EXERCISE 8-10 (10–15 minutes)

Current Year

Subsequent Year

1.

Working capital

Overstated

No effect

Current ratio

Overstated

No effect

Retained earnings

Overstated

No effect

Net income

Overstated

Understated

2.

Working capital

No effect

Current ratio

No effect

Retained earnings

No effect

Net income

No effect

Working capital

Overstated

No effect

Current ratio

Overstated

No effect

Retained earnings

Overstated

No effect

Net income

Overstated

Understated

*Assume that the correct current ratio is greater than one.

EXERCISE 8-11 (10–15 minutes)

$370,000

$200,000

$185,000

(c)

Event

Effect of Error

Adjust Income

Increase (Decrease)

1.

Understatement of ending

inventory

Decreases net income

$22,000

3.

Overstatement of ending

Increases net income

EXERCISE 8-12 (15–20 minutes)

Errors in Inventories

Year

Net

Income

Per Books

Add

Overstate-

ment Jan. 1

Deduct

Understate-

ment Jan. 1

Deduct

Overstate-

ment Dec. 31

Add

Understate-

ment Dec. 31

Corrected

Net Income

2009

$ 50,000

$3,000

$ 47,000

2012

56,000

45,000

EXERCISE 8-13 (15–20 minutes)

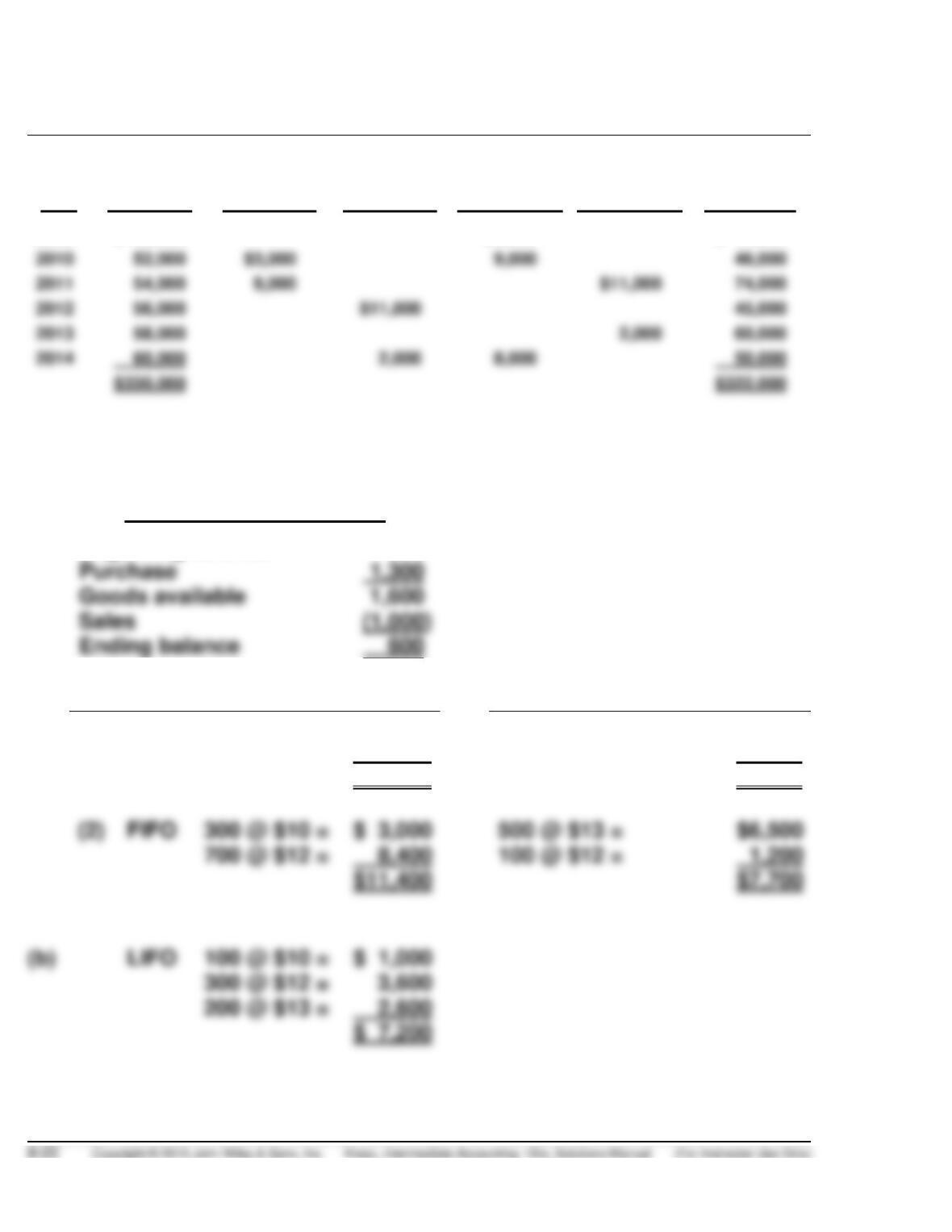

(a)

Units in ending inventory

Beginning balance

300

Purchase

Goods available

Sales

Ending balance

Cost of Goods Sold

Ending Inventory

(1)

LIFO

500 @ $13 =

$ 6,500

300 @ $10 =

$3,000

500 @ $12 =

6,000

300 @ $12 =

3,600

$12,500

$6,600

(2)

