CHAPTER 18

Revenue Recognition

*1. Realization and recognition;

1, 2, 3, 4,

1, 2, 3,

1, 2, 3, 4,

1

1, 2, 3, 4,

11, 29

5

9

*3. Long-term contracts.

17, 18,

19, 29

10, 11

15,16,

17, 18

6, 7, 15, 16,

17

14, 15, 16,

7, 8, 9,

12, 13, 14,

1, 2, 3, 4, 5,

1, 2, 3, 6

*4. Installment sales.

24, 25, 26,

27, 28, 29

22, 23, 24

11, 12, 14

20, 21, 23,

12, 13, 14

19, 20, 21,

1, 8, 9, 10,

1, 2, 3

*5. Repossessions on

installment sales.

13

21, 25, 26

10, 11, 12,

13, 14

*6. Cost-recovery method;

deposit method.

20, 21, 22,

30, 31

15

23, 24

7

*7. Franchising.

32, 33,

34, 35

16

27, 28

8

CA18-3

1. Describe and apply

1, 2, 3, 4

6, 7, 8, 9

CA18-1,

CA18-3,

2. Describe

accounting issues

5, 6, 7, 8, 9,

10, 11, 12, 13

1, 2, 3, 4, 5, 6

1, 2, 3, 4, 5, 6,

7, 8, 9, 10, 11

1

CA18-1,

CA18-2,

6, 7, 16, 17

3. Apply the

percentage-of–

14, 15, 17, 19

7, 8

12, 13, 14,

15, 16, 17

1, 2, 3, 4,

5,

CA18-6

16, 17

4. Apply the

completed-contract

16

9, 10

12, 16,

17, 18

1, 2, 3, 5,

6, 7, 15,

CA18-7

5. Identify the proper

accounting for

18

11

18

5, 6, 7, 15

23, 24, 25,

23, 24, 25, 26

11, 12, 13,

6. Describe the

20, 21, 22,

12, 13, 14

19, 20, 21, 22,

1, 8, 9, 10,

7. Explain the cost-

30, 31

15

23, 24

*8. Explain revenue

32, 33, 34, 35

16

27, 28

CA18-8

ASSIGNMENT CHARACTERISTICS TABLE

E18-1

Revenue recognition—point of sale.

Simple

5–10

E18-2

Revenue recognition—point of sale.

Simple

5–10

E18-3

Revenue recognition—point of sale.

Simple

5–10

E18-4

Revenue recognition—point of sale.

Simple

10–15

E18-5

Right of return.

Simple

5–10

E18-6

Revenue recognition on book sales with high returns.

Moderate

15–20

E18-7

Sales recorded both gross and net.

Simple

15–20

E18-8

Revenue recognition on marina sales with discounts.

Moderate

10–15

E18-9

Consignment computations.

Simple

15–20

E18-10

Multiple-deliverable agreement.

Simple

10–15

E18-11

Multiple-deliverable agreement.

Simple

5–10

E18-12

Recognition of profit on long-term contracts.

Moderate

20–25

E18-13

Analysis of percentage-of-completion financial statements.

Moderate

10–15

E18-14

Gross profit on uncompleted contract.

Simple

10–12

E18-15

Recognition of profit, percentage-of-completion.

Moderate

25–30

E18-16

Moderate

15–20

E18-17

Recognition of profit and balance sheet amounts for long-term

contracts.

Simple

15–25

E18-18

Long-term contract reporting.

Simple

15–25

E18-19

Installment-sales method calculations, entries.

Simple

15–20

E18-20

Analysis of installment-sales accounts.

Moderate

15–20

E18-21

Gross profit calculations and repossessed merchandise.

Moderate

15–20

E18-22

Interest revenue from installment sale.

Simple

10–15

E18-23

Installment-sales method and cost-recovery method.

Simple

10–15

E18-24

Installment-sales method and cost-recovery method.

Simple

15–20

*E18-25

Installment-sales—default and repossession.

Simple

10–15

*E18-26

Installment-sales—default and repossession.

Simple

15–20

*E18-27

Franchise entries.

Simple

14–18

*E18-28

Franchise fee, initial down payment.

Simple

12–16

P18-1

Comprehensive three-part revenue recognition.

Moderate

30–45

P18-2

Recognition of profit on long-term contract.

