CHAPTER 8

Valuation of Inventories: A Cost-Basis Approach

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Inventory accounts;

determining quantities,

costs, and items to be

included in inventory;

the inventory equation;

balance sheet disclosure.

1, 2, 3, 4,

5, 6, 8, 9

1, 3

1, 2, 3,

4, 5, 6

1, 2, 3

1, 2, 3, 5

5.

Flow assumptions.

12, 13, 16,

18, 20

5, 6, 7

9, 13, 14,

15, 16, 17,

18, 19, 20,

21, 22

1, 4, 5,

6, 7

5, 6, 7, 8, 11

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Identify major classifications of inventory.

1

1

2. Distinguish between perpetual and

periodic inventory systems.

3

2

4, 9, 13,

17

4, 5, 6

financial statements.

4. Understand the items to include as

inventory cost.

8

3

1, 2, 3, 4,

5, 6, 7, 8

1, 2, 3

CA8-1,

CA8-2,

CA8-4

18, 19, 20,

22

CA8–10

6. Explain the significance and use of a

LIFO reserve.

13, 18

21

CA8–11

7. Understand the effect of LIFO

liquidations.

20

8. Explain the dollar-value LIFO method.

14, 15, 17,

19

8, 9

22, 23, 24,

25, 26

1, 8, 9,

10, 11

CA8-9

of LIFO.

CA8-8,

inventory methods.

2

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E8-1

Inventoriable costs.

Moderate

15–20

E8-2

Inventoriable costs.

Moderate

10–15

E8-3

Inventoriable costs.

Simple

10–15

E8-4

Inventoriable costs—perpetual.

Simple

10–15

E8-5

Inventoriable costs—error adjustments.

Moderate

15–20

E8-6

Determining merchandise amounts—periodic.

Simple

10–20

E8-7

Purchases recorded net.

Simple

10–15

E8-8

Purchases recorded, gross method.

Simple

20–25

E8-9

Periodic versus perpetual entries.

Moderate

15–25

E8–10

Inventory errors—periodic.

Simple

10–15

E8–11

Inventory errors.

Simple

10–15

E8–12

Inventory errors.

Moderate

15–20

E8–13

FIFO and LIFO—periodic and perpetual.

Moderate

15–20

E8–14

FIFO, LIFO and average-cost determination.

Moderate

20–25

E8–15

FIFO, LIFO, average-cost inventory.

Moderate

15–20

E8–16

Compute FIFO, LIFO, average-cost—periodic.

Moderate

15–20

E8–17

FIFO and LIFO—periodic and perpetual.

Simple

10–15

E8–18

FIFO and LIFO; income statement presentation.

Simple

15–20

E8–19

FIFO and LIFO effects.

Moderate

20–25

E8–20

FIFO and LIFO—periodic.

Simple

10–15

E8–22

Alternate inventory methods—comprehensive.

Moderate

25–30

E8–23

Dollar-value LIFO.

Simple

E8–24

Dollar-value LIFO.

Simple

15–20

E8–25

Dollar-value LIFO.

Moderate

20–25

E8–26

Dollar-value LIFO.

Moderate

15–20

P8-1

Various inventory issues.

Moderate

30–40

P8-2

Inventory adjustments.

Moderate

25–35

P8-3

Purchases recorded gross and net.

Simple

20–25

P8-4

Compute FIFO, LIFO, and average-cost.

Complex

40–55

P8-5

Compute FIFO, LIFO, and average-cost.

Complex

40–55

and perpetual.

P8-7

Financial statement effects of FIFO and LIFO.

Moderate

30–40

P8-8

Dollar-value LIFO.

Moderate

30–40

P8-9

Internal indexes—dollar-value LIFO.

Moderate

25–35

P8–10

Internal indexes—dollar-value LIFO.

Complex

30–35

P8–11

Dollar-value LIFO.

Moderate

40–50

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Item

Description

Level of

Difficulty

Time

(minutes)

CA8-1

Inventoriable costs.

