CHAPTER 9

SOLUTIONS TO B EXERCISES

E9-1B (15–20 minutes)

Lower-of–

Part No.

Quantity

Per Unit

Total

Cost

Total

Market

Cost-or–

Market

Cost

Market

10

900

$135

$150.00

$121,500

$135,000

$121,500

11

1,500

90

78.00

135,000

117,000

117,000

13

300

255

270.00

76,500

81,000

76,500

20

600

308

312.00

184,800

187,200

184,800

21

2,400

24

14.00

57,600

480

22

450

360

352.50

162,000

158,625

158,625

E9-2B (10–15 minutes)

Item

Net

Realizable

Value

(Ceiling)

Net

Realizable

Value

Less

Normal

Profit

(Floor)

Replacement

Cost

Designated

Market

Cost

LCM

D

$180*

$140**

$240

$180

$150

$150

I

E9-3B (15–20 minutes)

Item

No.

Cost

per

Unit

Replacement

Cost

Net

Realizable

Value

Net Real.

Value

Less

Normal

Profit

Designated

Market

Value

LCM

Quantity

Final

Inventory

Value

A

$8.10

$8.00

$8.65*

$7.75**

$8.00

$8.00

1,200

$ 9,600

B

6.00

5.60

5.55

5.05

5.55

5.55

600

3,330

C

5.50

5.00

6.60

5.60

5.60

5.50

200

1,100***

D

7.25

7.50

7.50

6.60

7.50

7.25

700

5,075

E

2.10

2.00

2.15

1.95

2.00

2.00

1,000

2,000

F

4.05

4.00

4.60

3.85

4.00

4.00

500

2,000

G

8.75

8.15

8.40

7.90

8.15

8.15

2,000

H

9.95

9.00

9.20

9.20

9.20

300

2,760

E9-4B (10–15 minutes)

(a)

12/31/13

Cost of Goods Sold …………………………..

47,500

Inventory ……………………………………………………….

47,500

12/31/14

Cost of Goods Sold …………………………..

37,500

Inventory ……………………………………………………….

37,500

to Market ……………………………………………………..

47,500

E9-4B (Continued)

12/31/14

Allowance to Reduce Inventory

to Market ……………………………………………………….

10,000*

Recovery of Loss Due to

Market Decline of Inventory …………………………..

10,000

*Cost of inventory at 12/31/13 ………………………………

$ 865,000

Lower-of-cost-or-market at 12/31/13 …………………..

(817,500)

Allowance amount needed to reduce inventory

Cost of inventory at 12/31/14 ……………………………..

$1,025,000

Lower-of-cost-or-market at 12/31/14 …………………..

Allowance amount needed to reduce inventory

Recovery of previously recognized

loss

(c)

Both methods of recording lower-of-cost-or-market adjustments have

the same effect on net income.

