PROBLEM 18-1 (Continued)

Dement Publishing Division

Sales—fiscal 2014 …………………………………………………. $7,000,000

Less: Sales returns and allowances (20%) ……………… 1,400,000

Net sales—revenue to be recognized in fiscal 2014 …. $5,600,000

Ankiel Securities Division

Commissions and warranty returns are also selling expenses.

Both of these expenses will be accrued and will appear in the

operating expenses section of the income statement.

PROBLEM 18-2

(a)

2014

2015

2016

Contract price

$900,000

$900,000

$900,000

Less estimated cost:

Costs to date

Estimated cost to complete

—

Estimated total cost

Estimated total gross profit

$300,000

$300,000

$290,000

Gross profit recognized in—

2014:

$270,000

X $300,000 =

$135,000

$600,000

2015:

$450,000

X $300,000 =

$600,000

(b) In 2014 and 2015, no gross profit would be recognized.

Total billings ……………………………….. $900,000

PROBLEM 18-3

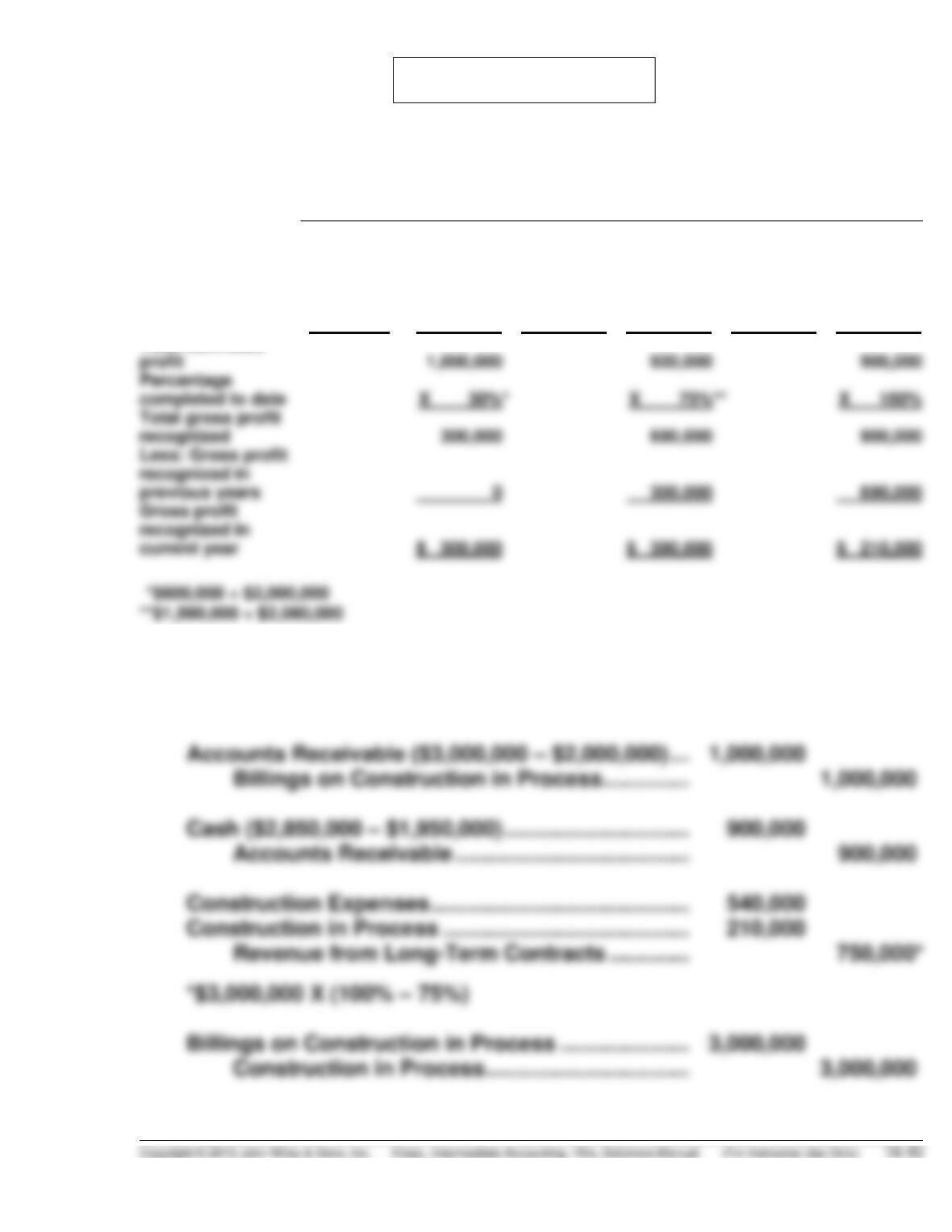

(a) Gross profit recognized in:

2014

2015

2016

Contract price

$3,000,000

$3,000,000

$3,000,000

Costs:

Costs to date

$ 600,000

$1,560,000

$2,100,000

Estimated costs

to complete

1,400,000

2,000,000

520,000

2,080,000

0

2,100,000

profit

920,000

Total gross profit

recognized

recognized in

previous years

300,000

690,000

recognized in

current year

$ 390,000

$ 210,000

Total estimated

(b) Construction in Process

($2,100,000 – $1,560,000) ………………………………… 540,000

Materials, Cash, Payables. ……………………….. 540,000

PROBLEM 18-3 (Continued)

(c) CHANCE COMPANY

Balance Sheet (Partial)

December 31, 2015

Current assets:

Accounts receivable

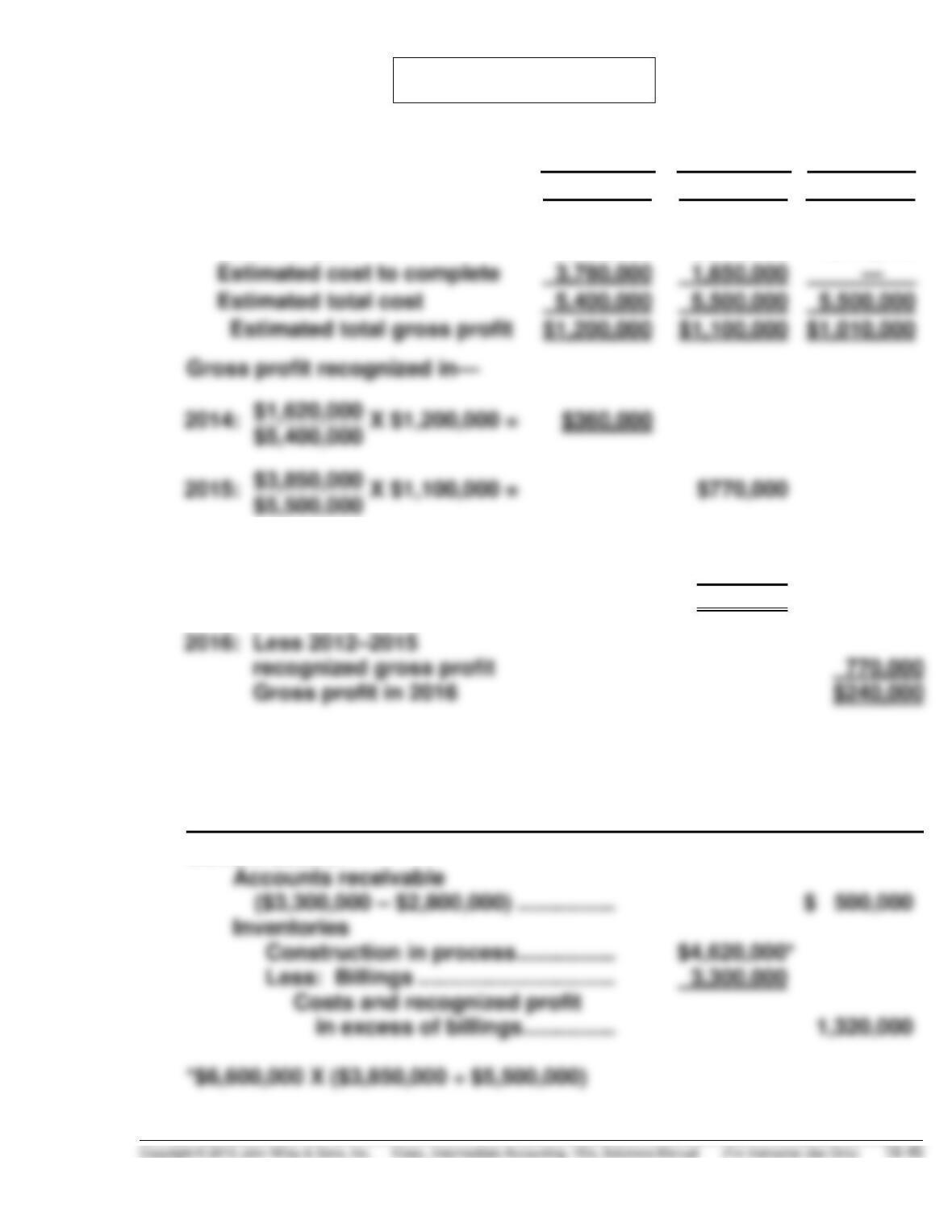

PROBLEM 18-4

(a)

2014

2015

2016

Contract price

$6,600,000

$6,600,000

$6,510,000

Less estimated cost:

Costs to date

1,620,000

3,850,000

5,500,000

Estimated cost to complete

—

Estimated total cost

Estimated total gross profit

$1,200,000

$1,100,000

$1,010,000

$5,400,000

$5,500,000

Less 2014 recognized

gross profit

360,000

Gross profit in 2015

$410,000

Gross profit in 2016

(b) HEWITT CONSTRUCTION COMPANY

Balance Sheet

December 31, 2015

Current assets:

PROBLEM 18-5

(a) The completed-contract method of revenue recognition recognizes income

only upon completion of a project or shipment of a product. All associ-

ated costs are expensed at the point of sale, and there are no interim

(b) Using the data provided for the Bluestem Tractor Plant, and on the

assumption that the percentage–of–completion method of revenue recog-

nition is used, the calculations of RCB’s revenue and gross profit for

Percentage-of–Completion

($000 omitted)

Year

Contract

Price

Costs

to Date

Estimated

Total

Costs

Estimated

Gross Profit

(Col. 2–Col. 4)

Percent

Complete

(Col. 3/Col. 4)

(1)

(2)

(3)

(4)

(5)