Moderate

15–20

CA8-2

Inventoriable costs.

Moderate

15–25

CA8-3

Inventoriable costs.

Moderate

25–35

CA8-4

Accounting treatment of purchase discounts.

Simple

15–25

CA8-5

General inventory issues.

Moderate

20–25

CA8-6

LIFO inventory advantages.

Simple

15–20

CA8-7

Average-cost, FIFO, and LIFO.

Simple

15–20

CA8-8

LIFO application and advantages.

Moderate

25–30

CA8-9

Dollar-value LIFO issues.

Moderate

25–30

CA8–10

FIFO and LIFO.

Moderate

30–35

CA8–11

LIFO Choices

Moderate

20–25

SOLUTIONS TO CODIFICATION EXERCISES

CE8-1

(a) Inventory is the aggregate of those items of tangible personal property that have any of the

following characteristics:

a. Held for sale in the ordinary of business.

b. To process of production for such sale.

c. To be currently consumed in the production of goods or services to be available for sale.

The term inventory embraces goods awaiting sale (the merchandise of a trading concern and the

finished goods of a manufacturer), goods in the course of production (work in process), and goods

(b) A customer is a reseller or a consumer, either an individual or a business that purchases a

vendor’s products or services for end use rather than for resale. This definition is consistent with

paragraph 280-10–50-42, which states that a group of entities known to a reporting entity to be

under common control shall be considered as a single customer, and the federal government, a

state government, a local government (for example, a country or municipality), or a foreign

government each shall be considered as a single customer.

45–19 Many sellers charge customers for shipping and handling in amounts in amounts that exceed

the related costs incurred. The components of shipping and handling costs, and the

determination of the amounts billed to customers for shipping and handling, may differ from

CE8-2 (Continued)

45–20 For those entities that determine under the indicators listed in paragraphs 605–45–45-4 through

45-18 that shipping and handling fees shall be reported gross, all amounts billed to a customer

45–21 Also, shipping and handling costs shall not be deducted from revenues (that is, netted against

shipping and handling revenues).

CE8-3

FASB ASC 330-10–35-1 and 15 with respect to adjustments to Lower of Cost or Market:

35-1 A departure from the cost basis of pricing the inventory is required when the utility of the goods

is no longer as great as their cost. Where there is evidence that the utility of goods, in their

35–15 Only in exceptional cases may inventories properly be stated above cost. For example,

precious metals having a fixed monetary value with no substantial cost of marketing may be

CE8-4

FASB ASC 330-10-S99-3 (SAB Topic 11.F, LIFO Liquidations) The following is the text of SAB

Topic 11.F, LIFO Liquidations.

Facts: Registrant on LIFO basis of accounting liquidates a substantial portion of its LIFO inventory and

as a result includes a material amount of income in its income statement which would not have been

recorded had the inventory liquidation not taken place.

Question: Is disclosure required of the amount of income realized as a result of the inventory liquidation?

ANSWERS TO QUESTIONS

1. In a retailing concern, inventory normally consists of only one category that is the product awaiting

resale. In a manufacturing company, inventories consist of raw materials, work in process, and

finished goods. Sometimes a manufacturing or factory supplies inventory account is also included.

2. (a) Inventories are unexpired costs and represent future benefits to the owner. A statement of

(b) Beginning and ending inventories are included in the computation of net income only for the

purpose of arriving at the cost of goods sold during the period of time covered by the state-

inventory are unexpired costs to be carried forward to a future period, rather than expensed.

3. In a perpetual inventory system, data are available at any time on the quantity and dollar amount

of each item of material or type of merchandise on hand. A physical inventory is a physical count

4. No, Mishima, Inc. should not report this amount on its balance sheet. As consignee, it does not

own this merchandise and therefore it is inappropriate for it to recognize this merchandise as part

of its inventory.

5. Product financing arrangements are essentially off-balance-sheet financing devices. These arrange-

6. (a) Inventory.

