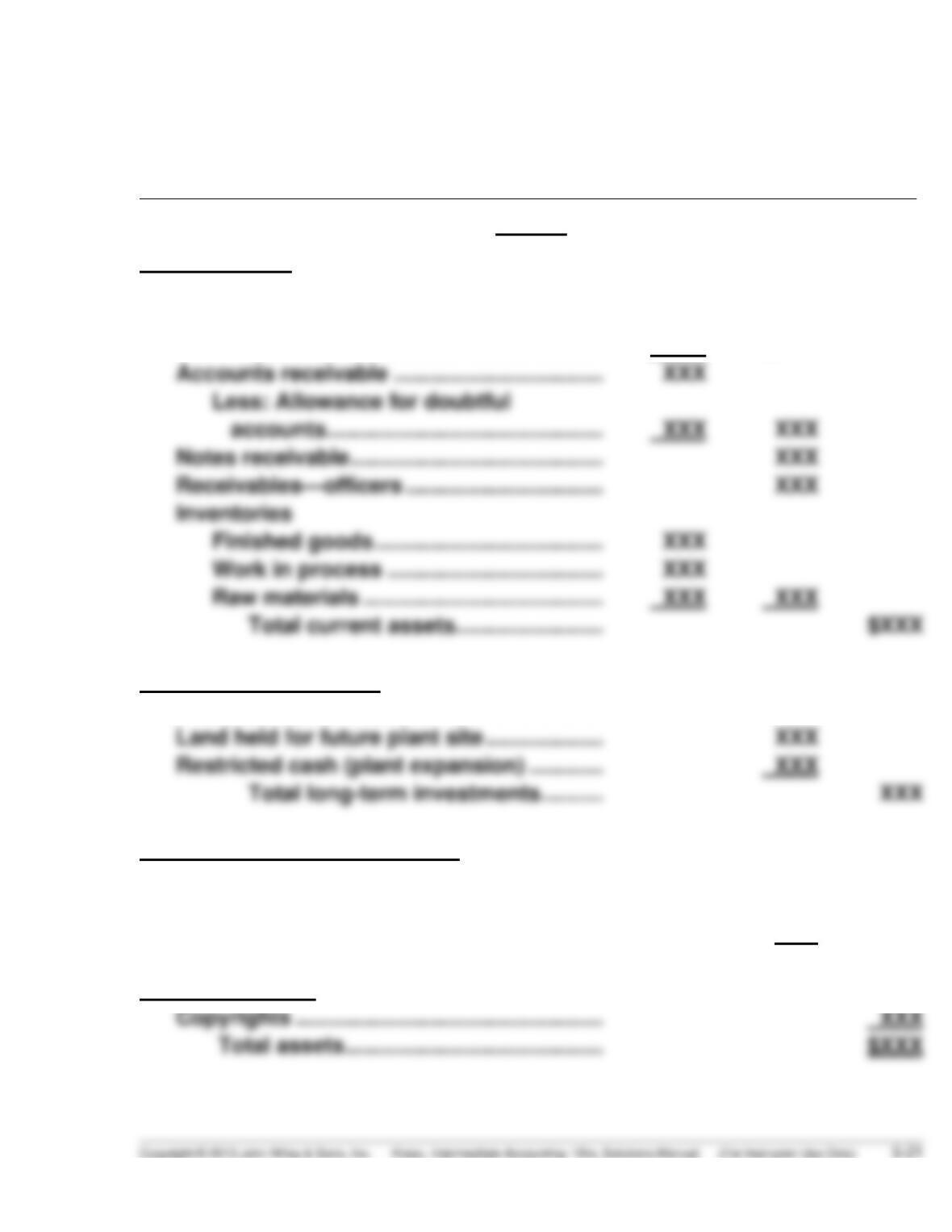

EXERCISE 5-4 (30–35 minutes)

Denis Savard Inc.

Balance Sheet

December 31, 20–

Assets

Current assets

Cash ……………………………………………………

$XXX

Less: Cash restricted for plant

expansion …………………………………….

XXX

$XXX

Accounts receivable …………………………….

XXX

Less: Allowance for doubtful

accounts ………………………………………

XXX

XXX

Notes receivable …………………………………..

XXX

Receivables—officers …………………………..

XXX

Inventories

Finished goods ……………………………….

XXX

Work in process ……………………………..

XXX

Raw materials …………………………………

XXX

Total current assets……………………

$XXX

Long-term investments

Preferred stock investments …………………

XXX

Land held for future plant site ……………….

XXX

Restricted cash (plant expansion) …………

Total long-term investments ……….

XXX

Property, plant, and equipment

Buildings ……………………………………………..

XXX

Less: Accum. depreciation—

buildings ……………………………………..

XXX

XXX

Intangible assets

Copyrights …………………………………………..

XXX

EXERCISE 5-4 (Continued)

Liabilities and Stockholders’ Equity

Current liabilities

Salaries and wages payable ………………………..

$XXX

Notes payable, short-term …………………………..

XXX

Unearned subscriptions revenue …………………

XXX

Unearned rent revenue ………………………………..

Total current liabilities …………………………..

Long-term debt

Bonds payable, due in four years ………………..

$XXX

Less: Discount on bonds payable ………………..

Total liabilities ……………………………………….

Stockholders’ equity

Capital stock:

Common stock ………………………………………

XXX

Additional paid-in capital:

Paid-in capital in excess of par

(common stock) …………………………………..

XXX

Total paid-in capital ………………………….

XXX

Retained earnings ………………………………………

retained earnings …………………………..

XXX

Less: Treasury stock, at cost ………………..

Equity attributable to Denis Savard, Inc. ………

Equity attributed to noncontrolling interest ….

Total stockholders’ equity ………………..

Note to instructor: An assumption made here is that cash included the

restricted cash for plant expansion. If it did not, then a subtraction from

cash would not be necessary or the cash balance would be “grossed up”

and then the restricted cash for plant expansion deducted.

