E5-11B (25–30 minutes)

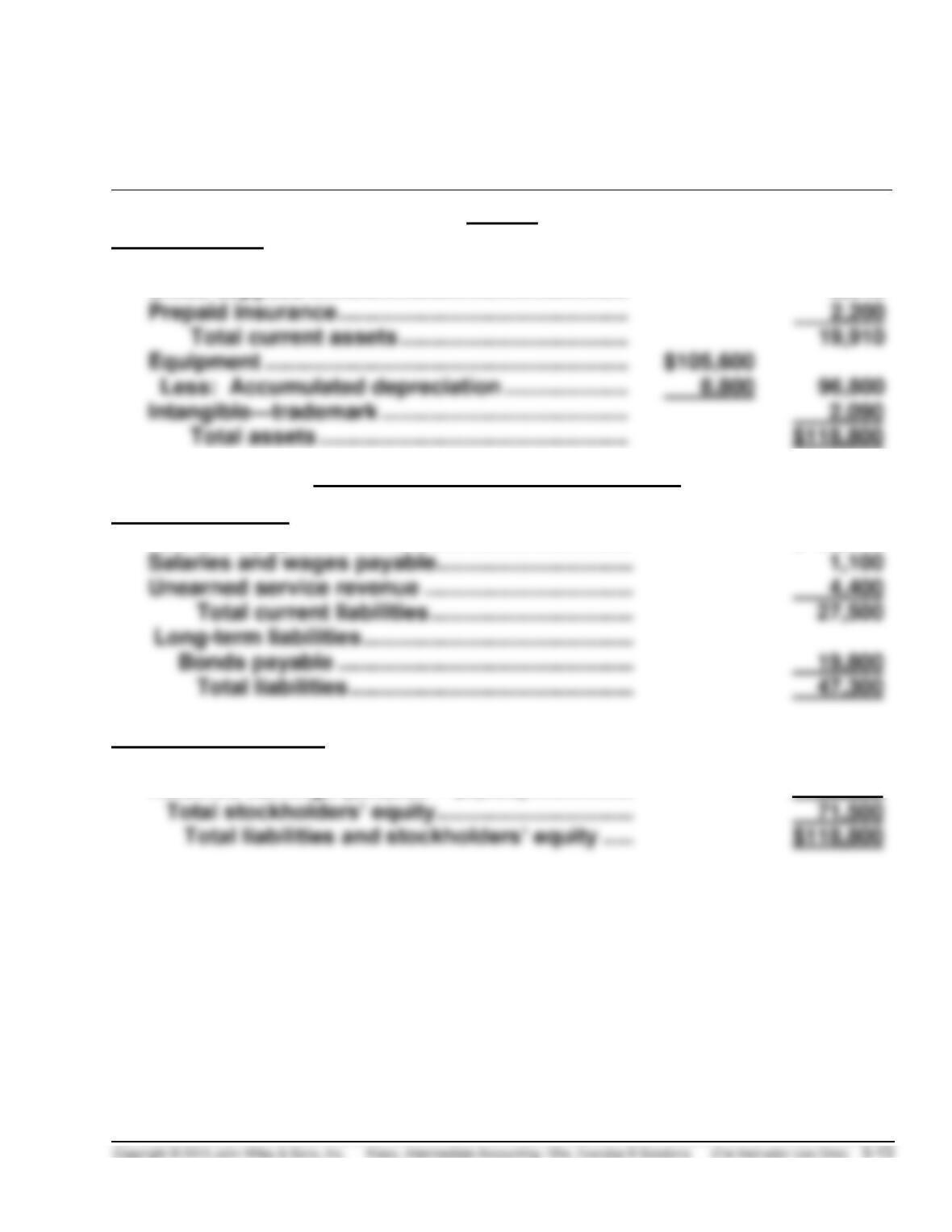

DE YOUNG CORPORATION

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ……………………………………………………………

$ 15,070

Office supplies …………………………………………….