FIFO

300 @ $10 =

$ 3,000

500 @ $13 =

700 @ $12 =

8,400

100 @ $12 =

1,200

$11,400

$7,700

(b)

LIFO

100 @ $10 =

$ 1,000

300 @ $12 =

200 @ $13 =

2,600

$ 7,200

EXERCISE 8-13 (Continued)

(c)

Sales revenue

$25,400

= ($24 X 200) + ($25 X 500) +

($27 X 300)

Cost of Goods Sold

= (200 @ $10) + (100 @ $10)

Gross Profit (FIFO)

+ (400 @ $12) + (300 @ $12)

(d)

LIFO matches more current costs with revenue. When prices are

rising (as is generally the case), this results in a higher amount for

EXERCISE 8-14 (20–25 minutes)

(a)

(1)

LIFO

600 @ $6.00 =

$3,600

100 @ $6.08 =

608

$4,208

(2)

Average cost

700 @ $6.35 = $4,445

EXERCISE 8-14 (Continued)

(b)

(1)

FIFO

500 @ $6.79 =

$3,395

200 @ $6.60 =

1,320

$4,715

(2)

LIFO

100 @ $6.00 =

$ 600

100 @ $6.08 =

500 @ $6.79 =

$4,603

(c)

Total merchandise available for sale

Less: Inventory (FIFO)

EXERCISE 8-15 (15–20 minutes)

(a) Shania Twain Company

COMPUTATION OF INVENTORY FOR PRODUCT

BAP UNDER FIFO INVENTORY METHOD

March 31, 2014

Units

Unit Cost

Total Cost

March 26, 2014

600

$12.00

$ 7,200

February 16, 2014

January 25, 2014 (portion)

2,000

(b) Shania Twain Company

COMPUTATION OF INVENTORY FOR PRODUCT

BAP UNDER LIFO INVENTORY METHOD

March 31, 2014

Units

Unit Cost

Total Cost

Beginning inventory

600

$ 4,800

January 5, 2014 (portion)

EXERCISE 8-15 (Continued)

(c) Shania Twain Company

COMPUTATION OF INVENTORY FOR PRODUCT

BAP UNDER WEIGHTED-AVERAGE INVENTORY METHOD

March 31, 2014

Units

Unit Cost

Total Cost

Beginning inventory

600

$ 8.00

$ 4,800

January 25, 2014

Weighted average cost

($44,600 ÷ 4,500)

$ 9.91*

March 31, 2014, inventory

$ 9.91

EXERCISE 8-16 (15–20 minutes)

(a)

(1)

2,100 units available for sale – 1,400 units sold = 700 units in the

ending inventory.

$3,210

Ending inventory at FIFO cost.

$2,930

Ending inventory at LIFO cost.

(3)

cost.

EXERCISE 8-16 (Continued)

(b)

(1)

LIFO will yield the lowest gross profit because this method will

yield the highest cost of goods sold figure in the situation

(2)

LIFO will yield the lowest ending inventory because LIFO uses the

EXERCISE 8-17 (10–15 minutes)

(a)

(1)

400 @ $30 =

$12,000

160 @ $25 =

4,000

$16,000

(2)

400 @ $20 =

$ 8,000

160 @ $25 =

4,000

(b)

(1)

FIFO

$16,000 [same as (a)]

(2)

LIFO

100 @ $20 =

400 @ $30 =

EXERCISE 8-18 (15–20 minutes)

First-in, first-out

Last-in, first-out

Sales revenue

$1,050,000

$1,050,000

Cost of goods sold:

Inventory, Jan. 1

$120,000

$120,000

Inventory, Dec. 31

Cost of goods sold

Gross profit

Operating expenses

*Purchases

6,000 @ $22 =

$132,000

10,000 @ $25 =

250,000

7,000 @ $30 =

210,000

$592,000

**Computation of inventory, Dec. 31:

First-in, first-out:

7,000 units @ $30 =

$210,000

1,000 units @ $25 =

25,000

$235,000

***Last-in, first-out:

6,000 units @ $20 =

$120,000

2,000 units @ $22 =

$164,000

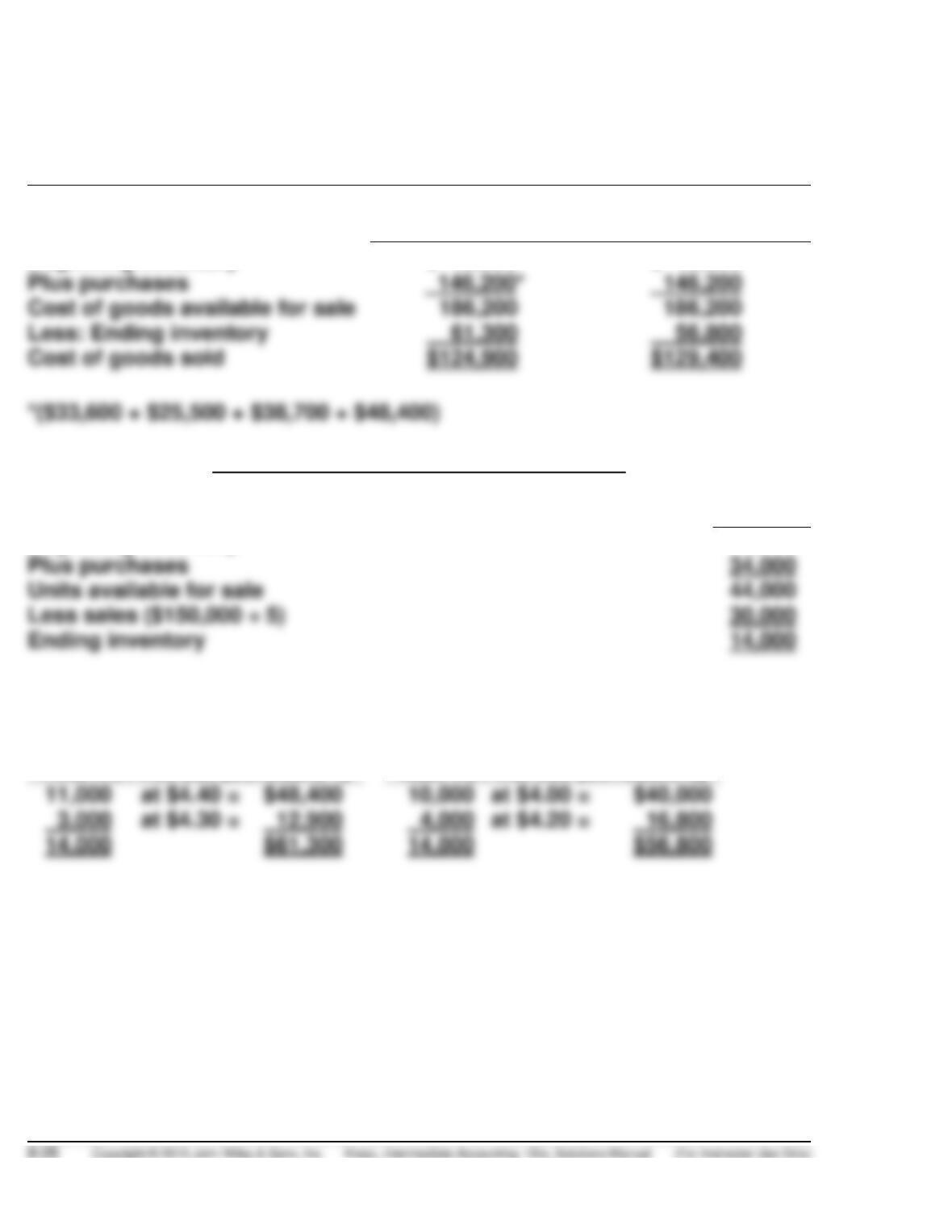

EXERCISE 8-19 (20–25 minutes)

Sandy Alomar Corporation

SCHEDULES OF COST OF GOODS SOLD

For the First Quarter Ended March 31, 2014

Schedule 1

First-in, First-out

Schedule 2 Last-in,

First-out

Beginning inventory

$ 40,000

$ 40,000

Cost of goods available for sale

Schedules Computing Ending Inventory

Units

Beginning inventory

10,000

Plus purchases

Units available for sale

Less sales ($150,000 ÷ 5)

The unit computation is the same for both assumptions, but the cost

assigned to the units of ending inventory are different.

First-in, First-out (Schedule 1)

Last-in, First-out (Schedule 2)

at $4.40 =

at $4.00 =

at $4.30 =

at $4.20 =

EXERCISE 8-20 (10–15 minutes)

(a)

FIFO Ending Inventory 12/31/14

76 @ $10.89* =

$ 827.64

24 @ $11.88** =

(b)

LIFO Cost of Goods Sold—2014

76 @ $10.89 =

$ 827.64

90 @ $14.85* =

15 @ $15.84** =

237.60

(c) FIFO matches older costs with revenue. When prices are declining, as

EXERCISE 8-21 (10–15 minutes)

(a) The difference between the inventory used for internal reporting

purposes and LIFO is referred to as the Allowance to Reduce

EXERCISE 8-21 (Continued)

