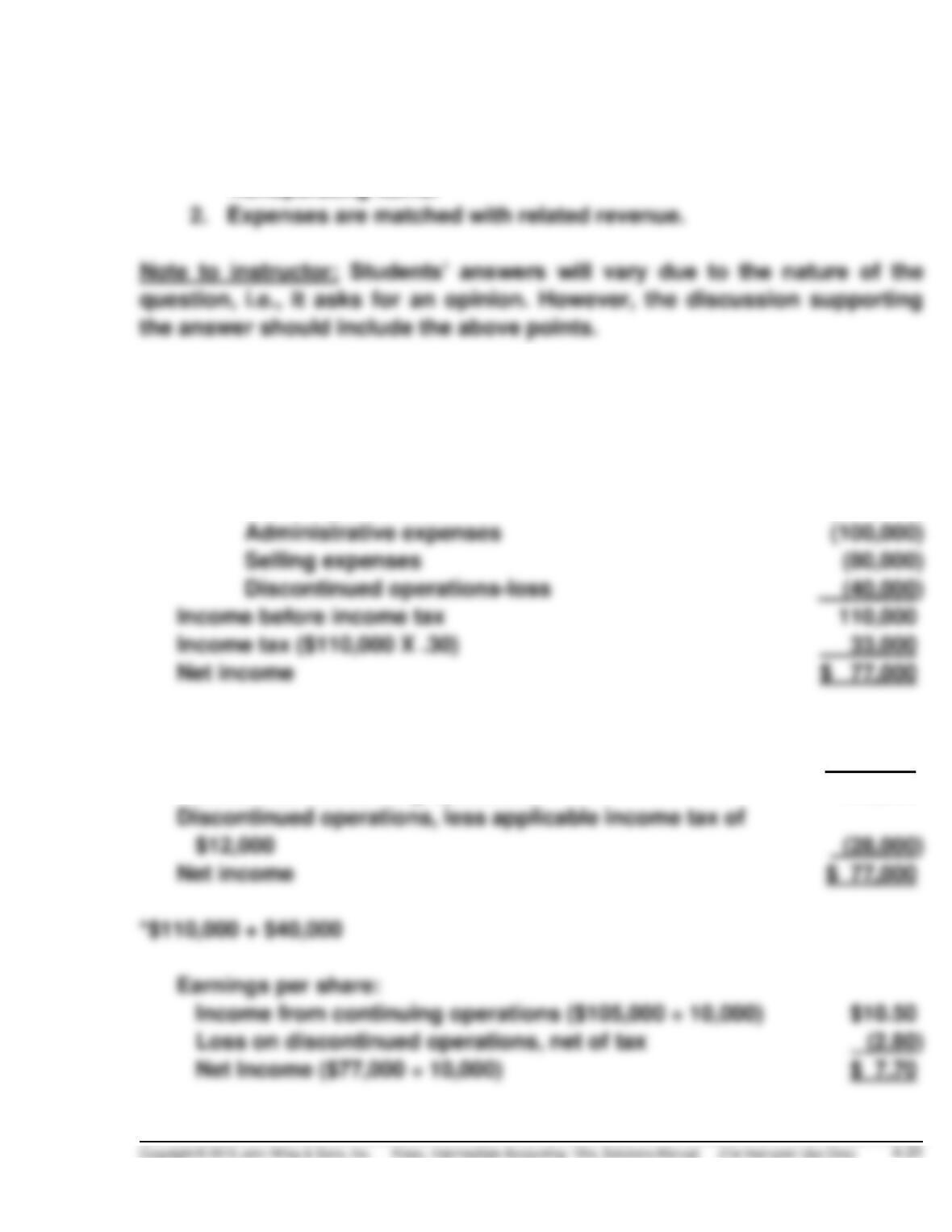

EXERCISE 4-7 (30–40 minutes)

