EXERCISE 19-22 (Continued)

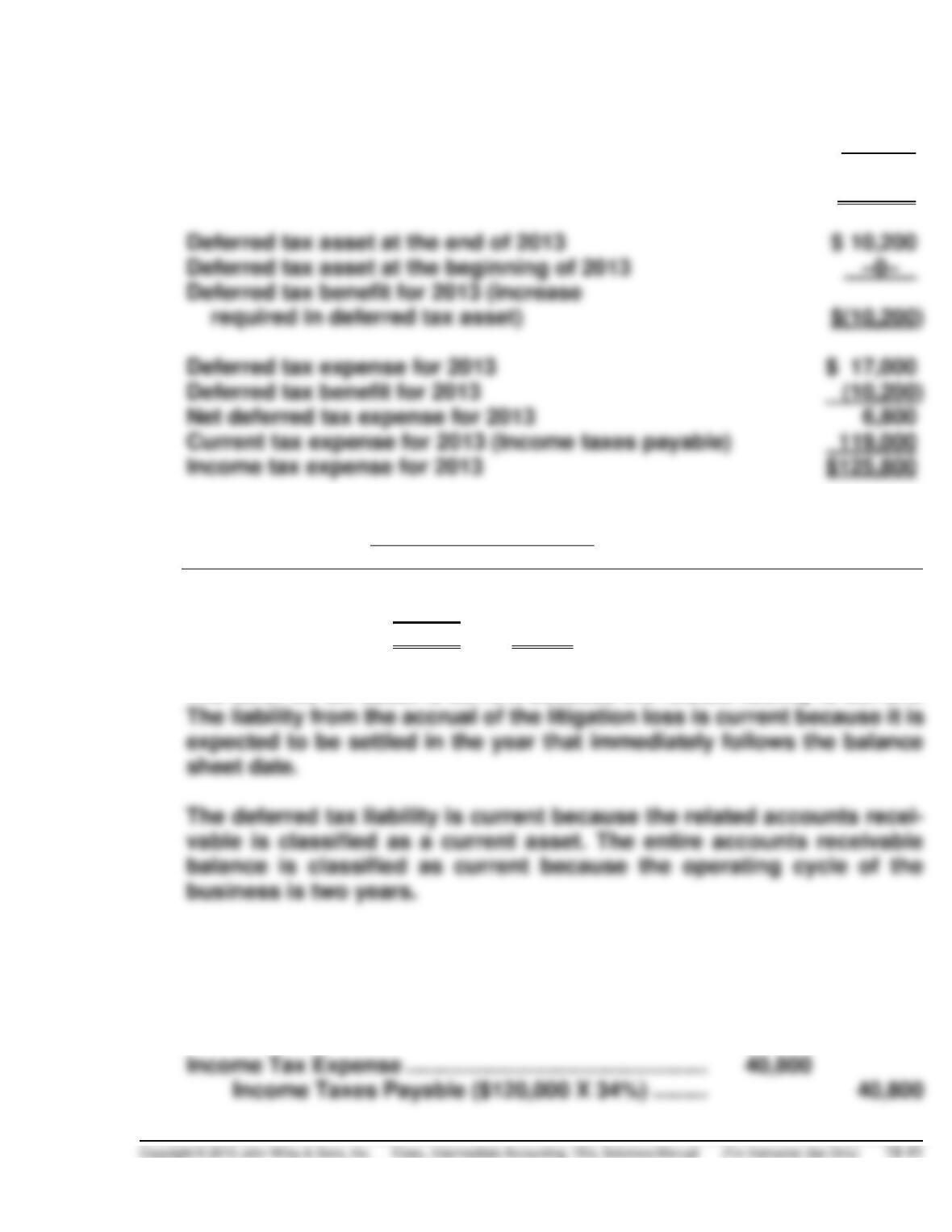

Deferred tax liability at the end of 2013 $17,000

Deferred tax liability at the beginning of 2013 –0–

Deferred tax expense for 2013 (increase

required in deferred tax liability) $17,000

(b)

Temporary

Difference

Resulting Deferred Tax

Related Balance

Sheet Account

Classification

(Asset)

Liability

Accounts receivable

$17,000

Accounts Receivable

Current

Litigation liability

$(10,200)

____

Lawsuit Obligation

Current

Totals

$(10,200)

$17,000

The deferred tax asset is current because the related liability is current.

