SOLUTIONS TO PROBLEMS

PROBLEM 24-1

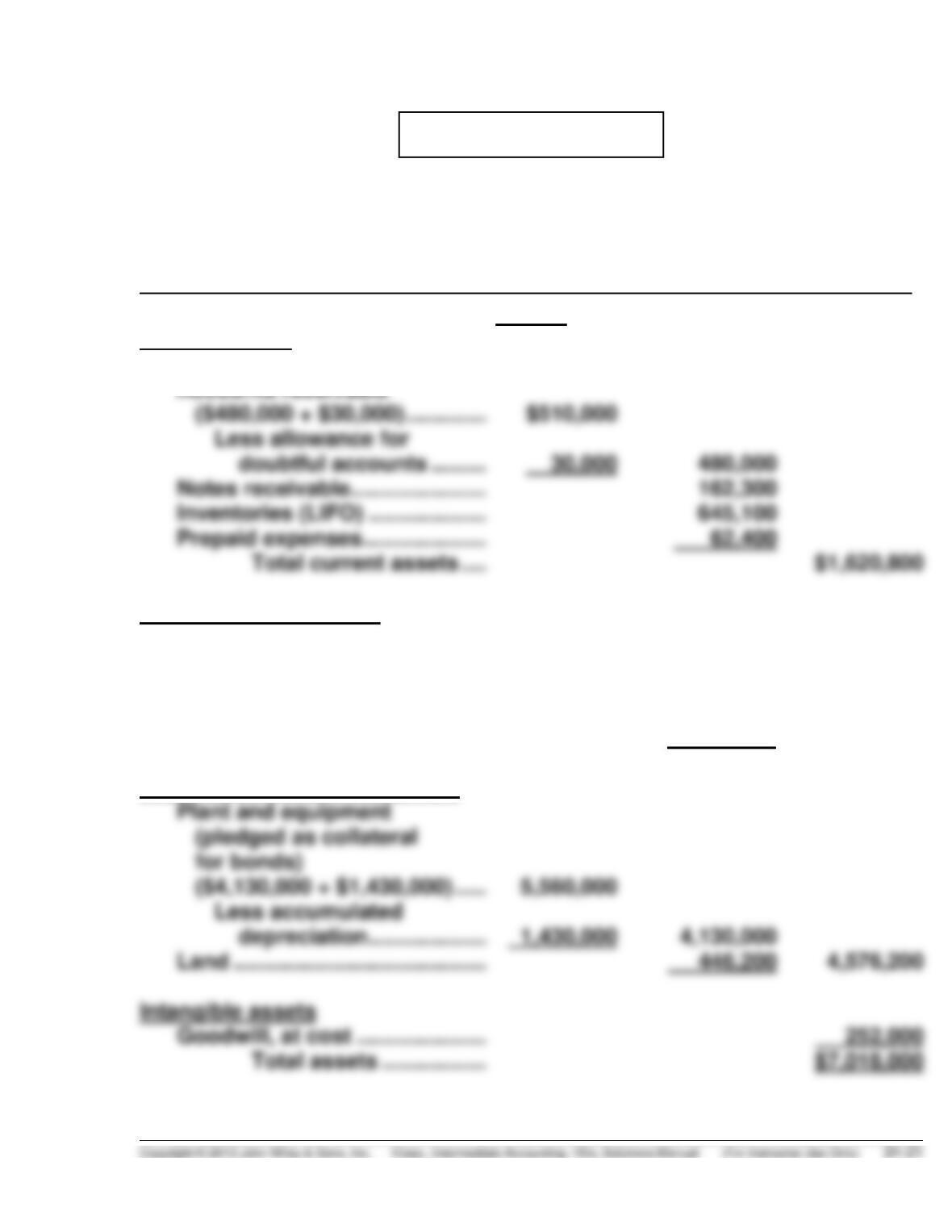

ALMADEN CORPORATION

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ($571,000 – $300,000) …. $ 271,000