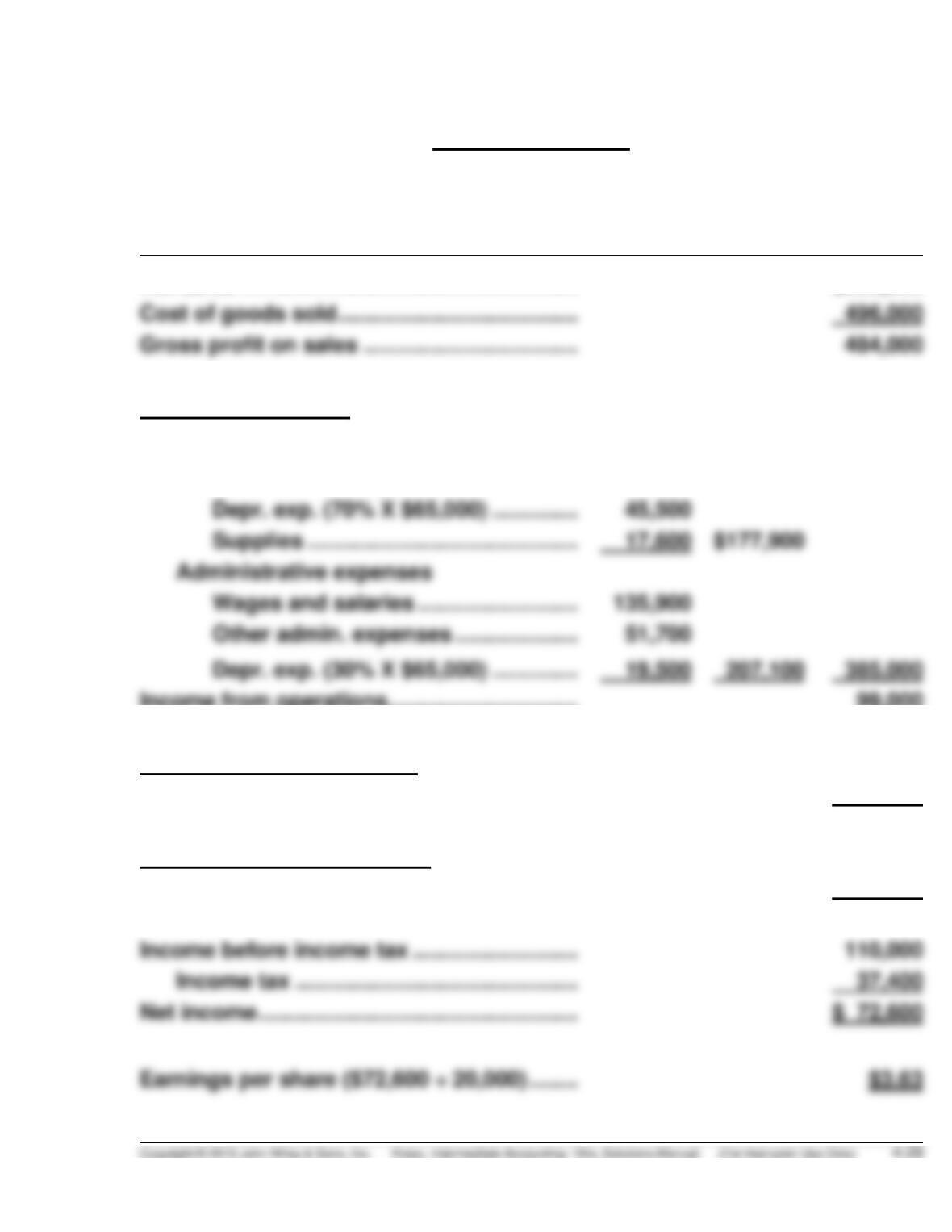

(a) Multiple-Step Form

LATIFA SHOE CO.

Income Statement

For the Year Ended December 31, 2014

Net sales ……………………………………………….

$980,000

Cost of goods sold …………………………………

Gross profit on sales …………………………..…

484,000

Operating Expenses

Selling expenses

Salaries and Wages ……………………..

$114,800

Depr. exp. (70% X $65,000) …………..

Supplies ……………………………………..

17,600

Administrative expenses

Wages and salaries ……………………..

Depr. exp. (30% X $65,000) …………..

19,500

Income from operations………………………….

99,000

Other Revenues and Gains

Rent revenue ……………………………………

29,000

128,000

Other Expenses and Losses

Interest expense ……………………………….

18,000

Income before income tax ………………………

110,000

Income tax ……………………………………….

37,400

Net income …………………………………………….