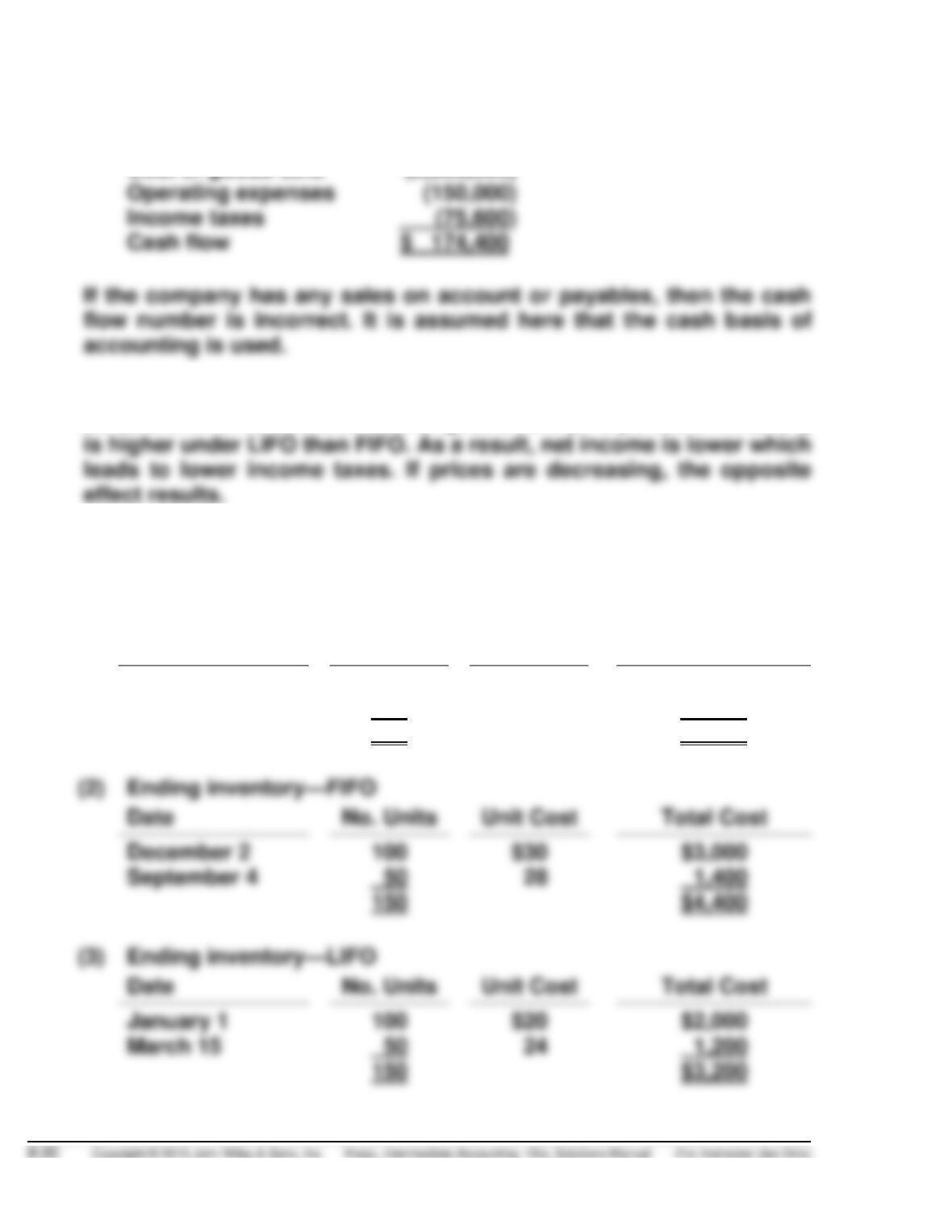

(c) Cash flow was computed as follows:

Revenue

$3,200,000

Cost of goods sold

(2,800,000)

Operating expenses

Income taxes

(d) The company has extra cash because its taxes are less. The reason

taxes are lower is because cost of goods sold (in a period of inflation)

EXERCISE 8-22 (25–30 minutes)

(a)

(1)

Ending inventory—Specific Identification

Date

No. Units

Unit Cost

Total Cost

December 2

100

$30

$3,000

July 20

50

25

1,250

150

$4,250

(2)

Date

Unit Cost

December 2

100

$30

$3,000

September 4

50

28

1,400

(3)