(b) Not shown, possibly in a note to the financial statements if material.

7. This omission would have no effect upon the net income for the year, since the purchases and the

ending inventory are understated in the same amount. With respect to financial position, both the

8. Cost, which has been defined generally as the price paid or consideration given to acquire an

asset, is the primary basis for accounting for inventories. As applied to inventories, cost means the

Questions Chapter 8 (Continued)

9. By their nature, product costs “attach” to the inventory and are recorded in the inventory account.

These costs are directly connected with the bringing of goods to the place of business of the buyer

and converting such goods to a salable condition. Such charges would include freight charges on

goods purchased, other direct costs of acquisition, and labor and other production costs incurred

in processing the goods up to the time of sale.

10. Cash discounts (purchase discounts) should not be accounted for as financial income when pay-

11. $60.00, $63.00, $61.80. (Freight-In not included for discount.)

12. Arguments for the specific identification method are as follows:

(1) It provides an accurate and ideal matching of costs and revenues because the cost is specifi–

cally identified with the sales price.

Arguments against the specific identification method include the following:

(1) The cost of using it restricts its use to goods of high unit value.

13. The first-in, first-out method approximates the specific identification method when the physical flow

of goods is on a FIFO basis. When the goods are subject to spoilage or deterioration, FIFO is

particularly appropriate. In comparison to the specific identification method, an attractive aspect of

Questions Chapter 8 (Continued)

probably least similar to current replacement costs. On the other hand, this method produces a

balance sheet value for the asset close to current replacement costs. It is claimed that FIFO is

deceptive when used in a period of rising prices because the reported income is not fully available

since a part of it must be used to replace inventory at higher cost.

The results achieved by the average-cost method resemble those of the specific identification

If it is assumed that actual cost is the appropriate method of valuing inventories, last-in, first-out is

not theoretically correct. In general, LIFO is directly adverse to the specific identification method

because the goods are not valued in accordance with their usual physical flow. An exception is the

application of LIFO to piled coal or ores which are more or less consumed in a LIFO manner.

Proponents argue that LIFO provides a better matching of current costs and revenues.

14. A company may obtain a price index from an outside source (external index)—the government, a

trade association, an exchange—or by computing its own index (internal index) using the double

15. Under the double extension method, LIFO inventory is priced at both base-year costs and current-

year costs. The total current-year cost of the inventory is divided by the total base-year cost to

obtain the current-year index.

The index for the LIFO pool consisting of product A and product B is computed as follows:

Base-Year Cost

Current-Year Cost

Product

Units

Unit

Total

Unit

Total

25,500

$260,100

10,350

$1,007,460

Base-Year Cost

Questions Chapter 8 (Continued)

16. The LIFO method results in a smaller net income because later costs, which are higher than

17. The dollar-value method uses dollars instead of units to measure increments, or reductions in a

LIFO inventory. After converting the closing inventory to the same price level as the opening

inventory, the increases in inventories, priced at base-year costs, is converted to the current price

level and added to the opening inventory. Any decrease is subtracted at base-year costs to

determine the ending inventory.

18. (a) LIFO layer—a LIFO layer (increment) is formed when the ending inventory at base-year prices

exceeds the beginning inventory at base-year prices.

19.

December 31, 2014 inventory at December 31, 2013 prices, $1,053,000 ÷ 1.08 ………..

$975,000

Less: Inventory, December 31, 2013 …………………………………………………………………..

800,000

Increment added during 2014 at December 31, 2014 prices, $175,000 X 1.08 …………..

$189,000

Add: Inventory at December 31, 2013 ………………………………………………………………….

800,000

20. Phantom inventory profits occur when the inventory costs matched against sales are less than the

replacement cost of the inventory. The cost of goods sold therefore is understated and profit is

considered overstated. Phantom profits are said to occur when FIFO is used during periods of

rising prices.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 8-1

RIVERA COMPANY

Balance Sheet (Partial)

December 31

Current assets

Cash …………………………………………………………..