2,640

Prepaid insurance ………………………………………..

2,200

Total current assets ……………………………….

Equipment …………………………………………………..

Less: Accumulated depreciation ………………..

Intangible—trademark ………………………………….

2,090

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………………………

$ 22,000

Salaries and wages payable …………………………..

Unearned service revenue …………………………….

4,400

Total current liabilities …………………………...

27,500

Long-term liabilities ……………………………………..

Bonds payable …………………………………………

19,800

Total liabilities ……………………………………….

47,300

Stockholders’ equity

Common stock ……………………………………………..

22,000

Retained earnings ($55,000 – $5,500) ……………..

49,500

Total stockholders’ equity …………………………..

71,500

E5-12B (30–35 minutes)

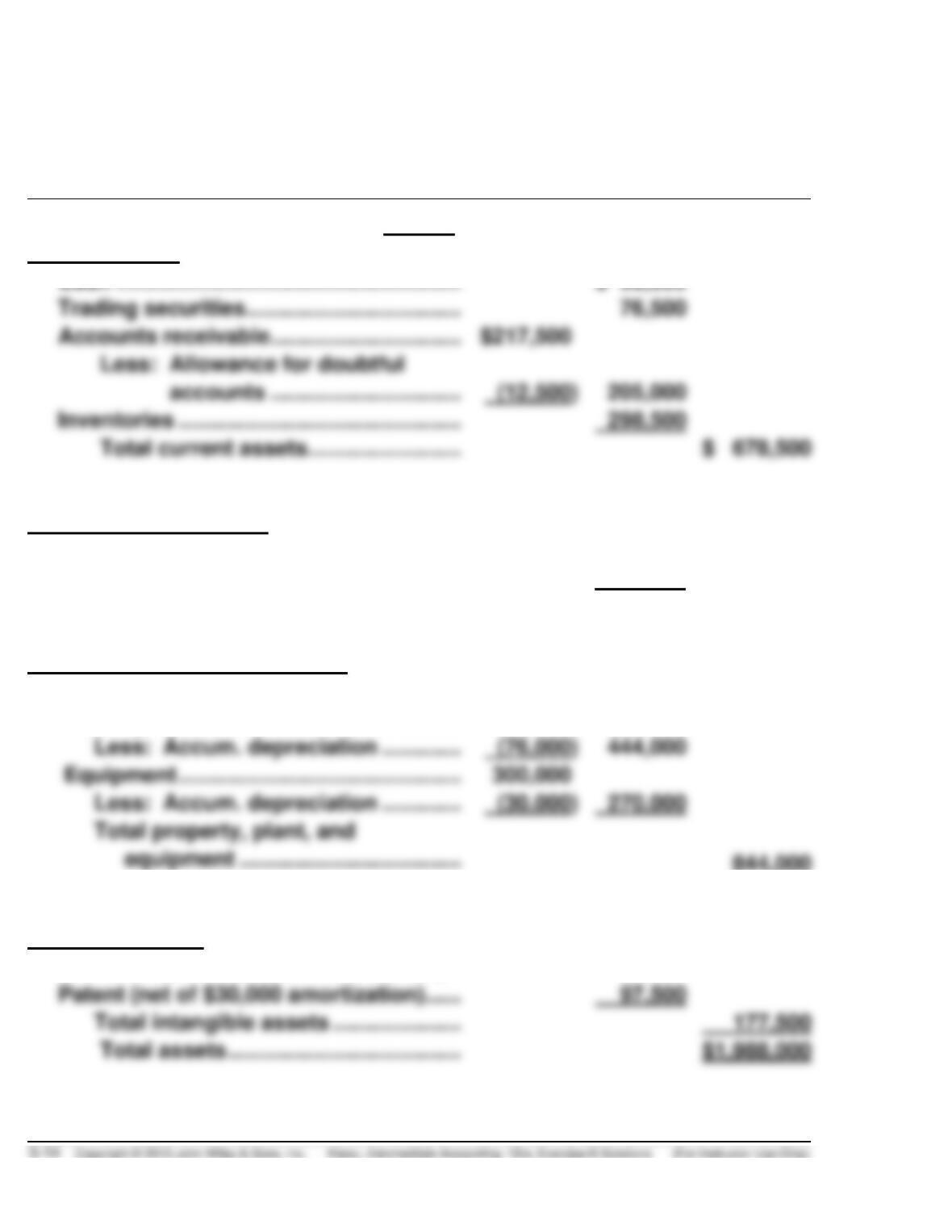

DO CORPORATION

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ………………………………………………..

$ 98,500

Trading securities ……………………………..

76,500

Accounts receivable ………………………….

Inventories ……………………………………….

298,500

Total current assets …………………….

Long-term investments

Investments in bonds ………………………..

149,500

Investments in stocks ……………………….

138,500

Total long-term investments ……….

288,000

Property, plant, and equipment

Land …………………………………………………

130,000

Building ……………………………………………

520,000

Less: Accum. depreciation ………….

444,000

Equipment ……………………………………….

Less: Accum. depreciation ………….

270,000

844,000

Intangible assets

Franchise (net of $80,000 amortization) …

80,000

Patent (net of $30,000 amortization)……

97,500

Total intangible assets …………………

Total assets ………………………………..

E5-12B (Continued)

