CHAPTER 17

Investments

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1. Debt securities.

1, 2, 3, 13

1

6

(a) Held-to-maturity.

4, 5, 7, 8,

10, 13, 21

1, 3

2, 3, 5

1, 7

(c) Available-for-sale.

4, 7, 8, 9,

10, 11, 21

2, 10

4

1, 2, 3, 4, 7

1

2. Bond amortization.

8, 9

1, 2, 3

3, 4, 5

1, 2, 3

3. Equity securities.

1, 12, 16

1

6

15, 21

12, 16,

19, 20

10, 11, 12

(b) Trading.

6, 7, 8, 10,

14, 15, 21

6

6, 7, 14, 15,

19, 20

6, 8

1, 3

(c) Equity method.

16, 17, 18,

19, 20

7

12, 13,

16, 17

8

4, 5

4. Comprehensive income.

22

9

10

9, 10, 12

5. Disclosures of investments.

18

10

5, 8, 9, 10,

11, 12

6. Fair value option.

25, 26, 27

19, 20, 21

7. Impairments.

24

10

18

3

28, 29, 30, 31,

32, 33, 34, 35

22, 23, 24,

25, 26, 27

13, 14, 15,

16, 17, 18

36, 37

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

accounting and

reporting treatment

for each category.

on bond investments.

1. Identify the three

categories of debt

securities and

describe the

1, 2, 3, 4, 5,

6, 7

1

CA17-1

3. Identify the

categories of equity

securities and

describe the

accounting and

reporting treatment

for each category.

12, 13, 14,

15

5, 6, 8

1, 6, 7, 8, 9,

11, 12, 14,

15, 16, 19,

20, 21

3, 5, 6, 8,

9, 10, 11,

12

CA17-1,

CA17-3,

CA17-5

value

option and the

accounting for

impairments

of debt and equity

investments.

6. Describe the

reporting of

reclassification

adjustments and the

accounting for

transfers between

categories.

22, 23

9

10

and accounting for

derivatives.

account for a fair

value hedge.

*9. Explain how to

account for a cash

flow hedge.

33, 34

24, 27

derivatives.

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E17-1

Investment classifications.

Simple

5–10

E17-2

Entries for held-to-maturity securities.

Simple

10–15

E17-3

Entries for held-to-maturity securities.

Simple

15–20

E17-4

Entries for available-for-sale securities.

Simple

10–15

E17-5

Effective-interest versus straight-line bond amortization.

Simple

20–30

E17-6

Entries for available-for-sale and trading securities.

Simple

10–15

E17-7

Trading securities entries.

Simple

10–15

E17-8

Available-for-sale securities entries and reporting.

Simple

presentation.

E17-10

Comprehensive income disclosure.

Moderate

20–25

E17-11

Equity securities entries.

Simple

20–25

E17-12

Journal entries for fair value and equity methods.

Simple

15–20

E17-13

Equity method.

Moderate

10–15

E17-14

Equity investment—trading.

Moderate

10–15

E17-15

Equity investments—trading.

Moderate

15–20

E17-16

Fair value and equity method compared.

Simple

15–20

E17-17

Equity method.

Simple

10–15

E17-18

Impairment of debt securities.

Moderate

15–20

E17-19

Fair value measurement.

Moderate

15–20

E17-20

Fair value measurement issues.

Moderate

15–20

Derivative transaction.

Moderate

15–20

Fair value hedge.

Moderate

20–25

Cash flow hedge.

Moderate

20–25

Fair value hedge.

Moderate

15–20

Call option.

Moderate

20–25

Cash flow hedge.

Moderate

25–30

P17-1

Debt securities.

Moderate

20–30

P17-2

Available-for-sale debt investments.

Moderate

30–40

P17-3

Available-for-sale investments.

Moderate

25–30

P17-4

Available-for-sale debt securities.

Moderate

25–35

P17-5

Equity securities entries and disclosures.

Moderate

25–35

P17-6

Trading and available-for-sale securities entries.

Simple

25–35

P17-7

Available-for-sale and held-to-maturity debt securities entries.

