CHAPTER 6

Accounting and the Time Value of Money

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

1.

Present value concepts.

1, 2, 3, 4,

5, 9, 17

2.

Use of tables.

13, 14

8

1

3.

Present and future value

problems:

a. Unknown future amount.

7, 19

1, 5, 13

2, 3, 4, 7

b. Unknown payments.

10, 11, 12

6, 12,

15, 17

8, 16, 17

2, 6

c. Unknown number of

periods.

4, 9

10, 15

2

d. Unknown interest rate.

15, 18

3, 11, 16

9, 10, 11, 14

2, 7

e. Unknown present value.

8, 19

2, 7, 8,

10, 14

3, 4, 5, 6,

8, 12, 17,

18, 19

1, 4, 7, 9,

13, 14

4.

Value of a series of irregular

deposits; changing interest

rates.

3, 5, 8

5.

pensions, bonds; choice

between projects.

14, 15

10, 11, 12,

13, 14, 15

6.

Deferred annuity.

7.

Expected Cash Flows.

20, 21, 22

13, 14, 15

Valuation of leases,

6

15

7, 12, 13,

3, 5, 6, 8, 9,

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief

Exercises

Exercises

Problems

1. Identify accounting topics where the

time value of money is relevant.

1, 3, 17

2. Distinguish between simple and

compound interest.

1, 3, 4, 17,

2

3. Use appropriate compound interest

tables.

4, 5, 13, 14

1

4. Identify variables fundamental to

solving interest problems.

6, 7, 10,

11, 12

5. Solve future and present value of 1

problems.

2, 7, 8, 10,

11, 12

1, 2, 3,

4, 7, 8

2, 3, 6, 9,

10, 15

1, 2, 3, 5,

7, 9, 10

6. Solve future value of ordinary and

annuity due problems.

8, 9, 10,

11, 13

5, 6, 9, 13

3, 4, 6,

15, 16

2, 7

14, 16, 17

11, 12, 17,

18, 19

5, 7, 8, 9,

10, 13, 14

8. Solve present value problems related

to deferred annuities and bonds.

2, 12, 15,

7, 8, 13, 14

6, 11, 12,

value measurement.

20, 21, 22

13, 14, 15

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E6-1

Using interest tables.

Simple

5–10

E6-2

Simple and compound interest computations.

Simple

5–10

E6-3

Computation of future values and present values.

Simple

10–15

E6-4

Computation of future values and present values.

Moderate

15–20

E6-5

Computation of present value.

Simple

10–15

E6-6

Future value and present value problems.

Moderate

15–20

E6-7

Computation of bond prices.

Moderate

12–17

E6-8

Computations for a retirement fund.

Simple

10–15

E6-9

Unknown rate.

Moderate

5–10

E6–11

Evaluation of purchase options.

Moderate

10–15

E6–12

Analysis of alternatives.

Simple

10–15

E6–13

Computation of bond liability.

Moderate

15–20

E6–14

Computation of pension liability.

Moderate

15–20

E6–15

Investment decision.

Moderate

15–20

E6–16

Retirement of debt.

Simple

10–15

E6–17

Computation of amount of rentals.

Simple

10–15

E6–18

Least costly payoff.

Simple

10–15

E6–19

Least costly payoff.

Simple

10–15

E6–20

Expected cash flows.

Simple

5–10

E6–21

Expected cash flows and present value.

Moderate

15–20

P6-1

Various time value situations.

Moderate

15–20

P6-2

Various time value situations.

Moderate

15–20

P6-3

Analysis of alternatives.

Moderate

20–30

P6-4

Evaluating payment alternatives.

Moderate

20–30

P6-5

Analysis of alternatives.

Moderate

20–25

P6-6

Purchase price of a business.

Moderate

25–30

P6-7

Time value concepts applied to solve business problems.

Complex

30–35

P6-8

Analysis of alternatives.

Moderate

20–30

P6-9

Analysis of business problems.

Complex

30–35

P6–10

Analysis of lease vs. purchase.

Complex

30–35

P6–11

Pension funding.

Complex

25–30

P6–12

Pension funding.

Moderate

20–25

P6–13

Expected cash flows and present value.

Moderate

20–25

P6–14

Expected cash flows and present value.

Moderate

20–25

P6–15

Fair value estimate.

Complex

20–25

SOLUTIONS TO CODIFICATION EXERCISES

CE6-1

(a) According to the Master Glossary, present value is a tool used to link uncertain future amounts

(cash flows or values) to a present amount using a discount rate (an application of the income

(c) Other codification references to present value are at (1) FASB ASC 820-10–35–33 and (2) FASB

ASC 820-10–55–55-4. Details for these references follow.