Long-term investments

Investments in land …………….. 185,000

Cash surrender value of

life insurance policy …………. 84,000

Cash restricted for plant

expansion ……………………….. 300,000 569,000

Property, plant, and equipment

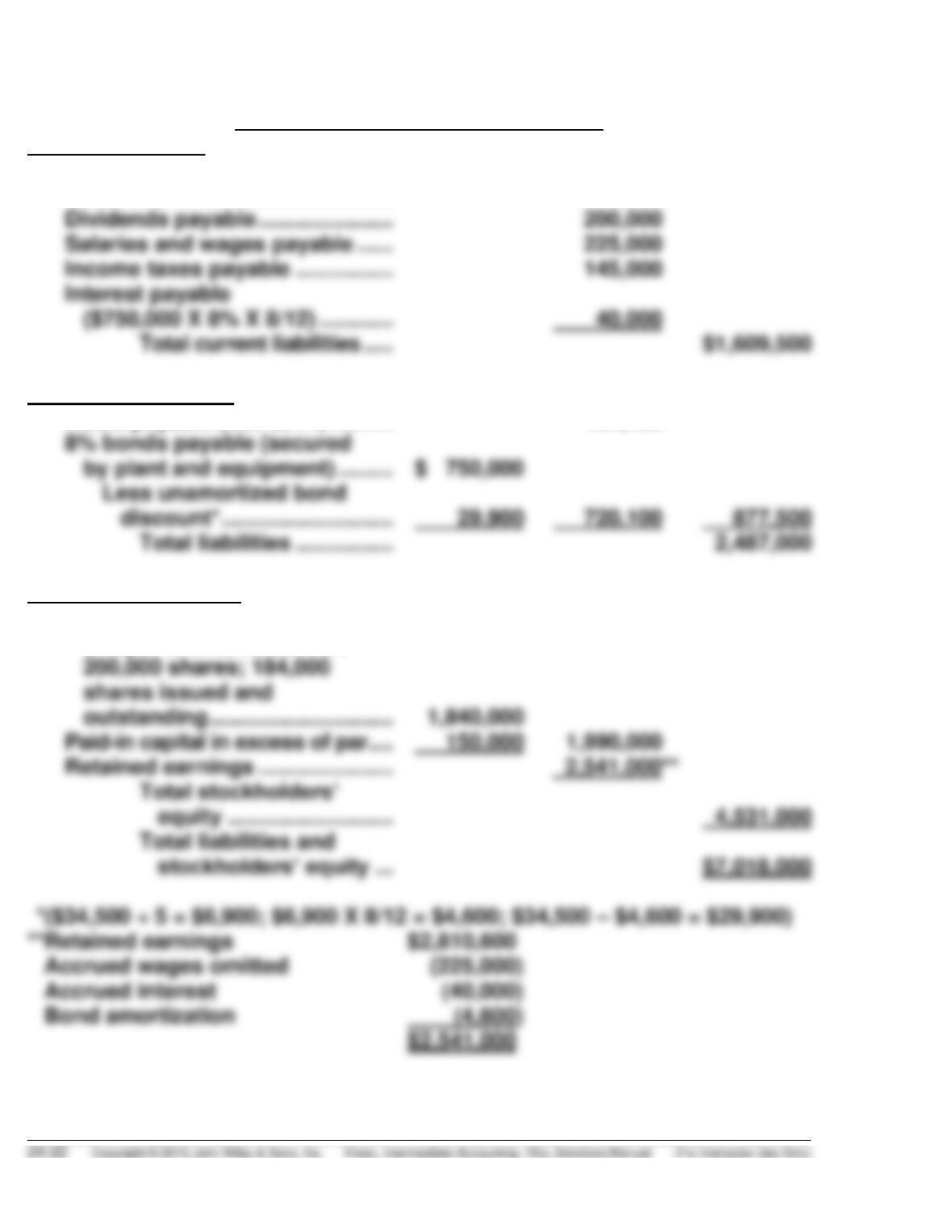

PROBLEM 24-1 (Continued)

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ………………….. $ 510,000

Unearned revenue …………………. 489,500

Long-term liabilities

Notes payable (due 2017) ………. 157,400

Stockholders’ equity

Common stock, par value

$10 per share; authorized

PROBLEM 24-1 (Continued)

Additional comments:

1. The information related to the competitor should be disclosed because

this innovation may have a significant effect on the company. The value

of the inventory is overstated because of the need to reduce selling

prices. This factor along with the net realizable value of the inventory

should be disclosed.