$ 190,000

Receivables (net) …………………………………………

Work in process …………………………………..

Prepaid insurance ……………………………………….

41,000

BRIEF EXERCISE 8-2

Inventory (150 X $34) ………………………………………………

5,100

Accounts Payable …………………………………………..

5,100

Accounts Payable (6 X $34) ……………………………………..

Inventory ……………………………………………………….

Accounts Receivable (125 X $50) …………………………..

6,250

Sales ……………………………………………………………..

6,250

Cost of Goods Sold (125 X $34) …………………………..

4,250

Inventory ……………………………………………………….

4,250

BRIEF EXERCISE 8-3

December 31 inventory per physical count ………………………

$ 200,000

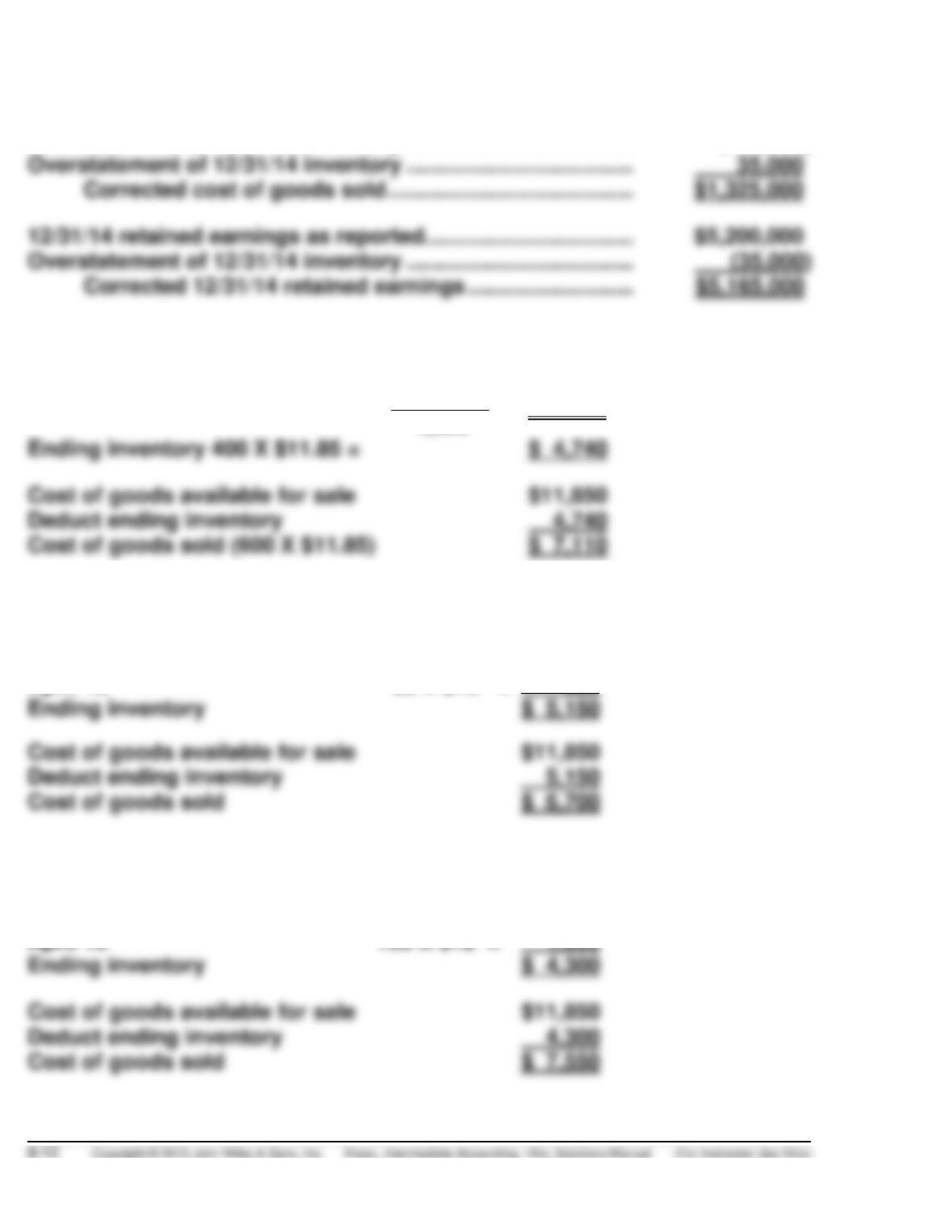

BRIEF EXERCISE 8-4

Cost of goods sold as reported ……………………………………….

$1,400,000

Overstatement of 12/31/13 inventory ……………………………….

(110,000)

Overstatement of 12/31/14 inventory ……………………………….

Overstatement of 12/31/14 inventory ……………………………….

BRIEF EXERCISE 8-5

Weighted average cost per unit

$11,850

=

$ 11.85

1,000

Cost of goods available for sale

$11,850

Deduct ending inventory

4,740

BRIEF EXERCISE 8-6

April 23

350 X $13

=

$ 4,550

April 15

50 X $12

=

600

Ending inventory

Cost of goods available for sale

$11,850

Deduct ending inventory

5,150

BRIEF EXERCISE 8-7

April 1 250 X $10 =

$ 2,500

April 15 150 X $12 =

1,800

Cost of goods available for sale

Deduct ending inventory

4,300

BRIEF EXERCISE 8-8

2013

$100,000

2014

$119,900 ÷ 1.10 = $109,000

$100,000 X 1.00 ……………………………………………………

$100,000

$9,000* X 1.10 ………………………………………………………

9,900

$109,900

$100,000 X 1.00 ……………………………………………………

$100,000

$9,000 X 1.10 ……………………………………………………….

9,900

$118,020

**$116,000 – $109,000

BRIEF EXERCISE 8-9

2014 inventory at base amount ($22,140 ÷ 1.08)