EXERCISE 4-7 (Continued)

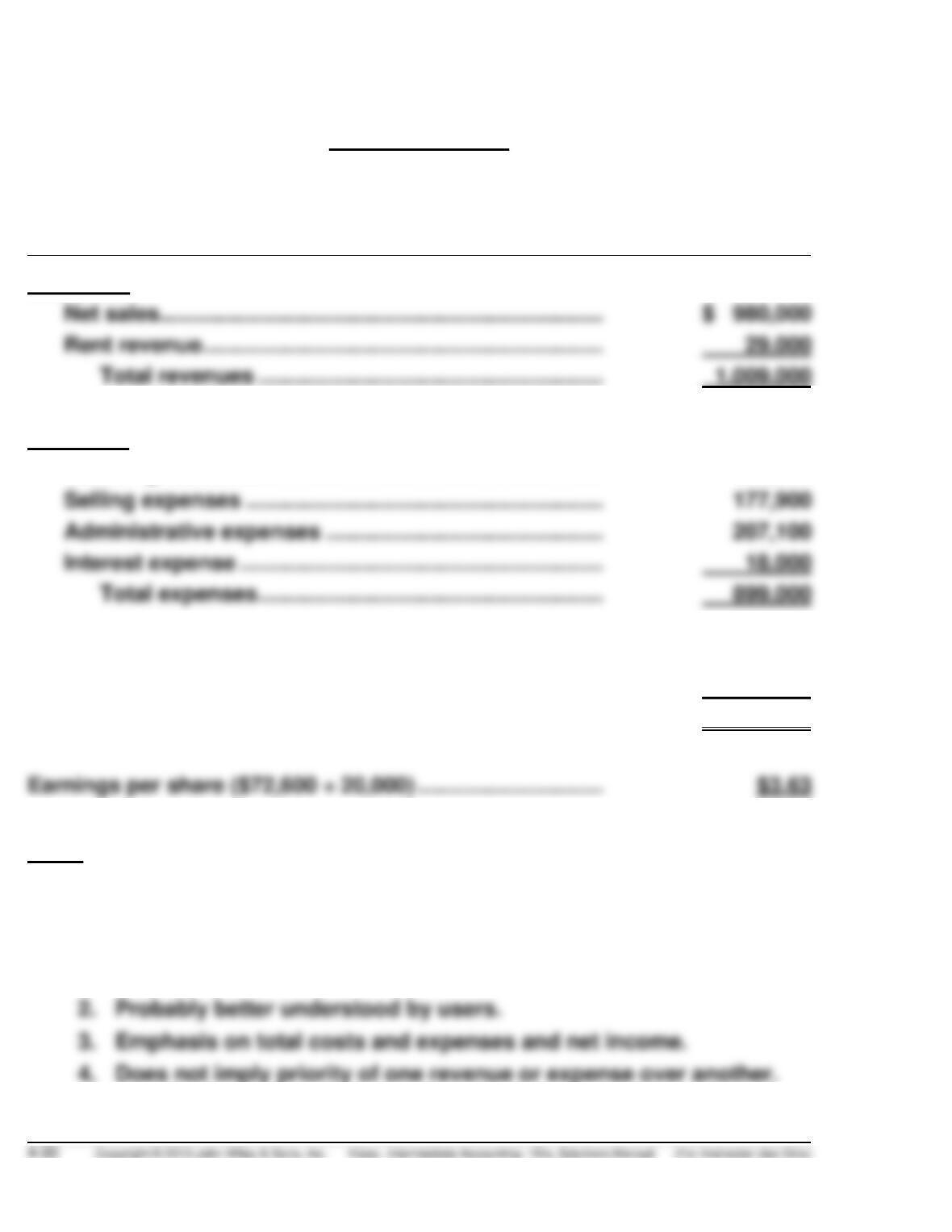

(b) Single-Step Form

LATIFA SHOE CO.

Income Statement

For the Year Ended December 31, 2014

Revenues

Net sales ………………………………………………………………

$ 980,000

Rent revenue …………………………..…………………………...

29,000

Total revenues ………………………………………………..

Expenses

Cost of goods sold ……………………………………………….

496,000

Selling expenses ………………………………………………….

177,900

Administrative expenses ………………………………………

207,100

Interest expense …………………………………………………..

18,000

Total expenses ………………………………………………..

899,000

Income before income tax ………………………………………….

110,000

Income tax ……………………………………………………………

37,400

Net income ………………………………………………………………..

$ 72,600

Note: An alternative income statement format for the single-step form is to

show income tax as part of expenses, and not as a separate item.

(c)

Single-step:

1. Simplicity and conciseness.

2. Probably better understood by users.

3. Emphasis on total costs and expenses and net income.

4. Does not imply priority of one revenue or expense over another.

EXERCISE 4-7 (Continued)

Multiple-step:

1. Provides more information through segregation of operating and

nonoperating items.

