EXERCISE 22-8 (5–10 minutes)

1. a. 6. a.

EXERCISE 22-9 (15–20 minutes)

December 31, 2015

Retained Earnings ($550,000 X 9/55) ………………………. 90,000

Accumulated Depreciation—Equipment …………… 90,000

(To correct for the omission of depreciation

expense in 2013)

EXERCISE 22-10 (20–25 minutes)

(a) Computation of depreciation for 2015:

Cost of building $800,000

Less: Depreciation prior to 2015

(b) Computation of 2015 depreciation expense on the equipment:

Cost of equipment $100,000

EXERCISE 22-11 (10–15 minutes)

(a) No entry necessary. Changes in estimates are treated prospectively.

(b) Depreciation Expense ………………………………………. 19,375*

Accumulated Depreciation—Equipment ……… 19,375

EXERCISE 22-12 (20–25 minutes)

(a) Cost of plant assets $1,600,000

Less: Depreciation prior to 2015

2012 ($1,600,000 X .25) $400,000

2015

2014

(b) Income before depreciation expense

$300,000

$270,000

Depreciation expense

115,000

225,000

Net income

$185,000

$ 45,000

EXERCISE 22-13 (10–15 minutes)

(a) The net income to be reported in 2015, using the retrospective approach,

would be computed as follows:

EXERCISE 22-14 (20–35 minutes)