Moderate

25–35

P17-8

Fair value and equity methods.

Moderate

20–30

investments.

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Item

Description

Level of

Difficulty

Time

(minutes)

P17-10

Gain on sale of securities and comprehensive income.

Moderate

20–30

P17-11

Equity investments—available-for-sale.

Complex

30–40

P17-12

Available-for-sale securities—statement presentation.

Moderate

20–30

*P17-13

Derivative financial instrument.

Moderate

20–25

*P17-14

Derivative financial instrument.

Moderate

20–25

*P17-15

Free-standing derivative.

Moderate

20–25

*P17-16

Fair value hedge interest rate swap.

Moderate

30–40

*P17-17

Cash flow hedge.

Moderate

25–35

*P17-18

Fair value hedge.

Moderate

25–35

CA17-1

Issues raised about investment securities.

Moderate

25–30

CA17-2

Equity securities.

Moderate

25–30

CA17-3

Financial statement effect of equity securities.

Simple

20–30

CA17-4

Equity securities.

Moderate

15–25

CA17-5

Investment accounted for under the equity method.

Simple

15–25

CA17-6

Equity investment.

Moderate

25–35

CA17-7

Fair value.

Moderate

25–35

SOLUTIONS TO CODIFICATION EXERCISES

CE17-1

Master Glossary

(a) Trading securities are securities that are bought and held principally for the purpose of selling

them in the near term and therefore held for only a short period of time. Trading generally reflects

active and frequent buying and selling, and trading securities are generally used with the

objective of generating profits on short-term differences in price.

CE17-2

According to FASB ASC 235-10-S99-1 (Notes to Financial Statements—SEC Materials):

(n) Accounting policies for certain derivative instruments. Disclosures regarding accounting policies

shall include descriptions of the accounting policies used for derivative financial instruments and

(1) A discussion of each method used to account for derivative financial instruments and

derivative commodity instruments;

(2) The types of derivative financial instruments and derivative commodity instruments accounted

for under each method;

CE17-2 (Continued)

(6) The method used to account for derivatives when the designated item matures, is sold, is

(7) Where and when derivative financial instruments and derivative commodity instruments, and

Instructions to paragraph 4-08(n).

1. For purposes of this paragraph (n), derivative financial instruments and derivative

commodity instruments (collectively referred to as “derivatives”) are defined as follows:

(i) Derivative financial instruments have the same meaning as defined by generally

accepted accounting principles (see Financial Accounting Standards Board

(“FASB”), Statement of Financial Accounting Standards No. 119, “Disclosure about

Derivative Financial Instruments and Fair Value of Financial Instruments,” (“FAS 119”)

paragraphs 5–7, (October 1994)), and include futures, forwards, swaps, options,

and other financial instruments with similar characteristics.

2. For purposes of paragraphs (n)(2), (n)(3), (n)(4), and (n)(7), the required disclosures

should address separately derivatives entered into for trading purposes and derivatives

entered into for purposes other than trading.

3. For purposes of paragraph (n)(6), anticipated transactions means transactions (other

than transactions involving existing assets or liabilities or transactions necessitated by

4. Registrants should provide disclosures required under paragraph (n) in filings with the

Commission that include financial statements of fiscal periods ending after June 15, 1997.

[45 FR 63669, Sept. 25, 1980, as amended at 46 FR 56179, Nov. 16, 1981; 50

CE17-3

According to FASB ASC 323-10–35-20 (Investments—Equity Method and Joint Ventures—Subsequent

Measurement):

The investor ordinarily shall discontinue applying the equity method if the investment (and net

CE17-4

According to FASB ASC 815-10–45-4 (Derivatives and Hedging—Other Presentation Matters—Balance

Sheet Netting);

Unless the conditions in paragraph 210–20–45-1 are met, the fair value of derivative instruments in a

ANSWERS TO QUESTIONS

1. A debt security is an instrument representing a creditor relationship with an entity. Debt securities

include U.S. government securities, municipal securities, corporate bonds, convertible debt, and

commercial paper. Trade accounts receivable and loans receivable are not debt securities

because they do not meet the definition of a security.

securities.

