CA 12-2 (Continued)

Developments between the balance sheet date and the date that the financial statements are

released would properly be reflected in notes to the statements as post-balance sheet (or

subsequent events) disclosure.

CA 12-3

(a) Research, as defined in GAAP (FASB ASC 730–10-25), is “planned search or critical investigation

aimed at discovery of new knowledge with the hope that such knowledge will be useful in developing

(b) The current accounting and reporting practices for research and development costs were

promulgated by the Financial Accounting Standards Board (FASB) in order to reduce the number

of alternatives that previously existed and to provide useful financial information about research

and development costs. The FASB considered four alternative methods of accounting: (1) charge

In reaching this decision, the FASB considered the three pervasive principles of expense

recognition: (1) associating cause and effect, (2) systematic and rational allocation, and

(3) immediate recognition. The FASB found little or no evidence of a direct causal relationship

between current research and development expenditures and subsequent future benefits. The

FASB also stated that the high degree of uncertainty surrounding future benefits, if any, of

(c) The following costs attributable only to research and development should be expensed as incurred:

Design and engineering studies.

Prototype manufacturing costs.

Administrative costs related solely to research and development.

The cost of equipment produced solely for development of the product ($315,000).

CA 12-4

(a) Investors and creditors are concerned with corporate profits, dividends, and cash flow. Employees

in Czeslaw Corporation’s R&D department are concerned about job security if the company begins

(b) Ethical issues include long-term versus short-term profits, concern for job security, loyalty to fellow

employees, and an efficient operation.

(c) Reid should do what is best for Czeslaw Corporation in the long run. He should choose to have the

FINANCIAL REPORTING PROBLEM

(a) P&G reports Goodwill of $57,562 million for 2011. P&G also reports

(net of amortization) Trademarks and other intangible assets of

$32,620 million in 2011.

COMPARATIVE ANALYSIS CASE

(a) (1) Coca-Cola reports: Trademarks, Goodwill and Other Intangible

(2) Coca-Cola: Intangible assets are 34.60% of total assets.

PepsiCo: Intangible assets are 45.61% of total assets.

(3) At Coca-Cola, intangible assets increased $2,024M from

$25,645M to $27,669M. At PepsiCo, intangibles increased $4,776M

(2) Coca-Cola had accumulated amortization of $445M and $316M

(3) Coca-Cola identified the composition of its intangible assets as

follows:

Trademarks with indefinite lives $ 6,430M

FINANCIAL STATEMENT ANALYSIS CASE 1

MERCK AND JOHNSON & JOHNSON

(a) The primary intangible assets of a healthcare products company

would probably be patents, goodwill and trademarks. The nature of

each of these is quite different; thus, an investor would normally want

to know what the composition of intangible assets is if it is material.