Simple

20–25

P18-4

Recognition of profit and balance sheet presentation,

percentage-of-completion.

Moderate

20–30

P18-5

Completed contract and percentage-of-completion

with interim loss.

Moderate

25–30

P18-6

Long-term contract with interim loss.

Moderate

20–25

P18-7

Long-term contract with an overall loss.

Moderate

20–25

P18-8

Installment-sales computations and entries.

Moderate

25–30

P18-9

Installment-sales income statements.

Moderate

30–35

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

P18-10

Installment-sales computations and entries.

Complex

30–40

P18-11

Installment-sales entries.

Simple

20–25

inventory.

P18-13

Installment repossession entries.

Moderate

20–25

P18-14

Installment-sales computations and schedules.

Complex

50–60

P18-15

Completed-contract method.

Moderate

20–30

P18-17

Comprehensive problem—long-term contracts.

Complex

50–60

CA18-1

Revenue recognition—alternative methods.

Moderate

20–30

CA18-2

Recognition of revenue—theory.

Moderate

35–45

CA18-3

Recognition of revenue—theory.

Moderate

25–30

CA18-4

Recognition of revenue—bonus dollars.

Moderate

30–35

CA18-5

Recognition of revenue from subscriptions.

Complex

35–45

CA18-6

Long-term contract—percentage-of-completion.

Moderate

20–25

CA18-7

Revenue recognition—membership fees, ethics.

Moderate

20–25

* CA18-8

Franchise revenue.

Moderate

35–45

SOLUTIONS TO CODIFICATION EXERCISES

CE18-1

Master Glossary

(a) Under the cost-recovery method, no profit is recognized until cash payments by the buyer,

including principal and interest on debt due to the seller and on existing debt assumed by the

CE18-2

According to FASB ASC 605-10–25-3 (Revenue Recognition—Recognition):

CE18-3

According to FASB ASC 910-605–50-2 (Contractors—Revenue Recognition—Disclosure):

CE18-4

According to FASB ASC 605-10–25-4 (Revenue Recognition—Recognition):

55-7 through 55-9, the installment-sales method apportions collections received between cost recov-

1. A series of highly publicized cases of companies recognizing revenue prematurely has caused

the SEC to increase its enforcement actions in this area. In some of these cases, significant

3. The revenue recognition principle indicates that revenue is recognized when it is 1) realized or

realizable and 2) when it is earned.

4. Revenues are recognized generally as follows:

(a) Revenue from selling products—date of delivery to customers.

6. The three alternatives available to a seller that is exposed to risks of ownership due to a return of

the product are:

(2) Recording the sale, but reducing sales by an estimate of future returns.

7. GAAP requires that such sales transactions not be recognized as current revenue unless all of

the following six conditions are met:

(2) The buyer has paid the seller, or the buyer is obligated to pay the seller, and the obligation

is not contingent on resale of the product.

(4) The buyer acquiring the product for resale has economic substance apart from that provided

by the seller.

(6) The seller can reasonably estimate the amount of future returns.

8. Bill and hold sales result when the buyer is not yet ready to take delivery but the buyer takes title

and accepts billing. Revenue is recognized at the time title passes, provided (1) the risk of

9. If a company sells a product in one period and agrees to buy it back in the next period, legal title

has transferred, but the economic substance of the transaction is that the seller retains the risks

11. A sale on consignment is the shipment of merchandise from a manufacturer (or wholesaler) to

a dealer (or retailer) with title to the goods and the risk of sale being retained by the manufacturer

who becomes the consignor. The consignee (dealer) is expected to exercise due diligence in

12. A multiple deliverable arrangement provides multiple products or services to customers as part of

13. Once the separate units of a multiple deliverable arrangement are determined, the amount paid

14. The two basic methods of accounting for long-term construction contracts are: (1) the percentage-

of-completion method and (2) the completed-contract method.

(1) The contract clearly specifies the enforceable rights regarding goods or services to be

(2) The buyer can be expected to satisfy all obligations under the contract.

(3) The contractor can be expected to perform the contractual obligations.

15.

Costs Incurred

X Total Revenue = Revenue Recognized

16. Under the percentage-of-completion method, income is reported to reflect more accurately the

production effort. Income is recognized periodically on the basis of the percentage of the job

17. The methods used to determine the extent of progress toward completion are the cost-to-cost

18. The two types of losses that can become evident in accounting for long-term contracts are:

(2) A loss related to an unprofitable contract.