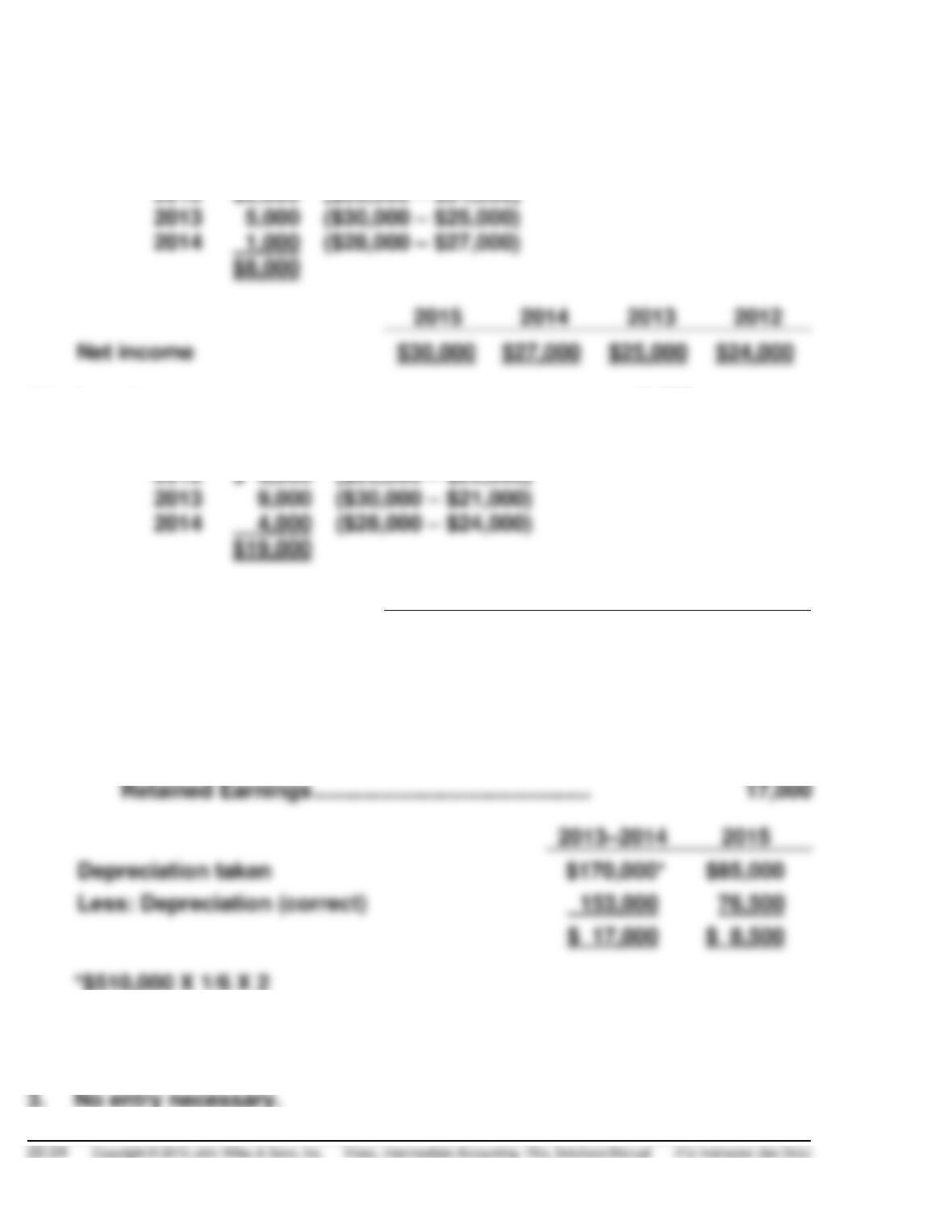

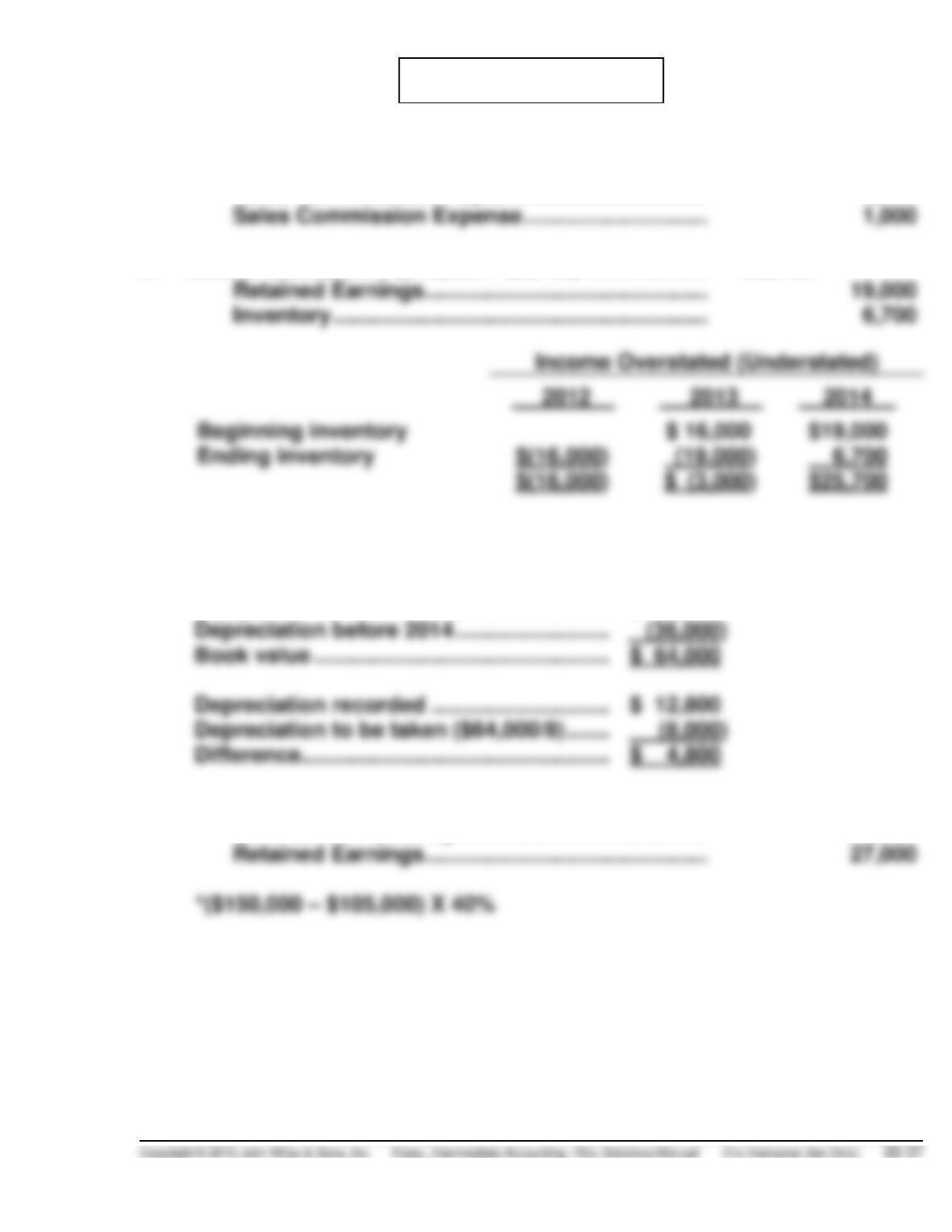

(a) Retained Earnings ……………………………………………. 8,000

Inventory …………………………..………………………. 8,000*

Net income

($30,000

$27,000

$25,000

$24,000

(b) Inventory …………………………………………………………. 19,000

Retained Earnings ……………………………………… 19,000*

2015

2014

2013

2012

Net income

($34,000

$28,000

$30,000

$26,000

EXERCISE 22-15 (15–20 minutes)