1. 820 Fair Value Measurements and Disclosures > 10 Overall > 35 Subsequent Measurement

35–33 Those valuation techniques include the following:

a. Present value techniques

2. 820 Fair Value Measurements and Disclosures > 10 Overall > 55 Implementation General,

paragraph 55-4 >>> Present Value Techniques

55-4 FASB Concepts Statement No. 7, Using Cash Flow Information and Present Value in

Accounting Measurements, provides guidance for using present value techniques to

measure fair value. That guidance focuses on a traditional or discount rate adjustment

CE6-2

Answers will vary. By entering the phrase “present value” in the search window, a list of references to

the term is provided. The site allows you to narrow the search to assets, liabilities, revenues, and

expenses.

CE6-2 (Continued)

50-1 The changes in the carrying amount of goodwill during the period shall be disclosed, including

the following (see Example 3 [paragraph 350-20–55-24]):

a. The aggregate amount of goodwill acquired.

50-2 For each goodwill impairment loss recognized, all of the following information shall be dis–

closed in the notes to the financial statements that include the period in which the impair–

ment loss is recognized:

a. A description of the facts and circumstances leading to the impairment.

(b) Liability reference: 410 Asset Retirement and Environmental Obligations > 20 Asset Retirement

Obligations > 30 Initial Measurement

Determination of a Reasonable Estimate of Fair Value

30-1 An expected present value technique will usually be the only appropriate technique with which

to estimate the fair value of a liability for an asset retirement obligation. An entity, when

using that technique, shall discount the expected cash flows using a credit-adjusted risk-free

rate. Thus, the effect of an entity’s credit standing is reflected in the discount rate rather

CE6-2 (Continued)

(c) Revenue or Expense reference: 720 Other Expenses> 25 Contributions Made> 30 Initial Measurement

30-1 Contributions made shall be measured at the fair values of the assets given or, if made in

30-2 Unconditional promises to give that are expected to be paid in less than one year may

CE6-3

Interest cost includes interest recognized on obligations having explicit interest rates, interest imputed

05-1 This Subtopic addresses the imputation of interest.

05-2 Business transactions often involve the exchange of cash or property, goods, or services for a

note or similar instrument. When a note is exchanged for property, goods, or services in a

bargained transaction entered into at arm’s length, there should be a general presumption that

05-3 This Subtopic provides guidance for the appropriate accounting when the face amount of a note

does not reasonably represent the present value of the consideration given or received in the

exchange. This circumstance may arise if the note is non-interest-bearing or has a stated

interest rate that is different from the rate of interest appropriate for the debt at the date of the

ANSWERS TO QUESTIONS

1. Money has value because with it one can acquire assets and services and discharge obligations.

The holding, borrowing or lending of money can result in costs or earnings. And the longer the

time period involved, the greater the costs or the earnings. The cost or earning of money as a

function of time is the time value of money.

2. Some situations in which present value measures are used in accounting include:

(a) Notes receivable and payable—these involve single sums (the face amounts) and may

involve annuities, if there are periodic interest payments.

(b) Leases—involve measurement of assets and obligations, which are based on the present value

of annuities (lease payments) and single sums (if there are residual values to be paid at the

conclusion of the lease).

3. Interest is the payment for the use of money. It may represent a cost or earnings depending upon

whether the money is being borrowed or loaned. The earning or incurring of interest is a function

of the time, the amount of money, and the risk involved (reflected in the interest rate).

4. The interest rate generally has three components:

(a) Pure rate of interest—This would be the amount a lender would charge if there were no

possibilities of default and no expectation of inflation.

(b) Expected inflation rate of interest—Lenders recognize that in an inflationary economy, they

5. (a) Present value of an ordinary annuity at 8% for 10 periods (Table 6-4).

(b) Future value of 1 at 8% for 10 periods (Table 6-1).

Questions Chapter 6 (Continued)

6. He should choose quarterly compounding, because the balance in the account on which interest

will be earned will be increased more frequently, thereby resulting in more interest earned on the

investment. This is shown in the following calculation:

7. $26,898 = $20,000 X 1.34489 (future value of 1 at 21/2% for 12 periods).

9. An annuity involves (1) periodic payments or receipts, called rents, (2) of the same amount,

(3) spread over equal intervals, (4) with interest compounded once each interval.

10.

Amount paid each year =

11.

Amount deposited each year =

$200,000

(future value of an ordinary annuity at 10% for

4 years).

4.64100

Amount deposited each year = $43,094.

13. The process for computing the future value of an annuity due using the future value of an ordinary

annuity interest table is to multiply the corresponding future value of the ordinary annuity by one

plus the interest rate. For example, the factor for the future value of an annuity due for 4 years at

12% is equal to the factor for the future value of an ordinary annuity times 1.12.

Questions Chapter 6 (Continued)

15. Present value = present value of an ordinary annuity of $25,000 for 20 periods at? percent.

16. 4.96764 Present value of ordinary annuity at 12% for eight periods.

(2.40183) Present value of ordinary annuity at 12% for three periods.

2.56581 Present value of ordinary annuity at 12% for eight periods, deferred three periods.

18. $27,600 = PV of an ordinary annuity of $6,900 for five periods at? percent.