The first type of loss is actually an adjustment in the current period of gross profit recognized on

the contract in prior periods. It arises when, during construction, there is a significant increase in the

19. The dollar amount of difference between the Construction in Process and the Billings on Con–

struction in Process accounts is reported in the balance sheet as a current asset if a debit and as

20. Under the installment-sales method, income recognition is deferred until the period of cash

collection. At the end of each year, the appropriate gross profit rate is applied to the cash

21. The two methods generally employed to account for cash received when cash collection of the sales

price is not reasonably assured are: (1) the cost–recovery method and (2) the installment-sales method.

22. The deposit method postpones recognizing a sale by treating the cash received from a buyer as

23. An installment sale is a special type of credit arrangement which provides for payment in periodic

installments over a predetermined period of time and results from the sale of real estate,

24. Under the installment-sales method of accounting, emphasis is placed on collection rather than

sale. Because of the unique characteristics of installment sales, particularly the longer collection

period and higher risk of loss through bad debts, gross profit is considered to be realized in

25. In the application of the installment-sales method, most companies record operating expenses

without regard to the fact that some portion of the year’s gross profit is to be deferred revenue.

26.

Year

Cash

Collected

X

*Gross Profit

Percentage

=

Gross Profit

Recognized

27. When interest is involved in installment sales, it should be separately accounted for as interest

28. With respect to the income statement, the degree of detail to be reported frequently will vary,

depending upon the magnitude of installment-sales revenues in relation to total sales. If install-

(1) Total, (2) Regular Sales, and (3) Installment Sales. Obviously, many variations are possible

and should be used to meet the necessities of information and full disclosure.

29. (a) Income (gross profit) on certain installment sales may be recognized on a basis of:

Gross Profit

X Collections.

30. Under the cost-recovery method, revenue is recognized (along with the relevant cost of goods sold)

in the period of the sale. However, the gross profit is deferred and is not recognized in the income

*31. Under the deposit method, revenue is not recognized. The deposit method treats cash advances

and other payments received as refundable deposits. The sales transaction is not considered

*32. It is improper to recognize the entire franchise fee as revenue at the date of sale when many of

*33. In a franchise sale, the franchisor may record initial franchise fees as revenue only when the

franchisor makes “substantial performance” of the services it is obligated to perform. Substantial

*34. Continuing franchise fees should be reported as revenue when they are earned and receivable

from the franchisee, unless a portion of them have been designated for a particular purpose. In

*35. (a) If it is likely that the franchisor will exercise an option to purchase the franchised outlet, the

initial franchise fee should not be recorded as a revenue but as a deferred credit. When