EXERCISE 19-23 (30–35 minutes)

(a) 2012

EXERCISE 19-23 (Continued)

2013

Income Tax Expense ………………………………………. 30,600

Income Taxes Payable ($90,000 X 34%) ……… 30,600

2014

Income Tax Refund Receivable ………………………. 71,400

2015

Income Tax Expense ……………………………………… 83,600

Income Taxes Payable …………………………….. 57,000*

Deferred Tax Asset ………………………………….. 26,600

*[($220,000 – $70,000) X 38%]

(c) 2014

Income Tax Refund Receivable ………………………. 71,400

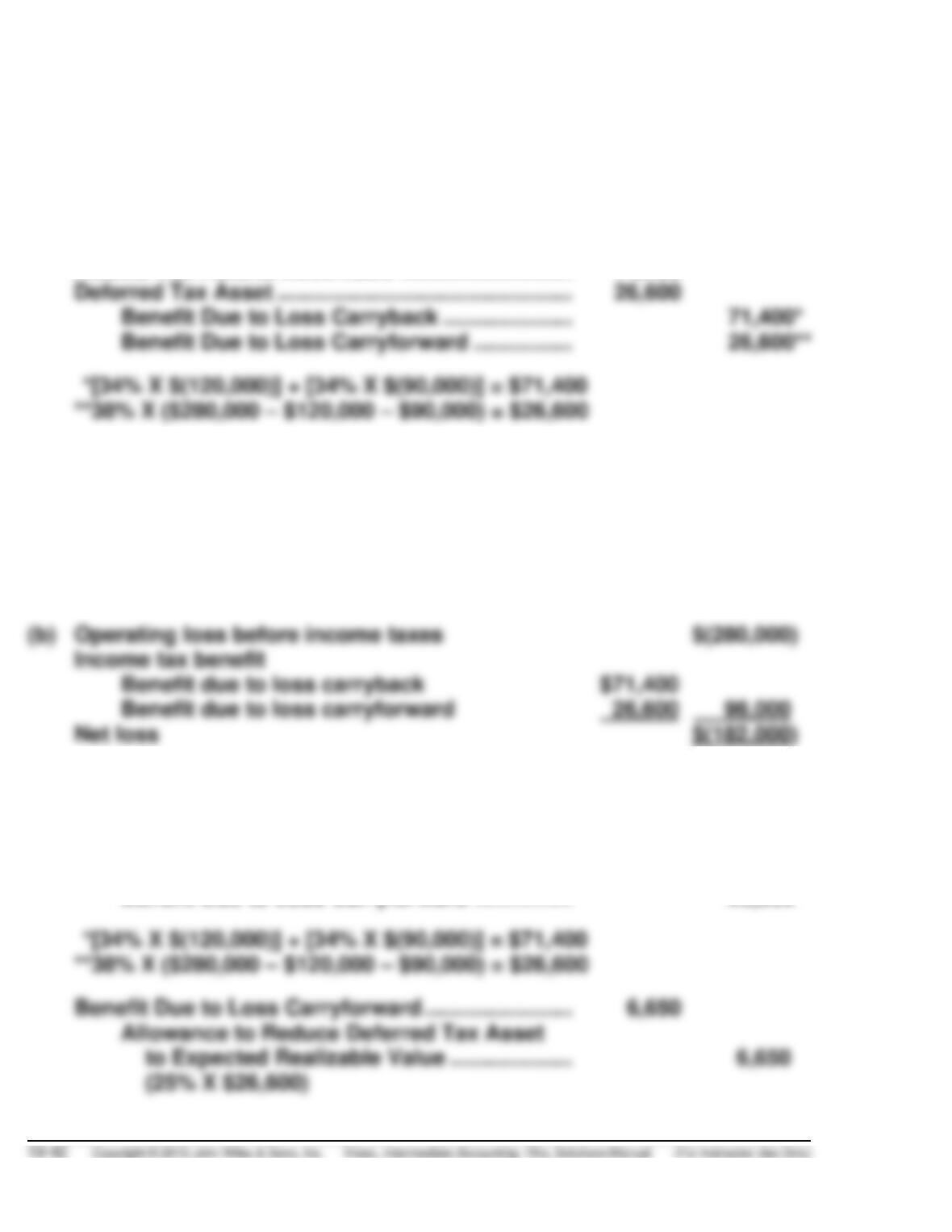

Deferred Tax Asset ………………………………………… 26,600

Benefit Due to Loss Carryback ………………… 71,400*

Benefit Due to Loss Carryforward ……………. 26,600**

EXERCISE 19-23 (Continued)

2015

Income Tax Expense …………………………………………. 83,600

(d) Operating loss before income taxes $(280,000)

Income tax benefit

Benefit due to loss carryback $71,400

Benefit due to loss carryforward ($26,600 – $6,650) 19,950 91,350

Net loss $(188,650)