$ 20,500

2013 inventory at base amount

(19,750)

Increase in base inventory

$ 750

Layer one $19,750 X 1.00

Layer two $ 750 X 1.08

2014 inventory at base amount

Increase in base inventory

Layer one $19,750 X 1.00

Layer two $ 750 X 1.08

Layer three $ 2,250 X 1.14

EXERCISE 8-1 (15–20 minutes)

Items 1, 3, 5, 8, 11, 13, 14, 16, and 17 would be reported as inventory in the

financial statements.

The following items would not be reported as inventory:

2. Cost of goods sold in the income statement.

4. Not reported in the financial statements.

6. Cost of goods sold in the income statement.

EXERCISE 8-2 (10–15 minutes)

Inventory per physical count

$441,000

Goods in transit to customer, f.o.b. destination

+ 38,000

Goods in transit from vendor, f.o.b. seller

+ 51,000

EXERCISE 8-3 (10–15 minutes)

1. Include. Ownership of the merchandise passes to customer only

when it is shipped.

2. Do not include. Title did not pass until January 3.

EXERCISE 8-4 (10–15 minutes)

1.

Raw Materials Inventory …………………………..

8,100

Accounts Payable …………………………………………..

8,100

2.

Raw Materials Inventory …………………………..

28,000

Accounts Payable …………………………………………..

28,000

3.

No adjustment necessary.

Accounts Payable …………………………………………………..

7,500

Raw Materials Inventory …………………………..

7,500

Raw Materials Inventory …………………………..

Accounts Payable …………………………………………..

19,800

EXERCISE 8-5 (15–20 minutes)

(a)

Inventory December 31, 2014 (unadjusted)

$234,890

Transaction 2

13,420

Transaction 3

-0-

Transaction 4

-0-

Transaction 5

Transaction 6

Transaction 7

Transaction 8

Inventory December 31, 2014 (adjusted)

$237,392

(b)

Transaction 3

Sales Revenue ………………………………………..