5. The fact that the gain on sale of certain plant assets was credited directly

to retained earnings has no effect on the balance sheet presentation.

6. Technically, the plant and equipment account should be separately dis-

closed and depreciation computed on each item individually. However,

the information to divide the accounts was not given in this problem.

7. Interest payable on the bonds ($750,000 X 8% X 8/12 = $40,000) was

8. Since the loss from heavy damage was caused by a fire after the balance

sheet date, this event does not reflect conditions existing at that date.

PROBLEM 24-2

(a) Determination of reportable segments:

1. Revenue test: 10% X $785,000* = $78,500. Only Segment C ($580,000)

meets this test.

(b) Disclosures required by GAAP:

A

B

C

Other

Totals

External Revenues

$40,000

$ 55,000

$480,000

$ 90,000

$665,000

Intersegment Revenues

20,000

100,000

120,000

Total Revenues

75,000

580,000

90,000

Cost of Goods Sold

Operating Expenses

40,000

235,000

30,000

Total Expenses

90,000

505,000

79,000

Operating Profit (Loss)

Identifiable Assets

Reconciliation of revenues

Total segment revenues ……………………………………………….. $785,000

PROBLEM 24-2 (Continued)

Reconciliation of profit or loss

Total segment operating profit ……………………………………… $ 82,000

Profits of immaterial segments ……………………………………… (11,000)