1. Accumulated Depreciation—Equipment …………….. 25,500

Depreciation Expense ………………………………… 8,500

2. Retained Earnings ……………………………………………. 45,000

Salaries and Wages Expense ……………………… 45,000

EXERCISE 22-15 (Continued)

4. Amortization Expense …………………………………….. 2,250

Retained Earnings ………………………………………….. 4,500

Copyrights ………………………………………………. 6,750

EXERCISE 22-16 (10–15 minutes)

1. Salaries and Wages Expense ………………………….. 3,400

Salaries and Wages Payable …………………….. 3,400

2. Salaries and Wages Expense ………………………….. 31,100

Salaries and Wages Payable …………………….. 31,100

EXERCISE 22-17 (10–15 minutes)

Retained Earnings …………………………………………………. 37,700

Inventory ……………………………………………………….. 16,200

Accumulated Depreciation—Equipment …………… 21,500

($38,500 – $17,000)

Computations:

Effect on retained earnings

over (under) statement

EXERCISE 22-18 (25–30 minutes)

(a) Effect of errors on 2015 net income: $24,700 overstatement

Computations:

Effect on 2015 net income

over (under) statement

Understatement of 2014 ending inventory

($ 9,600

Expensing of insurance premium in 2014

Failure to record sale of fully depreciated

(b) Effect of errors on working capital: $28,900 understatement

Computations:

Effect on working capital

over (under) statement

Overstatement of 2015 ending inventory

$( 8,100

Total effect on working capital (understated)

(c) Effect of errors on retained earnings: $26,600 understatement

Computations:

Effect on retained earnings

over (under) statement

Overstatement of 2015 ending inventory

$( 8,100

Expensing of insurance premium in 2014

EXERCISE 22-19 (20–25 minutes)

(a) 1. Supplies Expense ($2,700 – $1,100) ……………… 1,600

Supplies ………………………………………………. 1,600

2. Salary and Wages Expense ………………………….. 2,900

($4,400 – $1,500)

Salaries and Wages Payable …………………. 2,900

5. Rent Revenue ($28,000 ÷ 2) ………………………….. 14,000

Unearned Rent Revenue ……………………….. 14,000

(b) 1. Retained Earnings ………………………………………. 1,600

Supplies ………………………………………………. 1,600

2. Retained Earnings ………………………………………. 2,900

Salaries and Wages Payable …………………. 2,900

7. Same as in (a).

EXERCISE 22-19 (Continued)

(c) 6. Retained Earnings ………………………………………. 27,000

7. Retained Earnings ………………………………………. 4,320

EXERCISE 22-20 (20–25 minutes)

2014

2015

Income before tax

$101,000

$77,400

Corrections:

Sales erroneously included in 2014 income

(38,200)

38,200

Adjustment to bond interest expense*

Corrected income before tax

*Bond interest expense for 2014 and 2015 was computed as follows:

Book Value of Bonds

Stated Interest

Effective Interest

2014

$235,000

$15,000

$16,450**

2015

EXERCISE 22-20 (Continued)

***Erroneous depreciation taken in 2015:

EXERCISE 22-21 (10–15 minutes)

2014

2015

Item

Over–

statement

Under-

statement

No

Effect

Over–

statement

Under-

statement

No

Effect

(1)

X

X

(2)

X

X

(3)

X

(4)

X

X

(5)

X

X

*EXERCISE 22-22 (25–30 minutes)

Because Beyonce Co. now has a 30% interest in Elton John Corp. as of

7/1/15, it is necessary to first adjust the investment in Elton John to the

equity method in prior periods. The following schedule provides this

information:

12/31/14

6/30/15

Note to instructor: Under GAAP, goodwill is not amortized.