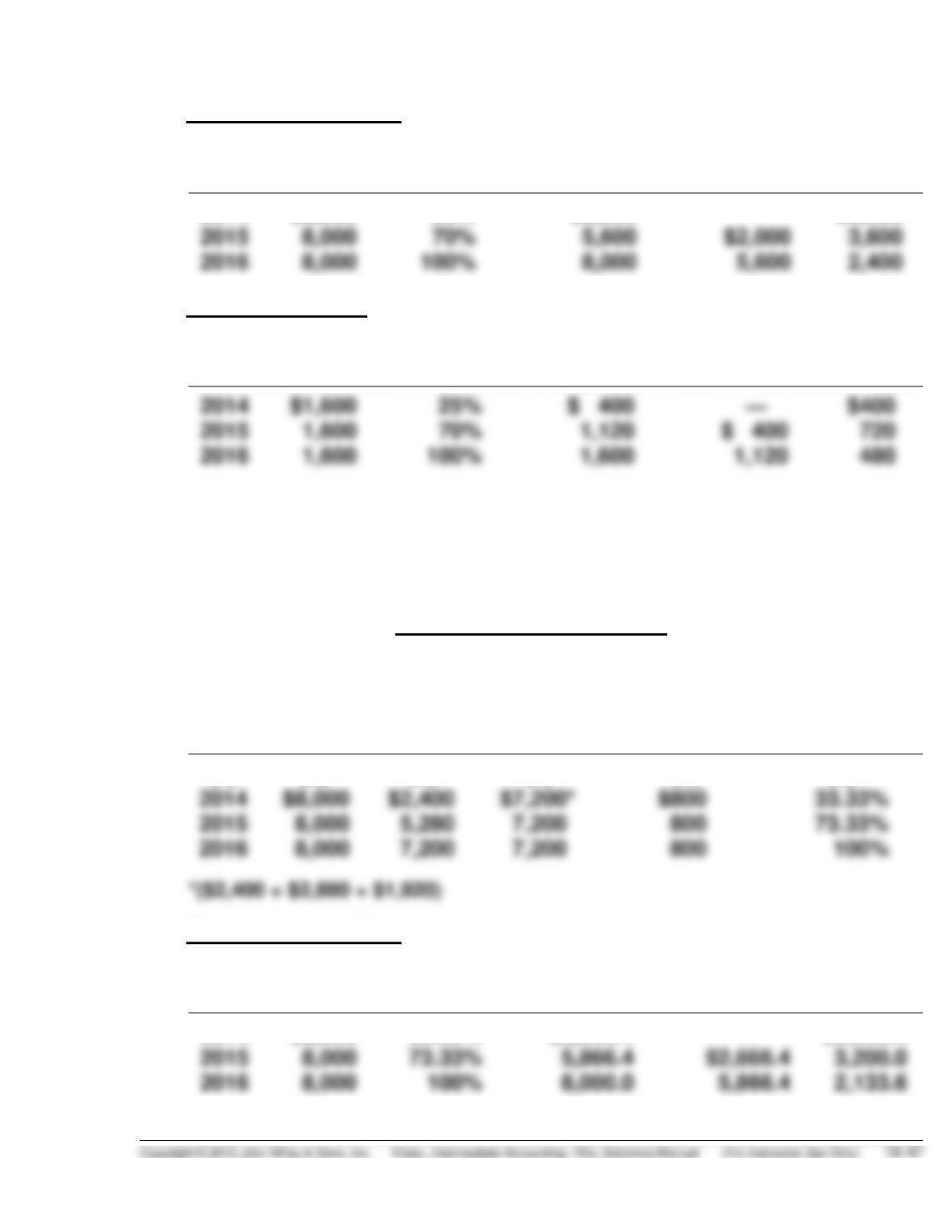

(6)

2014

$8,000

$1,600

$6,400*

$1,600

25%

2015

4,480

70%

2016

6,400

PROBLEM 18-5 (Continued)

Revenue recognition

Year

Contract

Price

Percent

Complete

Revenue

Recognizable

Less Prior

Year(s)

Current

Year

2014

$8,000

25%

$2,000

—

$2,000

2015

70%

$2,000

3,600

Profit recognition

Year

Estimated

Profit

Percent

Complete

Profit

Recognizable

Less Prior

Year(s)

Current

Year

2014

$1,600

2. Assuming the same facts as in Instruction (b) 1., but that cost

overruns of $800,000 were experienced in 2014, RCB’s revenue,

cost of sales, and gross profit for 2014, 2015, and 2016 were

calculated as follows:

Percentage-of–Completion

($000 omitted)

Year

Contract

Price

Costs

to Date

Estimated

Total

Costs

Estimated

Gross Profit

(Col. 2–Col. 4)

Percent

Complete

(Col. 3/Col. 4)

(1)

(2)

(3)

(4)

(5)

(6)

7,200

Revenue recognition

Year

Contract

Price

Percent

Complete

Revenue

Recognizable

Less Prior

Year(s)

Current

Year

2014

$8,000

33.33%

$2,666.4

—

$2,666.4

PROBLEM 18-5 (Continued)

Profit recognition

Year

Estimated

Profit

Percent

Complete

Profit

Recognizable

Less Prior

Year(s)

Current

Year

2014

$800

33.33%

$266.6

—

$266.6

2015

73.33%

3. Assuming the same facts as in Instructions (b) 1. and (b) 2., but

that additional cost overruns of $850,000 are experienced in 2015,

RCB’s revenue, cost of sales, and gross profit for 2014, 2015, and

2016 are calculated as follows:

Percentage-of–Completion

($000 omitted)

Year

Contract

Price

Costs

to Date

Estimated

Total

Costs

Estimated

Gross Profit

(Col. 2–Col. 4)

Percent

Complete

(Col. 3/Col. 4)

(1)

(2)

(3)

(4)

(5)

(6)

Revenue recognition

Year

Contract

Price

Percent

Complete

Revenue

Recognizable

Less Prior

Year(s)

Current

Year

2014

$8,000

33.33%

$2,666.4

—

$2,666.4

2016

1,908.0

Profit recognition

Year

Estimated

Profit

Percent

Complete

Profit

Recognizable

Less Prior

Year(s)