(b) Many corporate executives complain that investors are too concerned

about the short–term and don’t reward good long-term planning. As a

(c) If a company reports goodwill on its balance sheet, it can only have

resulted from one thing—the company must have purchased another

FINANCIAL STATEMENT ANALYSIS CASE 2

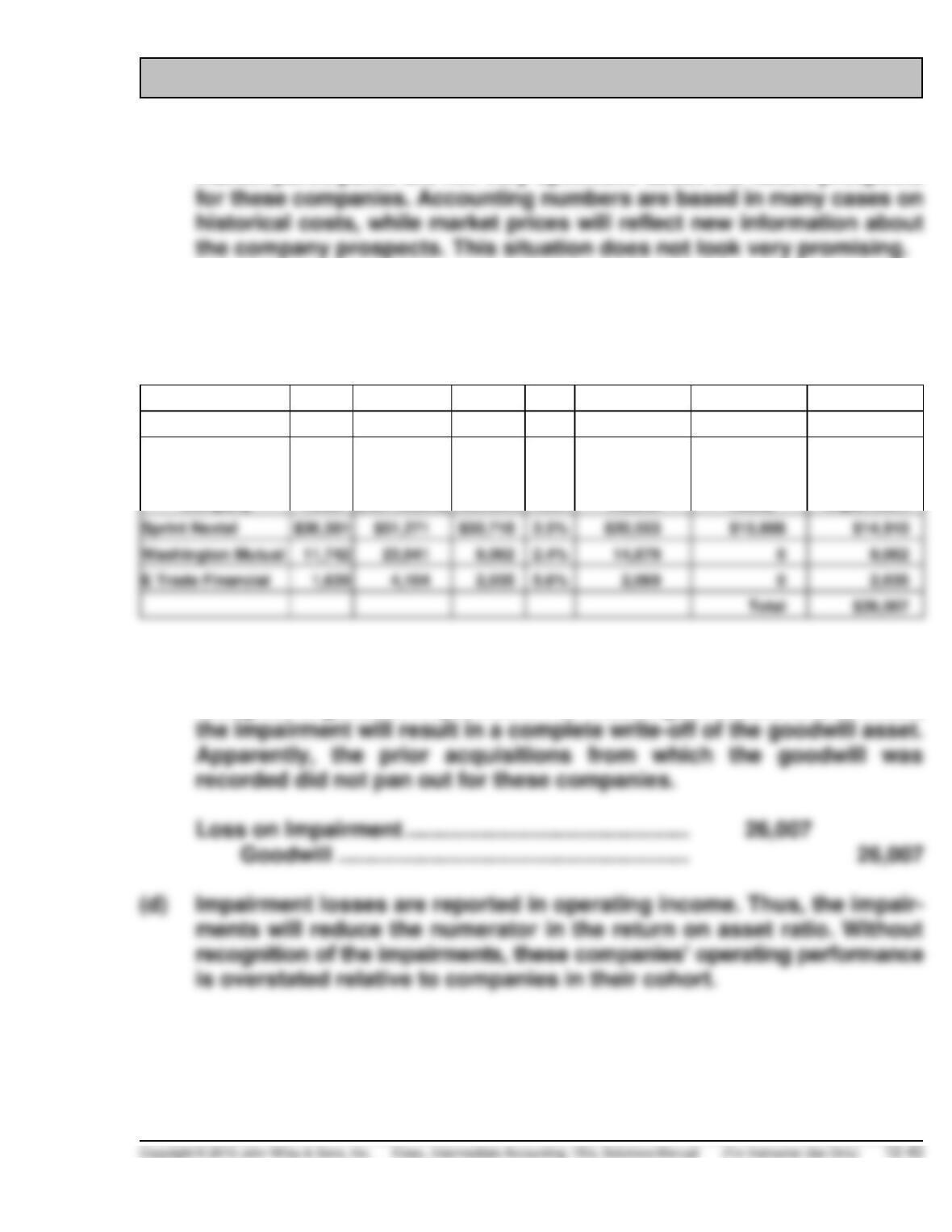

(a) The depressed market values (less than book value) suggest that

market participants are not very optimistic about the future prospects

(b) Because the market (fair) value of each company is less than its book

value of its net assets, it fails the first step in the goodwill impairment

test; an impairment should be recorded.

A

B

C

D

E

F

G

H

(Columns C–D)

(Columns B–F)

(Columns D–G)

Company

Market

Value

Book Value

(Net Assets)

Carrying

Value of

Goodwill

ROA

Estimated Fair

Value of Net

Assets

Implied GW

(NA-Market

Value)

Goodwill

Impairment

Sprint Nextel

$15,808

E Trade Financial

4,104

$26,007

(c) As indicated in the expanded spreadsheet above, unless their market

values increases dramatically, each of these companies is likely to

recognize a goodwill impairment. For Washington Mutual and E-Trade,

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

There is a full year of amortization on the copyright. There is no

amortization for the trade name, which is considered an indefinite-life

intangible.

Amortization expense = $15,000/10 = $1,500

Amortization Expense ……………………………………………..

1,500

Copyrights ……………………………………………………..

1,500

Lost on Impairment …………………………..…………………….

3,500

Trade Names …………………………………………………..

3,500

Analysis

Impairment losses are recorded in operating income. Because impairments

tend to be nonrecurring items, their recognition can make operating income

Principles

The accounting for impairments provides relevant information about

intangible assets by indicating in a timely fashion that intangible assets

PROFESSIONAL RESEARCH

(a) FASB ASC 350-10–05.

(b) Codification String: Assets > 350 Intangibles – Goodwill and other >

10 Overall > 20 Glossary

Goodwill

An asset representing the future economic benefits arising from other

(c) Overall Accounting for Goodwill: Codification String; Assets > 350

Intangibles – Goodwill and other > 20 Goodwill > 35 Subsequent

Measurement.

(d) Codification String: Assets > 350 Intangibles – Goodwill and other >

20 Goodwill > 35 Subsequent Measurement

35–48 All goodwill recognized by a public or nonpublic subsidiary

(subsidiary goodwill) in its separate financial statements that

PROFESSIONAL RESEARCH (Continued)

with impaired goodwill resides must be tested for impairment if

the event that gave rise to the loss at the subsidiary level would

PROFESSIONAL SIMULATION

Journal Entries

January 2, 2014

Patents …………………………………………………….. 80,000

Cash …………………………………………………… 80,000

July 1, 2014

Measurement

Computation of impairment loss:

The book value of $34,125 is greater than net cash flows of $25,000.