EXERCISE 4-8 (15–20 minutes)

(a) Net sales $ 540,000

Cost of goods sold (210,000)

(b) Income from continuing operations before income tax $150,000*

Income tax ($150,000 X .30) 45,000

Income from continuing operations 105,000

EXERCISE 4-9 (30–35 minutes)

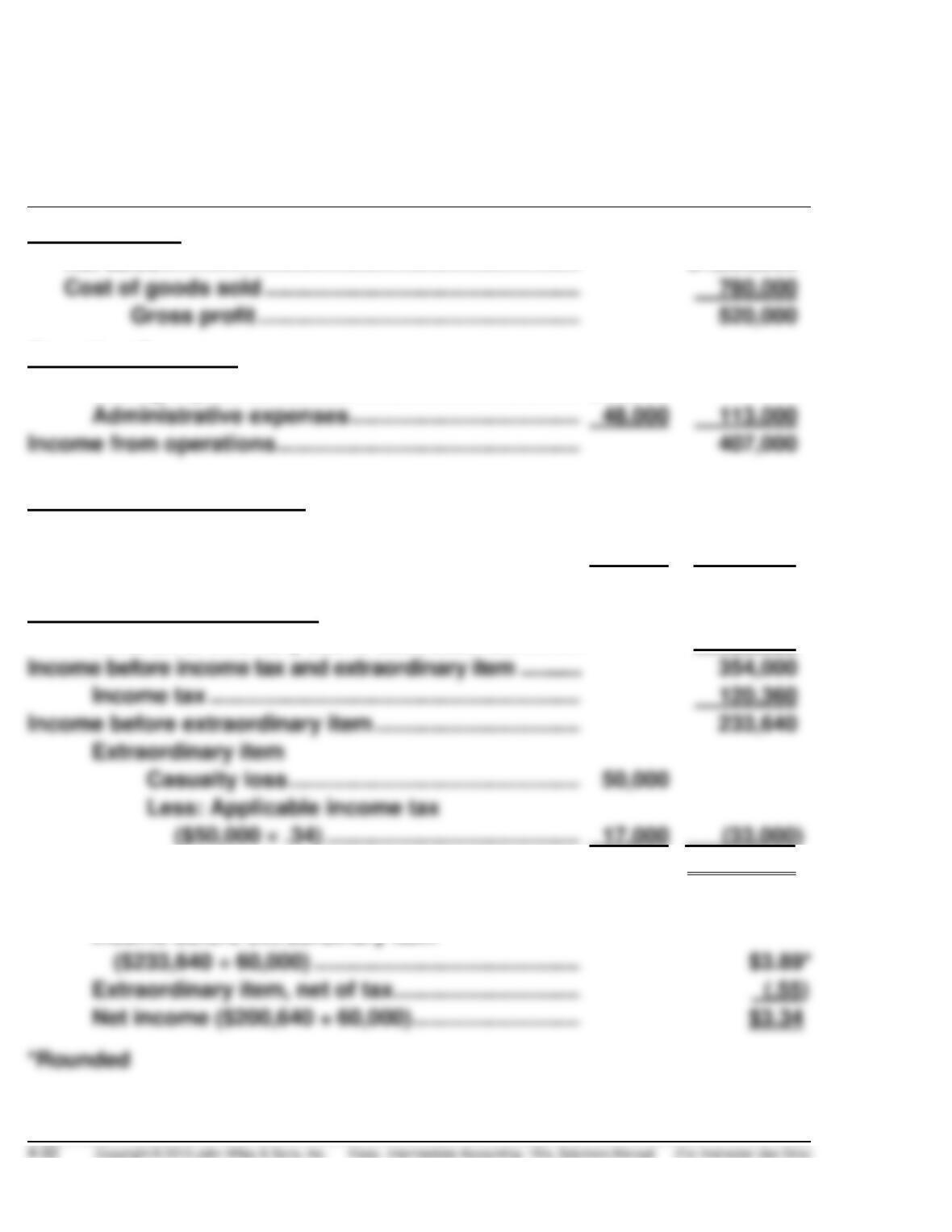

(a) IVAN CALDERON CORP.

Income Statement

For the Year Ended December 31, 2014

Sales Revenue

Net sales …………………………………………………………….

$1,300,000

Cost of goods sold ……………………………………………..

780,000

Gross profit ………………………………………………

520,000

Operating Expenses

Selling expenses …………………………………………….

$65,000

Administrative expenses …………………………………

113,000

Income from operations ……………………………………………

407,000

Other Revenues and Gains

Dividend revenue ……………………………………………

20,000

Interest revenue ……………………………………………..

7,000

27,000

434,000

Other Expenses and Losses

Write-off of inventory due to obsolescence …………..

80,000

Income before income tax and extraordinary item ………….

354,000

Income tax ……………………………………………………..

120,360

Income before extraordinary item ……………………………..