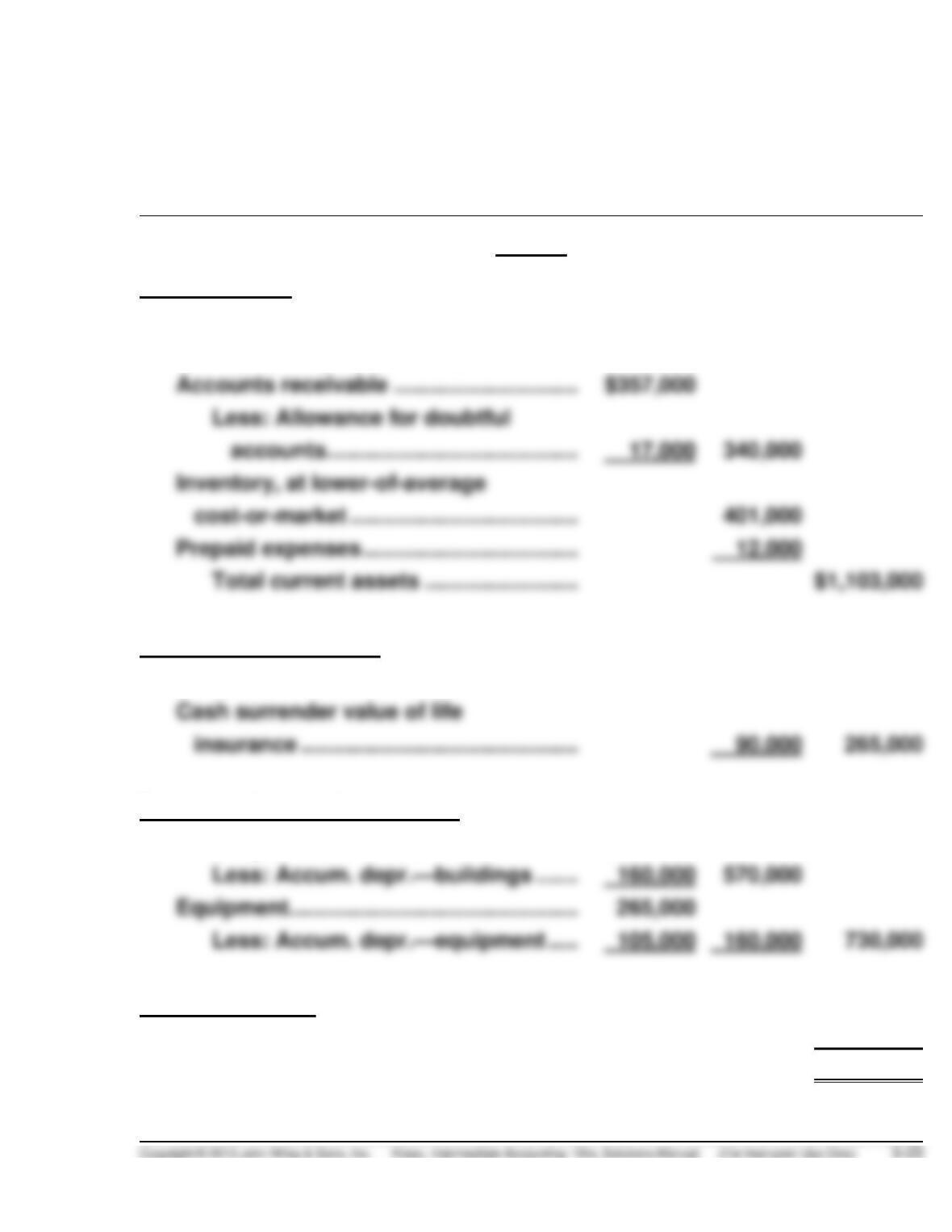

EXERCISE 5-5 (30–35 minutes)

Uhura Company

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ………………………………………………..

$230,000

Equity investments (trading) ……………..

120,000

Accounts receivable …………………………

$357,000

accounts …………………………………..

17,000

340,000

cost-or-market ……………………………….

401,000

Prepaid expenses ……………………………..

Total current assets …………………….

$1,103,000

Long-term investments

Land held for future use ……………………

175,000

insurance …………………………..………….

90,000

Property, plant, and equipment

Buildings ………………………………………….

$730,000

Less: Accum. depr.—buildings …….

570,000

Equipment ………………………………………..

Less: Accum. depr.—equipment …..

Intangible assets

Goodwill …………………………………………..

80,000

Total assets ………………………………..