12,800

Accounts Receivable …………………………..

12,800

(To reverse sale entry in 2014)

Transaction 4

Purchases (Inventory) ……………………………..

Accounts Payable …………………………..

Transaction 8

Sales Returns and Allowances…………………

Accounts Receivable ………………………

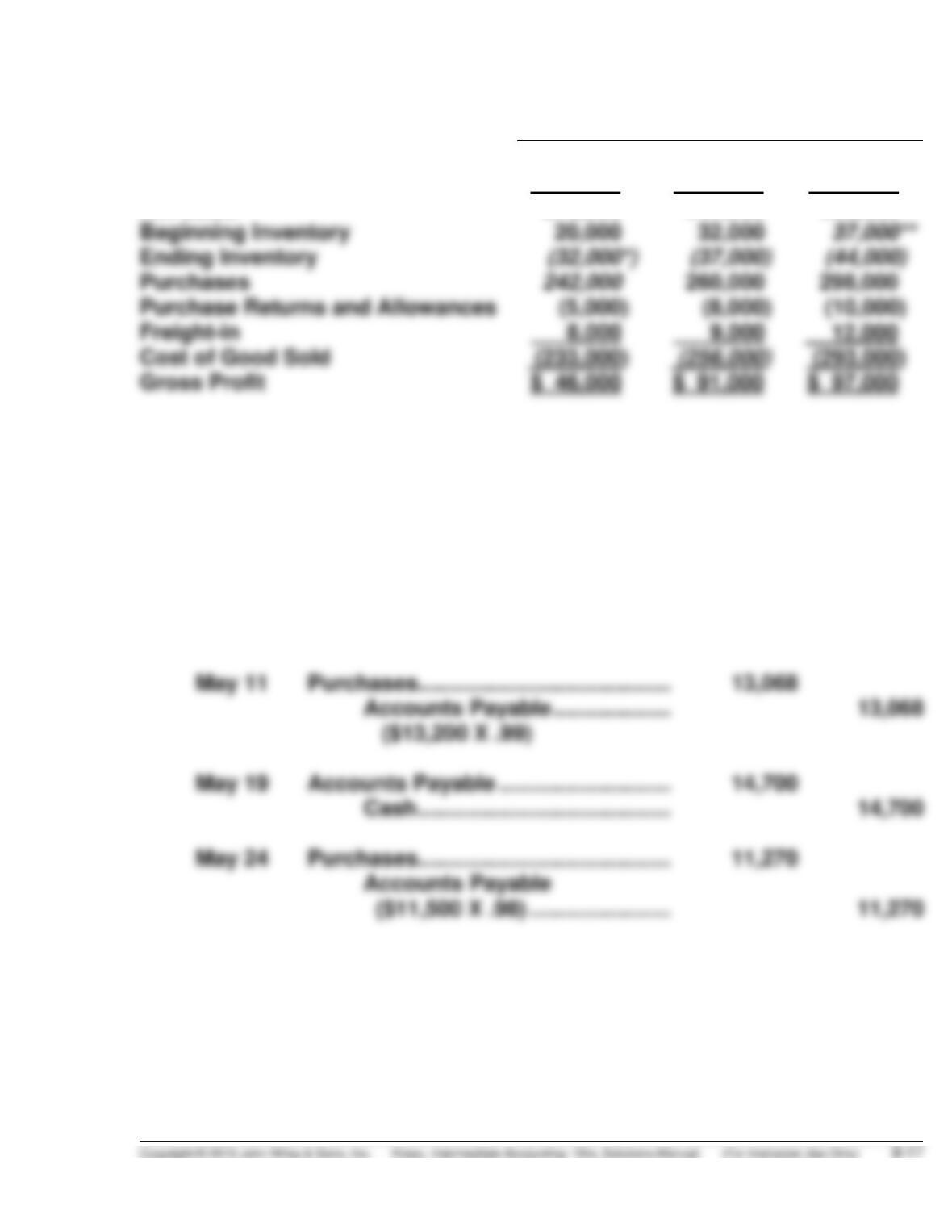

EXERCISE 8-6 (10–20 minutes)

2013

2014

2015

Sales

$290,000

$360,000

$410,000

Sales Returns

(11,000)

(13,000)

(20,000)

Net Sales

279,000

347,000

390,000

Beginning Inventory

Ending Inventory

Purchases

242,000

260,000

Purchase Returns and Allowances

Cost of Good Sold

*This was given as the beginning inventory for 2014.