2. The variety in bond features along with the variability in interest rates permits investors to shop

for exactly the investment that satisfies their risk, yield, and marketability desires, and permits

issuers to create a debt instrument best suited to their needs.

3. Cost includes the total consideration to acquire the investment, including brokerage fees and

other costs incidental to the purchase.

4. The three types of classifications are:

5. A debt investment should be classified as held-to-maturity only if the company has both: (1) the

positive intent and (2) the ability to hold those securities to maturity.

8. $3,500,000 X 10% = $350,000; $350,000 ÷ 2 = $175,000. Wheeler would make the following entry:

10. Unrealized holding gains and losses for trading securities should be included in net income for

the current period. Unrealized holding gains and losses for available-for-sale securities should be

reported as other comprehensive income and as a separate component of stockholders’ equity.

Unrealized holding gains and losses are not recognized for held-to-maturity securities.

Questions Chapter 17 (Continued)

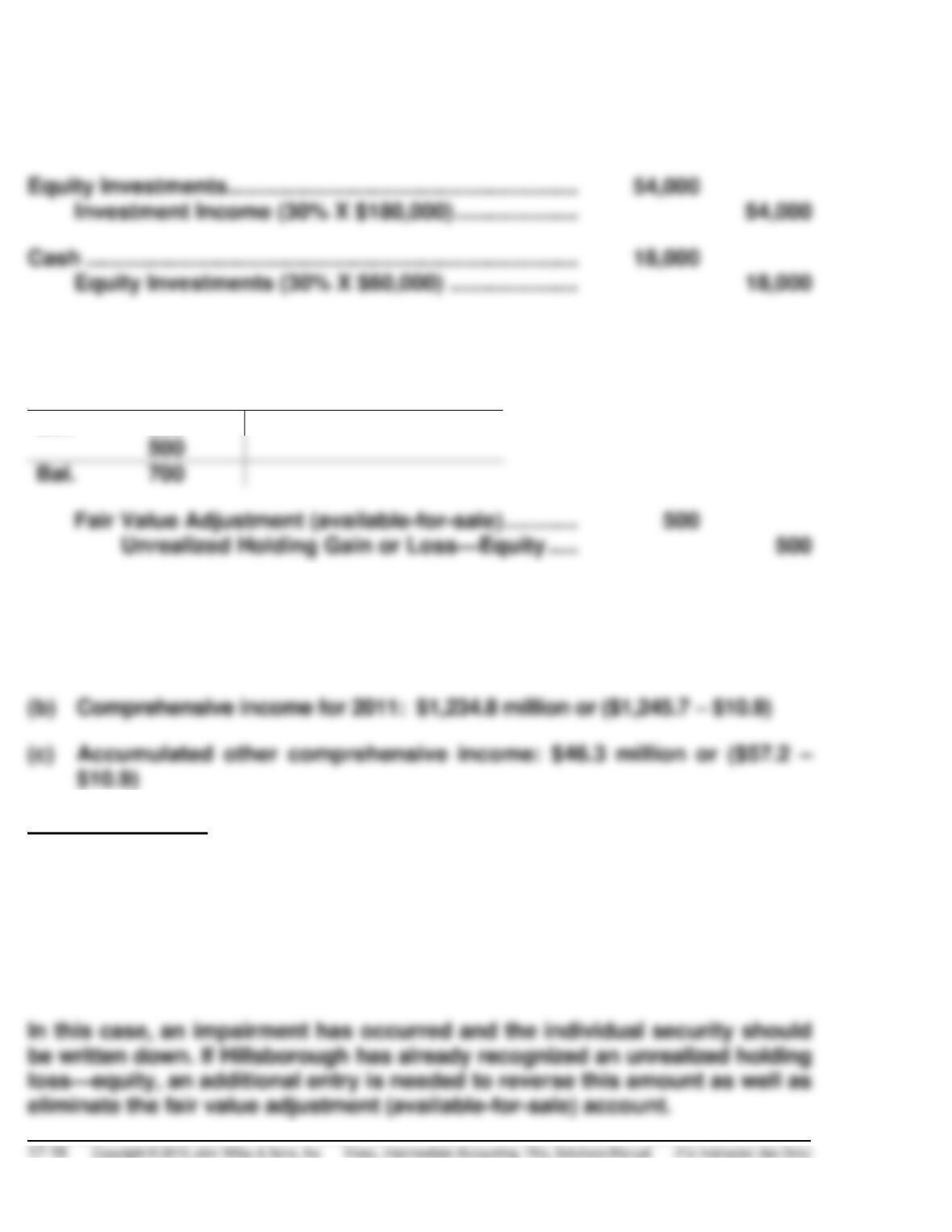

11. (a) Unrealized Holding Gain or Loss—Equity ………………………………. 60,000

12. Investments in equity securities can be classified as follows:

(a) Holdings of less than 20% (fair value method)—investor has passive interest.

13. Investments in stock do not have a maturity date and therefore cannot be classified as held–to–

maturity securities.

14. Selling price of 10,000 shares at $27.50 ……………………………………….. $275,000

Less: Brokerage commissions ……………………………………………………. (1,770)

15. Both trading and available-for-sale equity securities are reported at fair value. However, any

16. Significant influence over an investee may result from representation on the board of directors,

participation in policy-making processes, material intercompany transactions, interchange of

managerial personnel, or technological dependency. An investment (direct or indirect) of 20% or

more of the voting stock of an investee constitutes significant influence unless there exists

evidence to the contrary.

17. Under the equity method, the investment is originally recorded at cost, but is adjusted for

18. The 20% rule is that an investment (direct or indirect) of 20 percent or more of the voting stock of

an investee leads to the presumption that an investor has the ability to exercise significant

influence over an investee and the equity method should be used. However, there are other

Questions Chapter 17 (Continued)

Factors that could lead to a conclusion of no significant ownership, when ownership in above

19. Dividends subsequent to acquisition should be accounted for as a reduction in the Equity

Investment received account.

20. Ordinarily, Raleigh Corp. should discontinue applying the equity method and not provide for