A computation of the ending balance in the investment account of Elton

John Corp. can now be made as follows:

Investment in Elton John Corp. 1/1/14 $1,400,000

*EXERCISE 22-23 (15–20 minutes)

(a) Prior to January 2, 2014, Dan Aykroyd Corp. carried the investment in

Martin Company under the equity method of accounting as evidenced

from the entries in the investment account. Use of the equity method

(b) The carrying amount of the investment in Martin as of December 31,

2014, would be computed as follows:

Carrying amount, 12/31/13 (from the given

account information) $3,690,000

bComputation of Excess Dividends Received over Share of Earnings:

Dividends

Received

Share of Martin Co.

Income

Excess Dividends Received

Over Share of Earnings

*EXERCISE 22-23 (Continued)

Note to instructor: The entry in 2014 to record the receipt of the

dividend would be:

Cash ……………………………………………………………… 50,400

TIME AND PURPOSE OF PROBLEMS

Problem 22-1 (Time 30–35 minutes)

Purpose—to provide a problem that requires the student to: (1) account for a change in estimate,

(2) record a correction of an error, and (3) account for a change in accounting principle. The student is

also required to compute corrected/adjusted net income amounts.

Problem 22-2 (Time 30–40 minutes)

Purpose—to develop an understanding of the way in which accounting changes and error corrections

Problem 22-3 (Time 30–40 minutes)

Problem 22-4 (Time 40–50 minutes)

Purpose—to allow the student to see the impact of accounting changes on income and to examine an

ethical situation related to the motivation for change.

Problem 22-5 (Time 30–35 minutes)

Purpose—to develop an understanding of the impact which a change in the method of inventory pricing

Problem 22-6 (Time 25–30 minutes)

Purpose—to develop an understanding of the journal entries and the reporting which are necessitated

Problem 22-7 (Time 25–30 minutes)

Purpose—to provide a problem that requires the student to analyze ten transactions and to prepare

adjusting or correcting entries for these transactions.

Problem 22-8 (Time 30–35 minutes)

Problem 22-9 (Time 20–25 minutes)

Time and Purpose of Problems (Continued)

Problem 22-10 (Time 50–60 minutes)

Purpose—to develop an understanding of the correcting entries and income statement adjustments that

*Problem 22-11 (Time 20–25 minutes)

Purpose—to provide the student with a problem involving an investment that grows from 10% to 40%

(from lack of significant influence to significant influence). The student is required to account for the

effect of this change on income.

*Problem 22-12 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the proper entries to reflect a change from