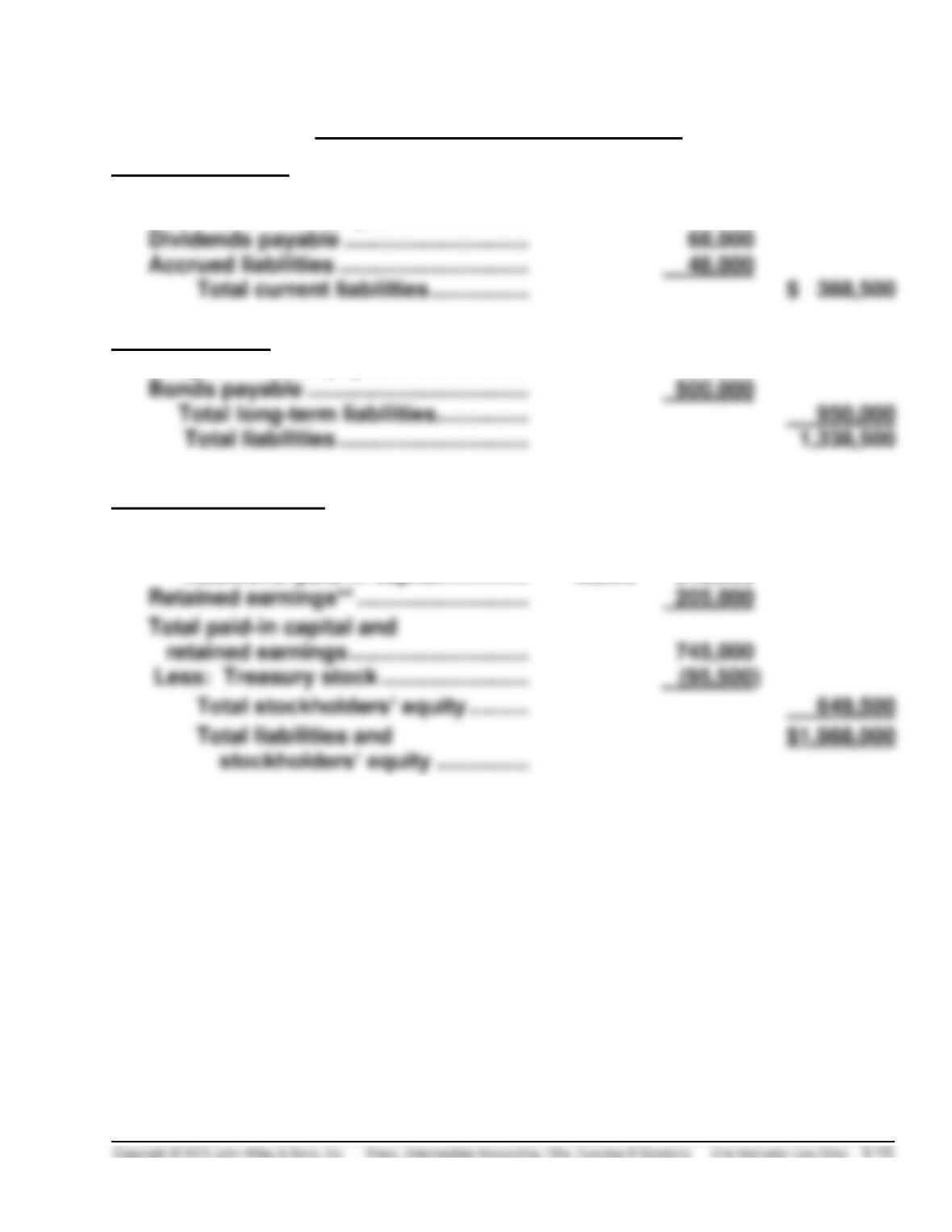

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ………………………….

$227,500

Short-term notes payable ……………….

45,000

Dividends payable …………………………

68,000

Accrued liabilities ………………………….

48,000

Total current liabilities …………….

Long-term debt

Long-term notes payable ……………….

450,000

Bonds payable ………………………………

Total long-term liabilities ……………

Stockholder’s equity

Paid-in capital

Common stock ($5 par) …………….

$500,000

Additional paid-in capital…………..

40,000

540,000

retained earnings ………………………..

745,000

Total stockholders’ equity ……….

(**Retained earnings computation is on the next page.)

E5-12B (Continued)

**Computation of Retained Earnings:

Sales ……………………………………………………………………….

$4,050,000

Investment revenue ………………………………………………….

31,500

Extraordinary gain ……………………………………………………

40,000

Cost of goods sold …………………………………………………..

Selling expenses ………………………………………………………

Administrative expenses …………………………………………..

Interest expense ………………………………………………………

(105,500)

Net income ………………………………………………………………

$ 166,000

Beginning retained earnings……………………………………..

$ 109,000

Prior period adjustment—depreciation error ………………

(70,000)

Beginning retained earnings, restated ……………………….

39,000

Net income ………………………………………………………………

166,000

Ending retained earnings ………………………………………….

$ 205,000

E5-13B (15–20 minutes)

(a)

1.

(f)

1.

(k)

5.

(d)

2.

(i)

3.

E5-14B (25–35 minutes)

DUONG INC.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………………

$ 88,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense …………………………….

Increase in accounts receivable ……………..

Increase in accounts payable …………………

16,000

Net cash provided by operating activities …….

Cash flows from investing activities

Purchase of equipment ……………………………….

Cash flows from financing activities

Issuance of common stock ………………………….

40,000

Payment of cash dividends ………………………….

(46,000)

Net cash used by financing activities ……………

Net increase in cash …………………………………………

Cash at beginning of year …………………………………

26,000

E5-15B (25–35 minutes)