Note: Using the assumption in part (c), the income tax section of the

2015 income statement would appear as follows:

EXERCISE 19-24 (30–35 minutes)

(a) 2012

Income Tax Expense ……………………………………… 48,000

Income Taxes Payable ($120,000 X 40%) ……. 48,000

2013

Benefit Due to Loss Carryforward …………………… 15,750

Allowance to Reduce Deferred Tax Asset

to Expected Realizable Value …………………. 15,750

(50% X $31,500)

2015

(b) Operating loss before income taxes $(280,000)

Income tax benefit

EXERCISE 19-24 (Continued)

(c) Income before income taxes $120,000

EXERCISE 19-25 (15–20 minutes)

(a) 2014

Income Tax Expense ($120,000 X .40) …………….. 48,000

Income Taxes Payable ……………………………. 48,000

2015

2016

Income Tax Expense …………………………………….. 72,000

Income Taxes Payable ……………………………. 32,000

EXERCISE 19-25 (Continued)

(b) Loss before income taxes $(570,000)

Income tax benefit

TIME AND PURPOSE OF PROBLEMS

Problem 19-1 (Time 40–45 minutes)

Purpose—to provide the student with an understanding of how to compute and properly classify

Problem 19-2 (Time 50–60 minutes)

Purpose—to provide the student with a situation where: (1) a temporary difference originates over a

Problem 19-3 (Time 40–45 minutes)

Purpose—to provide the student with an understanding of how future temporary differences for existing

depreciable assets are considered in determining the future years in which existing temporary

Problem 19-4 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of permanent and temporary differences when

there are multiple differences and a single rate.

Problem 19-5 (Time 20–25 minutes)

Purpose—to provide the student with a situation involving a net operating loss which can be partially

Problem 19-6 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of how the computation and classification of

deferred income taxes are affected by the individual future year(s) in which future taxable and

deductible amounts are scheduled to occur because of existing temporary differences. Two situations

are given and the student is required to compute and classify the deferred income taxes for each. A net

deferred tax asset results in both cases.

Problem 19-7 (Time 45–50 minutes)

Purpose—to provide the student with a situation where: (1) a temporary difference originates in one

Time and Purpose of Problems (Continued)

Problem 19-8 (Time 40–50 minutes)

Purpose—to test a student’s understanding of the relationships that exist in the subject area of

Problem 19-9 (Time 40–50 minutes)

Purpose—to test a student’s ability to compute and classify deferred taxes for three temporary

differences and to draft the income tax expense section of the income statement for the year.