233,640

Extraordinary item

Casualty loss ………………………………………….

50,000

Less: Applicable income tax

($50,000 .34) …………………………………….

Net income ………………………………………………………………

$ 200,640

Per share of common stock:

($233,640 ÷ 60,000) …………………………..………….

Extraordinary item, net of tax …………………………..

Net income ($200,640 ÷ 60,000) ………………………..

Income before extraordinary item

EXERCISE 4-9 (Continued)

(b) IVAN CALDERON CORP.

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, Jan. 1, as reported ……………………………………….

$ 980,000

(depreciation error) (net of $18,700 tax) …………………………..

Retained earnings, Jan. 1, as adjusted ……………………………………….

Less: Dividends declared ……………………………………………………….

EXERCISE 4-10 (20–25 minutes)

Computation of net income:

2014 net income after tax ……………………………………………………

$33,000,000

2014 net income before tax

[$33,000,000 ÷ (1 – .34)] …………………………..

Add back major casualty loss …………………………..

Income from operations …………………………..

Income tax (34% X $68,000,000) …………………………..

Income before extraordinary item …………………………..

Extraordinary item:

Casualty loss ……………………………………………………….

Less: Applicable income tax reduction …………………………..

(11,880,000)

EXERCISE 4-10 (Continued)

Net income ……………………………………………………………………………..

$33,000,000

Less: Provision for preferred dividends

(8% of $4,500,000) ……………………………………………………….

360,000

Income available to common stockholders …………………………..

Common stock shares ……………………………………………………….

÷10,000,000

Income statement presentation

Per share of common stock:

Income before extraordinary item …………………………..

Extraordinary item, net of tax ………………………………………..

*Rounded

EXERCISE 4-11 (20–25 minutes)