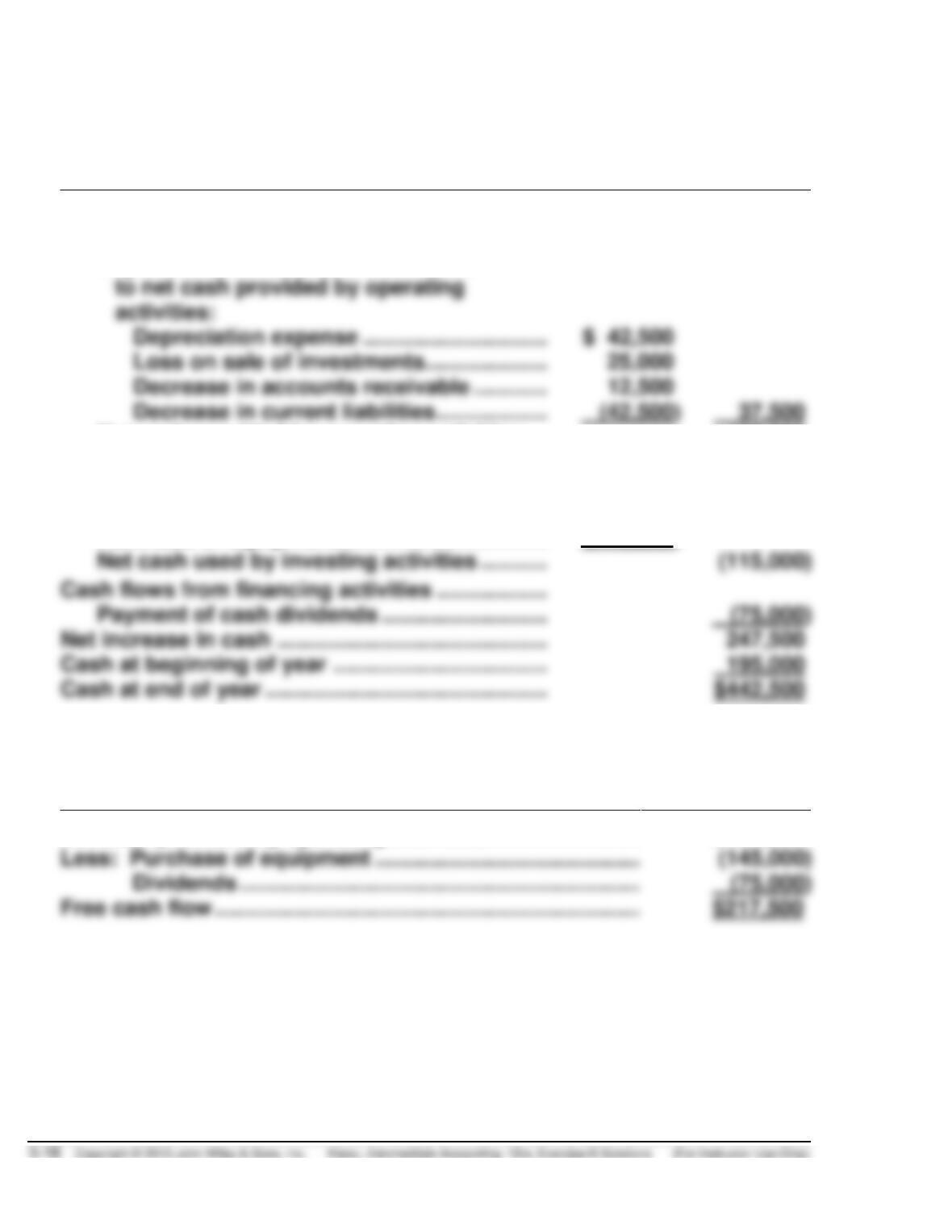

(a) GARCIA CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ………………………………………………

$400,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense …………………………

Loss on sale of investments………………..

Decrease in accounts receivable …………

Decrease in current liabilities ………………

(42,500)

37,500

Net cash provided by operating activities ….

437,500

Cash flows from investing activities……………….

Sale of investments

[($185,000 – $130,000) – $25,000] ……………

30,000

Purchase of equipment …………………………….

(145,000)

Cash flows from financing activities ………………

Payment of cash dividends ………………………

Cash at beginning of year ……………………………..

Cash at end of year ……………………………………….

(b)

Free Cash Flow Analysis

Net cash provided by operating activities …………………….

$437,500

Less: Purchase of equipment …………………………………….

Dividends ………………………………………………………..