additional losses beyond the carrying value of $170,000. However, if Raleigh Corp.’s loss is not

21. Trading securities should be reported at aggregate fair value as current assets. Individual held-to–

maturity and available-for-sale securities are classified as current or noncurrent depending upon the

22. Reclassification adjustments are necessary to insure that double counting does not result when

realized gains or losses are reported as part of net income but also are shown as part of other

comprehensive income in the current period or in previous periods.

23. When a security is transferred from one category to another, the transfer should be recorded at

24. A debt security is impaired when “it is probable that the investor will be unable to collect all

25. Fair value is defined as “the price that would be received to sell an asset or paid to transfer a

liability in an orderly transaction between market participants at the measurement date.” Fair

value is therefore a market-based measure.

26. The fair value option gives companies the option to report most financial instruments at fair value

with all gains and losses related to changes in fair value reported in the income statement. This

27. No. The fair value option is generally available only at the time a company first purchases the

Questions Chapter 17 (Continued)

*28. An underlying is a special interest rate, security price, commodity price, index of prices or rates,

or other market-related variable. Changes in the underlying determine changes in the value of

*29. See illustration below:

Feature

Traditional Financial Instrument

(e.g., Trading Security)

Derivative Financial Instrument

(e.g., Call Option)

Payment Provision

Stock price times the number

of shares.

Change in stock price (underlying)

times number of shares (notional

amount).

Initial Investment

For a traditional financial instrument, an investor generally must pay the full cost, while derivatives

require little initial investment. In addition, the holder of a traditional security is exposed to all risks

*30. The purpose of a fair value hedge is to offset the exposure to changes in the fair value of a

recognized asset or liability or of an unrecognized firm commitment.

*31. The unrealized holding gain or loss on available-for-sale securities should be reported as income

*32. This is likely a setting where the company is hedging the fair value of a fixed-rate debt obligation.

The fixed payments received on the swap will offset fixed payments on the debt obligation. As a

*33. A cash flow hedge is used to hedge exposures to cash flow risk, which is exposure to the

*34. Derivatives used in cash flow hedges are accounted for at fair value on the balance sheet but

gains or losses are recorded in equity as part of other comprehensive income.