**This was calculated as the ending inventory for 2014.

EXERCISE 8-7 (10–15 minutes)

(a)

May 10

Purchases ……………………………………………………….

14,700

Accounts Payable …………………………..

14,700

($15,000 X .98)

May 11

Purchases ……………………………………………………….

13,068

Accounts Payable …………………………..

13,068

($13,200 X .99)

May 19

Accounts Payable …………………………..

14,700

Cash ……………………………………………………….

14,700

May 24

Purchases ……………………………………………………….

11,270

Accounts Payable

11,270

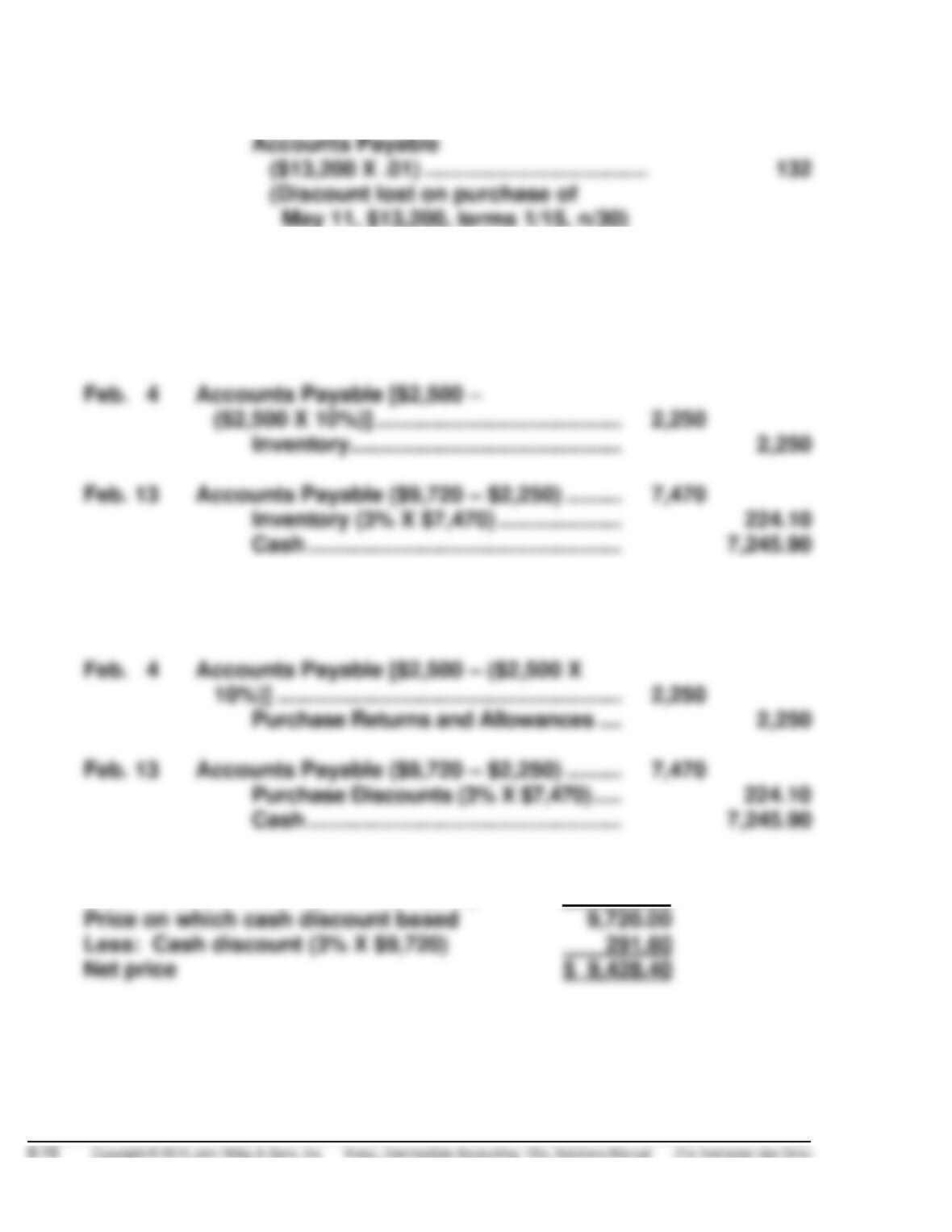

EXERCISE 8-7 (Continued)

(b)

May 31

Purchase Discounts Lost …………………………..

132

Accounts Payable

($13,200 X .01) ……………………………………………..

(Discount lost on purchase of

May 11, $13,200, terms 1/15, n/30)

EXERCISE 8-8 (20–25 minutes)

(a)

Feb. 1

Inventory [$10,800 – ($10,800 X 10%)] ………………………

9,720

Accounts Payable …………………………..

9,720

Inventory ……………………………………………………….

2,250

Feb. 13

Accounts Payable ($9,720 – $2,250) …………………………

7,470

Inventory (3% X $7,470) …………………………..

Cash ……………………………………………………….

(b)

Feb. 1

Purchases [$10,800 – ($10,800 X 10%)] …………………….

9,720

Accounts Payable …………………………..

9,720

Purchase Returns and Allowances ……………………….

2,250

Feb. 13

Accounts Payable ($9,720 – $2,250) …………………………

Purchase Discounts (3% X $7,470) ………………………..

Cash ……………………………………………………….

(c)

Purchase price (list)

$10,800.00

Less: Trade discount (10% X $10,800)

1,080.00

Price on which cash discount based