*PROBLEM 24-3

(a) BRADBURN CORPORATION

Ratio Analysis

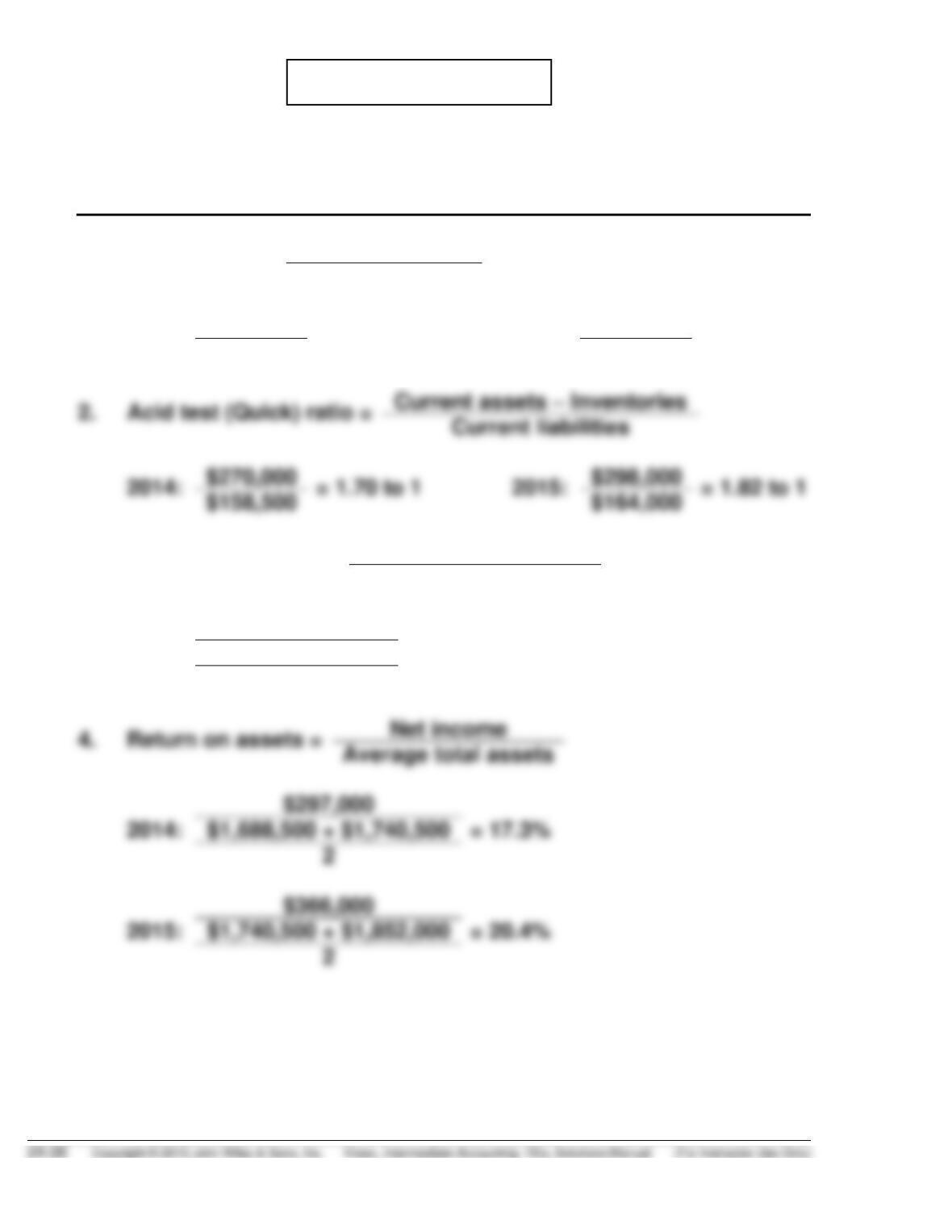

1.

Current ratio =

Current assets

Current liabilities

2014:

$320,000

= 2.02 to 1

2015:

$403,000

= 2.46 to 1

$158,500

$164,000

2.

Acid test (Quick) ratio =

$270,000

$298,000

$158,500

$164,000

3.

Inventory turnover =

Cost of goods sold

Average inventory

$1,530,000

2015:

$50,000 + $105,000

= 19.7 times (every 18.5 days)

2

= 17.3%

2015:

= 20.4%

*PROBLEM 24-3 (Continued)

5.

Percent Changes

Amounts

Percent Increase

(000s omitted)

2015

2014

(b) Other financial reports and financial analyses which might be helpful

to the commercial loan officer of Topeka National Bank include:

1. The Statement of Cash Flows would highlight the amount of cash

provided by operating activities, the other sources of cash, and the

(c) Bradburn Corporation should be able to finance the plant expansion

from internally generated funds as shown in the calculations presented

on the next page.

*PROBLEM 24-3 (Continued)

(000 omitted)

2015

2016

2017

Sales revenue

$3,000.0

$3,333.3

$3,703.6

Cost of goods sold

1,530.0

1,642.8

1,763.8

Gross margin

1,470.0

1,690.5

1,939.8

Operating expenses

860.0

Income before income taxes

Income taxes (40%)

244.0

Net income

$ 366.0

Add: Depreciation

Deduct: Dividends

Note repayment

(6.0)

Funds available for plant expansion

Plant expansion

Excess funds

$ 131.9

$ 229.1

Assumptions:

Sales revenue increases at a rate

of 11.11%.

Cost of goods sold increases at rate

Depreciation remains constant at

$102,500.

Dividends remain at $2 per share.