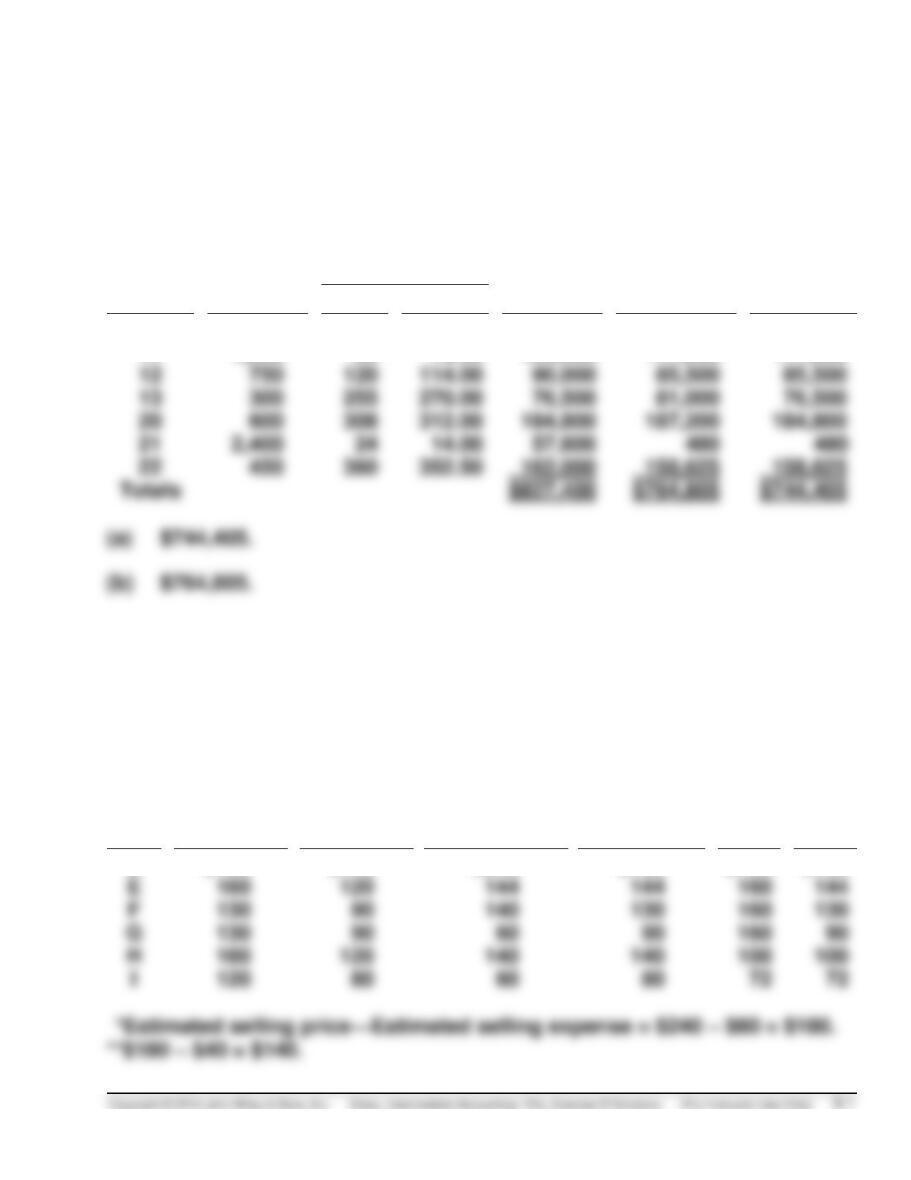

E9-5B (20–25 minutes)

(a)