SOLUTIONS TO BRIEF EXERCISES

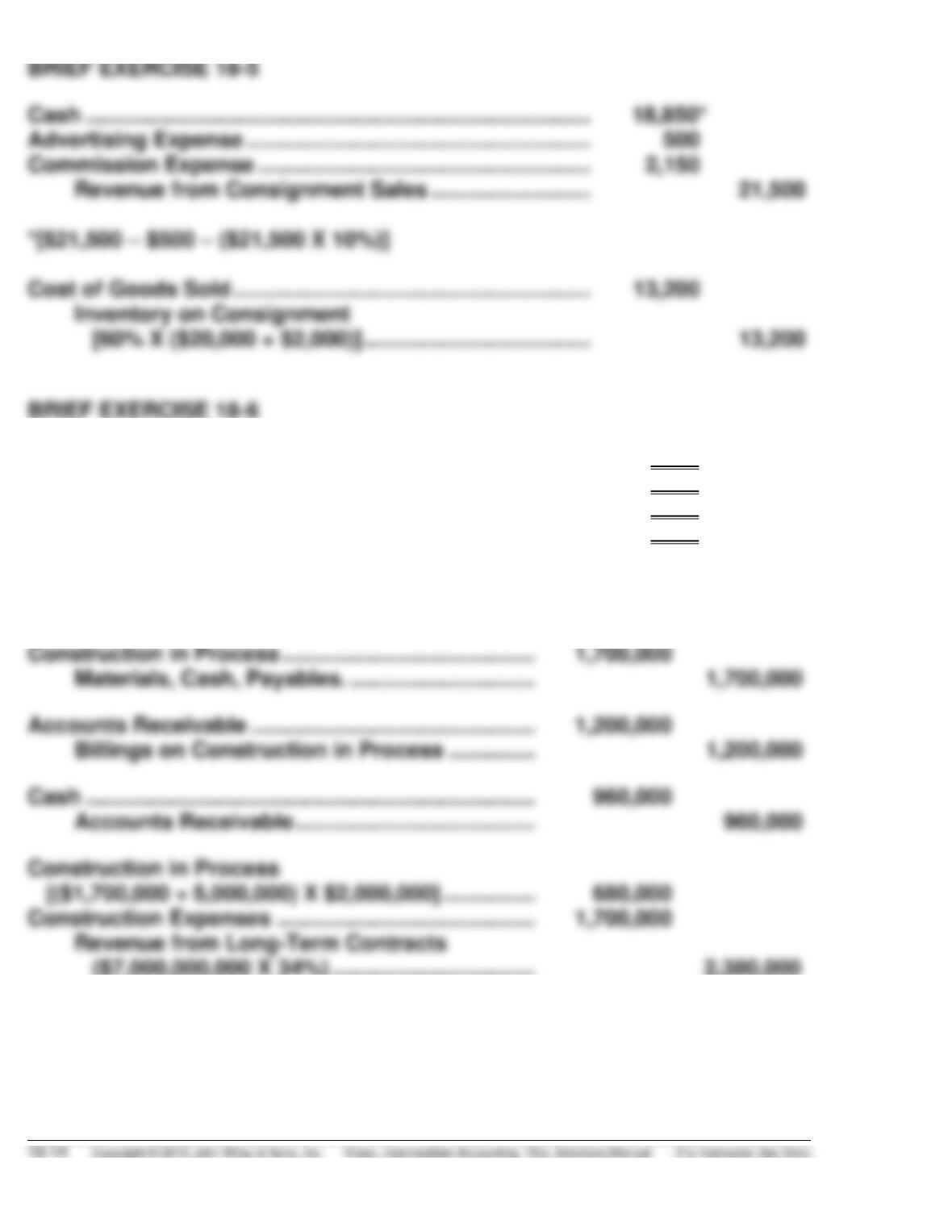

BRIEF EXERCISE 18-1

Accounts Receivable ……………………………………….. 103,400

Sales Revenue ($110,000 X 94%) ………………… 103,400

BRIEF EXERCISE 18-2

Accounts Receivable ………………………….. 78,000

(b) Sales Returns and Allowances …………………… 27,000

Allowance for Sales Returns and

Allowances

[(15% X $700,000) – $78,000] …………… 27,000

January income ………………………………………………………. $ 0

February income ($4,000 – $3,000) X 50% …………………. $500

March income ($4,000 – $3,000 X 30%) ……………………… $300

April income ($4,000 – $3,000 X 20%) ……………………….. $200

BRIEF EXERCISE 18-7

BRIEF EXERCISE 18-8

Current Assets

Accounts receivable ………………………………….. $ 240,000

Inventories

Construction in process ……………………… $2,450,000

BRIEF EXERCISE 18-10

Current Assets

Accounts receivable ………………………………….. $240,000

Inventories

Construction in process ……………………… $1,715,000

Installment Accounts Receivable, 2014 ………………… 150,000

Installment Sales Revenue ……………………………. 150,000

Cash ………………………………………………………………….. 54,000

Installment Accounts Receivable, 2014 …………. 54,000

Cost of Installment Sales …………………………………….. 102,000

Installment Accounts Receivable ………………….. 520

*[$275 – ($520 – $208)]

BRIEF EXERCISE 18-14

Current Assets

Installment accounts receivable due in 2015 ….. $ 65,000

BRIEF EXERCISE 18-15

2014 $0

2015 $2,000 ($15,000 – $13,000)

EXERCISE 18-1 (5–10 minutes)

(a) Notes Receivable ……………………………………. 600,000

EXERCISE 18-2 (5–10 minutes)

(a) Accounts Receivable ………………………………. 410,000

Sales Revenue …………………………………. 370,000

EXERCISE 18-3 (5–10 minutes)