E5-16B (25–35 minutes)

(a) GOKHALE CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………….

$187,500

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense ………………………..

Increase in accounts receivable …………

Decrease in inventory ………………………..

13,500

Decrease in accounts payable ……………

10,500

Net cash provided by operating activities…..

Cash flows from investing activities ……………..

Sale of land …………………………………………….

58,500

Purchase of equipment …………………………..

(90,000)

Net cash used by investing activities ……….

(31,500)

Cash flows from financing activities

Payment of cash dividends ……………………..

Net increase in cash …………………………………….

Cash at beginning of year …………………………….

33,000

The issuance of common stock to retire $75,000 of bonds payable is a

significant noncash financing transaction which would be disclosed in

notes accompanying the financial statements.

E5-16B (Continued)

(b) Current cash debt coverage ratio =

Cash debt coverage ratio =

Free Cash Flow Analysis

Net cash provided by operating activities …………………..

$198,000

Less: Purchase of equipment ……………………………………

(90,000)

Dividends ……………………………………………………….

E5-17B (25–35 minutes)

(a) GONZALVO CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………….

$66,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Loss on sale of equipment ……………………

Depreciation expense …………………………..

Patent amortization ………………………………

Increase in current liabilities …………………

15,600

Net cash provided by operating activities ……

Cash flows from investing activities

Sale of equipment ……………………………………..

12,000

Addition to building …………………………………..

(32,400)

Investment in stock……………………………………

(19,200)

Net cash used by investing activities ………….

(39,600)

Cash flows from financing activities

Issuance of bonds ……………………………………..

60,000

(36,000)

Purchase of treasury stock ………………………..

(13,200)

Net cash provided by financing activities ……

aAn additional proof to arrive at the increase in cash is provided as

follows:

Total current assets—end of period ……………..

$355,800

[from part (b)]

Total current assets—beginning of period …….

Increase in current assets during the period …

Increase in current assets other than cash ……

34,800

E5-17B (Continued)