SOLUTIONS TO PROBLEMS

PROBLEM 19-1

(a) X(.40) = $320,000 taxes due for 2014

X = $320,000 ÷ .40

X = $800,000 taxable income for 2014

(b) Taxable income [from part (a)]………………………….. $800,000

Pretax financial income for 2014 ………………… $890,000

(c) 2014

Income Tax Expense

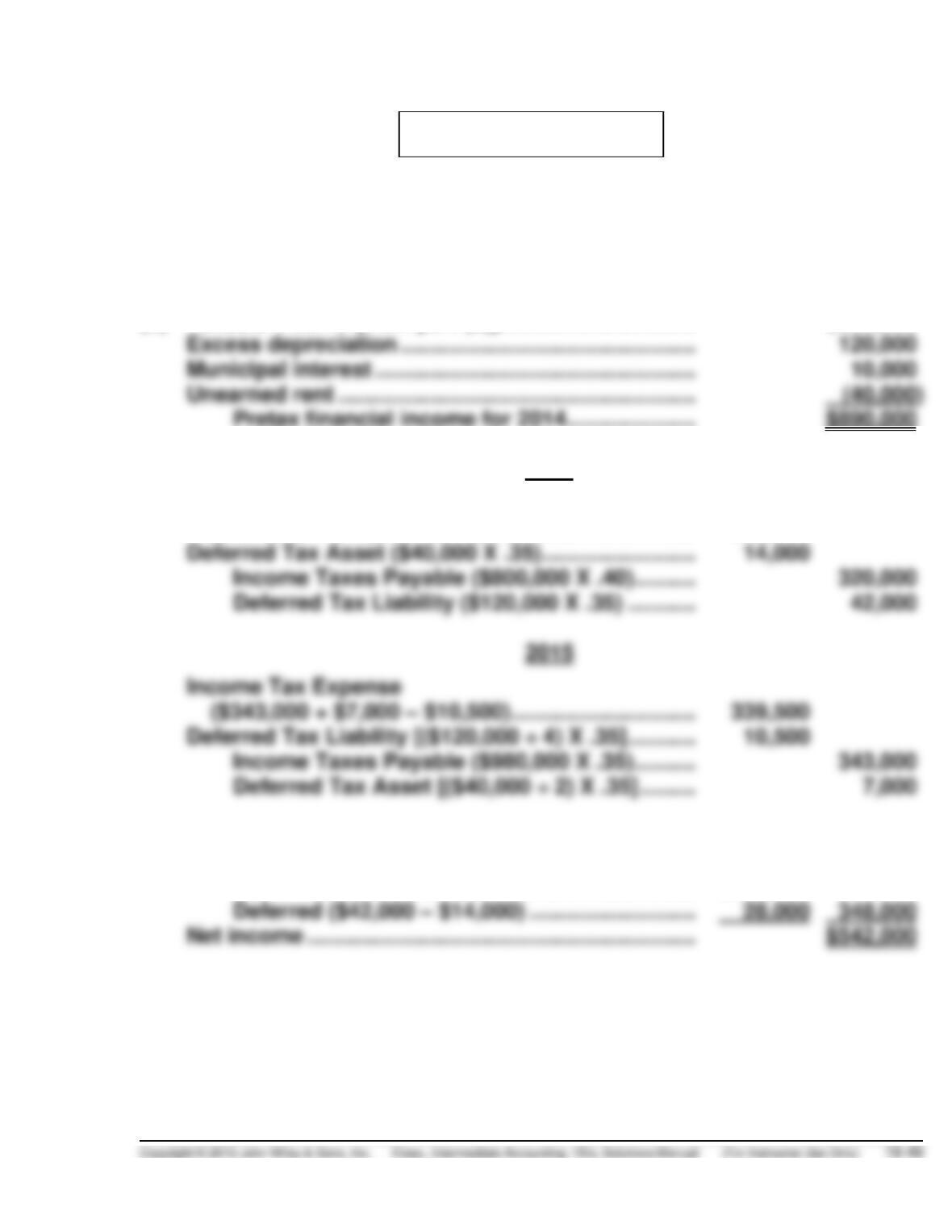

($320,000 + $42,000 – $14,000) ………………………. 348,000

(d) Income before income taxes …………………………….. $890,000

Income tax expense

Current …………………………………………………….. $320,000

PROBLEM 19-2

(a) Before deferred taxes can be computed, the amount of temporary

difference originating (reversing) each period and the resulting cumula-

tive temporary difference at each year-end must be computed:

2014

2015

2016

2017

Pretax financial income

$290,000

$320,000

$350,000

($(420,000

320,000

350,000

Cumulative Temporary

Difference At End of Year

2014

$140,000

2015

$265,000

($140,000 + $125,000)

2016

$385,000

($265,000 + $120,000)

Because the temporary difference causes pretax financial income to

exceed taxable income in the period it originates, the temporary

difference will cause future taxable amounts.

PROBLEM 19-2 (Continued)

The deferred taxes at the end of 2014 would be computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

$140,000

35%

$49,000

Deferred tax liability at the end of 2014 …………………………. $ 49,000

2015

Income Tax Expense ……………………………………….. 7,000*

Deferred Tax Liability ………………………………… 7,000

*The adjustment due to the change in the tax rate is computed as

follows:

Cumulative temporary difference at the end

of 2014 ……………………………………………………………………. $140,000

Newly enacted tax rate for future years ………………………… 40%

PROBLEM 19-2 (Continued)

Taxable income for 2015 ………………………………………………. $225,000

The deferred taxes at December 31, 2015, are computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

$265,000

40%

$106,000

Deferred tax liability at the end of 2015 ………………………….. $106,000

2016

Income Tax Expense ……………………………………… 152,000

Income Taxes Payable …………………………….. 104,000

Deferred Tax Liability ………………………………. 48,000

The deferred taxes at December 31, 2016, are computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

$385,000

40%

$154,000

PROBLEM 19-2 (Continued)

2017

Income Tax Expense …………………………………….. 180,000

Deferred Tax Liability ……………………………………. 44,000

The deferred taxes at December 31, 2017, are computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

$275,000

40%

$110,000

(b) 2015

Income before income taxes …………………………. $320,000

Income tax expense

Current …………………………………………………… $90,000

PROBLEM 19-3

Book Depreciation

Tax Depreciation

Difference

2014

$ 150,000

$ 120,000*

($ 30,000

2015

150,000

240,000

(90,000)

2016

150,000

240,000

(90,000)

2017

150,000

240,000

(90,000)

2018

150,000

240,000

(90,000)

2019

150,000

120,000*

30,000

2020

150,000

2021

150,000

(a) Pretax financial income for 2015 ……………………. $1,400,000

Nontaxable interest ……………………………………….. (60,000)

(b) Income Tax Expense …………………………………….. 469,000

Income Taxes Payable ……………………………. 437,500

PROBLEM 19-3 (Continued)

Scheduling—End of 2015

Future Years

2016

2017

2018

Enacted tax rate

Deferred tax (asset) liability

Future taxable (deductible)

Future Years

2019

2020

2021

Total

Enacted tax rate

Deferred tax (asset) liability

Future taxable (deductible)

The net deferred tax liability at December 31, 2015, is $21,000.