SOLUTIONS TO PROBLEMS

PROBLEM 22-1

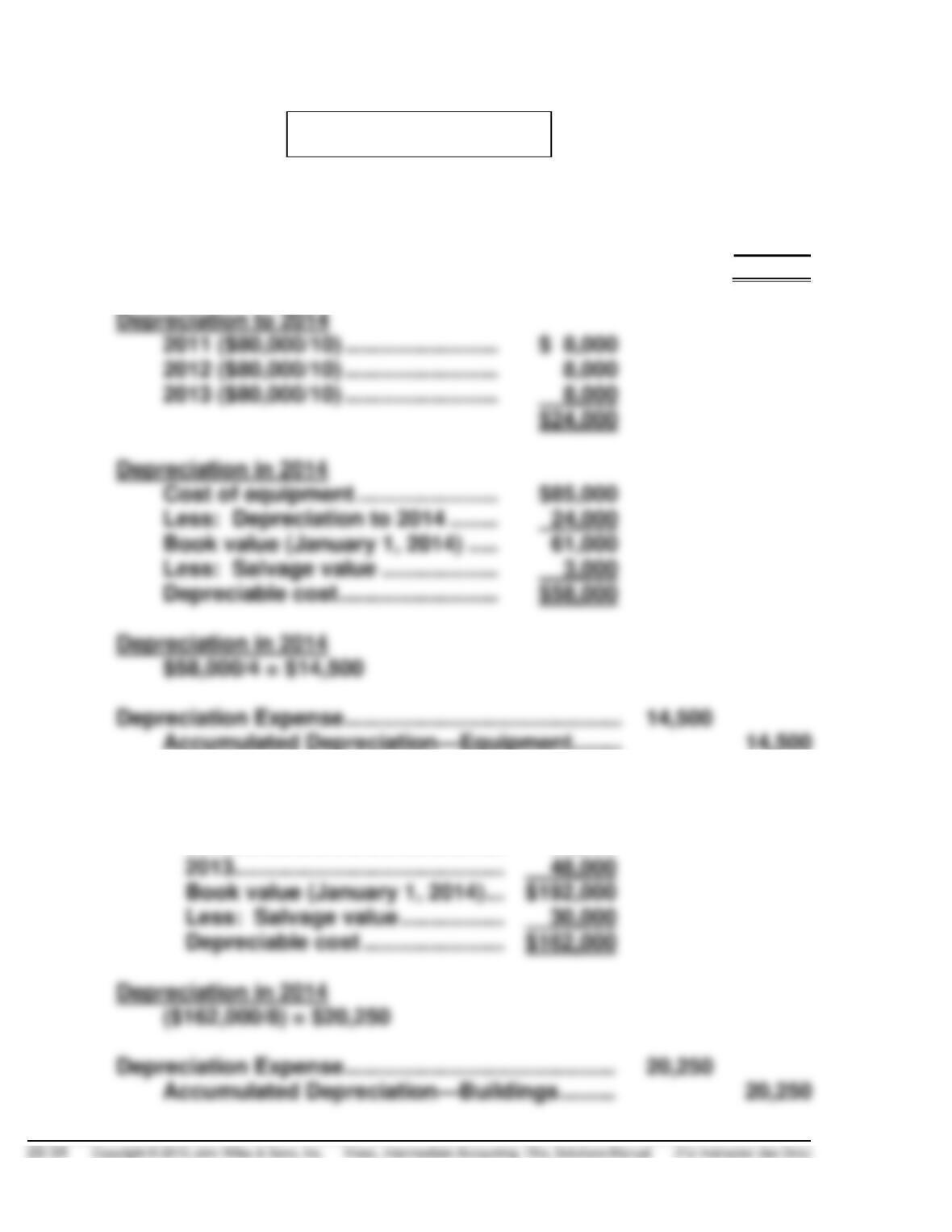

(a) 1. Cost of equipment ………………………………………………….. $85,000

Less: Salvage value …………………………..…………………… 5,000

Depreciable cost ……………………………………………………. $80,000

2. Cost of Building …………………………….. $300,000

Less: Depreciation to 2014

2012…………………………………….. 60,000

PROBLEM 22-1 (Continued)