(d) Topeka National Bank should probably grant the extension of the loan,

if it is really required, because the projected cash flows for 2016 and

2017 indicate that an adequate amount of cash will be generated from

*PROBLEM 24-4

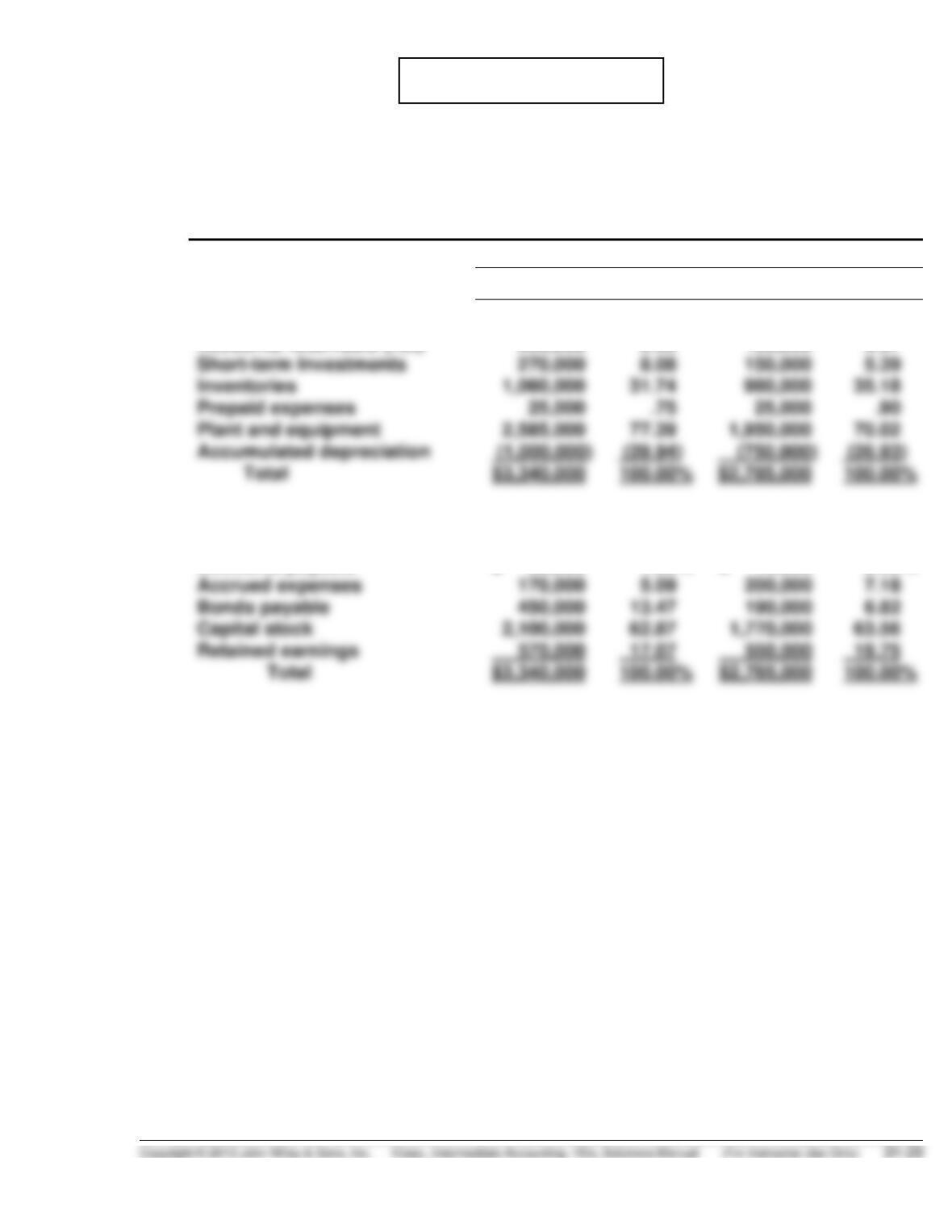

(a) GILMOUR COMPANY

Comparative Balance Sheet

December 31, 2015 and 2014

December 31

Assets

2015

2014

Cash

$ 180,000

5.39%

$ 275,000

9.87%

Accounts receivable (net)

220,000

6.59

155,000

5.57

Short-term Investments

270,000

8.08

150,000

5.39

Inventories

31.74

980,000

35.18

Prepaid expenses

.75

.90

Plant and equipment

77.39

70.02

Accumulated depreciation

(1,000,000)

(29.94)

(26.93)

Total

100.00%

Liabilities and

Stockholders’ Equity

Accounts payable

$ 50,000

1.50%

$ 75,000

2.69%

Accrued expenses

170,000

5.09

7.18

Bonds payable

450,000

13.47

6.82

Capital stock

62.87

63.56

Retained earnings

Total

100.00%

*PROBLEM 24-4 (Continued)

(b) GILMOUR COMPANY

Comparative Balance Sheet

December 31, 2015 and 2014

December 31

Increase or (Decrease)

Assets

2015

2014

$ Change

% Change

Cash

$ 180,000

$ 275,000

$ (95,000)

(34.55)

Accounts receivable (net)

220,000

155,000

65,000

41.94

Investments

270,000

150,000

80.00

Inventories

980,000

80,000

8.16

Prepaid expenses

0

Plant and equipment

32.56

Accumulated depreciation

33.33

Total

$ 3,340,000

$2,785,000

19.93%

Liabilities and

Stockholders’ Equity

Accounts payable

$ 50,000

$ 75,000

$ (25,000)

(33.33)

Accrued expenses

200,000

(15.00)

Bonds payable

190,000

136.84

Capital stock

18.64

Retained earnings

3.64

Total

$3,340,000

$2,785,000

$555,000

19.93%

(c) The component percentage (common-size) balance sheet makes easier

analysis possible. It actually reduces total assets and total liabilities

and stockholders’ equity to a common base. Thus, the statement is

simplified into figures that can be more readily grasped. It can also

possible improvements could be made.