Scheduling—End of 2014

Future Years

2015

2016

2017

2018

Enacted tax rate

Deferred tax (asset) liability

Future taxable (deductible)

Future Years

2019

2020

2021

Total

Enacted tax rate

Deferred tax (asset) liability

Future taxable (deductible)

PROBLEM 19-3 (Continued)

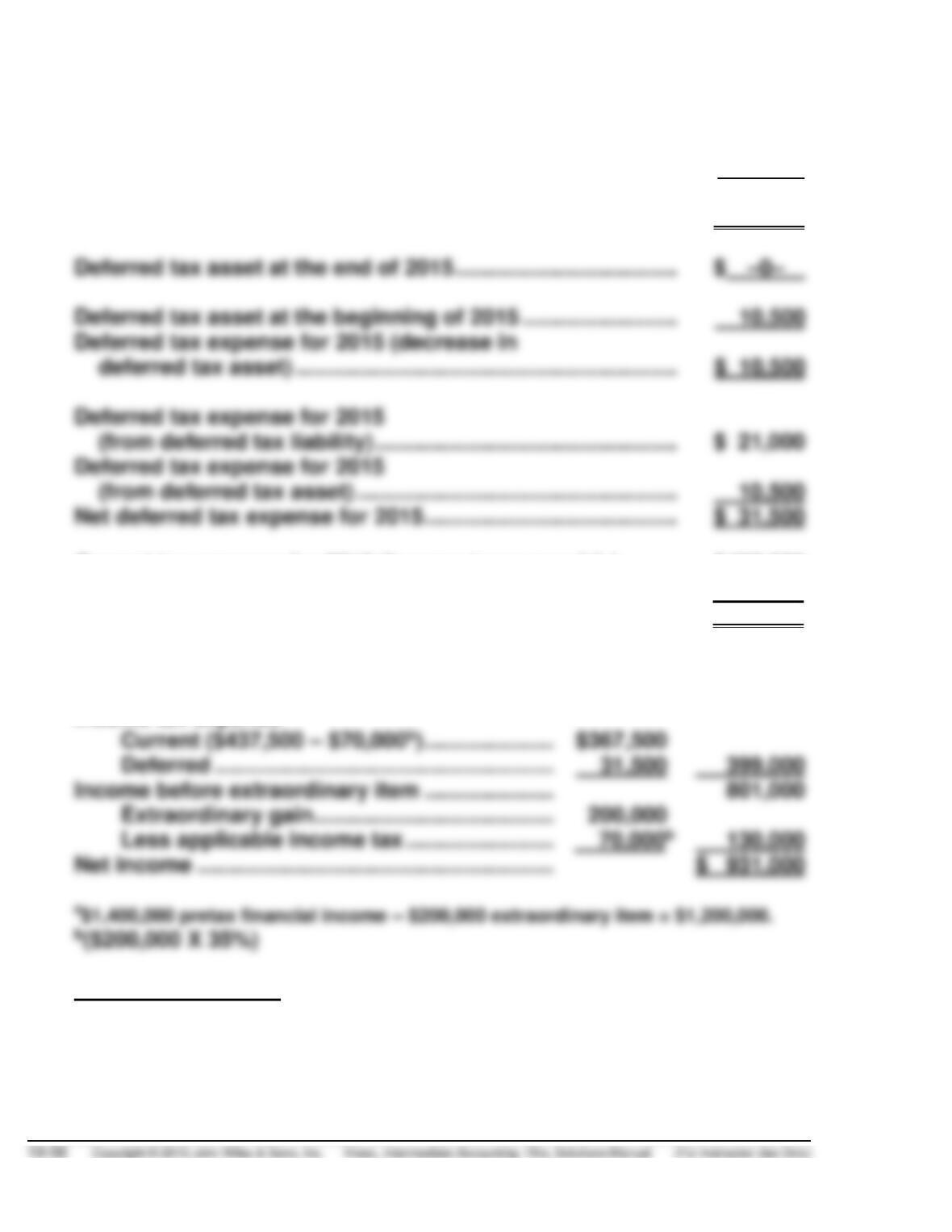

The net deferred tax asset at December 31, 2014, is $10,500.