3. Depreciation Expense ($120,000 – $16,000) ÷ 8 ….. 13,000

Accumulated Depreciation—Machinery ……… 13,000

Accumulated Depreciation—Machinery …………….. 3,000

Retained Earnings …………………………………….. 3,000

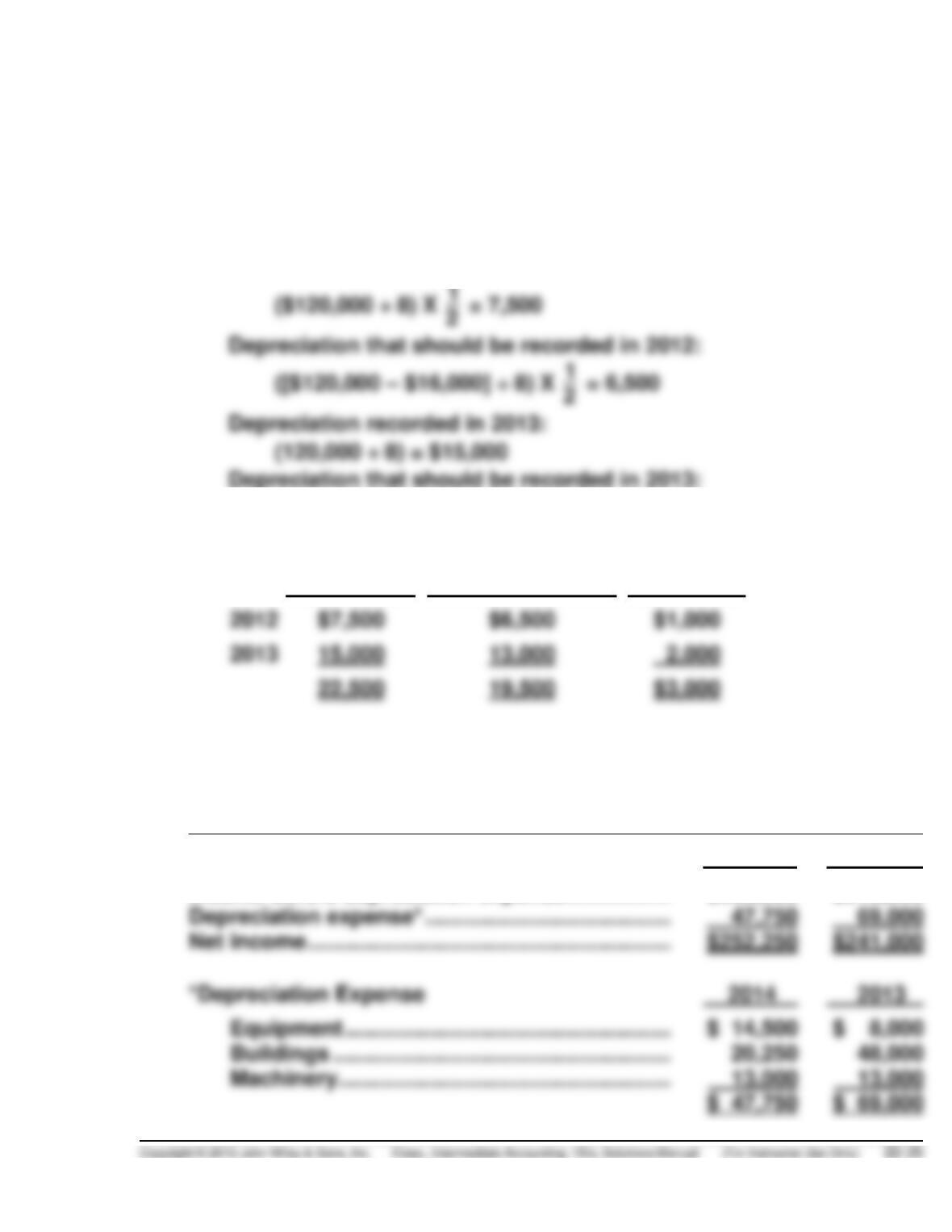

Depreciation recorded in 2012:

(120,000 – $16,000) ÷ 8 = 13,000

Depreciation

taken

Depreciation that

should be taken

Differences

(b) HOLTZMAN COMPANY

Comparative Income Statements

For the Years 2014 and 2013

2014

2013

Income before depreciation expense………………..

$300,000

$310,000

Depreciation expense* …………………………………….