Less: Cash discount (3% X $9,720)

EXERCISE 8-9 (15–25 minutes)

(a)

Jan. 4

Accounts Receivable …………………………..

640

Sales Revenue(80 X $8) …………………………..

640

Jan. 11

Purchases ($150 X $6) …………………………..

900

Accounts Payable …………………………..

900

Jan. 13

Accounts Receivable …………………………..

1,050

Sales Revenue (120 X $8.75) …………………………..

Jan. 20

Purchases (160 X $7) …………………………..

1,120

Accounts Payable …………………………..

Jan. 27

Accounts Receivable …………………………..

900

Sales Revenue (100 X $9) …………………………..

900

Jan. 31

Inventory ($7 X 110) …………………………..

770

Cost of Goods Sold…………………………..

1,750*

Purchases ($900 + $1,120) …………………………..

2,020

Inventory (100 X $5) …………………………..

500

EXERCISE 8-9 (Continued)

(c)

Jan. 4

Accounts Receivable …………………………..

640

Sales Revenue (80 X $8) …………………………..

640

Cost of Goods Sold …………………………..

400

Inventory (80 X $5) …………………………..

400

Jan. 11

Inventory ……………………………………………………….

900

Accounts Payable (150 X $6) …………………………..

900

Jan. 13

Accounts Receivable …………………………..

1,050

Sales Revenue (120 X $8.75) …………………………..

Cost of Goods Sold …………………………..

700

Inventory ([(20 X $5) +

(100 X $6)] ……………………………………………………

700

Jan. 20

Inventory ……………………………………………………….

1,120

Accounts Payable (160 X $7) …………………………..

1,120

Jan. 27

Accounts Receivable …………………………..

900

Sales Revenue (100 X $9) …………………………..

Cost of Goods Sold …………………………..

650

Inventory [(50 X $6) +

(d)

Sales revenue