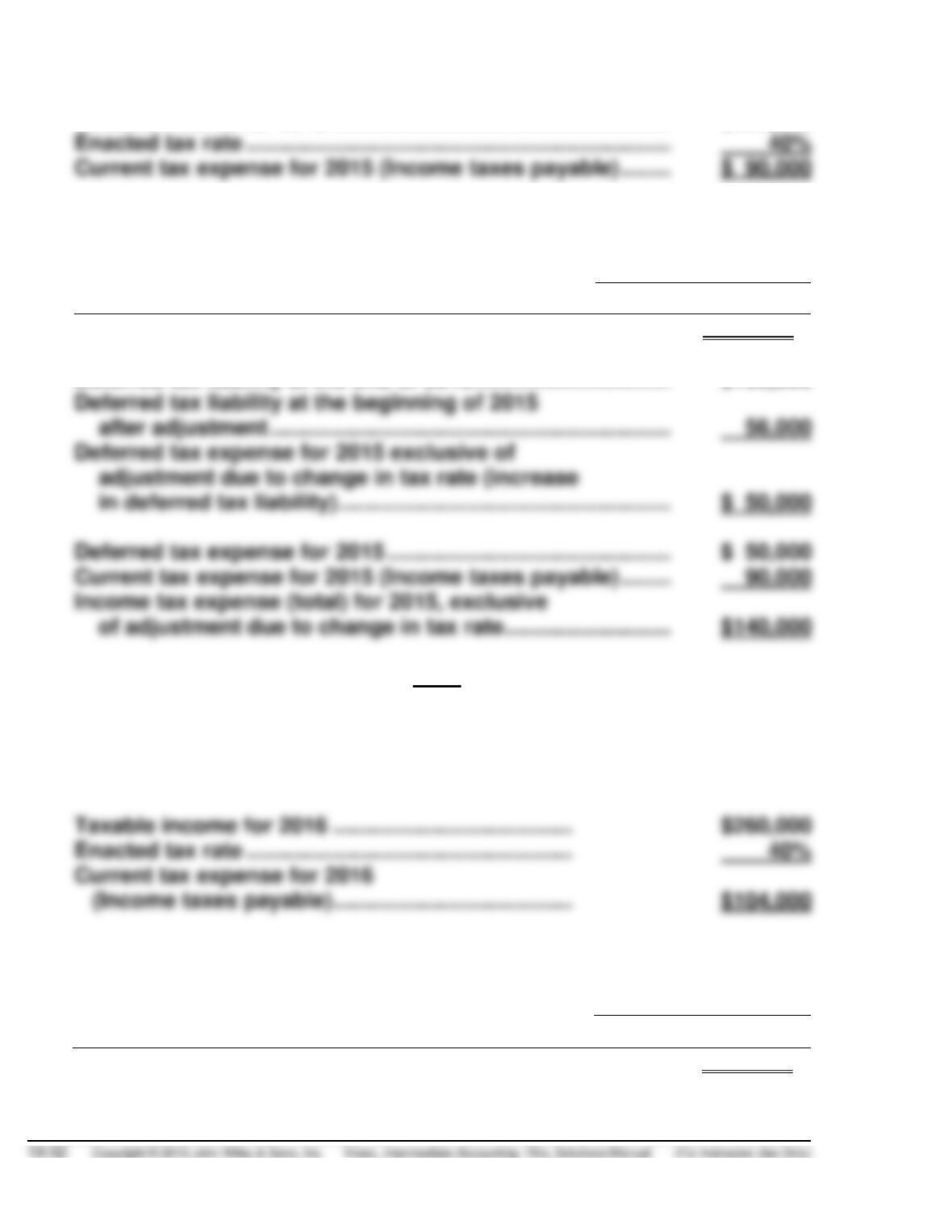

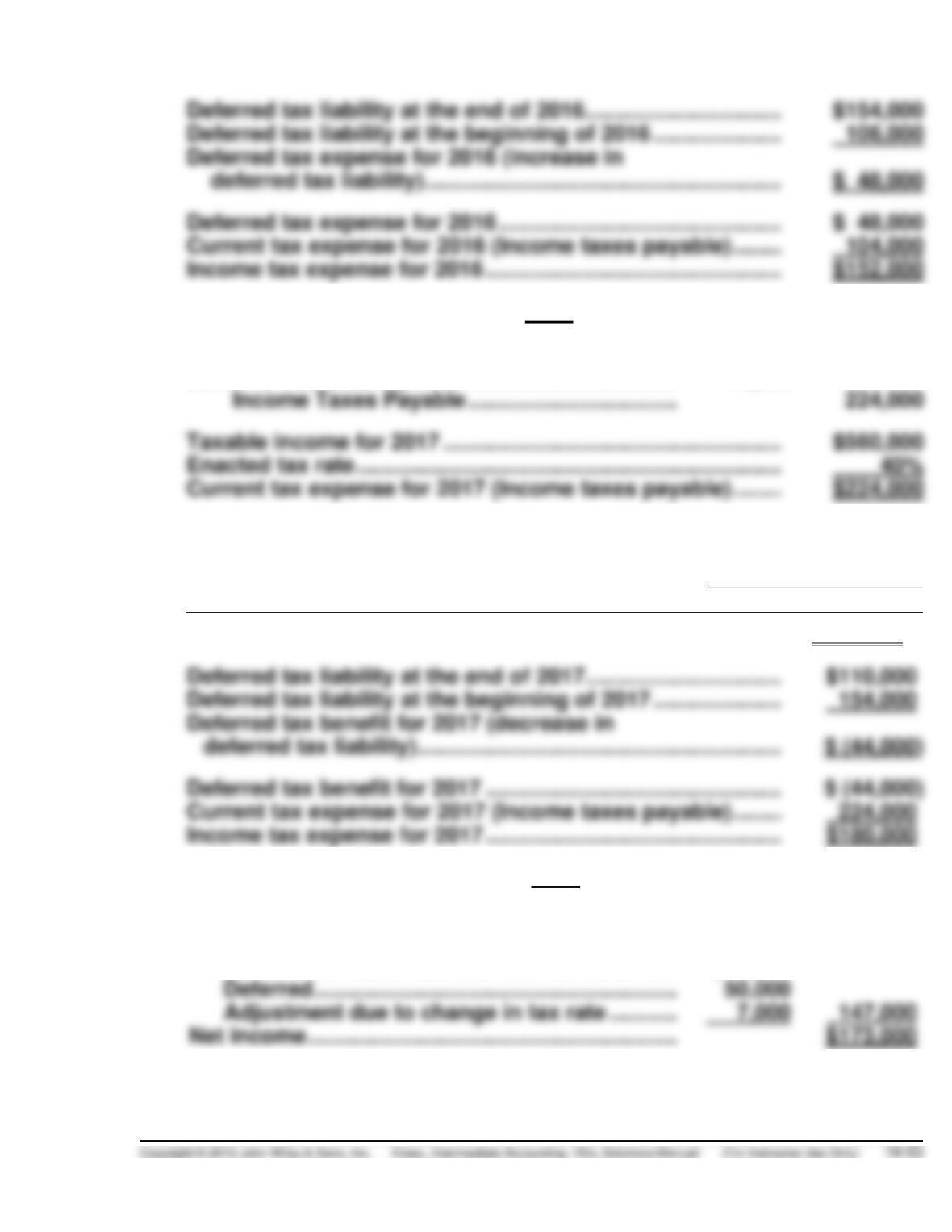

Deferred tax liability at the end of 2015 …………………………... $ 21,000

Deferred tax liability at the beginning of 2015 …………………. –0–

Deferred tax expense for 2015 (increase in

deferred tax liability) ………………………………………………….. $ 21,000

Current tax expense for 2015 (Income taxes payable) ……… $437,500

Deferred tax expense for 2015 ……………………………………….. 31,500

Income tax expense for 2015 …………………………………………. $469,000

(c) Income before income taxes and

extraordinary item ……………………………………. $1,200,000a

Income tax expense

(d) Long-term liabilities

Deferred tax liability …………………………………….. $21,000

PROBLEM 19-4

(a) Schedule of Pretax Financial Income

and Taxable Income for 2014