$2,178,000

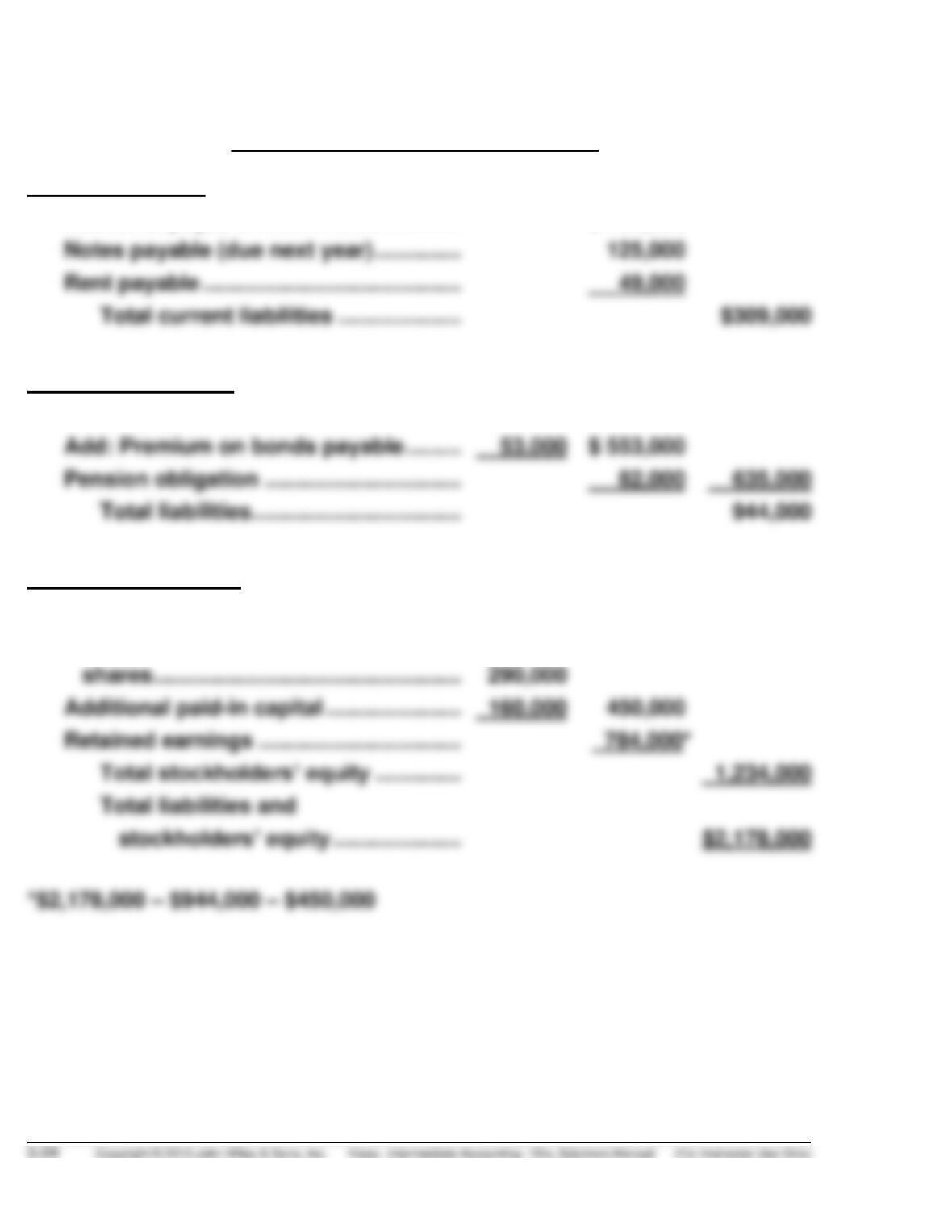

EXERCISE 5-5 (Continued)

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ……………………………..

$ 135,000

Notes payable (due next year) ……………

Rent payable …………………………..………..

49,000

Total current liabilities …………………

Long-term liabilities

Bonds payable ………………………………….

$500,000

Add: Premium on bonds payable ……….

53,000

$ 553,000

Pension obligation …………………………..

Total liabilities ……………………………..

Stockholders’ equity

Additional paid-in capital …………………..

Retained earnings …………………………….

Total stockholders’ equity ……………

Common stock, $1 par, authorized

400,000 shares, issued 290,000

EXERCISE 5-6 (30–35 minutes)

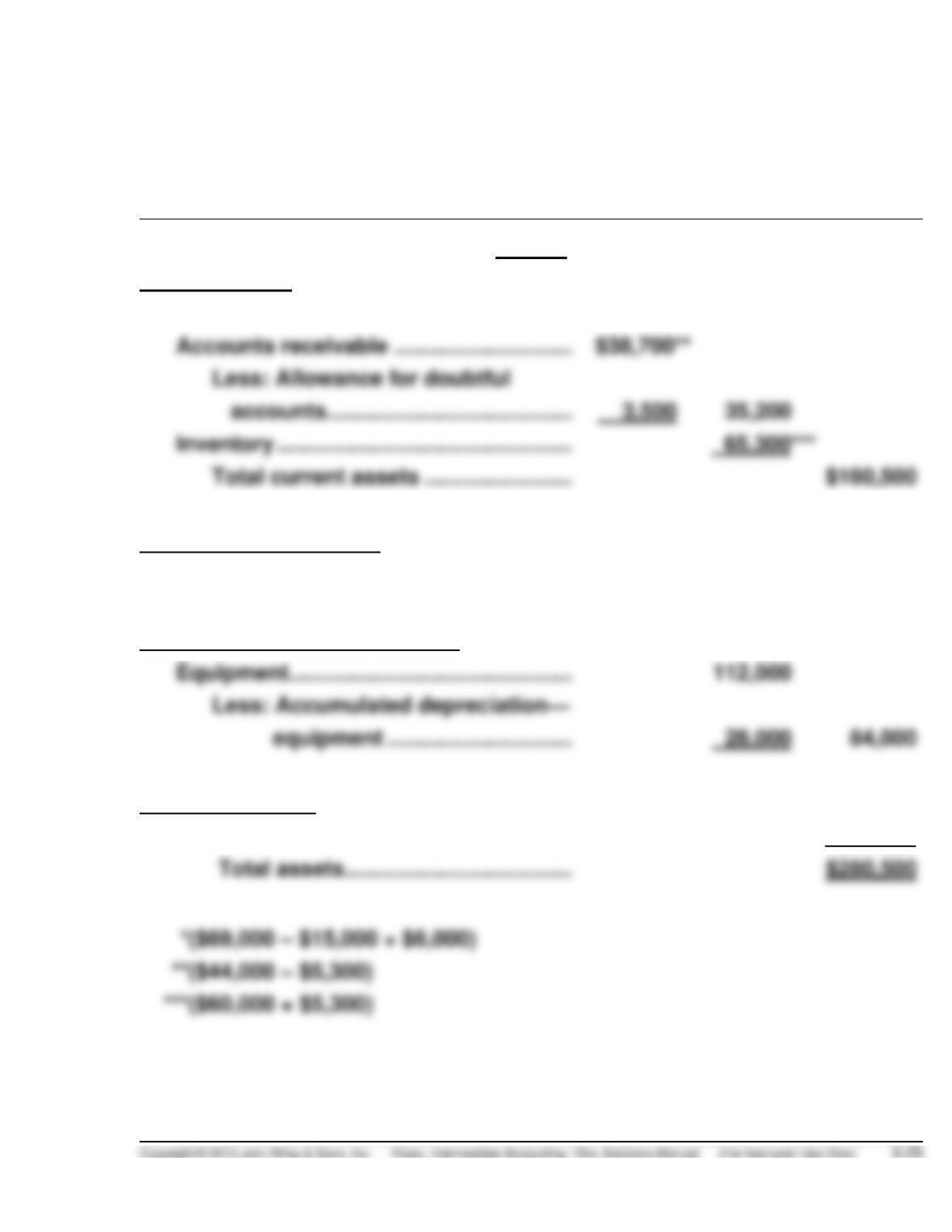

Geronimo Company

Balance Sheet

July 31, 2014

Assets

Current assets

Cash ……………………………………………………….