*35. A hybrid security is a security that has characteristics of both debt and equity and often is a

Questions Chapter 17 (Continued)

*36. The voting-interest model is when a company owns more than 50% of another company. The

*37. A variable-interest entity (VIE) is an entity that has one of the following characteristics:

(a) Insufficient equity investment at risk. Stockholders are assumed to have sufficient capital

investment to support the entity’s operations. If thinly capitalized, the entity is considered

a VIE and is subject to the risk-and-reward model.

(b) Stockholders lack decision-making rights. In some cases, stockholders do not have the

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 17-1

(a) Debt Investments ……………………………………………… 74,086

Cash …………………………………………………………. 74,086

BRIEF EXERCISE 17-2

(a) Debt Investments (available-for-sale) …………………. 74,086

Cash …………………………………………………………. 74,086

BRIEF EXERCISE 17-3

(a) Debt Investments ……………………………………………… 65,118

Cash …………………………………………………………. 65,118

BRIEF EXERCISE 17-4

(a) Debt Investments (trading) ……………………………… 50,000

Cash ……………………………………………………….. 50,000

BRIEF EXERCISE 17-5

(a) Equity Investments (available-for-sale) …………….. 13,200

Cash ……………………………………………………….. 13,200

BRIEF EXERCISE 17-6

(a) Equity Investments (trading) …………………………... 13,200

Cash ……………………………………………………….. 13,200

BRIEF EXERCISE 17-7

Equity Investments ………………………………………………… 300,000

Cash ………………………………………………………………. 300,000

BRIEF EXERCISE 17-8

Fair Value Adjustment (available-for-sale)

Bal. 200

Bal. 700

BRIEF EXERCISE 17-9

(a) Other comprehensive income (loss) for 2011: ($10.9) million

Note to instructor: In 2011, Starbucks also reported foreign currency trans–

lation adjustments, which affected accumulated other comprehensive income.

BRIEF EXERCISE 17-10

Loss on Impairment …………………………..…………………….. 10,000

Debt Investments (available-for-sale) …………………. 10,000

SOLUTIONS TO EXERCISES

EXERCISE 17-1 (5–10 minutes)

(a) 1. (b) 2. (c) 1. (d) 2. (e) 2. (f) 3.

EXERCISE 17-2 (10–15 minutes)

(a) January 1, 2013

Debt Investments ………………………………………. 300,000

Cash ………………………………………………….. 300,000

(b) December 31, 2013

EXERCISE 17-3 (15–20 minutes)

(a) January 1, 2013

(b) Schedule of Interest Revenue and Bond Premium Amortization

Effective-Interest Method

12% Bonds Sold to Yield 10%

Date

Cash

Received

Interest

Revenue

Premium

Amortized

Carrying Amount

of Bonds

1/1/13

—

—

—

$322,744.44

12/31/13

12/31/14

12/31/15

12/31/16

12/31/17

EXERCISE 17-3 (Continued)