19. The IRS argues that the future reserves should be discounted to present value. The result would

be smaller reserves and therefore less of a charge to income. As a result, income would be higher

and income taxes may therefore be higher as well.

SOLUTIONS TO BRIEF EXERCISES

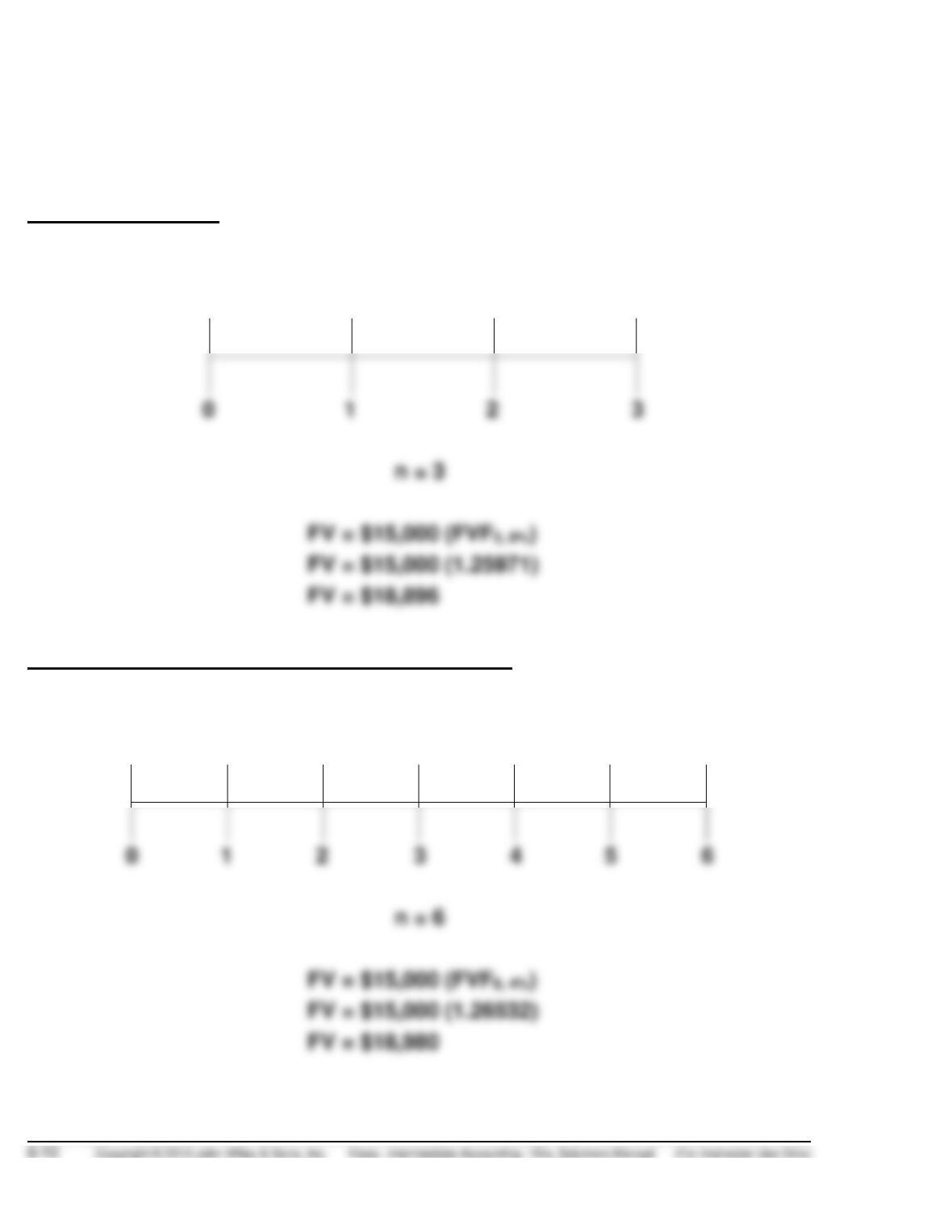

BRIEF EXERCISE 6-1

8% annual interest

i = 8%

PV = $15,000 FV = ?

8% annual interest, compounded semiannually

i = 4%

PV = $15,000 FV = ?