$60,000*

Accounts receivable …………………………..

Inventory …………………………..……………………….

Total current assets …………………………..

Long-term investments

Bond sinking fund ………………………………………

15,000

Property, plant, and equipment

Equipment ………………………………………………….

equipment …………………………..

84,000

Intangible assets

Patents ………………………………………………………

21,000

($69,000 – $15,000 + $6,000)

***

($60,000 + $5,300)

EXERCISE 5-6 (Continued)

Liabilities and Stockholders’ Equity

Current liabilities

Notes and accounts payable ……………………….

$ 44,000

Income taxes payable………………………………….

6,000

Total current liabilities …………………………..

Long-term liabilities …………………………………………

75,000

Total liabilities ……………………………………….

125,000

EXERCISE 5-7 (15–20 minutes)

Current assets

Cash …………………………………………………………..

$ 87,000*

Less: Restricted cash (plant expansion) ……….

50,000

$ 37,000

Trading securities at fair value (cost,

$31,000) ……………………………………………………

29,000

Accounts receivable (of which $50,000 is

pledged as collateral on a bank loan) …………

Less: Allowance for doubtful accounts …………

12,000

Interest receivable [($40,000 X 6%) X 8/12] …….

Inventories at lower of cost (determined

using LIFO) or market

Finished goods ………………………………………

Work in process …………………………………….

Raw materials …………………………..……………

207,000

*An acceptable alternative is to report cash at $37,000 and simply report

the restricted cash (plant expansion) in the investments section.

EXERCISE 5-8 (10–15 minutes)

1. Dividends payable of $2,375,000 will be reported as a current liability

[(1,000,000 – 50,000) X $2.50].

2. Bonds payable of $25,000,000 and interest payable of $3,000,000

EXERCISE 5-9 (30–35 minutes)

(a) Allessandro Scarlatti Company

Balance Sheet (Partial)

December 31, 2014

Current assets

Cash ………………………………………………….

$ 34,396*

Accounts receivable …………………………..

Inventory ……………………………………………

Prepaid expenses ……………………………….

*

Cash balance

$ 40,000

Add: Cash disbursement after discount

($39,000 X 98%)

38,220

Less: Cash sales in January ($30,000 – $21,500)

Cash collected on account

Bank loan proceeds ($35,324 – $23,324)

(12,000)

**

Accounts receivable balance

$ 89,000

Add: Accounts reduced from January collection

($23,324 ÷ 98%)

23,800

***

Inventory

$171,000

Less: Inventory received on consignment

12,000

Adjusted inventory

$159,000

EXERCISE 5-9 (Continued)

Current liabilities

Accounts payable ………………………………………

$115,000a

Notes payable ……………………………………………

Total current liabilities …………………………..

a

Accounts payable balance

$ 61,000

Add: Cash disbursements

$39,000

Adjusted accounts payable

$115,000

b

Notes payable balance

$ 67,000

Less: Proceeds of bank loan

12,000

Adjusted notes payable

$ 55,000

(b)

Adjustment to retained earnings balance:

Add: January sales discounts

[($23,324 ÷ 98%) X .02] ………………………

$ 476

Deduct: January sales ………………………………….

January purchase discounts

($39,000 X 2%) ………………………………

December purchases ………………………

Consignment inventory ……………………

Change (decrease) to retained earnings …………

$(57,304)

EXERCISE 5-10 (15–20 minutes)

(a) In order for a liability to be reported for threatened litigation, the

amount must be probable and payment reasonably estimable. Since

these conditions are not met an accrual is not required.

(d) Although Bad Debt Expense of $300,000 should be debited and the

Allowance for Doubtful Accounts credited for $300,000, this does not

result in a liability. The allowance for doubtful accounts is a valuation

account (contra asset) and is deducted from accounts receivable on

the balance sheet.

EXERCISE 5-11 (25–30 minutes)