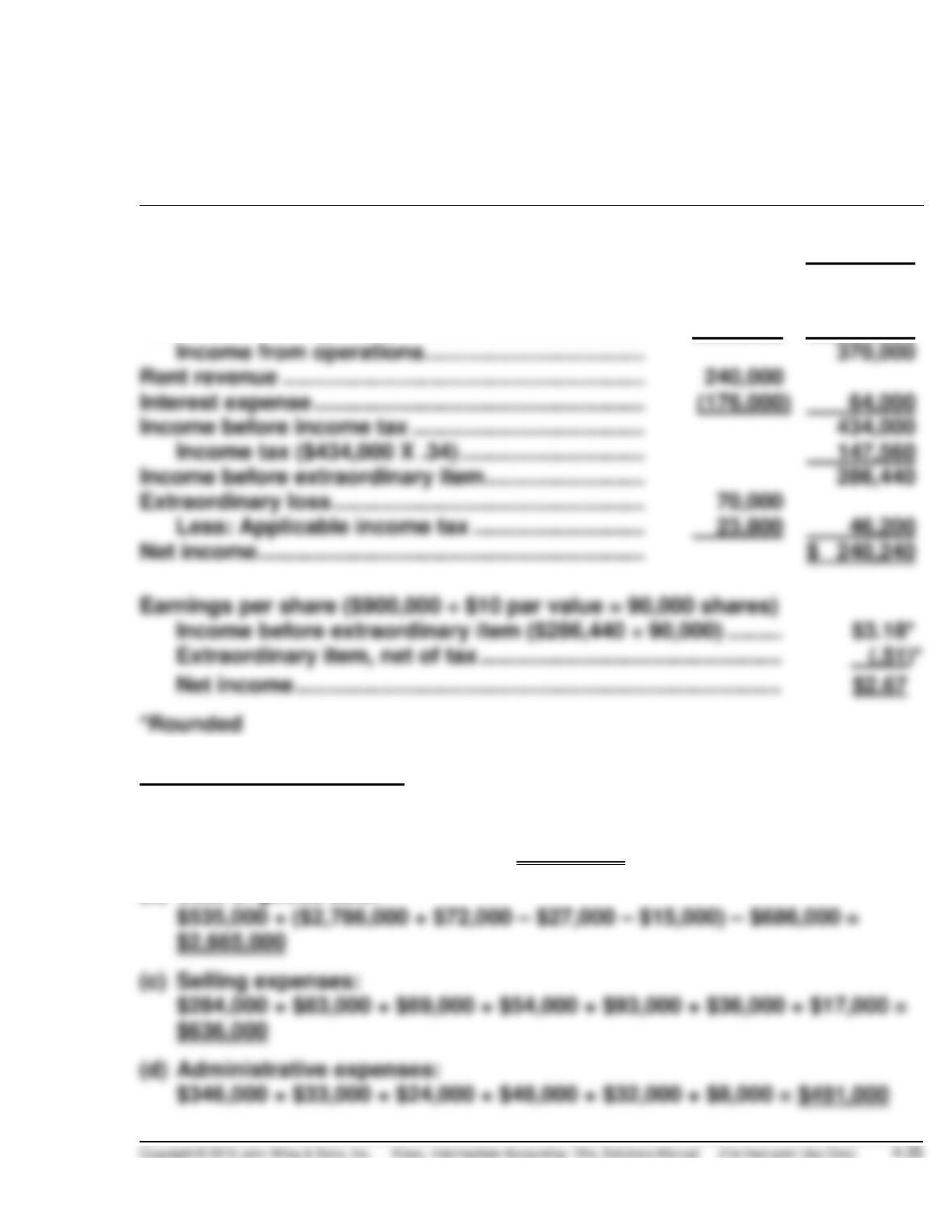

SPOCK CORPORATION

Income Statement

For the Year Ended December 31, 2014

Net sales(a) ………………………………………………………

$4,162,000

Cost of goods sold(b) ………………………………………..

2,665,000

Gross profit ………………………………………………..

1,497,000

Selling expenses(c) …………………………………………..

$636,000

Administrative expenses(d) ……………………………….

491,000

1,127,000

Income from operations ………………………………

Interest expense ………………………………………………

Income before income tax ………………………………..

Income before extraordinary item ……………………..

Extraordinary loss ……………………………………………

23,800

Income before extraordinary item ($286,440 ÷ 90,000) ………

Supporting computations

(a) Net sales:

$4,275,000 – $34,000 – $79,000 = $4,162,000

(b) Cost of goods sold:

EXERCISE 4-12 (20–25 minutes)

(a) EDDIE ZAMBRANO CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2014

Balance, January 1, as reported ……………………………………….

$225,000*

Correction for depreciation error (net of $10,000 tax) ………..

Balance, January 1, as adjusted……………………………………….

189,000

Add: Net income …………………………..…………………………………

144,000**

333,000

Less: Dividends declared ………………………………………………..

100,000

Balance, December 31 …………………………………………………….

$233,000

(b) Total retained earnings would still be reported as $233,000. A restriction

does not affect total retained earnings; it merely labels part of the retained

earnings as being unavailable for dividend distribution. Retained earnings

would be reported as follows:

EXERCISE 4-13 (15–20 minutes)

Net income:

Income from continuing operations

before income tax ……………………………………………………….

$23,650,000

Income tax (35% X $23,650,000) …………………………..

Income from continuing operations …………………………..

Discontinued operations

Loss before income tax…………………………..

Preferred dividends declared: …………………………..

$ 1,075,000

Weighted average common shares outstanding…………………………..

4,000,000

Earnings per share

Income from continuing operations …………………………..

$3.57*

Discontinued operations, net of tax …………………………..

EXERCISE 4-14 (15–20 minutes)