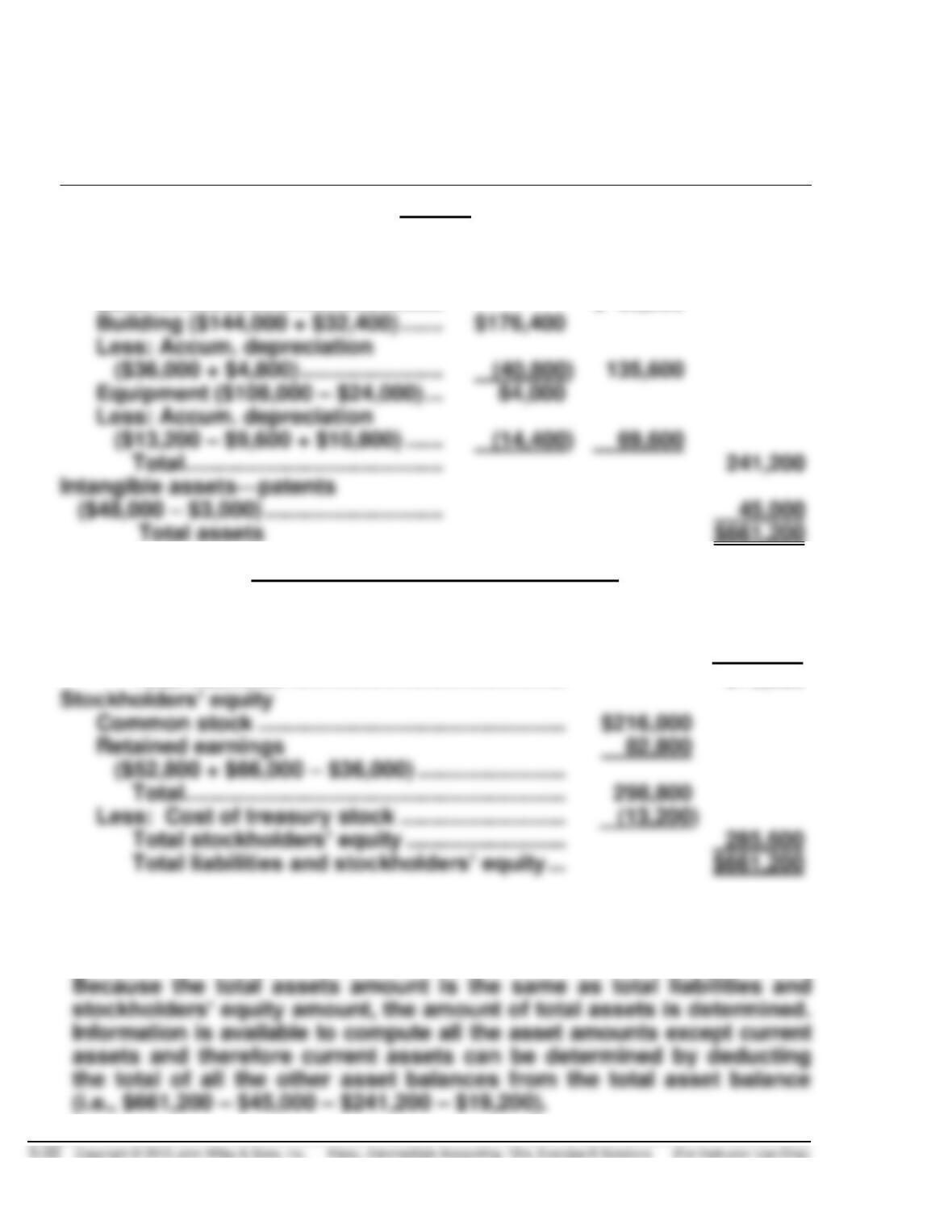

(b) GONZALVO CORPORATION

Balance Sheet

December 31, 2014

Assets

Current assets ……………………………….

$355,800b

Long-term investments …………………..

19,200

Property, plant, and equipment ……….

Land ………………………………………..

$ 36,000

Building ($144,000 + $32,400) …….

($36,000 + $4,800) …………………..

Equipment ($108,000 – $24,000) …

($13,200 – $9,600 + $10,800) ……

69,600

Total……………………………………

($48,000 – $3,000) ………………………..

Liabilities and Stockholders’ Equity

Current liabilities ($180,000 + $15,600) ……………

$195,600

Long-term liabilities

Bonds payable ($120,000 + $60,000) …………….

180,000

Total liabilities ………………………………………

375,600

Common stock …………………………..………………

($52,800 + $66,000 – $36,000) ……………………

Total……………………………………………………..

Less: Cost of treasury stock ………………………

(13,200)

Total stockholders’ equity ……………………..

285,600

b

The amount determined for current assets is computed last and is a

“plug” figure. That is, total liabilities and stockholders’ equity is

computed because information is available to determine this amount.

E5-18B (25 minutes)

(a) HARRISON CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………….

$62,500*

Adjustments to net income:

Depreciation expense ………………………….

$13,500

Increase in accounts receivable ……………

(8,000)

Decrease in inventory ………………………….

Decrease in accounts payable ……………..

Net cash provided by operating activities …..

Cash flows from investing activities………………..

Sale of land ………………………………………………

Purchase of building …………………………………

Net cash used by investing activities …………

Cash flows from financing activities ……………….

Payment of cash dividends ……………………….

(30,000)

Net increase in cash ………………………………………

Cash at beginning of year ………………………………

The issuance of common stock to convert $25,000 of bonds payable is a

significant noncash financing transaction which would be disclosed in

notes accompanying the financial statements.