Date

Unit Cost

March 15

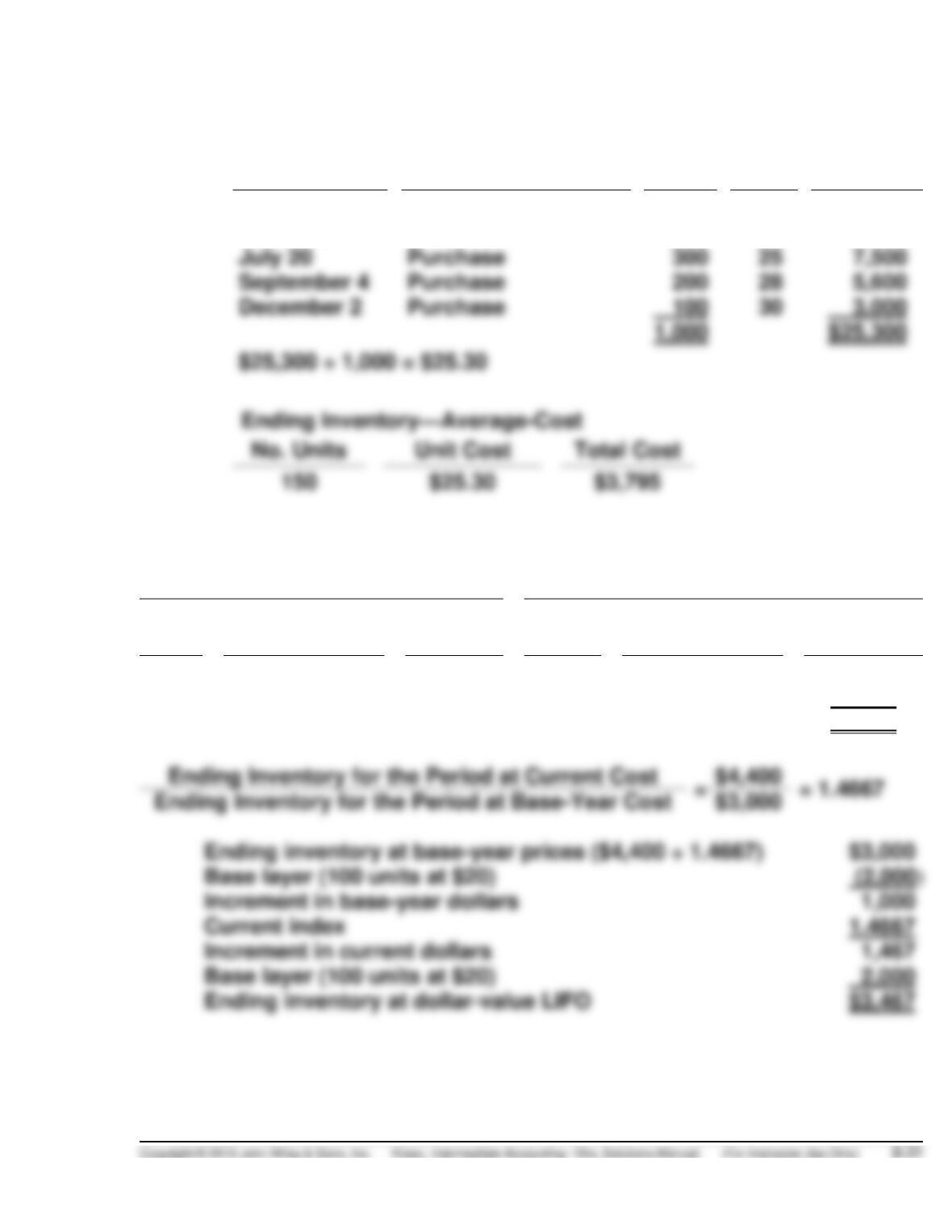

EXERCISE 8-22 (Continued)

(4)

Ending inventory—Average-Cost

Date

Explanation

No.

Units

Unit

Cost

Total

Cost

January 1

Beginning inventory

100

$20

$ 2,000

March 15

Purchase

300

24

7,200

December 2

Purchase

100

30

3,000

1,000

(b) Double Extension Method

Base-Year Costs

Current Costs

Units

Base-Year

Cost Per Unit

Total

Units

Current-Year

Cost Per Unit

Total

150

$20

$3,000

100

$30

$3,000

50

$28

1,400

$4,400

Ending Inventory for the Period at Current Cost

$3,000

Base layer (100 units at $20)

Increment in current dollars

Ending inventory at dollar-value LIFO

EXERCISE 8-23 (5–10 minutes)

$97,000 – $92,000 = $5,000 increase at base prices.

EXERCISE 8-24 (15–20 minutes)

(a)

12/31/14 inventory at 1/1/14 prices, $140,000 ÷ 1.12

$125,000

Inventory 1/1/14

160,000

Inventory at 1/1/14 prices

$160,000

Less decrease at 1/1/14 prices

35,000

(b)

12/31/15 inventory at base prices, $172,500 ÷ 1.15

$150,000

12/31/14 inventory at base prices

125,000

Inventory at 12/31/14

$125,000

EXERCISE 8-25 (20–25 minutes)