February

March

April

Sales

$71,000

$76,000

$67,000

Cost of goods sold

Inventory, beginning

21,500

23,000

19,010

Purchases

49,000

43,000

51,000

Cost of goods available

70,500

66,000

70,010

Inventory, ending

23,000

19,010

24,000

Cost of goods sold

47,500

46,990

46,010

Gross profit

23,500

29,010

20,990

fluctuations of inventory*

$22,500

$29,000

$22,600

*

Jan. 31

Feb. 28

Mar. 31

Apr. 30

Inventory at cost

$21,500

$23,000

$19,010

$24,000

Inventory at the lower-of-cost-

or-market

20,000

20,500

16,500

23,100

Allowance amount needed to

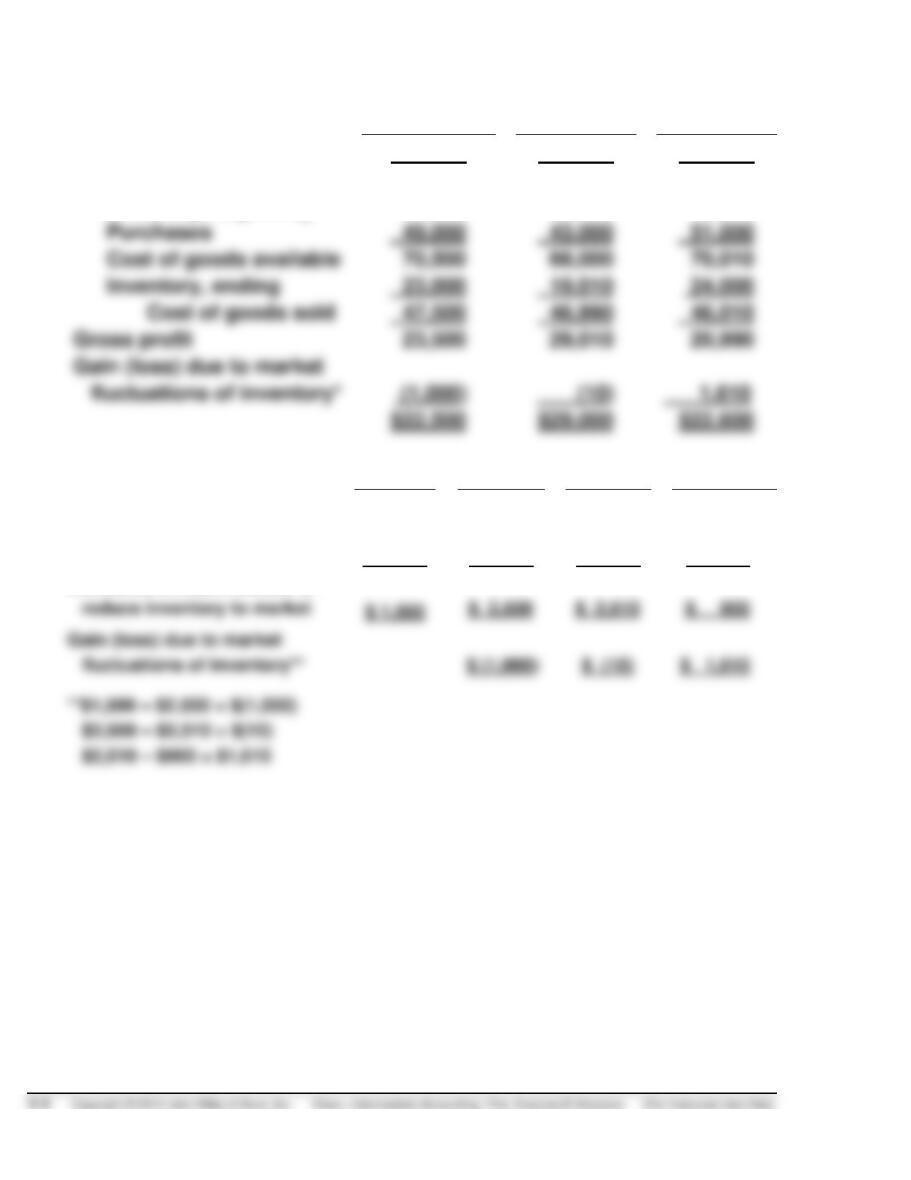

E9-5B (Continued)

(b)

Jan. 31

Loss Due to Market Decline of Inventory …..

1,500

Allowance to Reduce Inventory

to Market ……………………………………..

1,500

Allowance to Reduce Inventory

to Market ……………………………………..

1,000

Allowance to Reduce Inventory

to Market ……………………………………..

Recovery of Loss Due to Market

Decline of Inventory ……………………..

1,610

E9–6B (15-20 minutes)

Net realizable value (ceiling)

$56 – $18 = $38

Net realizable value less normal profit (floor)

$38 – $ 4 = $34

Replacement cost

$40

Designated market

$38

Ceiling

Cost

$48

$38

9-6 Copyright © 2014 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Exercise B Solutions (For Instructor Use Only)