47,750

69,000

*Depreciation Expense

2014

2013

PROBLEM 22-2

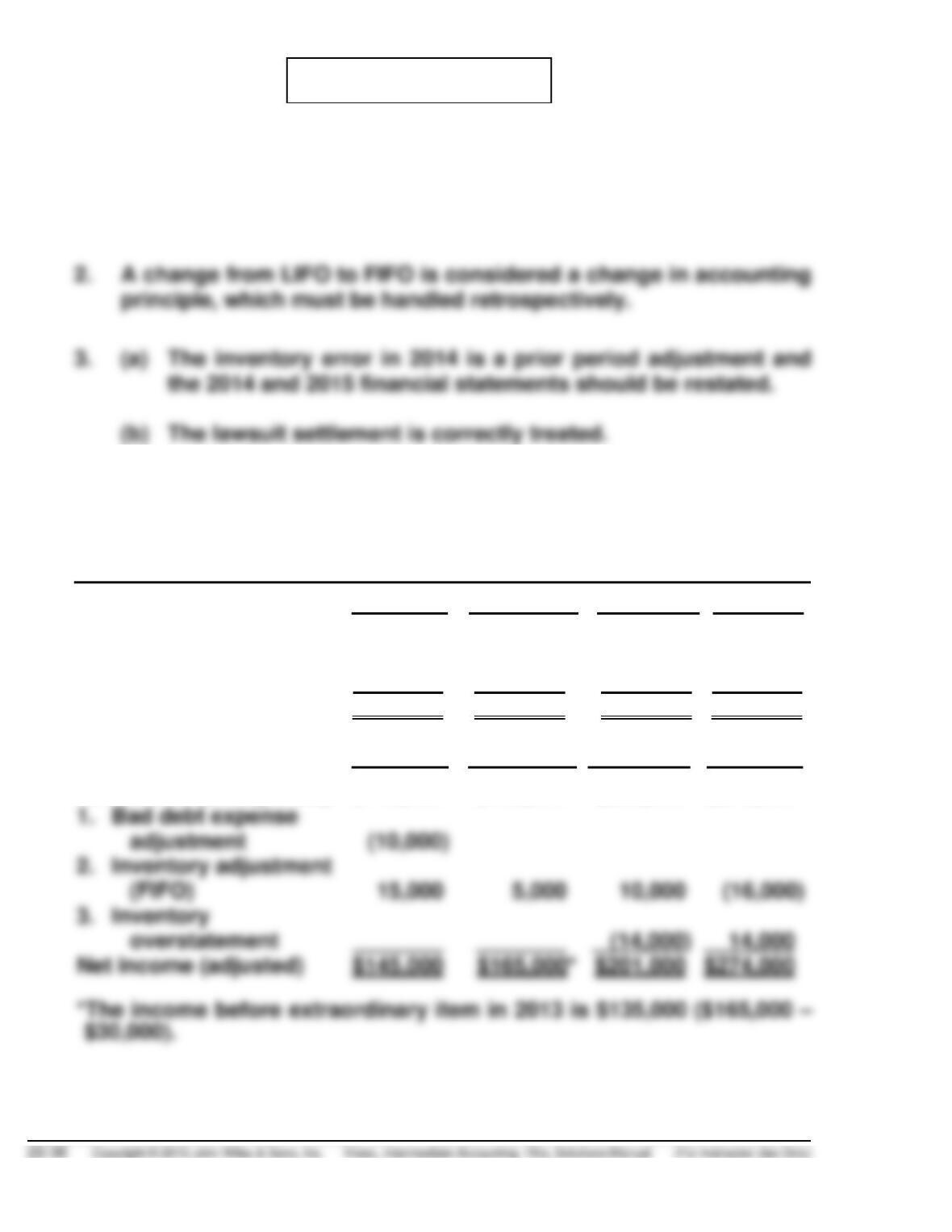

(a) 1. Bad debt expense for 2012 should not have been reduced by

$10,000. A change in the experience rate is considered a change

in estimate, which should be handled prospectively.

(b) BOTTICELLI INC.

Comparative Income Statements

For the Years 2012 through 2015

2012

2013

2014

2015

Income before

extraordinary item

$145,000

$135,000*

$201,000

$274,000

Extraordinary gain

30,000

Net income (see below)

$145,000

$165,000

$201,000

$274,000

2012

2013

2014

2015

Net income (unadjusted)

$140,000

$160,000

$205,000

$276,000

Net income (adjusted)

$145,000

$201,000

$274,000

PROBLEM 22-3

1. Retained Earnings …………………………………………….. 3,500

Sales Commissions Payable ……………………….. 2,500

2. Cost of Goods Sold ($19,000 + $6,700) ……………….. 25,700

3. Accumulated Depreciation—Equipment ……………… 4,800

Depreciation Expense …………………………………. 4,800*

*Equipment cost …………………………………. $100,000

4. Construction in Process ……………………………………. 45,000

Deferred Tax Liability ………………………………….. 18,000*

PROBLEM 22-4

(a) ASTON CORPORATION

Projected Income Statement

For the Year Ended December 31, 2014

Sales …………………………………………….. $29,000,000

Cost of goods sold ………………………… $14,000,000

Depreciation expense …………………….. 1,600,000a

Operating expenses ……………………….. 6,400,000 22,000,000

Conditions met:

1. Net income before taxes and bonus > $7,000,000.

2. Payable for income taxes does not exceed $3,000,000.

aDepreciation for the current year includes $600,000 for the old equip-

PROBLEM 22-4 (Continued)

(b) Students’ answers will vary.

There is nothing unethical about changing the first-year election of

depreciation back to the straight-line method provided that it meets with

the approval of appropriate corporate decision makers. Considering the

immediate needs for cash of $1,000,000 for the president’s bonus and

Some stakeholders and their interests are:

Stakeholder

Interests

President

Personal gain of $1,000,000 bonus.