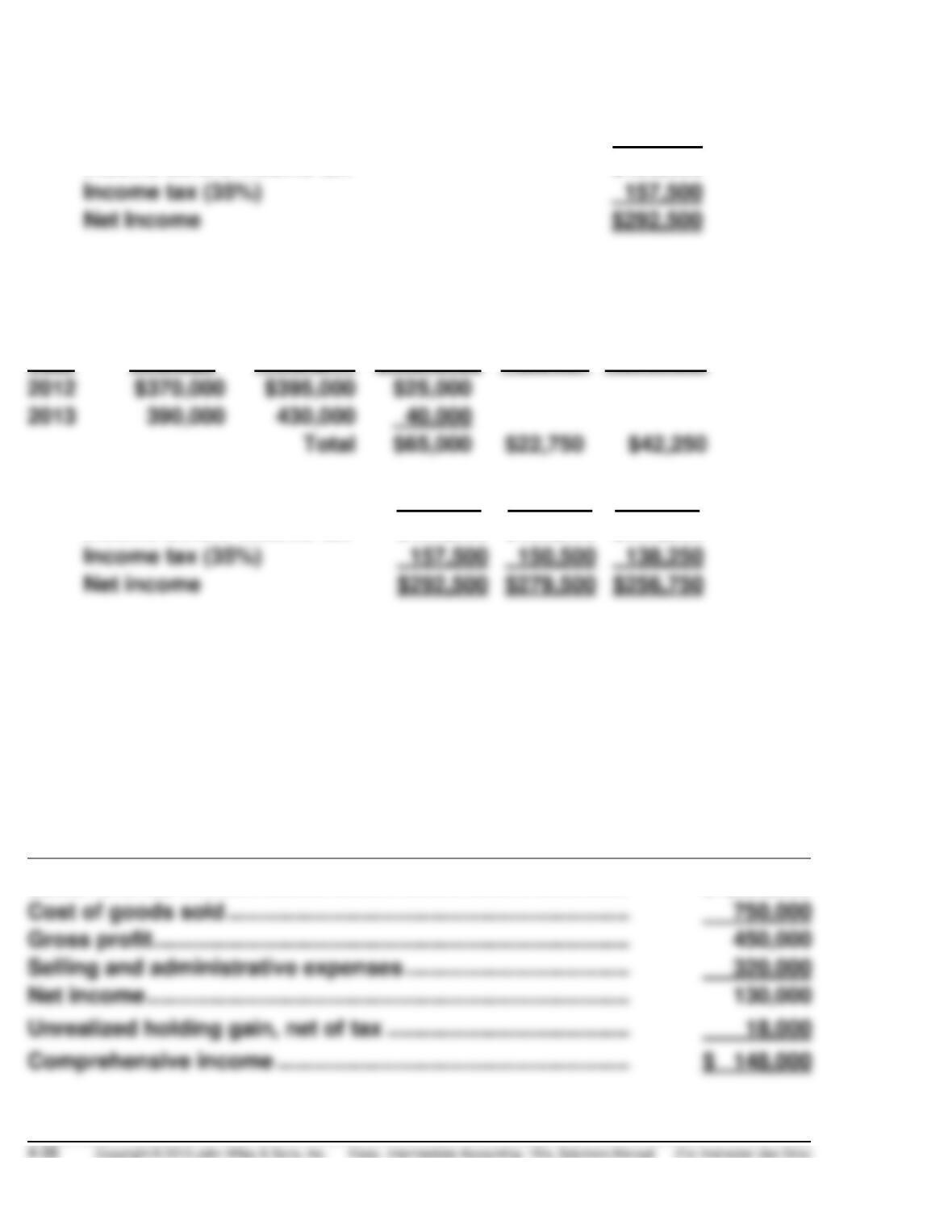

(a) 2014

Income before income tax $450,000

(b) Cumulative effect for years prior to 2014.

Year

Weighted-

Average

FIFO

Difference

Tax Rate

(35%)

Net Effect

$370,000

$22,750

(c)

2014

2013

2012

Income before income tax

$450,000

$430,000

$395,000

Income tax (35%)

Net income

$292,500

$279,500

$256,750

EXERCISE 4-15 (15–20 minutes)

(a)

ROXANNE CARTER CORPORATION

Statement of Comprehensive Income

For the Year Ended December 31, 2014

Sales revenue …………………………………………………………………

$1,200,000

Cost of goods sold ……………………………………………………….…

750,000

Gross profit …………………………..………………………………………..

Selling and administrative expenses ………………………………..

320,000

(b)

ROXANNE CARTER CORPORATION

Income Statement and Comprehensive Income Statement

For the Year Ended December 31, 2014

Sales ………………………………………………………………………………

$1,200,000

Cost of goods sold ………………………………………………………….

750,000

Gross profit …………………………………………………………………….

450,000

Selling and administrative expenses ………………………………..

320,000

Net income ……………………………………………………….…………….

$ 130,000

Comprehensive Income

EXERCISE 4-16 (15–20 minutes)

C. REITHER CO.

Statement of Stockholders’ Equity

For the Year Ended December 31, 2014

Total

Retained

Earnings

Accumulated

Other

Comprehensive

Income

Common

Stock

Beginning balance

$520,000

$ 90,000

$80,000

$350,000

Comprehensive income

Net income*

120,000

120,000

Other comprehensive income

Unrealized holding loss

Comprehensive income

Dividends

(10,000)

EXERCISE 4-17 (30–35 minutes)