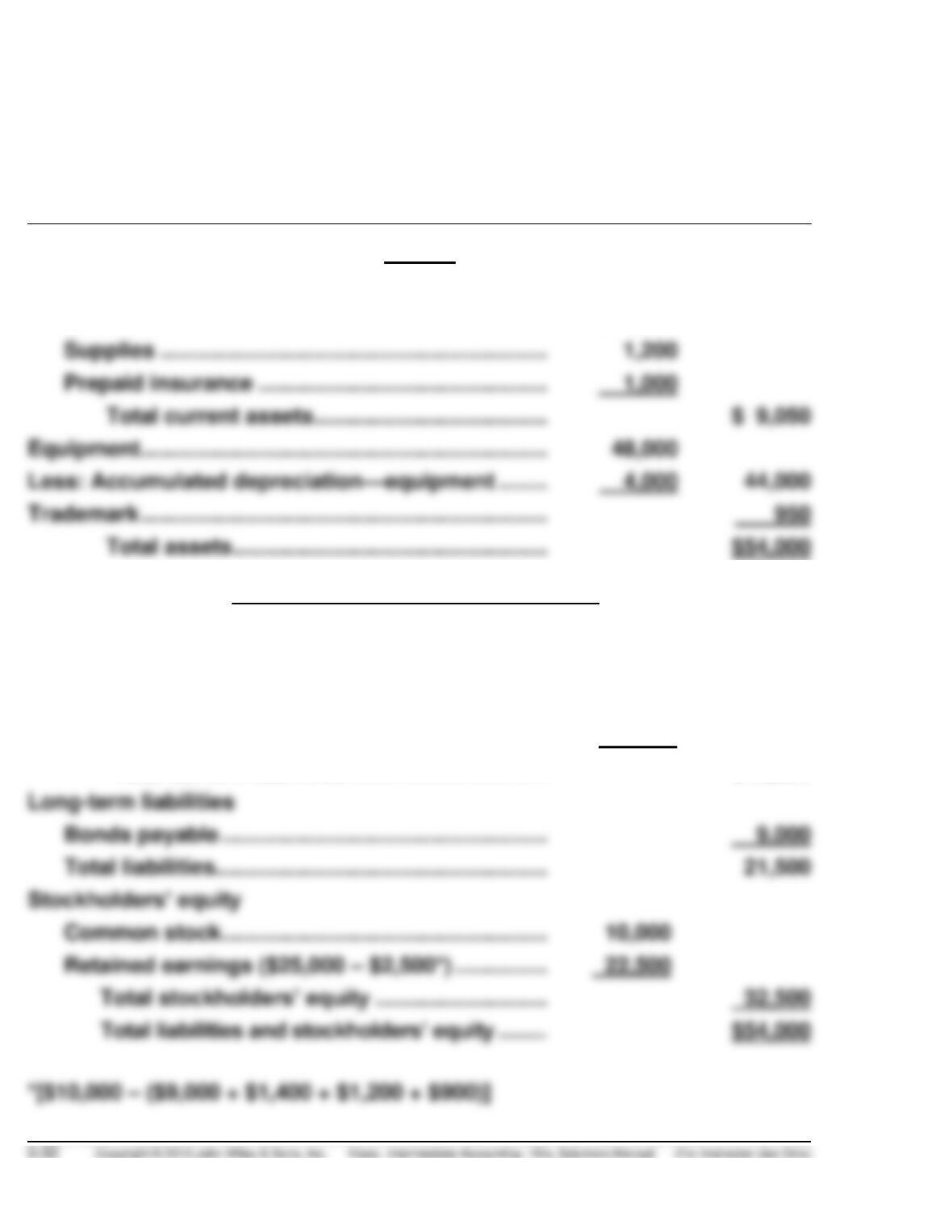

Kelly Corporation

Balance Sheet

December 31, 2014

Assets

Current assets

Cash …………………………………………………………….

$ 6,850

Supplies ……………………………………………………….

Prepaid insurance …………………………………………

1,000

Total current assets …………………………………

$ 9,050

Equipment ………………………………………………………….

Less: Accumulated depreciation—equipment ………

4,000

Trademark ……………………………………………………….…

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ………………………………………….

$10,000

Salaries and wages payable …………………………..

500

Unearned service revenue ……………………………..

2,000

Total current liabilities …………………………..

$12,500

Long-term liabilities

Bonds payable ………………………………………………

9,000

Total liabilities……………………………………………….

Common stock ………………………………………………

Retained earnings ($25,000 – $2,500*) …………….

Total stockholders’ equity ………………………..

EXERCISE 5-12 (30–35 minutes)