(d) A statement such as that in part (b) is a good analysis and breakdown

of the total change in assets and liabilities and stockholders’ equity.

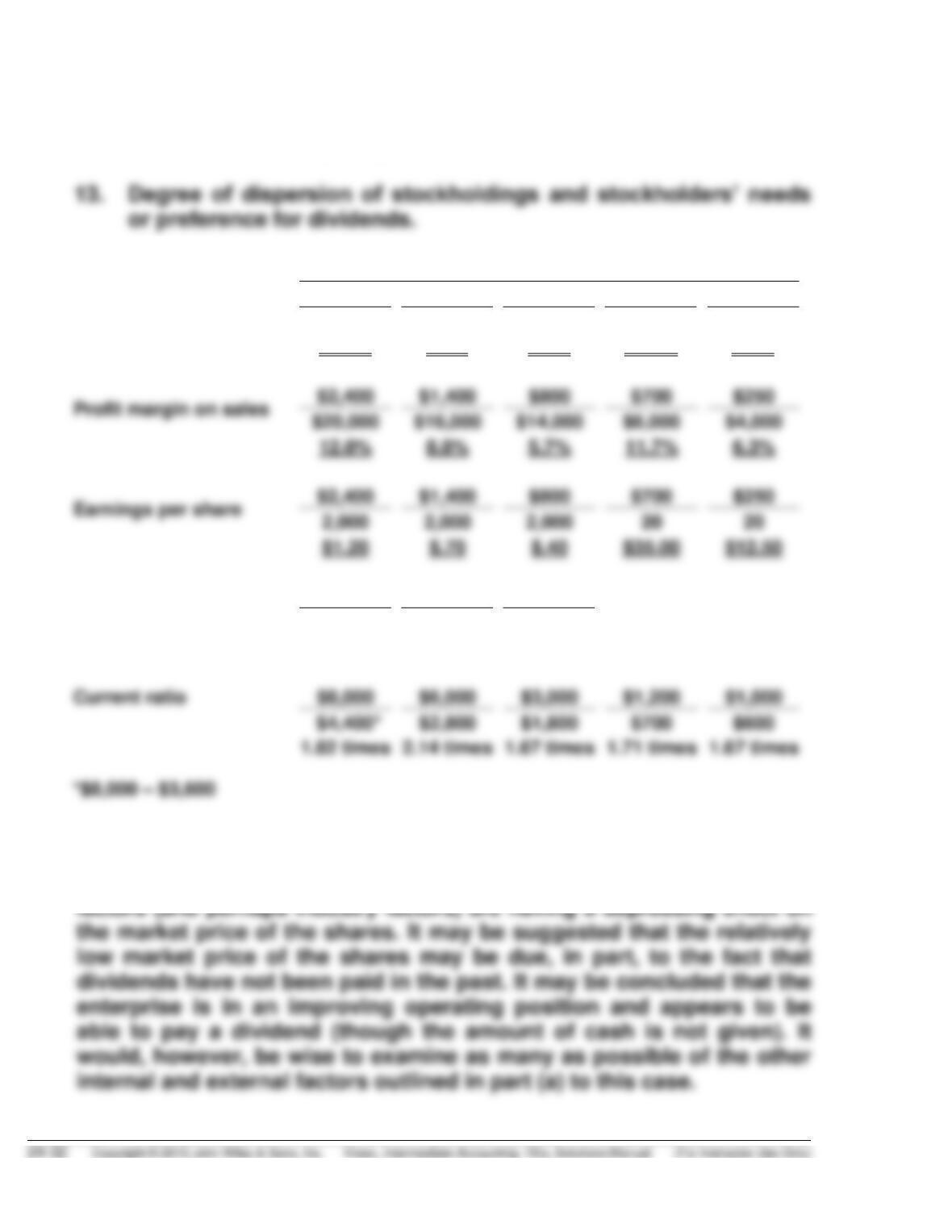

*PROBLEM 24-5

(a) In establishing a dividend policy, the following are factors that should

be taken into consideration:

1. The expansion plans or goals of the organization and the need for

monies to finance new activities.