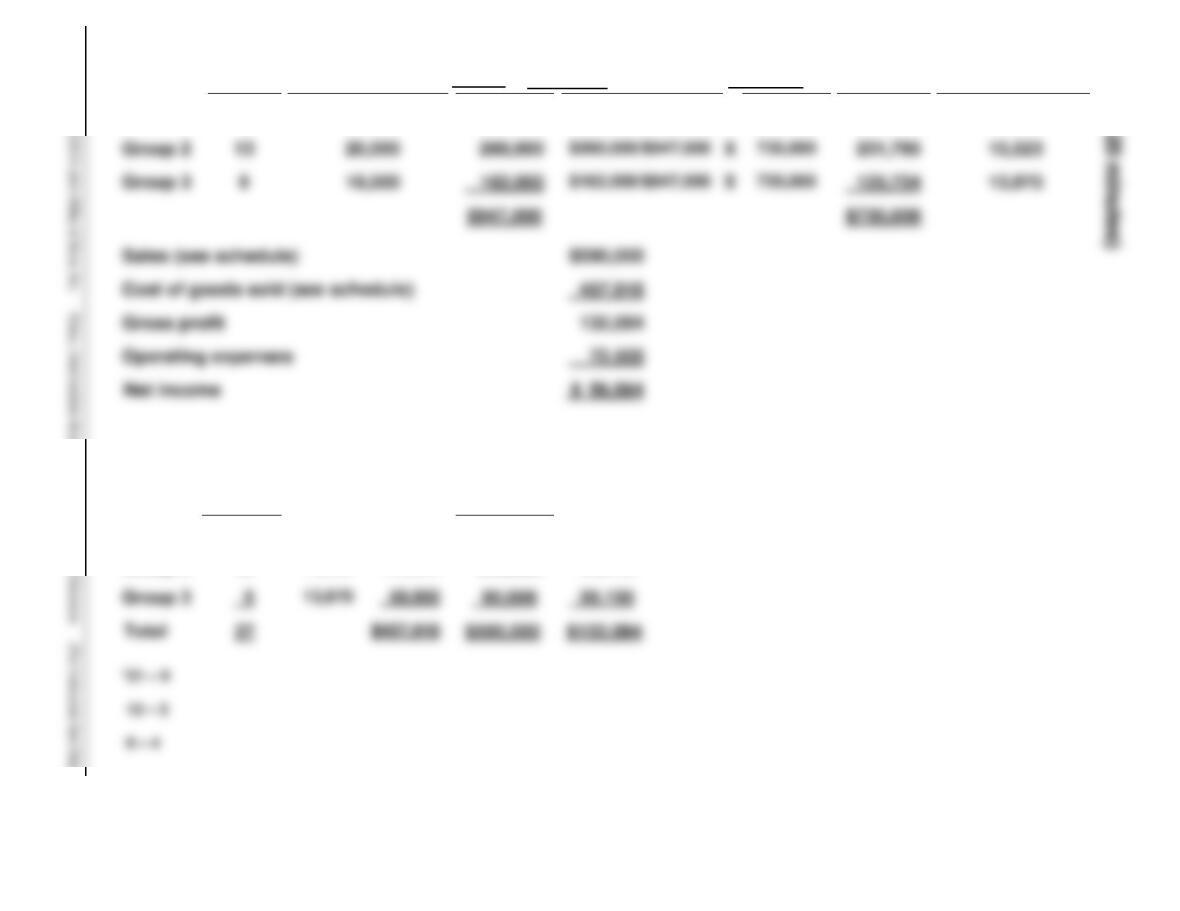

E9-7B (15–20 minutes)

Cost Per Lot

(Cost Allocated/

No. of Lots)

$19,403

$457,916

Group 3

Cost

Allocate

d to Lots

$407,471

Total

Cost

$735,000

X

Relative Sales

Price

$525,000/$947,000

Gross

Profit

$ 67,164

44,770

Total

Sales

Price

$ 525,000

Sales

$300,000

200,000

Sales

Price Per Lot

$25,000

Cost Cost of

Per Lots

Lot Sold

$19,403 $232,836

15,523 155,230

No. of

Lots

21

Number

of Lots

Sold*

12

10

Group 1

Group 1

Group 2

$590,000

132,084

Sales (see schedule)

Gross profit

Operating expenses

Group 3

E9-8B (12–17 minutes)

Total estimated selling price:

Lounge chairs, 80 X $45 ………………………………………….