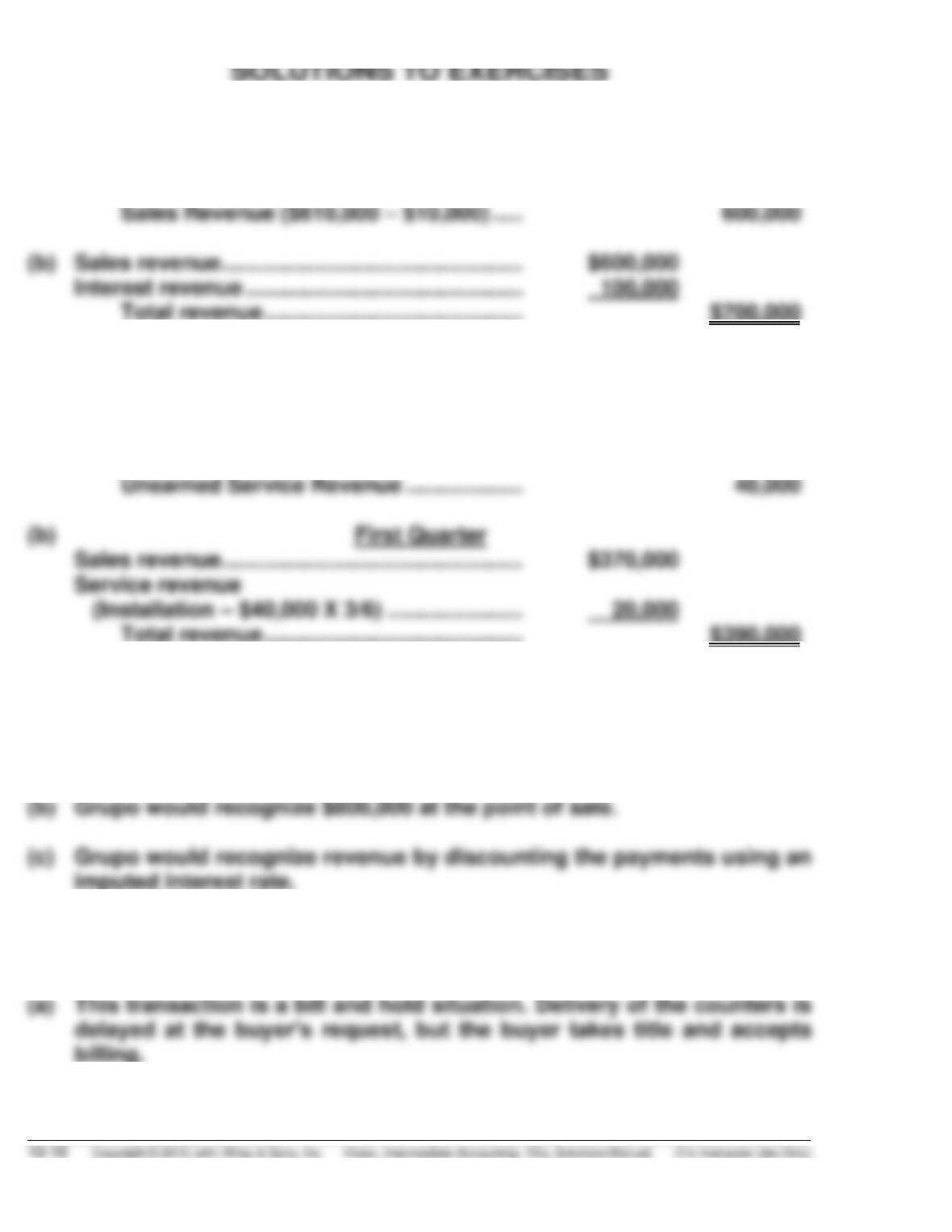

(a) Grupo would recognize $1,000,000 of revenue at delivery.