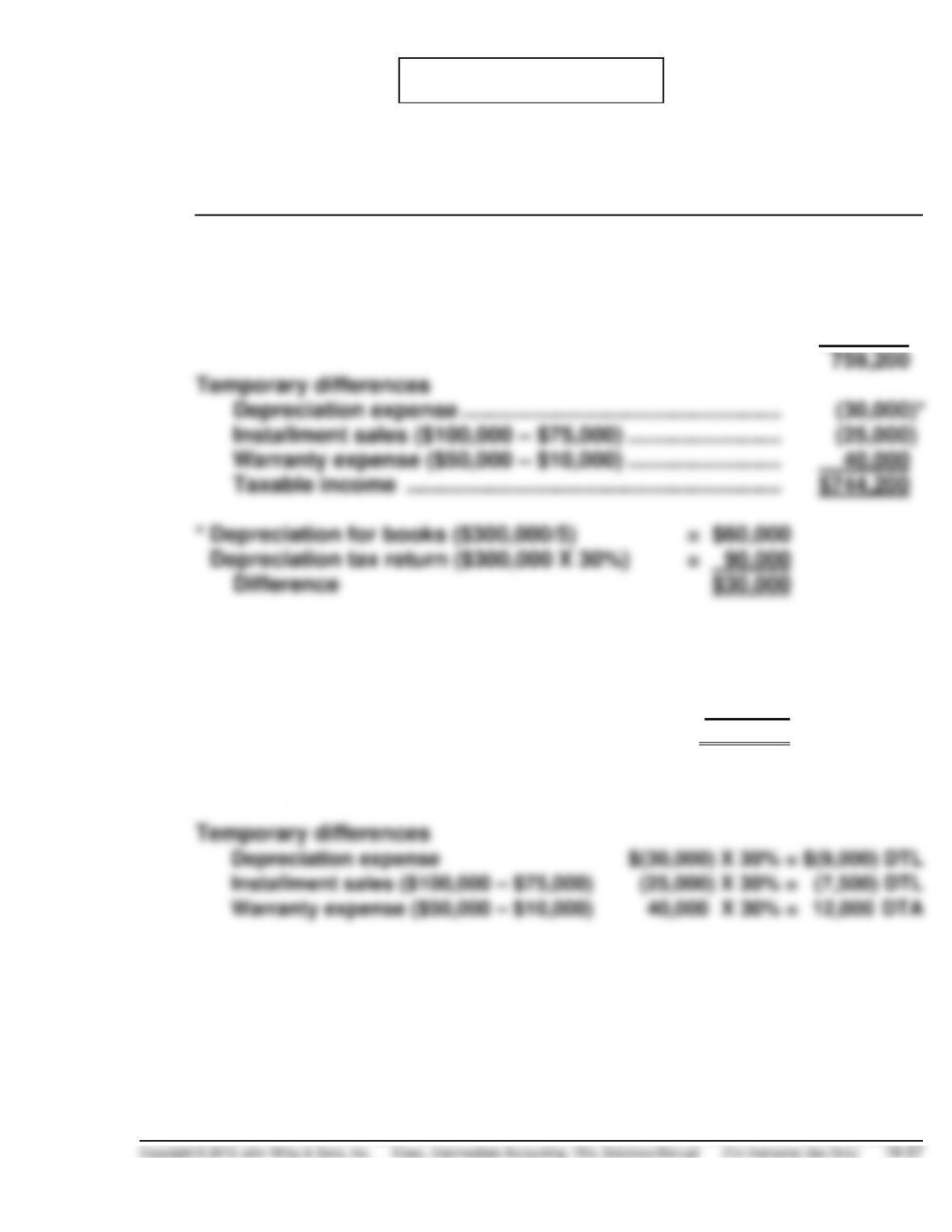

Pretax financial income ………………………………………………. $750,000

Permanent differences

Insurance expense …………………………..……………………. 9,000

Bond interest revenue …………………………………………… (4,000)

Pollution fines ………………………………………………………. 4,200

The income taxes payable for 2014 is as follows:

Taxable income ………………………………… $744,200

Tax rate ……………………………………………. 30%

Income taxes payable ……………………….. $223,260

The computation of the deferred income taxes for 2014 is as follows:

PROBLEM 19-4 (Continued)

(b) The journal entry to record income taxes payable, income tax expense

and deferred income taxes is as follows:

Income Tax Expense …………………………..…………. 227,760*

PROBLEM 19-5

(a) 2014

Income Tax Refund Receivable

[($50,000 X 30%) + ($80,000 X 40%)] ………………… 47,000

Benefit Due to Loss Carryback ……………………. 47,000

2016

Income Tax Expense …………………………………………. 35,000

Income Taxes Payable ($100,000 X 35%) ……… 35,000

(b) The income tax refund receivable account totaling $47,000 will be

reported under current assets on the balance sheet at December 31, 2014.

This type of receivable is usually listed immediately above inventory in

PROBLEM 19-5 (Continued)

(c) 2014 Income Statement

Operating loss before income taxes …………… $(180,000)

(d) 2015 Income Statement

Income before income taxes ………………………. $70,000

Income tax expense

Current ………………………………………………. $ 8,000a

Deferred …………………………………………….. 20,000 28,000

Net income …………………………..…………………… $42,000