$3,600

Armchairs, 60 X $40 ………………………………………………..

Straight chairs, 140 X $25 ……………………………………….

$9,500

Sales during 2014:

40 X $45 …………………………………………………………………

$1,800

20 X $40 …………………………………………………………………

24 X $25 …………………………………………………………………

600

Ratio of cost to selling price, $5,985 ÷ $9,500……………………

63%

Gross profit realized in 2014, (100% – 63%) X $3,200 ………..

$1,184

Inventory on December 31, 2014, $5,985 – ($3,200 X 63%) …

$3,969

E9-9B (5 minutes)

Commitments) ………………………………………………………

Estimated Liability on Purchase

Commitments ……………………………………………….

15,000

Unrealized Holding Loss—Income (Purchase

E9-10B (15–20 minutes)

(a) If the commitment is material in amount, there should be a footnote in

the balance sheet stating the nature and extent of the commitment. The

(b) The drop in the market price of the commitment should be charged to

operations in the current year if it is material in amount. The following

entry would be made:

(c) Assuming the $15,000 market decline entry was made on December 31,

2014, as indicated in (b), the entry when the materials are received in

January 2015 would be:

E9-11B (8–13 minutes)

1.

25%

= 33.33% OR 33 1/3%.

100% – 25%

= 25%.

100% – 20%

E9-12B (10–15 minutes)

(a)

Inventory, May 1 (at cost) ……………………………..

$ 40,000

Purchases (gross) (at cost) ………………………….

160,000

Purchase discounts …………………………………….

(3,000)

7,500

Goods available (at cost) ……………………..

Sales (at selling price) ………………………………….

Sales returns (at selling price)………………………

Net sales (at selling price) …………………………...

Less: Gross profit (25% of $232,500) …………….

Sales (at cost) …………………………………….

174,375

Approximate inventory, May 31

E9-12B (Continued)

(b) Gross profit as a percent of sales must be computed:

Inventory, May 1 (at cost) ………………………………………..

$ 40,000

Purchases (gross) (at cost) ……………………………………..

160,000

Purchase discounts ………………………………………………..

7,500

Goods available (at cost) …………………………..

Sales (at selling price) …………………………..………………..

$250,000

Sales returns (at selling price) …………………………..

(17,500)

Net sales (at selling price) ……………………………………….

Sales (at cost) = Sales/(1 + .25) ………………………..

186,000

Approximate inventory, May 31

E9-13B (15–20 minutes)

(a)

Merchandise on hand, January 1 …………………………..

$ 76,000

Purchases ………………………………………………………

$144,000

Less: Purchase returns and allowances …………..

(4,800)

Net purchases ………………………………………………..

Freight-in ……………………………………………………….

6,800

Total merchandise available for sale ………………………..

Cost of goods sold* ………………………………………………..

Ending inventory …………………………………………….

Less: Undamaged goods …………………………..

(21,800)

(b)

Cost of goods sold = 75% of sales of

$200,000 = $150,000

E9-14B (10–15 minutes)

Beginning inventory …………………………………………..

$ 210,000

Purchases …………………………………………………………

805,000

1,015,000

Purchase returns ……………………………………………….

Goods available (at cost) ……………………………………

Sales …………………………………………………………………

Sales returns ……………………………………………………..

Net sales ……………………………………………………………

Less: Gross profit (20% X $899,000) …………………..

E9-15B (10–15 minutes)

Beginning inventory (at cost) ……………………………..

$ 78,000

Purchases (at cost) …………………………………………….

112,000

Goods available (at cost) …………………………...

190,000

Sales (at selling price) ………………………………………..

Less sales returns ……………………………………………..

Net sales ……………………………………………………………

Less: Gross profit* (16.67% of $88,000) ………………

Net sales (at cost) ………………………………………

Estimated inventory (at cost) ………………………………

116,670