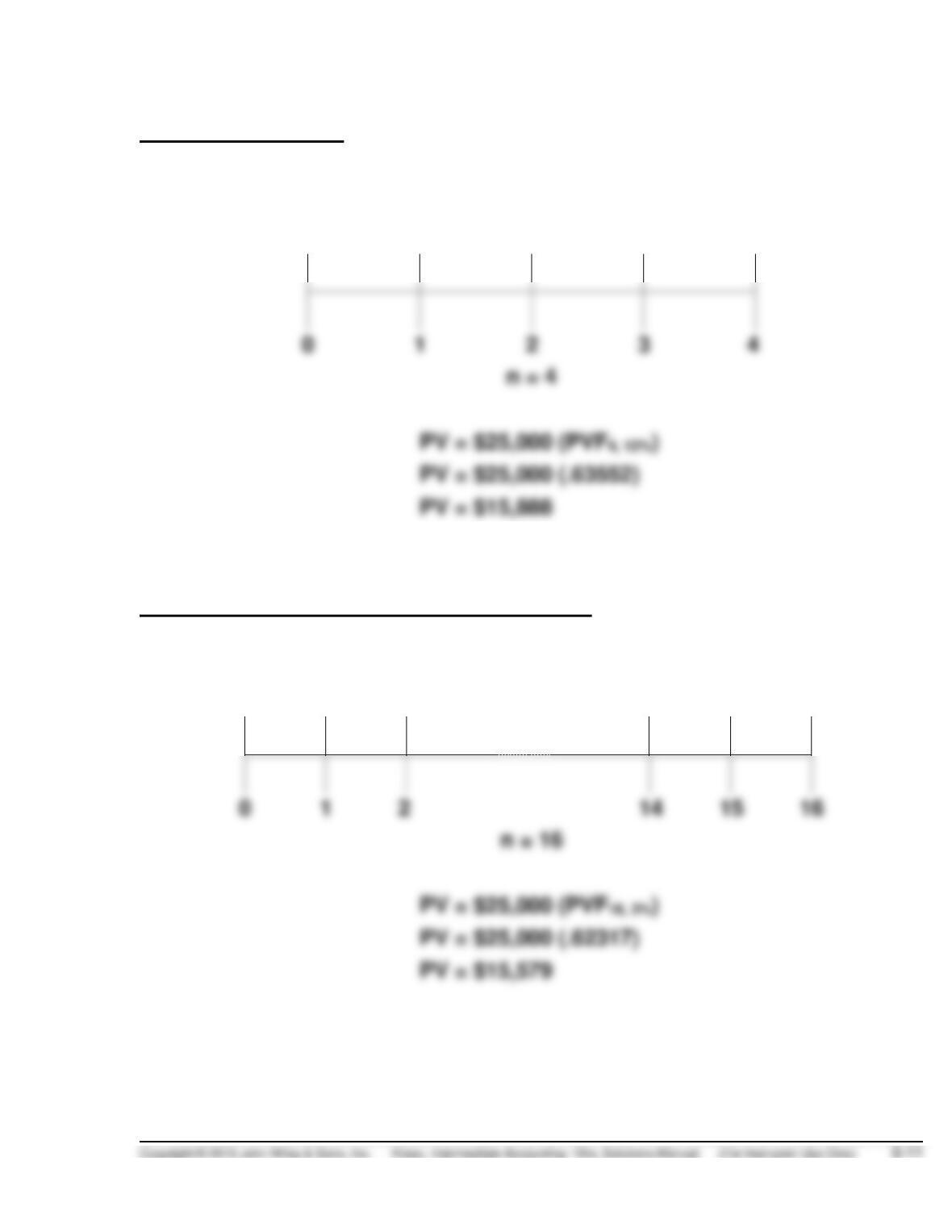

BRIEF EXERCISE 6-2

12% annual interest

i = 12%

PV = ? FV = $25,000

12% annual interest, compounded quarterly

i = 3%

PV = ? FV = $25,000

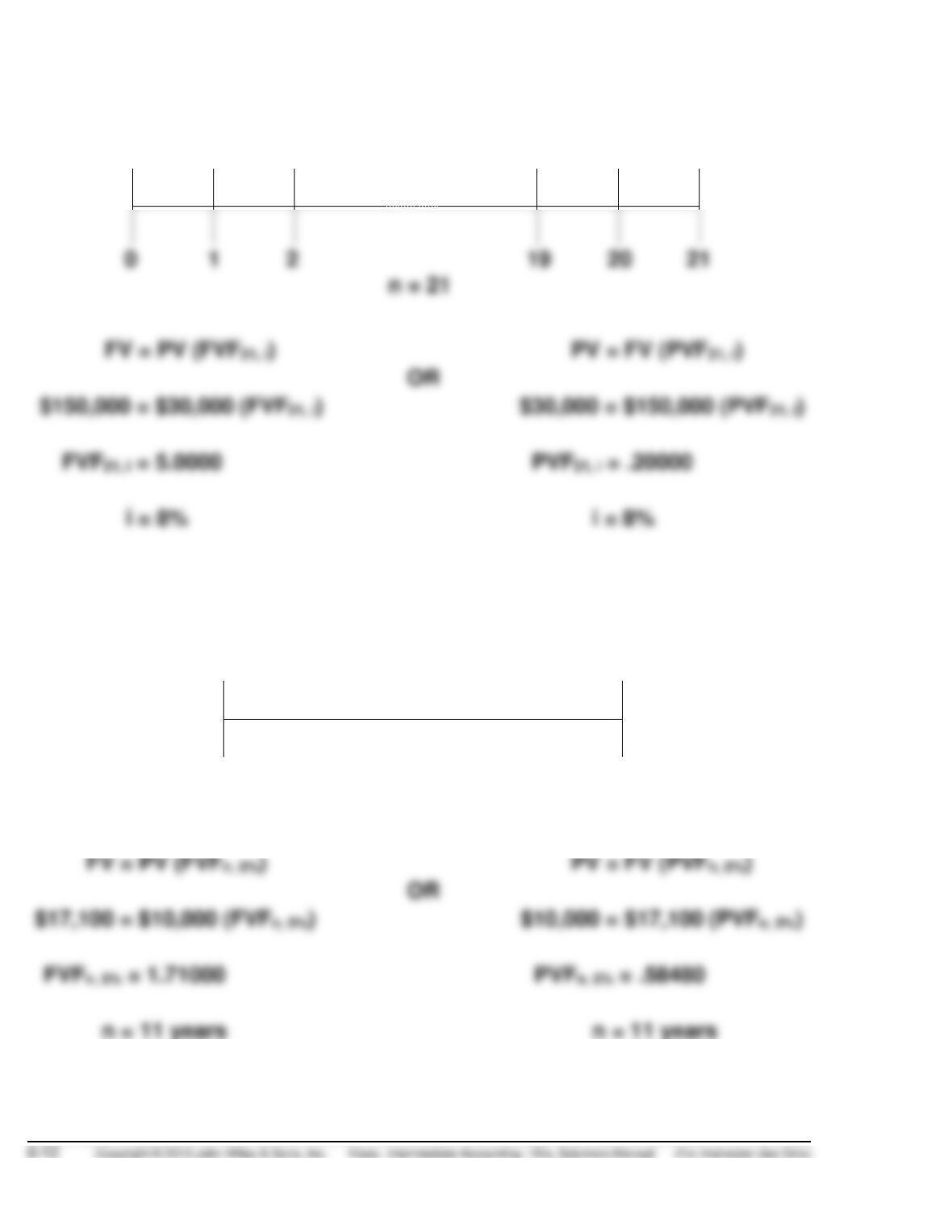

BRIEF EXERCISE 6-3

i = ?

PV = $30,000 FV = $150,000

2

20 21

PV = FV (PVF21, i)

$30,000 = $150,000 (PVF21, i)

FVF21, i = 5.0000

PVF21, i = .20000

i = 8%

i = 8%

BRIEF EXERCISE 6-4

i = 5%

PV = $10,000 FV = $17,100

0

?

n = ?

PV = FV (PVFn, 5%)

$17,100 = $10,000 (FVFn, 5%)