5. The ability of the organization to maintain a given dividend in future

years. To offer a dividend this year that cannot be maintained

may be harmful. It could also be harmful to establish a policy

seeming to call for increasing dividends over the years in the event

the increase could not be kept up.

6. The current position of the company. Is cash available to pay the

dividend? Will working capital be decreased to a dangerous level?

*PROBLEM 24-5 (Continued)

12. Personal tax situations of stockholders if known—whether preference

for dividends or capital gains.

(b)

2015

2014

2013

2012

2011

Return on assets

$2,400

$1,400

$800

$700

$250

$22,000

$19,000

$11,500

$4,200

$3,000

10.9%

7.4%

7.0%

16.7%

8.3%

Profit margin on sales

$2,400

$1,400

$800

$700

$250

$6,000

$4,000

12.0%

8.8%

5.7%

11.7%

6.3%

Earnings per share

$2,400

$1,400

$800

$700

$250

20

20

$35.00

Price-earnings ratio

$9

$6

$4

$1.20

$.70

$.40

7.5 times

8.6 times

10 times

Current ratio

$8,000

$6,000

$3,000

$1,200

$1,000

$2,800

$1,800

$700

$600

(c) While the return on assets, profit margin on sales, and earnings per

share have been increasing, the market price of the shares has not

given full recognition to these increases. This suggests that market

*PROBLEM 24-5 (Continued)

A dividend in the range of 12¢ to 36¢ being 10% to 30% of earnings per

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 24-1 (Time 10–20 minutes)

Purpose—to provide the student with an understanding of the necessary information which must be

CA 24-2 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the necessary information which should be

CA 24-3 (Time 24–30 minutes)

Purpose—to provide the student with an understanding of the types of disclosures which are necessitated

under certain circumstances. This case involves three independent situations dealing with such concepts

situations.

CA 24-4 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the proper accounting for subsequent event

transactions. Bankruptcy, issue of debt, strikes, and other typical subsequent event transactions are

presented.

CA 24-5 (Time 30–35 minutes)

CA 24-6 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of segment reporting. The case explores why a

CA 24-7 (Time 24–30 minutes)

Purpose—to provide the student with an understanding of the concepts underlying the applications of

CA 24-8 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the applications and requirements of interim

Time and Purpose of Concepts for Analysis (Continued)

CA 24-9 (Time 30–35 minutes)

Purpose—to provide the student with an understanding of the concepts of interim reporting and its

CA 24-10 (Time 24–30 minutes)

Purpose—to provide the student with an understanding of the conceptual merits underlying the prepara-

CA 24-11 (Time 15–20 minutes)

Purpose—to provide the student with an understanding of an ethical dilemma that may arise in the

future. In this case, the reason for the profit margin increasing is not properly described by the financial

vicepresident and the controller realizes the misstatement. The question is what should the controller do?

CA 24-12 (Time 10–15 minutes)

Purpose—to provide the student with an understanding of an ethical dilemma that may arise in the

*CA 24-13 (Time 24–35 minutes)

Purpose—to provide the student with an understanding of the effects which various transactions have

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 24-1

Koch Corporation must disclose the following information regarding inventories:

1. The dollar amount assigned to inventory.

The following information must be disclosed for property, plant, and equipment:

1. The balance of major classes of depreciable assets (assets classified by nature or function).

CA 24-2

Item 1

The staff auditor reviewing the loan agreement misinterpreted its requirements. Retained earnings are

Item 2

Unless cumulative preferred dividends are involved, no recommendation by the CPA is required. Common

stock dividend policy is understood by readers of financial statements to be discretionary on the part of

the board of directors. The company need not commit itself to a prospective common stock dividend policy

future.