Therefore the franchise is impaired. The impairment loss is computed as

follows:

PROFESSIONAL SIMULATION (Continued)

Financial Statements

Intangible assets as of December 31, 2013

Note that the net loss and all organization costs are expensed in 2013.

Intangible assets as of December 31, 2014

IFRS CONCEPTS AND APPLICATION

IFRS12-1

IFRS guidance related to intangible assets is presented in IAS 38, “Intangible

Assets.” IFRS related to impairments is found in IAS 36, “Impairment of

Assets.”

IFRS12-2

Similarities include (1) in GAAP and IFRS, the costs associated with research

and development are segregated into the two components; (2) IFRS and

GAAP are similar for intangibles acquired in a business combination. That

Notable differences are: (1) while costs in the research phase are always

expensed under both IFRS and GAAP, under IFRS costs in the development

phase are capitalized once technological feasibility is achieved; (2) IFRS

permits some capitalization of internally generated intangible assets (e.g.,

brand value), if it is probable there will be a future benefit and the amount

can be reliably measured. GAAP requires expensing of all costs associated

with internally generated intangibles; (3) IFRS requires an impairment test at

IFRS12-3

The IASB and FASB have identified a project, in a very preliminary stage,

which would consider expanded recognition of internally generated

IFRS12-4

Research and Development Expense ……………………….

430,000

Accounts Payable …………………………………………..

505,000

IFRS12-5

(a) Capitalize

(b) Expense

(c) Capitalize

(d) Expense

(e) Expense

IFRS12-6

Loss on Impairment ………………………………………………..

190,000

Patents ($300,000 – $110,000) ………………………….

190,000

IFRS12-7

Patents [$130,000 – ($110,000 – $11,000)] …………………

Recovery of Loss from Impairment…………………..

IFRS12-8

Because the recoverable amount of the division exceeds the carrying

amount of the assets, goodwill is not considered to be impaired. No entry is

necessary.

IFRS12-9

Loss on Impairment ………………………………………………..

50,000

Goodwill ($800,000 – $750,000) ………………………..

IFRS12–10

(a) In accordance with IFRS, the $325,000 is a research and development

(b)

Patents ……………………………………………………….

36,000

Research and Development Expense ……………………….

94,000

Cash ……………………………………………………….

130,000

(to record research and development costs)

Patents ……………………………………………………….

24,000

Cash ……………………………………………………….

Amortization Expense ……………………………………………..

12,000

Patents ($60,000 / 5 years) …………………………..

IFRS12-10 (Continued)

(c)

Patents …………………………………………………………………..

47,200

Cash ………………………………………………………………

Note: The cost of defending the patent is capitalized because the

defense was successful and because it extended the useful life of the

patent.

Amortization Expense ……………………………………………..

11,900

Patents ……………………………………………………….

11,900

(To record one year’s amortization expense:

(d) Additional engineering and consulting costs required to advance the

design of a product to the manufacturing stage are R&D costs. As

IFRS12–11

(a) IFRS 3 addresses goodwill, while IAS 38 addresses intangible assets.

(b) IFRS 3 defines goodwill as “an asset representing the future economic

IFRS12-11 (Continued)

(d) Goodwill recognised in a business combination is an asset represent–

ing the future economic benefits arising from other assets acquired in

a business combination that are not individually identified and

separately recognised. Goodwill does not generate cash flows

independently of other assets or groups of assets, and often

contributes to the cash flows of multiple cash-generating units.

Applying the requirements in paragraph 80 results in goodwill being

tested for impairment at a level that reflects the way an entity

manages its operations and with which the goodwill would naturally

be associated. Therefore, the development of additional reporting

systems is typically not necessary (par. 82).

If the initial allocation of goodwill acquired in a business combination

cannot be completed before the end of the annual period in which the

business combination is effected, that initial allocation shall be

completed before the end of the first annual period beginning after

the acquisition date (par. 84).

IFRS12-11 (Continued)

In accordance with IFRS 3 Business Combinations, if the initial

accounting for a business combination can be determined only

provisionally by the end of the period in which the combination is

effected, the acquirer:

In such circumstances it might also not be possible to complete the

initial allocation of the goodwill recognised in the combination before

IFRS12–12

(a) M&S shows Intangible Assets on the statement of financial position. In

its footnotes, M&S reposts Goodwill, Brands, and Computer Software.