n = 11 years

n = 11 years

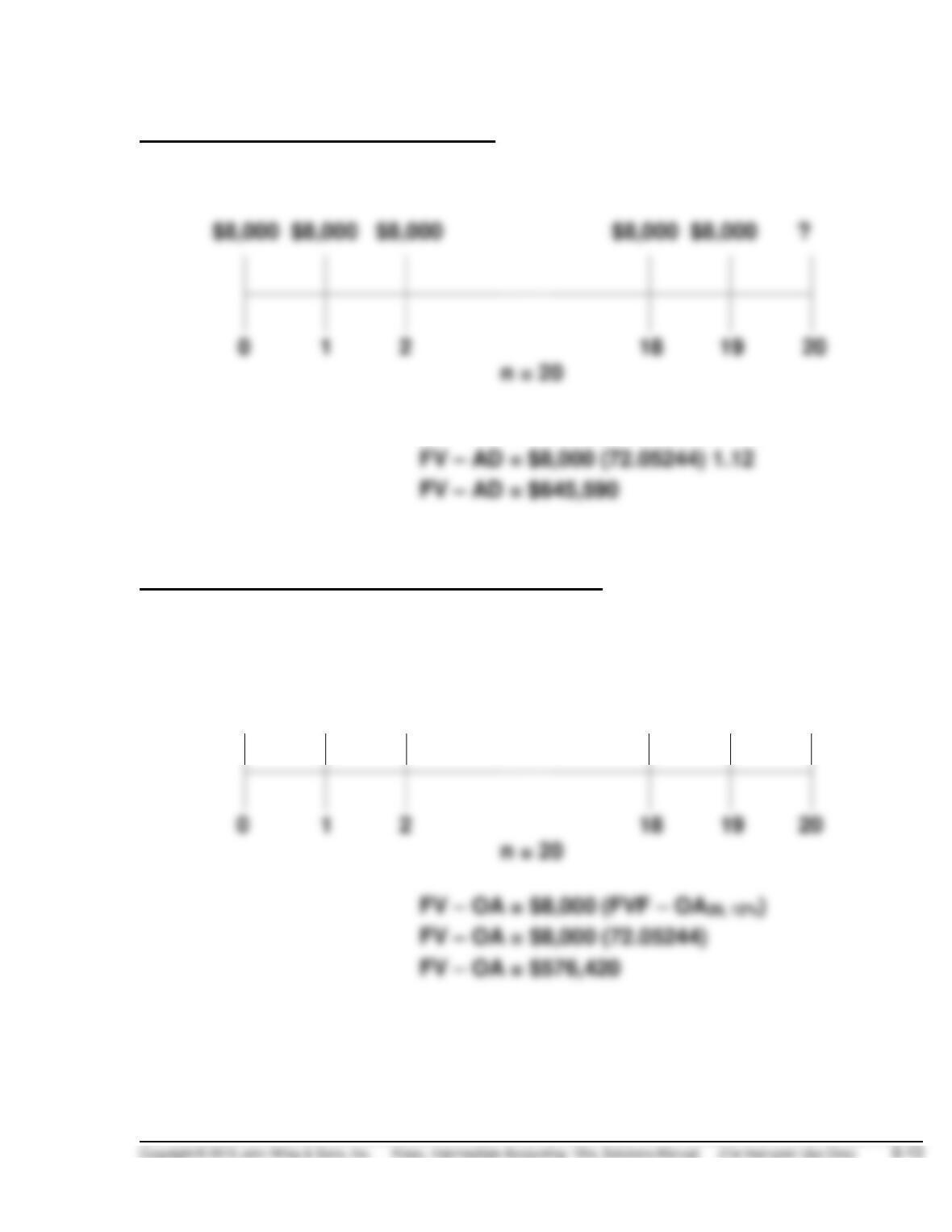

BRIEF EXERCISE 6-5

First payment today (Annuity Due)

i = 12%

R = FV – AD =

FV – AD = $8,000 (FVF – OA20, 12%) 1.12

First payment at year-end (Ordinary Annuity)

i = 12%

FV – OA =

?