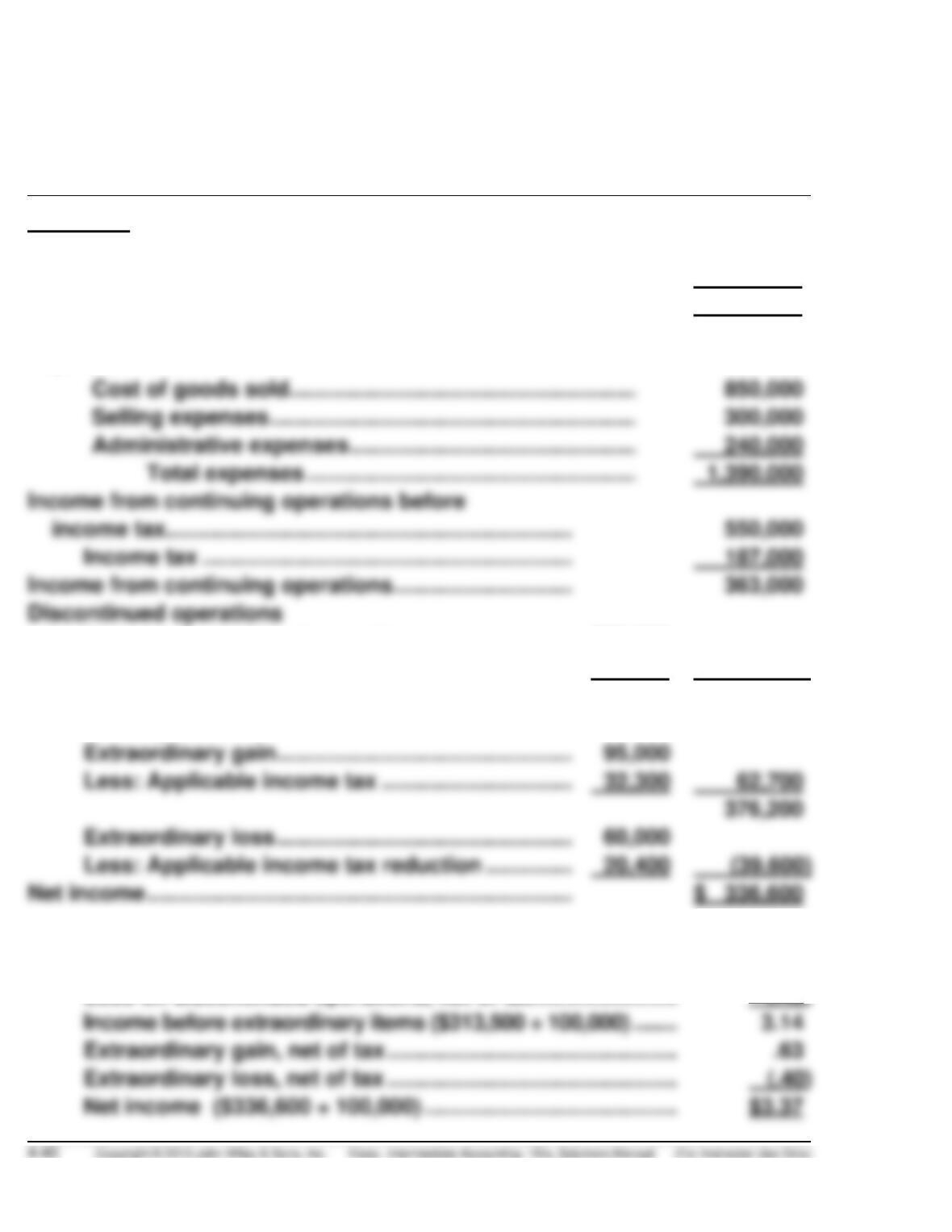

(a) ROLAND CARLSON INC.

Income Statement

For the Year Ended December 31, 2014

Revenues

Sales revenue …………………………………………………………………..

$1,900,000

Rent revenue …………………………………………………………………….

40,000

Total revenues ……………………………………………………….

1,940,000

Expenses

Cost of goods sold…………………………………………………..

850,000

Selling expenses ……………………………………………………..

300,000

Administrative expenses ………………………………………….

240,000

Total expenses ………………………………………………..

1,390,000

income tax ………………………………………………………….

550,000

Income tax …………………………………………………….

187,000

Income from continuing operations …………………………

363,000

Discontinued operations

Loss on discontinued operations ……………………

$75,000

Less: Applicable income tax reduction ……………

25,500

(49,500)

Income before extraordinary items ………………………….

313,500

Extraordinary items:

Extraordinary gain ………………………………………….

Less: Applicable income tax …………………………..

32,300

62,700

376,200

Extraordinary loss ………………………………………….

Less: Applicable income tax reduction ……………

20,400

(39,600)

Per share of common stock:

Income from continuing operations ($363,000 ÷ 100,000)………

$3.63

Loss on discontinued operations, net of tax …………………….

(.49)

Income before extraordinary items ($313,500 ÷ 100,000) ……….

Extraordinary gain, net of tax ………………………………………….

Extraordinary loss, net of tax ………………………………………….

(.40)