Current $

Price Index

Base Year $

Change from

Prior Year

2011

$ 80,000

1.00

$ 80,000

—

2013

1.20

90,000

2016

1.45

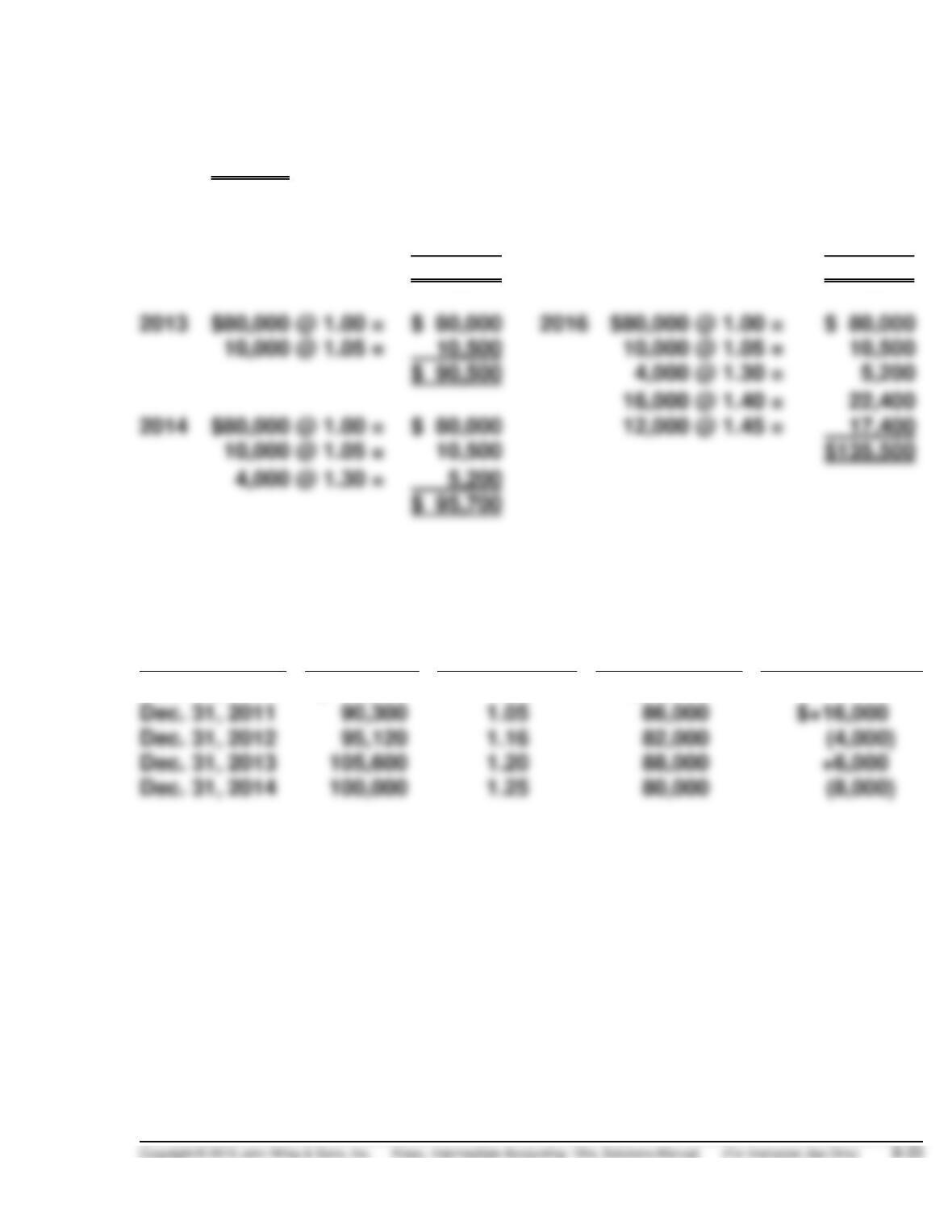

EXERCISE 8-25 (Continued)

Ending Inventory—Dollar-value LIFO:

2011

$80,000

2015

$80,000 @ 1.00 =

$ 80,000

10,000 @ 1.05 =

10,500

2012

$80,000 @ 1.00 =

$ 80,000

4,000 @ 1.30 =

5,200

30,000 @ 1.05 =

31,500

16,000 @ 1.40 =

22,400

$111,500

$118,100

2013

$80,000 @ 1.00 =

$ 80,000

2016

$80,000 @ 1.00 =

$ 80,000

10,000 @ 1.05 =

10,500

10,000 @ 1.05 =

$ 90,500

4,000 @ 1.30 =

16,000 @ 1.40 =

22,400

2014

$80,000 @ 1.00 =

$ 80,000

12,000 @ 1.45 =

17,400

$135,500

4,000 @ 1.30 =

5,200

$ 95,700

EXERCISE 8-26 (15–20 minutes)

Date

Current $

Price Index

Base-Year $

Change from

Prior Year

Dec. 31, 2010

$ 70,000

1.00

$70,000

—

Dec. 31, 2011

90,300

1.05

95,120

Dec. 31, 2014

1.25

EXERCISE 8-26 (Continued)

Ending Inventory—Dollar-value LIFO:

Dec. 31, 2010

$70,000

Dec. 31, 2011

$70,000 @ 1.00 =

$70,000

16,000 @ 1.05 =

$86,800

Dec. 31, 2012

$70,000 @ 1.00 =

$70,000

12,000 @ 1.05 =

$82,600

Dec. 31, 2013

$70,000 @ 1.00 =

$70,000

12,000 @ 1.05 =

12,600

6,000 @ 1.20 =

7,200

$89,800

Dec. 31, 2014

$70,000 @ 1.00 =

$70,000

$80,500

TIME AND PURPOSE OF PROBLEMS

Problem 8-1 (Time 30–40 minutes)

Problem 8-2 (Time 25–35 minutes)

Problem 8-3 (Time 20–25 minutes)

Purpose—to provide the student with an opportunity to prepare general journal entries to record pur–

chases on a gross and net basis.

Problem 8-4 (Time 40–55 minutes)

Purpose—to provide a problem where the student must compute the inventory using a FIFO, LIFO, and

Problem 8-5 (Time 40–55 minutes)

Purpose—to provide a problem where the student must compute the inventory using a FIFO, LIFO, and

Problem 8-6 (Time 25–35 minutes)

Purpose—to provide a problem where the student must compute cost of goods sold using FIFO, LIFO,

and weighted average, under both a periodic and perpetual system.

Problem 8-7 (Time 30–40 minutes)

Purpose—to provide a problem where the student must identify the accounts that would be affected if

LIFO had been used rather than FIFO for purposes of computing inventories.

Problem 8-8 (Time 30–40 minutes)

Problem 8-9 (Time 25–35 minutes)

Problem 8-10 (Time 30–35 minutes)

Problem 8-11 (Time 40–50 minutes)

Purpose—to provide the student with an opportunity to write a memo on how a dollar-value LIFO

pool works. In addition, the student must explain the step-by-step procedure used to compute dollar

value LIFO.