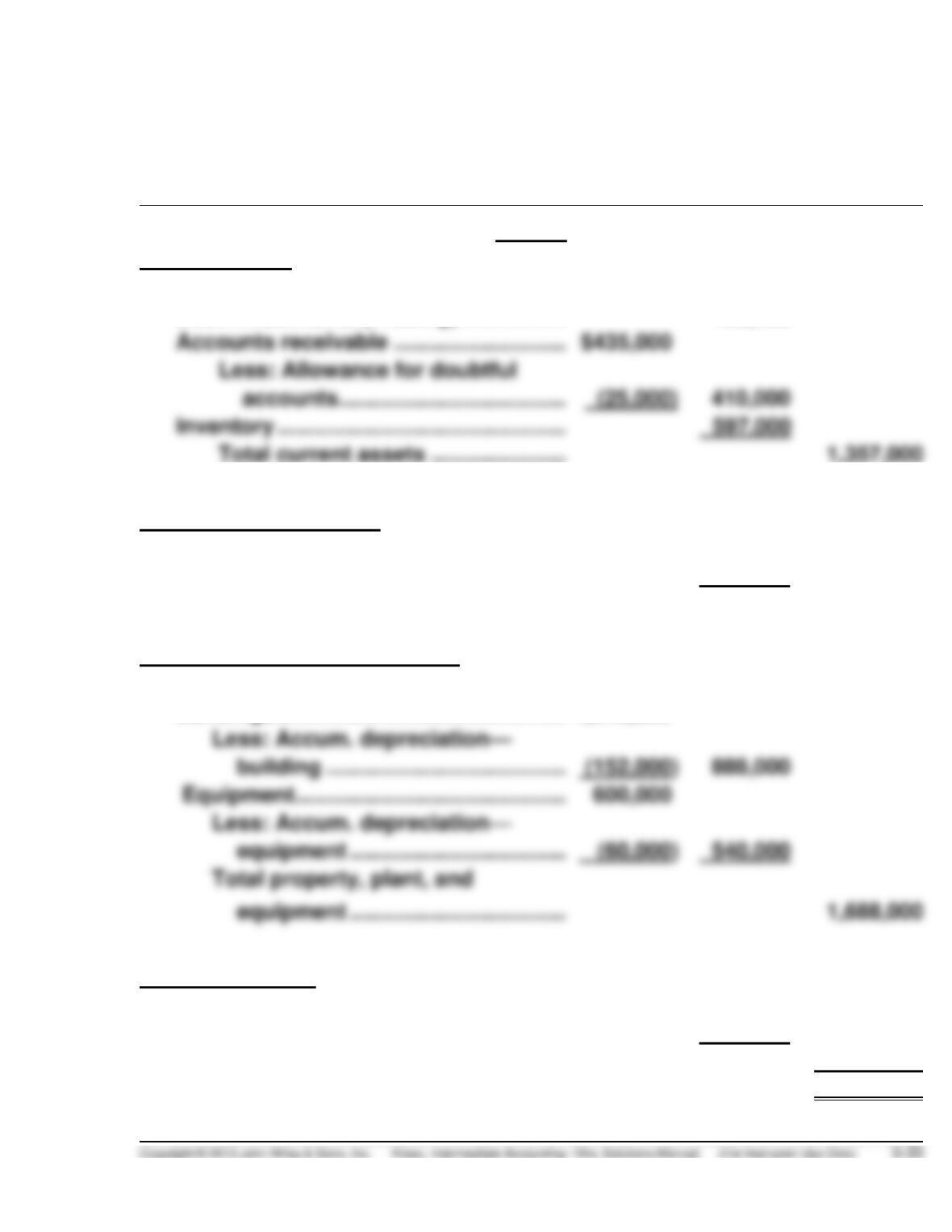

Scott Butler Corporation

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ……………………………………………….

$197,000

Debt investments (Trading) ………………

153,000

Accounts receivable ………………………..

Inventory …………………………..…………….

Total current assets …………………..

Long-term investments

Debt investments …………………………….

299,000

Equity investments ………………………….

277,000

Total long-term investments ………

576,000

Property, plant, and equipment

Land ……………………………………………….

260,000

Buildings …………………………………………

1,040,000

building ………………………………….

888,000

Equipment ………………………………………

equipment ………………………………

540,000

Intangible assets

Franchises ……………………………………………..

160,000

Patents ……………………………………………

195,000

Total intangible assets ………………..

355,000

Total assets ………………………………..

$3,976,000

EXERCISE 5-12 (Continued)

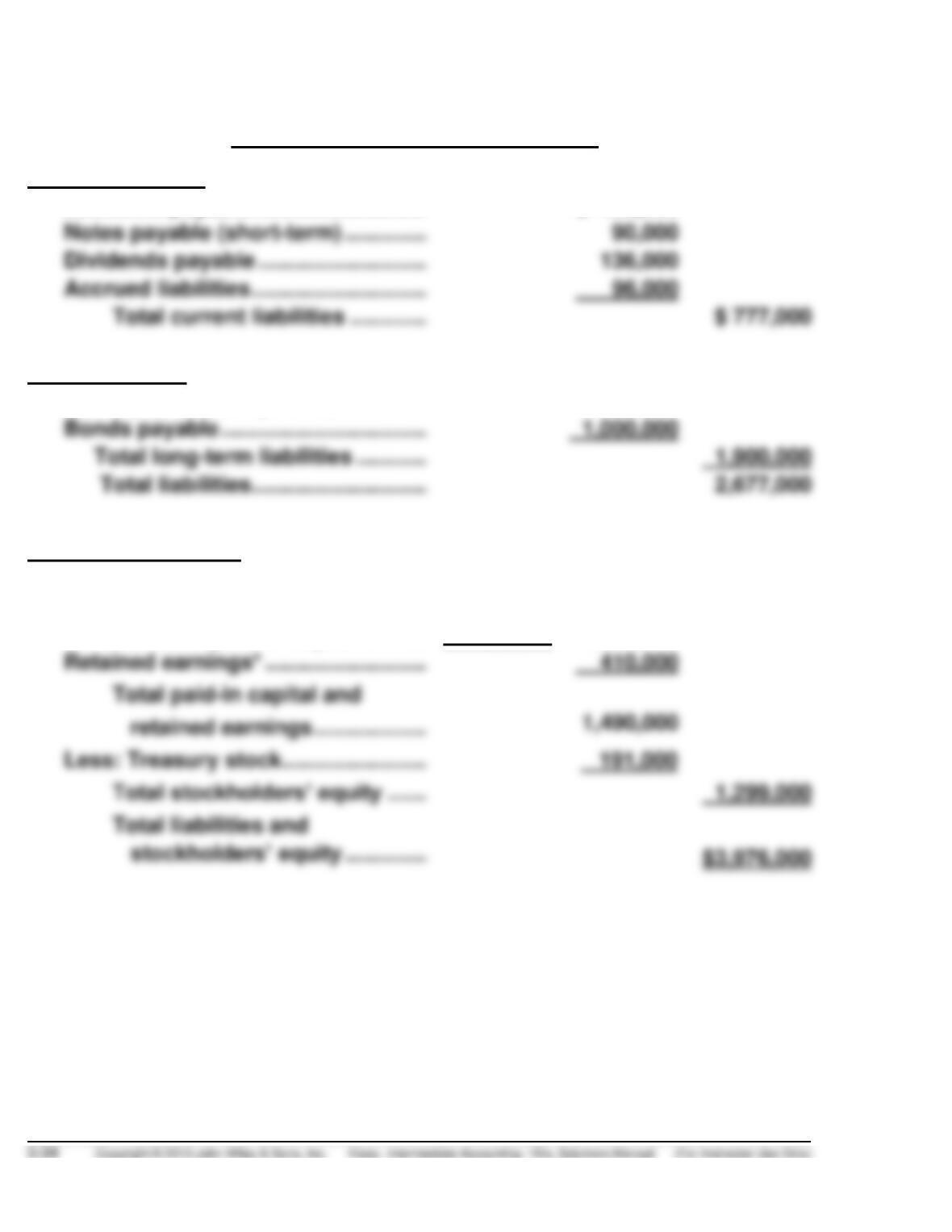

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………

$ 455,000

Notes payable (short-term) ……………

Dividends payable ………………………..

136,000

Accrued liabilities …………………………

96,000

Total current liabilities …………..

Long-term debt

Notes payable (long-term) …………….

900,000

Bonds payable ……………………………..

Total long-term liabilities ………….