(c) December 31, 2013

Cash …………………………………………………………… 36,000

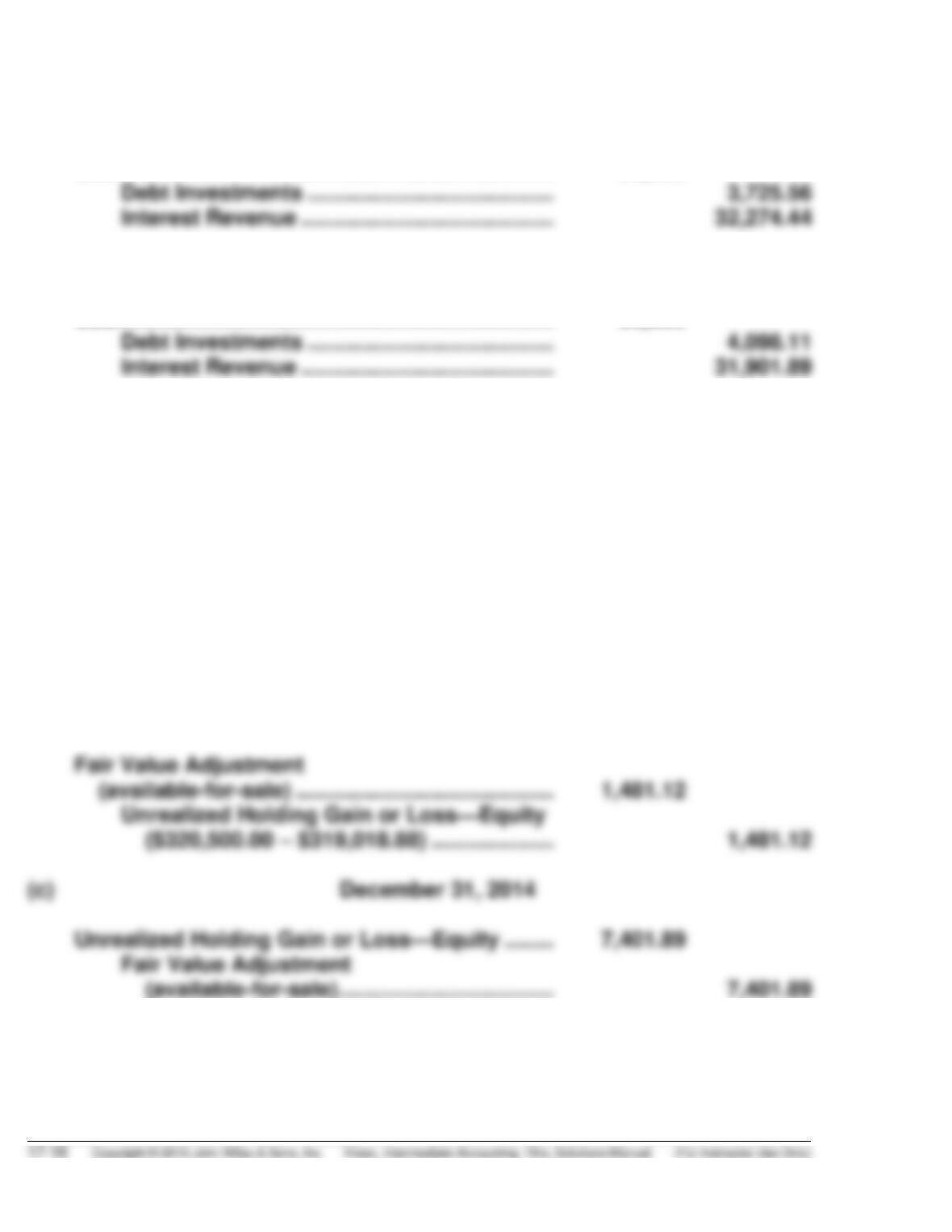

(d) December 31, 2014

Cash …………………………………………………………… 36,000

EXERCISE 17-4 (10–15 minutes)

(a) January 1, 2013

Debt Investments (available-for-sale) ……………. 322,744.44

Cash ……………………………………………………. 322,744.44

(b) December 31, 2013

Cash …………………………………………………………… 36,000

Debt Investments (available-for-sale) …….. 3,725.56

Interest Revenue ($322,744.44 X .10) ……… 32,274.44

EXERCISE 17-4 (Continued)

Amortized

Cost

Fair Value

Unrealized

Gain (Loss)

Available-for-sale bonds

$314,920.77

$309,000.00

$(5,920.77)

EXERCISE 17-5 (20–30 minutes)