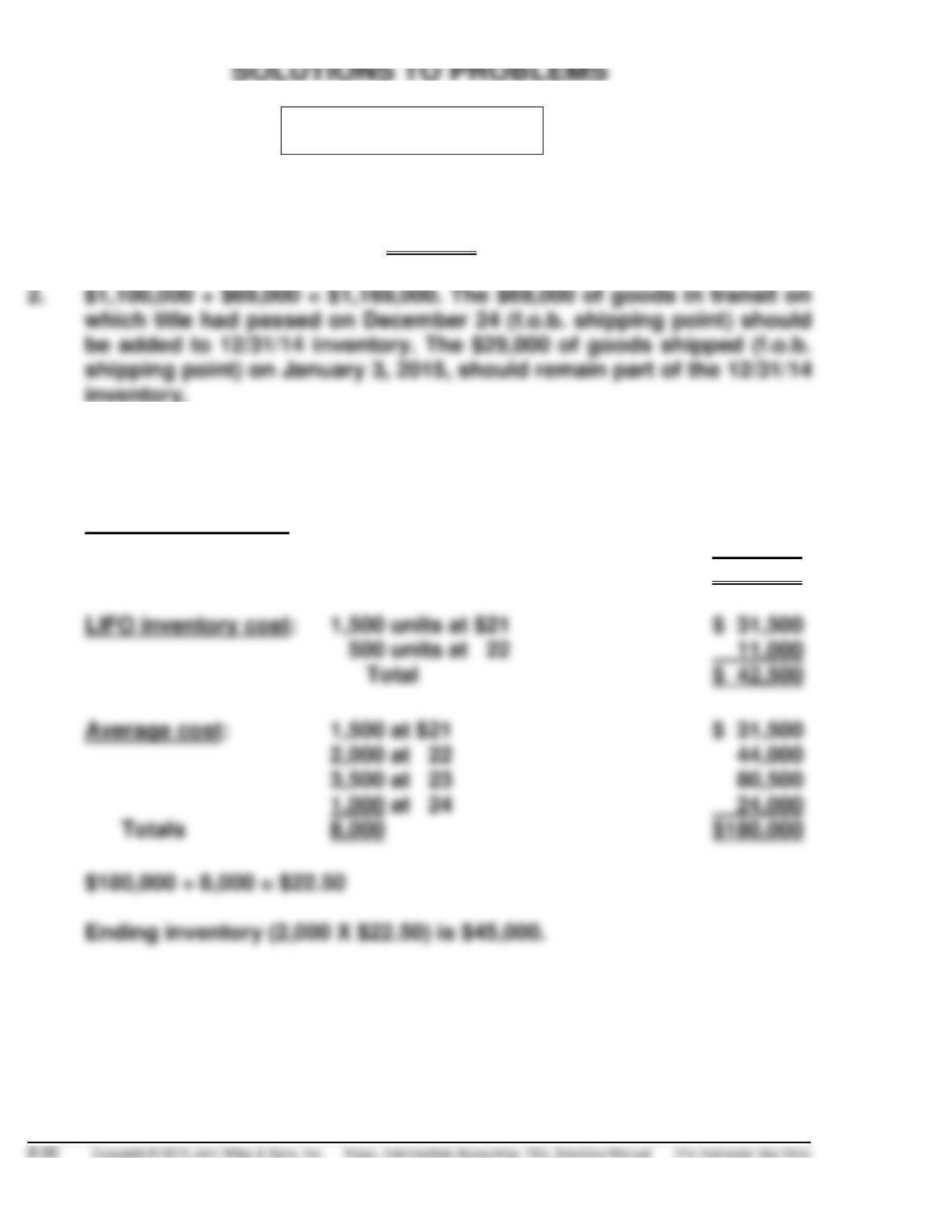

PROBLEM 8-1

1. $175,000 – ($175,000 X .20) = $140,000;

$140,000 – ($140,000 X .10) = $126,000, cost of goods purchased

3. Because no date was associated with the units issued or sold, the

periodic (rather than perpetual) inventory method must be assumed.

FIFO inventory cost:

1,000 units at $24

$ 24,000

1,000 units at 23

23,000

Total

$ 47,000

LIFO inventory cost:

1,500 units at $21

$ 31,500

500 units at 22

11,000

Total

$ 42,500

Average cost:

1,500 at $21

$ 31,500

2,000 at 22

3,500 at 23

1,000 at 24

24,000

Totals

8,000

$180,000

$180,000 ÷ 8,000 = $22.50

Ending inventory (2,000 X $22.50) is $45,000.

PROBLEM 8-1 (Continued)