CFO

Board of Directors

May be subject to the manipulations of the CEO

Placed in ethical dilemma between the interests

PROBLEM 22-5

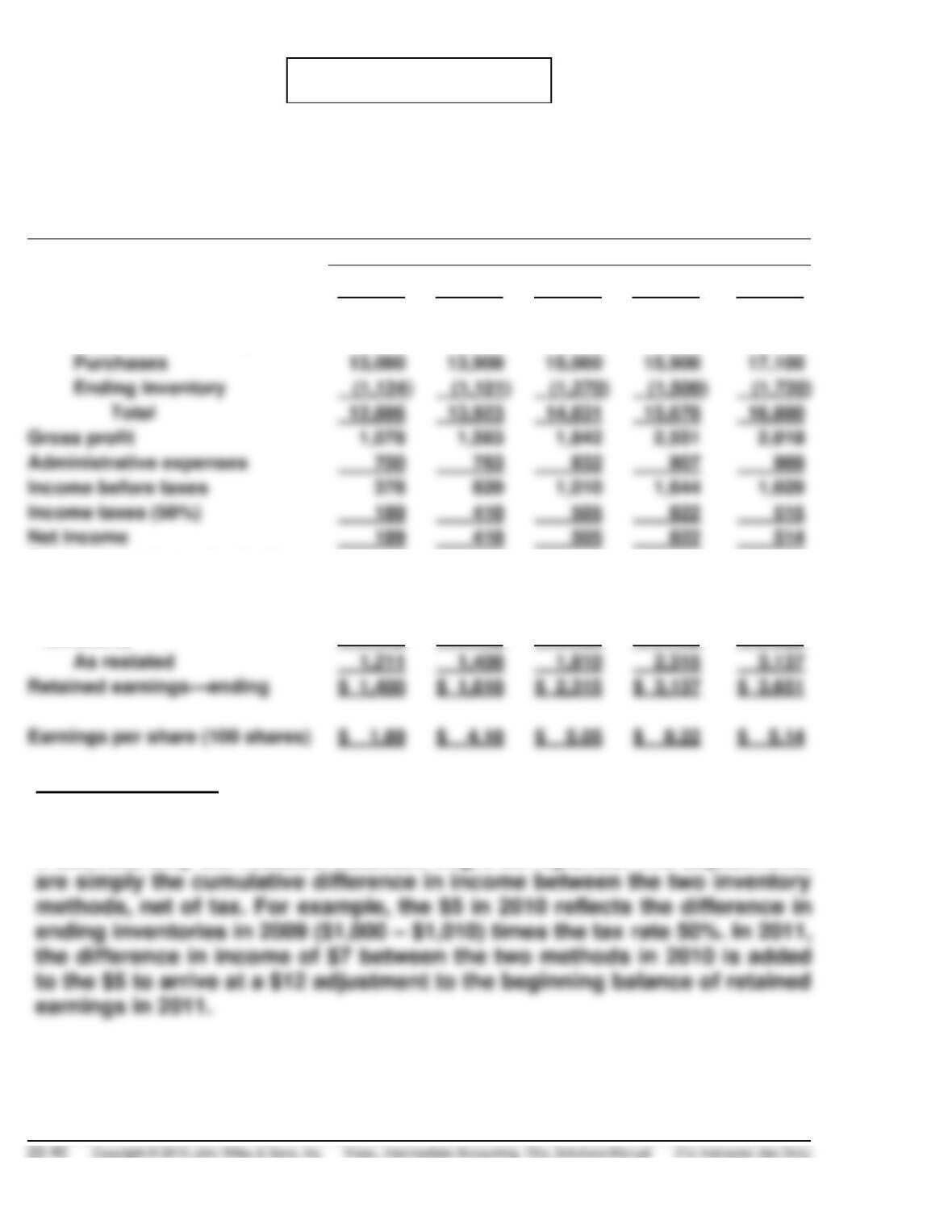

UTRILLO INSTRUMENT COMPANY

Statement of Income and Retained Earnings

For the Years Ended May 31

2010

2011

2012

2013

2014

Sales—net

$13,964

$15,506

$16,673

$18,221

$18,898

Cost of goods sold

Beginning inventory

1,010

1,124

1,101

1,270

1,500

Purchases

Ending inventory

Total

Gross profit

1,078

1,583

1,842

2,551

2,018

Administrative expenses

Income before taxes

1,010

1,644

1,029

Income taxes (50%)

Net income

Retained earnings—beginning:

As originally reported

1,206

1,388

1,759

2,237

3,005

Adjustment (See note* and

schedule)

5

12

51

78

132

As restated

Earnings per share (100 shares)

*Note to instructor:

The retained earnings balances are usually reported in the above manner.

If desired, only the restated balances might be reported. The adjustments