EXERCISE 18-4 (10–15 minutes)

EXERCISE 18-4 (Continued)

(b) Revenue is reported at the time title passes if (1) the risks of ownership

has passed; (2) the buyer makes a fixed commitment of purchase the

EXERCISE 18-5 (5-10 minutes)

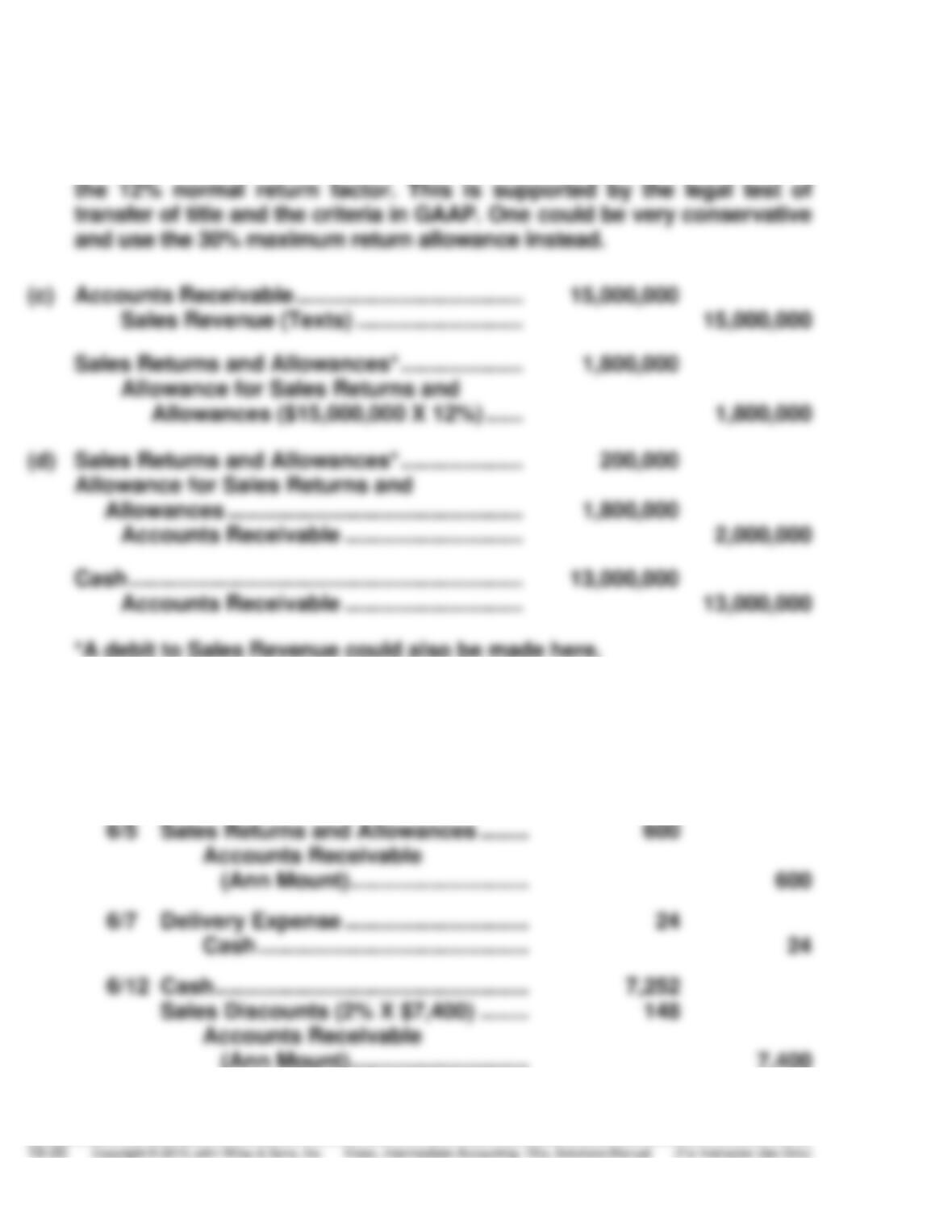

(a) Accounts Receivable ……………………………….. 1,500,000

Sales Revenue ………………………………….. 1,500,000

EXERCISE 18-6 (15–20 minutes)

(a) Uddin could recognize revenue at the point of sale based upon the time

EXERCISE 18-6 (continued)

(b) Based on the available information and lack of any information indi–

cating that any of the criteria in GAAP were not met, the correct treatment

is to report revenue at the time of shipment as the gross amount less

EXERCISE 18-7 (15–20 minutes)

(a) 1. 6/3 Accounts Receivable (Ann Mount) …. 8,000

Sales Revenue ………………………. 8,000