Total liabilities …………………………

Stockholder’s equity

Paid-in capital

Common stock ($5 par) ……………

$1,000,000

Additional paid-in capital …………

80,000

1,080,000

Retained earnings* ……………………….

retained earnings ………………..

Less: Treasury stock …………………….

Total stockholders’ equity ……..

EXERCISE 5-12 (Continued)

*Computation of Retained Earnings:

Sales revenue

$8,100,000

Investment revenue

63,000

Extraordinary gain

80,000

Cost of goods sold

Selling expenses

Administrative expenses

Interest expense

(211,000)

Net income

$ 332,000

Beginning retained earnings

$ 78,000

Net income

332,000

Ending retained earnings

$410,000

Or ending retained earnings can be computed as follows:

Add: Treasury stock

Less: Paid-in capital in excess of par

Ending retained earnings

$ 410,000

Note to instructor: There is no dividends account. Thus, the 12/31/14 retained

earnings balance already reflects any dividends declared.

EXERCISE 5-13 (15–20 minutes)

(a)

4.

(f)

1.

(k)

1.

(b)

3.

(g)

5.

(l)

2.

(c)

4.

(h)

4.

(m)

2.

(e)

1.

(j)

4.

EXERCISE 5-14 (25–35 minutes)

Constantine Cavamanlis Inc.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………………

$44,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense ……………………………….

$ 6,000

Increase in accounts receivable ………………..

Increase in accounts payable ……………………

5,000

8,000

Net cash provided by operating activities ……….

Cash flows from investing activities

Purchase of equipment ………………………………….

Cash flows from financing activities

Payment of cash dividends …………………………..

Net cash used by financing activities ……………..

Net increase in cash ……………………………………………

Cash at beginning of year ……………………………………

EXERCISE 5-15 (25–35 minutes)

(a) Zubin Mehta Corporation

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………..…………………………

$160,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense ………………………………..

Loss on sale of investments ……………………….

Decrease in accounts receivable ………………..

Decrease in current liabilities ……………………..

15,000

Net cash provided by operating activities …………

175,000

Cash flows from investing activities

Sale of investments …………………………………………

12,000

Purchase of equipment ……………………………………

Net cash used by investing activities ……………….

Cash flows from financing activities

Payment of cash dividends …………………………..

Net increase in cash ……………………………………………..

Cash at beginning of year ……………………………………..

78,000

(b) Free Cash Flow Analysis

Net cash provided by operating activities ………………

$175,000

Less: Purchase of equipment ………………………………

(58,000)

Dividends …………………………………………………..

(30,000)

Free cash flow ……………………………………………………..

$ 87,000

EXERCISE 5-16 (20–25 minutes)

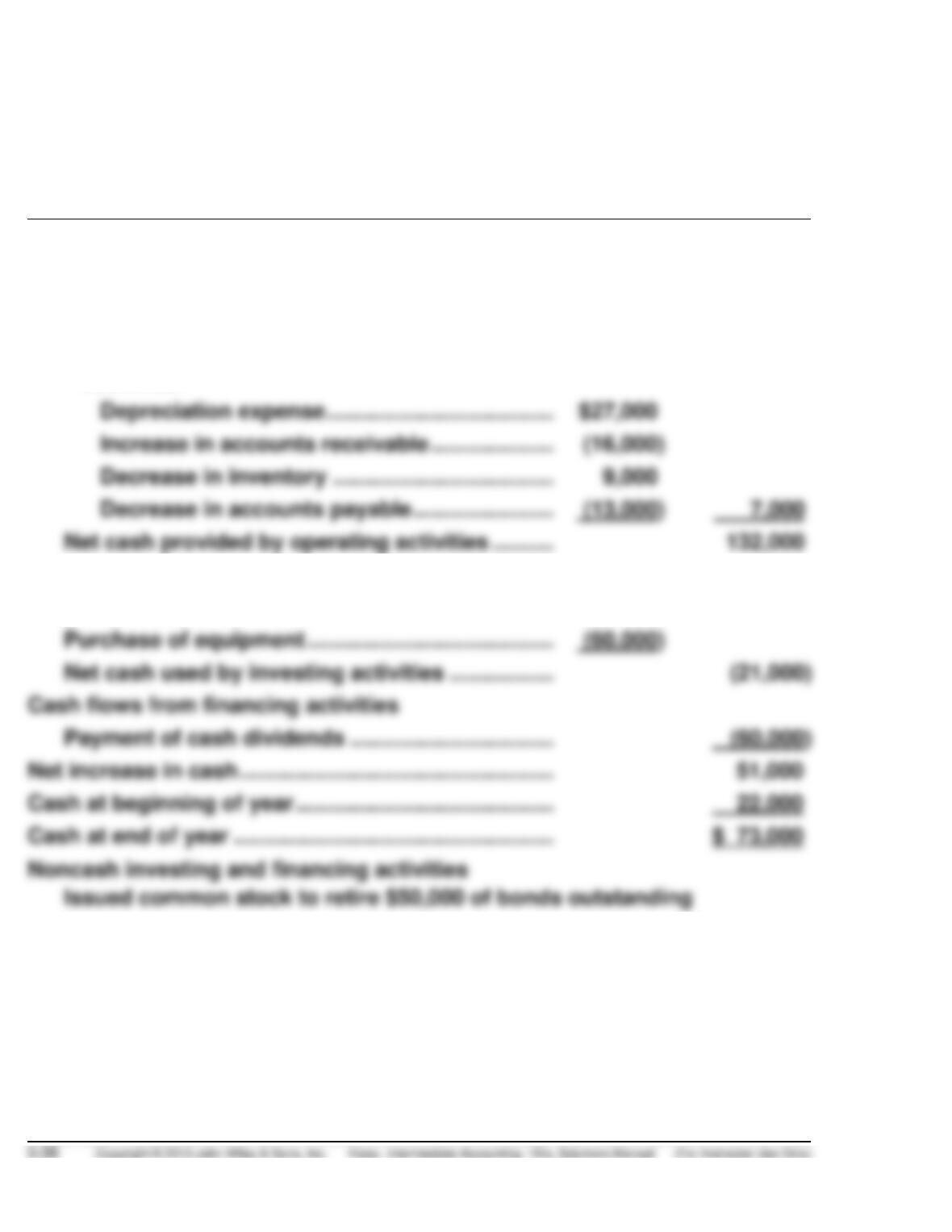

(a) Shabbona Corporation

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………………..