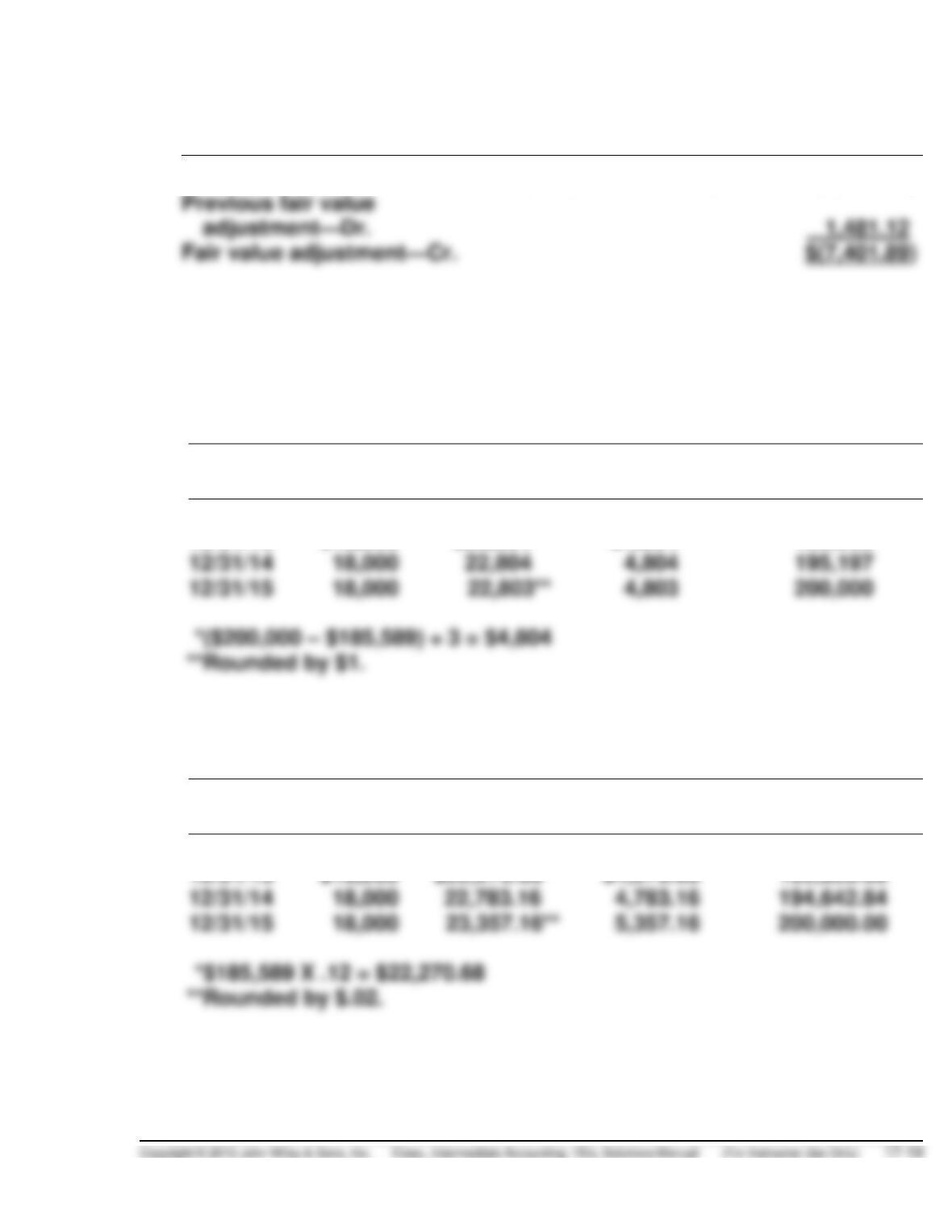

(a) Schedule of Interest Revenue and Bond Discount Amortization

Straight-line Method

9% Bond Purchased to Yield 12%

Date

Cash

Received

Interest

Revenue

Bond Discount

Amortization

Carrying Amount

of Bonds

1/1/13

—

—

—

$185,589

12/31/13

$18,000

$22,804

*$4,804*

190,393

12/31/14

195,197

(b) Schedule of Interest Revenue and Bond Discount Amortization

Effective-Interest Method

9% Bond Purchased to Yield 12%

Date

Cash

Received

Interest

Revenue

Bond Discount

Amortization

Carrying Amount

of Bonds

1/1/13

—

—

—

$185,589.00

12/31/13

$18,000

$22,270.68*

12/31/14

EXERCISE 17-5 (Continued)