*Beginning retained earnings + Net income – Dividends = Ending retained

earnings

E5-18B (Continued)

2014

2013

(b) Current ratio

$167,500

= 9.9

$138,500

= 5.9

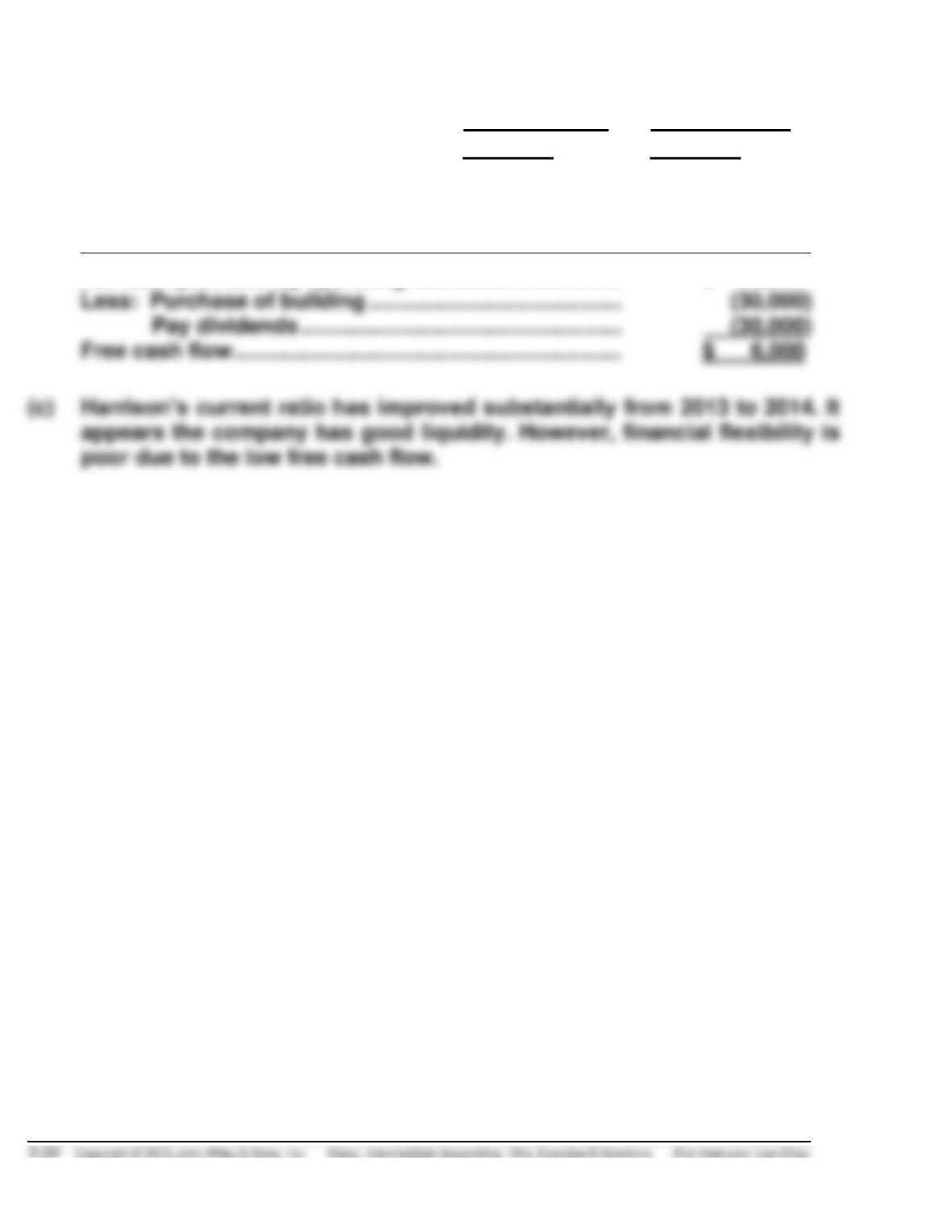

$ 17,000

$ 23,500

Free Cash Flow Analysis

Net cash provided by operating activities ………………………..

$ 66,000

Less: Purchase of building …………………………………………….