Item 3

A competitive development of this nature normally is considered to be the type of subsequent event that

provides evidence with respect to a condition that did not exist at the date of the balance sheet. In some

circumstances the auditor might conclude that Ace’s poor competitive situation was evident at year-

end. In any event, the development should be disclosed to users of the financial statements because

CA 24-2 (Continued)

Item 4

The lease agreement with Wichita National Bank meets the criteria for a capital lease because it con-

tains a bargain purchase option (a 25-year-life building can be purchased at the end of 10 years for $1).

Additionally, unless the fair value of the building is considerably greater than its $2,400,000 cost, the

CA 24-3

Situation 1

When a company sells a product subject to a warranty, it is probable that there will be expenses

incurred in future accounting periods relating to revenues recognized in the current period. As such, a

liability has been incurred to honor the warranty at the same date as the recognition of the revenue.

Situation 2

Even though: (1) there is a probable loss on the contract, (2) the amount of the loss can be reasonably

estimated and (3) the likelihood of the loss was discovered prior to the issuance of the financial state–

ments, the fact that the contract was entered into subsequent to the date of the financial statements

Situation 3

The fact that a company chooses to self-insure the contingency of injury to others caused by its vehicles

is not enough of a basis to accrue a loss contingency that has not occurred at the date of the financial

statements. An accrual or “reserve” cannot be made for the amount of insurance premium that would

CA 24-4

1. The financial statements should be adjusted for the expected loss pertaining to the remaining

receivable of $240,000. Such adjustment should reduce accounts receivable to their realizable

value as of December 31, 2014.

4. This case is a difficult problem. If this event is of the second type which provides evidence with

respect to conditions that did not exist at December 31, 2014, then appropriate disclosures should

indicate that:

(a) Recovery of costs invested in plant and inventory is in doubt.

CA 24-5

To: Anthony Reese, Accountant

From: Student

Date: Current date

Subject: Determination of reportable segments for Winsor Corp.

I have analyzed the segment information which you gave me and determined that the funeral, the

cemetery, and the real estate segments must be reported separately. The remaining three—the

limousine, floral, and dried whey segments—can be combined under the category of other.

To make this determination, I applied three criteria put forth by the FASB to the information provided for

2015. First, a segment must be reported separately if its revenue is greater than or equal to

10 percent of the enterprise’s combined revenue. This is the case with both the funeral and the cemetery

segments as revenue for both is greater than $40,600 (10 percent of combined revenue).

CA 24-5 (Continued)

Third, a segment must be reported separately if its identifiable assets are greater than or equal to

10 percent of the combined identifiable assets for all segments. Again, the funeral, the cemetery, and

the real estate segments meet this test. Note that the limousine, floral, and dried whey segments meet

CA 24-6

(a) Some companies such as H. J. Heinz have only one dominant product or service and therefore it

is impossible to provide segmented data in a meaningful fashion. Dominant means that a given

segment has 90% of all the sales, profit and identifiable assets of the company. In this case,

CA 24-7

(a) Financial reporting for segments of a business enterprise involves reporting financial information

bases of segmentation.

(b) The reasons for requiring financial data to be reported by segments include the following:

1. They would provide more detailed disclosure of information needed by investors, creditors,

and other users of financial statements.

2. Appraisers can evaluate major segments of a business enterprise before considering the

CA 24-7 (Continued)

(c) The possible disadvantages of requiring financial data to be reported by segments include the

following:

1. They could be misinterpreted due to the public’s general lack of appreciation of the limitations

of the somewhat arbitrary bases for most allocations of common costs.

2. They may disguise the interdependence of all the segments.

3. They might result in misleading comparisons of segments of different enterprises.

considered by many to be insurmountable.

(d) The accounting difficulties inherent in segment reporting include the following:

1. The transfer prices must be determined. Transfer prices are those charged when one segment

deals with another segment of the same enterprise. Various possible transfer prices exist,

and the company must select one.

2. The computation of segment net income must be defined. The net income may be merely a

contribution margin, that is, sales less variable costs, or a more conventional measure of net

income. If a contribution-margin approach is used, the variable costs must be identified. If a

3. The treatment of segment information in interim financial reports must be established.

4. The method of presenting segment information in financial statements must be established.

Such presentation may be by notes or by separate financial statements.

CA 24-8

(a) 1. The company should report its quarterly results as if each interim period is an integral part

of the annual period.