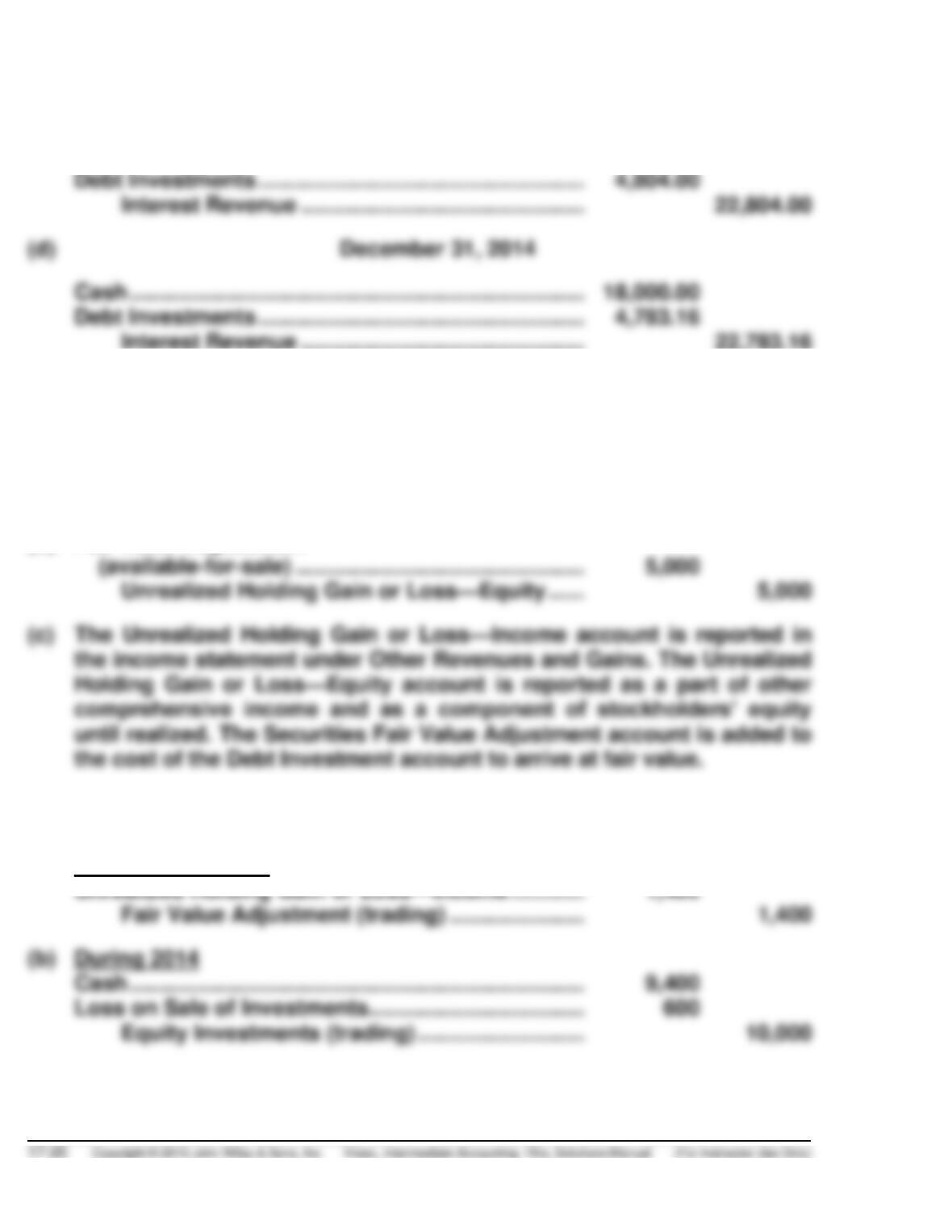

(c) December 31, 2014

Cash ……………………………………………………………….. 18,000.00

EXERCISE 17-6 (10–15 minutes)

(a) Fair Value Adjustment

(trading) ………………………………………………………. 5,000

Unrealized Holding Gain or Loss—Income …. 5,000

(b) Fair Value Adjustment

EXERCISE 17-7 (10–15 minutes)

(a) December 31, 2013