$125,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense …………………………………

Increase in accounts receivable ………………….

Decrease in inventory ………………………………..

Decrease in accounts payable …………………….

7,000

Net cash provided by operating activities …………

Cash flows from investing activities

Sale of land …………………………………………………….

39,000

Net cash used by investing activities ……………….

Cash flows from financing activities

Payment of cash dividends ……………………………..

Net increase in cash ……………………………………………..

Cash at beginning of year ……………………………………..

EXERCISE 5-16 (Continued)

(b) Current cash debt coverage =

.61 to 1

Free Cash Flow Analysis

Net cash provided by operating activities ……………………..

$132,000

Less: Purchase of equipment ……………………………………..

(60,000)

Dividends ………………………………………………………….

(60,000)

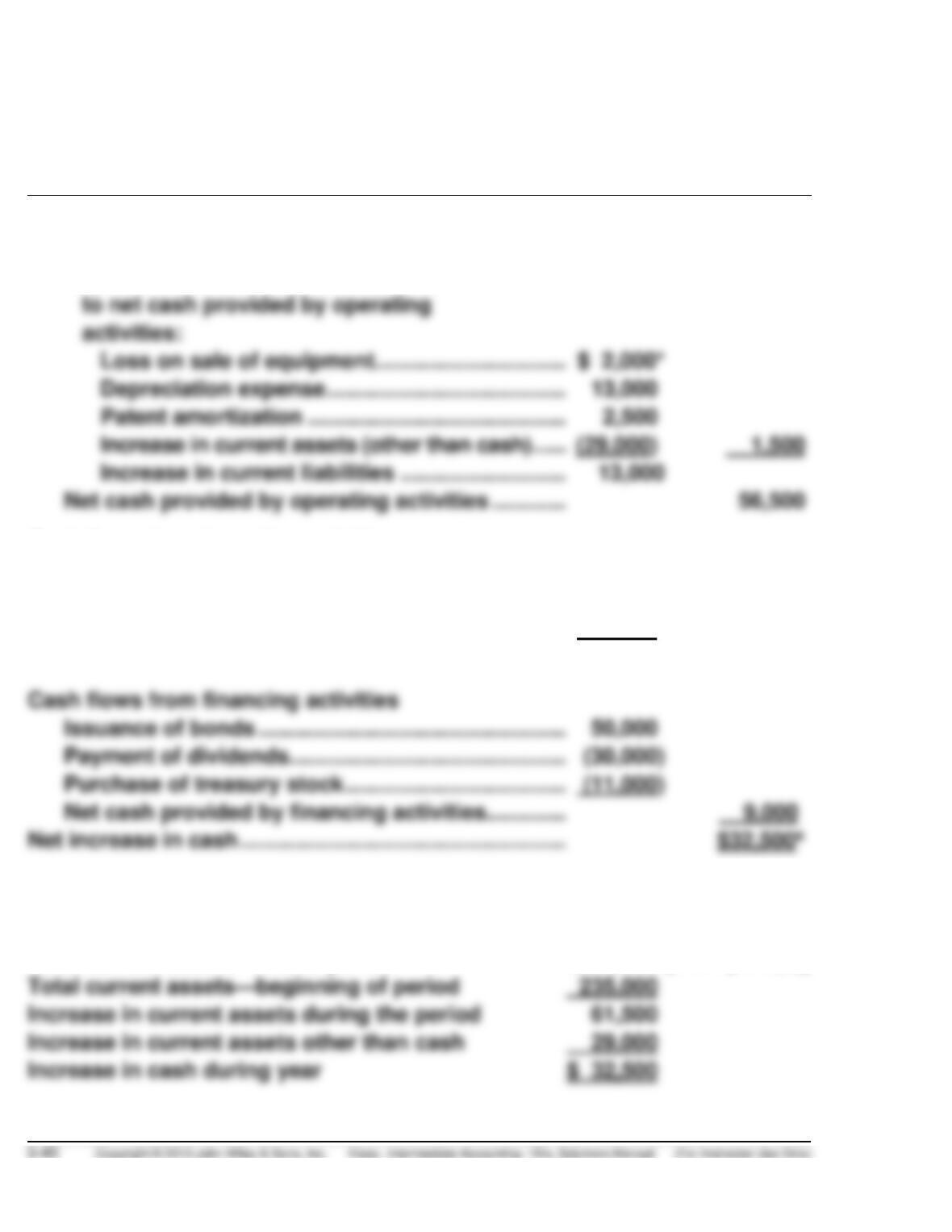

EXERCISE 5-17 (30–35 minutes)

(a) Grant Wood Corporation

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………………….

$55,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Loss on sale of equipment …………………………..

$ 2,000*

Depreciation expense …………………………………..

Patent amortization …………………………..…………

Increase in current assets (other than cash) ……..

1,500

Increase in current liabilities ………………………..

Net cash provided by operating activities …………..

Cash flows from investing activities

Sale of equipment ……………………………………………..

10,000

Addition to building …………………………………………..

(27,000)

Investment in stock …………………………………………..

(16,000)

Net cash used by investing activities …………………

(33,000)

Cash flows from financing activities

Issuance of bonds …………………………………………….

50,000

Payment of dividends ………………………………………..

(30,000)

Purchase of treasury stock ………………………………..

(11,000)

Net cash provided by financing activities……………

*[$10,000 – ($20,000 – $8,000)]

aAn additional proof to arrive at the increase in cash is provided as follows:

Total current assets—end of period

$296,500

[from part (b)]

Total current assets—beginning of period

Increase in current assets during the period

Increase in current assets other than cash

29,000