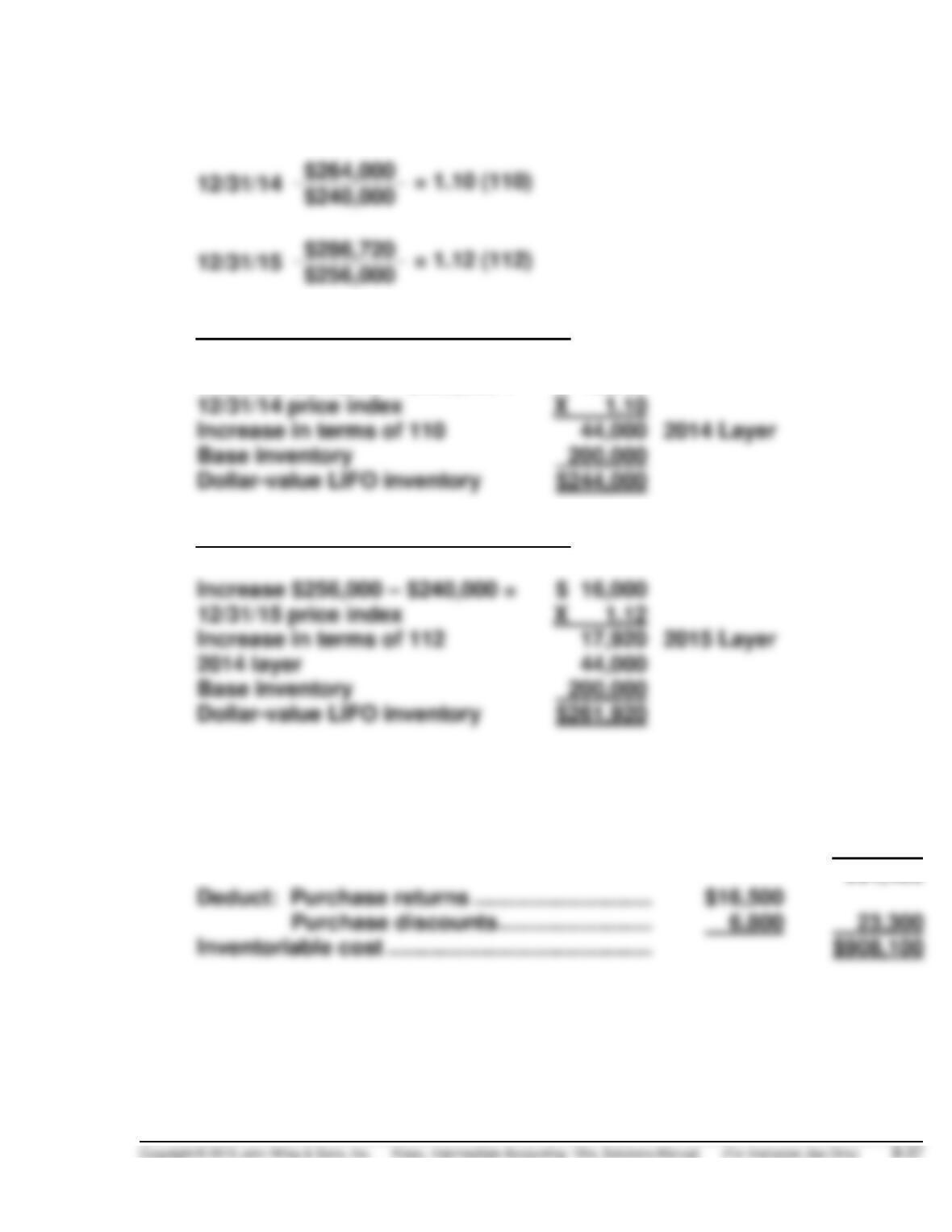

4. Computation of price indexes:

Dollar-value LIFO inventory 12/31/14:

Increase $240,000 – $200,000 =

$ 40,000

Increase in terms of 110

Base inventory

Dollar-value LIFO inventory 12/31/15:

Base inventory

5. The inventoriable costs for 2015 are:

Merchandise purchased …………………………...

$909,400

Add: Freight-in ………………………………………..

22,000

931,400

Deduct: Purchase returns ………………………..

Purchase discounts …………………….

23,300

PROBLEM 8-2

DIMITRI COMPANY

Schedule of Adjustments

December 31, 2014

Inventory

Accounts

Payable

Net Sales

Initial amounts

$1,520,000

$1,200,000

$8,150,000

Adjustments:

1.

NONE

NONE

(40,000)

2.

76,000

76,000

NONE

NONE

4.

32,000

NONE

(47,000)

5.

26,000

NONE

NONE

NONE

7.

NONE

56,000

NONE

8.

8,000

Total adjustments

195,000

140,000

1. The $31,000 of tools on the loading dock were properly included in the

physical count. The sale should not be recorded until the goods are

picked up by the common carrier. Therefore, no adjustment is made to

inventory, but sales must be reduced by the $40,000 billing price.

2. The $76,000 of goods in transit from a vendor to Dimitri were shipped

f.o.b. shipping point on 12/29/14. Title passes to the buyer as soon as

3. The work-in–process inventory sent to an outside processor is Dimitri’s

PROBLEM 8-2 (Continued)

4. The tools costing $32,000 were recorded as sales ($47,000) in 2014.

However, these items were returned by customers on December 31, so

5. The $26,000 of Dimitri’s tools shipped to a customer f.o.b. destination

are still owned by Dimitri while in transit because title does not pass on

6. The goods received from a vendor at 5:00 p.m. on 12/31/14 should be

included in the ending inventory, but were not included in the physical

7. The $56,000 of goods received on 12/26/14 were properly included in

8. Since one-half of the freight-in cost ($8,000) pertains to merchandise

properly included in inventory as of 12/31/14, $4,000 should be added

PROBLEM 8-3

(a)

1.

8/10

Purchases ………………………………………………………

12,000

Accounts Payable……………………………………

12,000

8/13

Accounts Payable …………………………..………………

Purchase Returns and Allowances …………..

8/15

Purchases ………………………………………………………

16,000

Accounts Payable……………………………………

16,000

Purchases ………………………………………………………

20,000

Accounts Payable……………………………………

20,000

8/28

Accounts Payable …………………………..………………

16,000

Cash ………………………………………………………

16,000

2. Purchases—addition to beginning inventory in cost of goods

sold section of income statement.

(b)

1.

8/10

Purchases ………………………………………………………

11,760

Accounts Payable ($12,000 X .98) …………….

11,760

Accounts Payable …………………………..………………

Purchase Returns and Allowances

($1,200 X .98) ………………………………………..