$8,000 $8,000 $8,000 $8,000 $8,000

BRIEF EXERCISE 6-6

i = 11%

FV – OA =

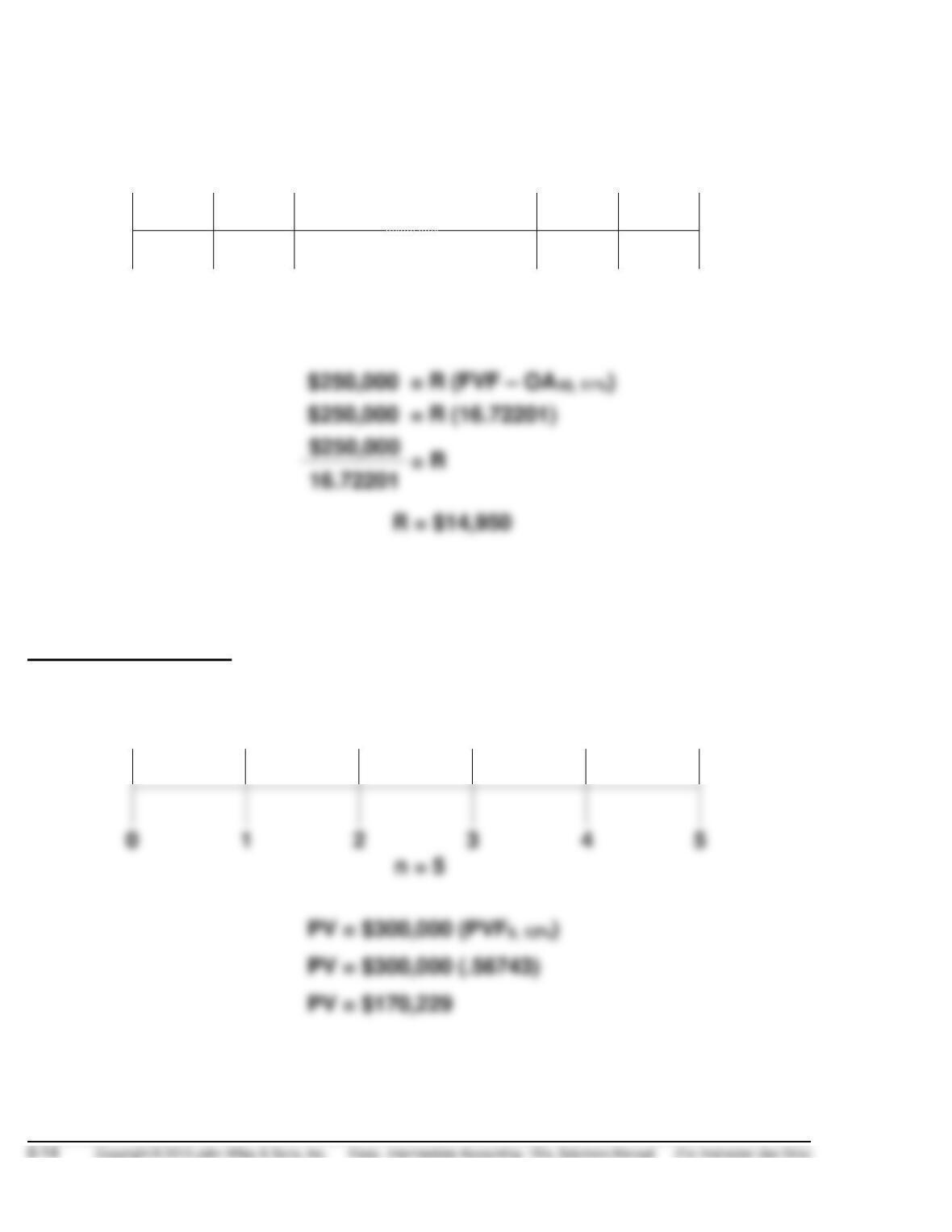

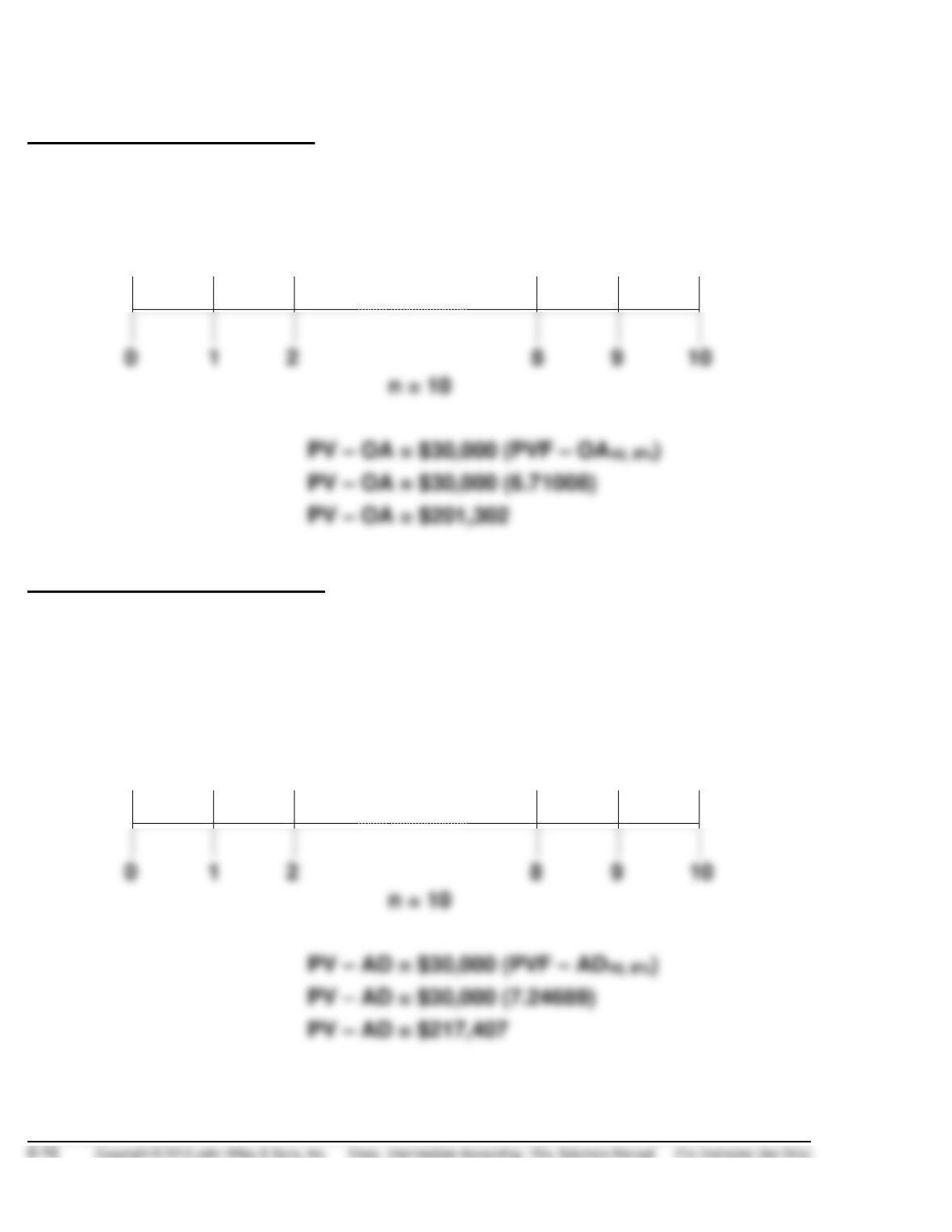

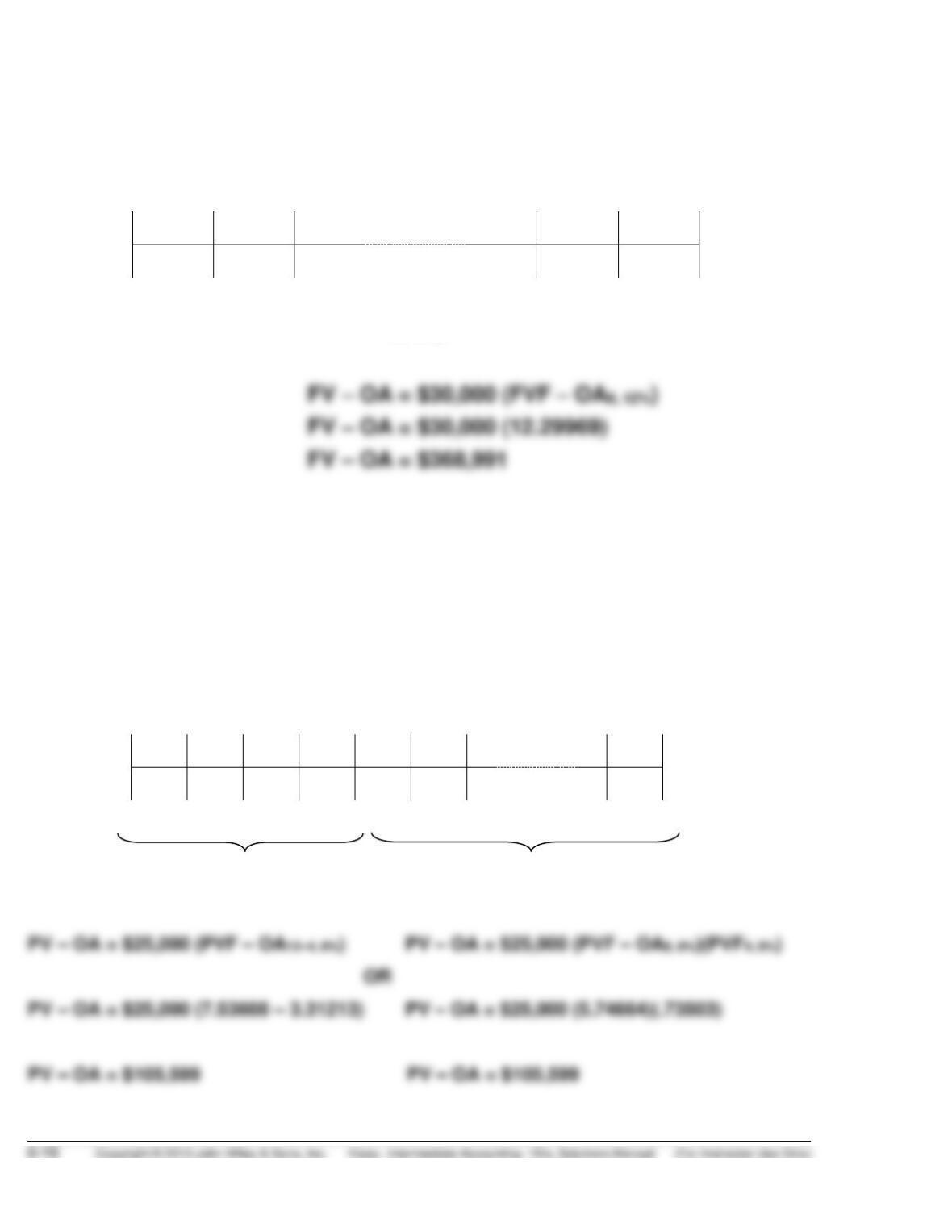

R = ? ? ? ? $250,000

0

1

2

8

9 10

n = 10

BRIEF EXERCISE 6-7

12% annual interest

i = 12%

PV = ? FV = $300,000

0

1

2

4 5

BRIEF EXERCISE 6-8

With quarterly compounding, there will be 20 quarterly compounding periods,

at 1/4 the interest rate:

BRIEF EXERCISE 6-9

i = 10%

FV – OA =

R = $100,000

$16,380 $16,380 $16,380

BRIEF EXERCISE 6-10

First withdrawal at year-end

i = 8%

PV – OA = R =

? $30,000 $30,000 $30,000 $30,000 $30,000

First withdrawal immediately

i = 8%

PV – AD =

?

R =

$30,000 $30,000 $30,000 $30,000 $30,000

BRIEF EXERCISE 6-11

i = ?

PV = R =

$793.15 $75 $75 $75 $75 $75

BRIEF EXERCISE 6-12

i = 8%

PV =

$300,000 R = ? ? ? ? ?

BRIEF EXERCISE 6-13

i = 12%

R =

$30,000 $30,000 $30,000 $30,000 $30,000

12/31/11

12/31/12

12/31/13

12/31/17

12/31/18 12/31/19

n = 8

BRIEF EXERCISE 6-14

i = 8%

PV – OA = R =

? $25,000 $25,000 $25,000 $25,000

0

1

2

3

4

5

6

11

12

n = 4 n = 8

BRIEF EXERCISE 6-15

i = 8%

PV = ?

PV – OA = R = $2,000,000

? $140,000 $140,000 $140,000 $140,000 $140,000

BRIEF EXERCISE 6-16

PV – OA = $20,000

$4,727.53 $4,727.53 $4,727.53 $4,727.53

BRIEF EXERCISE 6-17

PV – AD = $20,000

$? $? $? $?

0

1

2

5 6