Current

Year

2014

$800

33.33%

$266.6

—

$266.6

2015

(50)

(50)

(316.6)

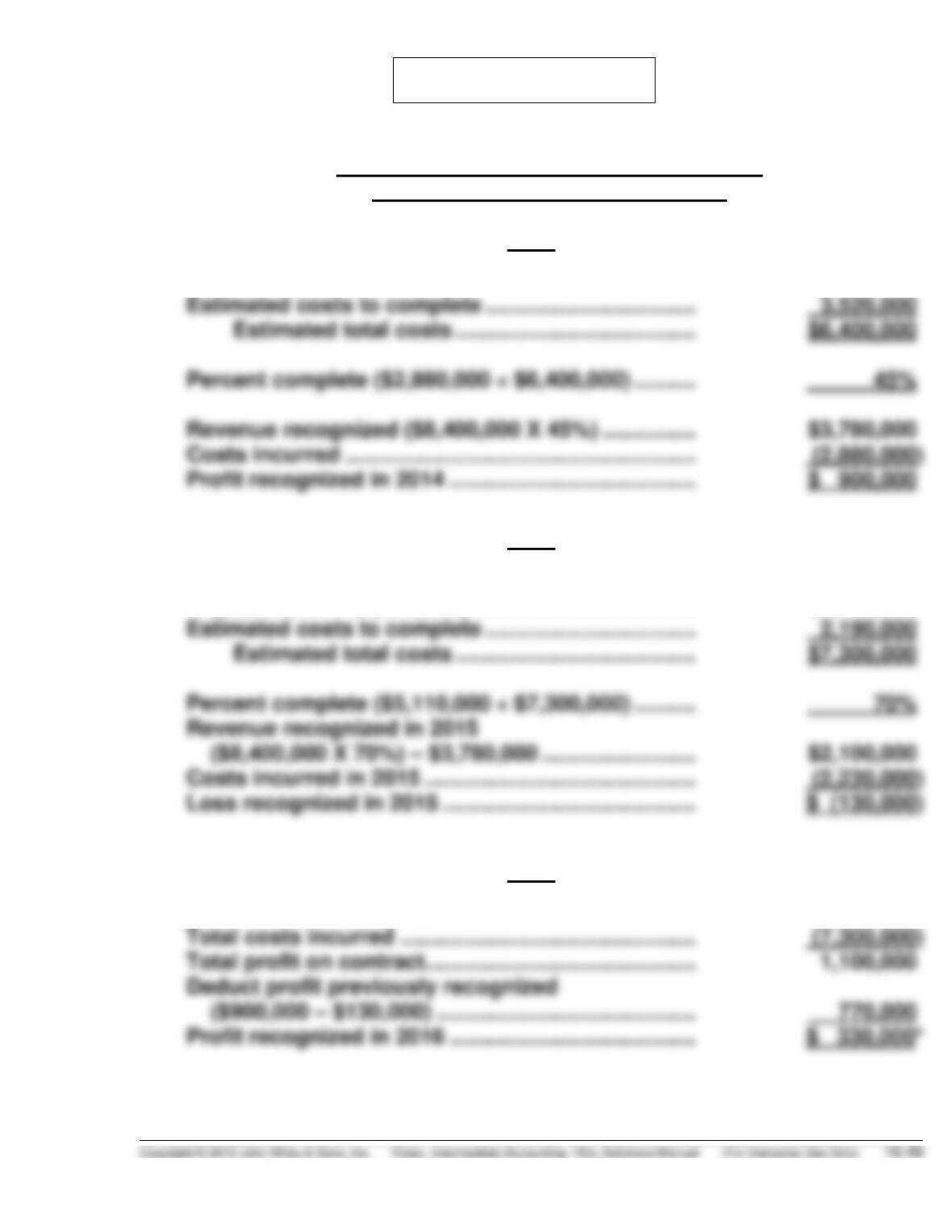

PROBLEM 18-6

(a) Computation of Recognizable Profit/Loss

Percentage-of–Completion Method

2014

Costs to date (12/31/14) ……………………………………. $2,880,000

2015

Costs to date (12/31/15)

($2,880,000 + $2,230,000)………………………………. $5,110,000

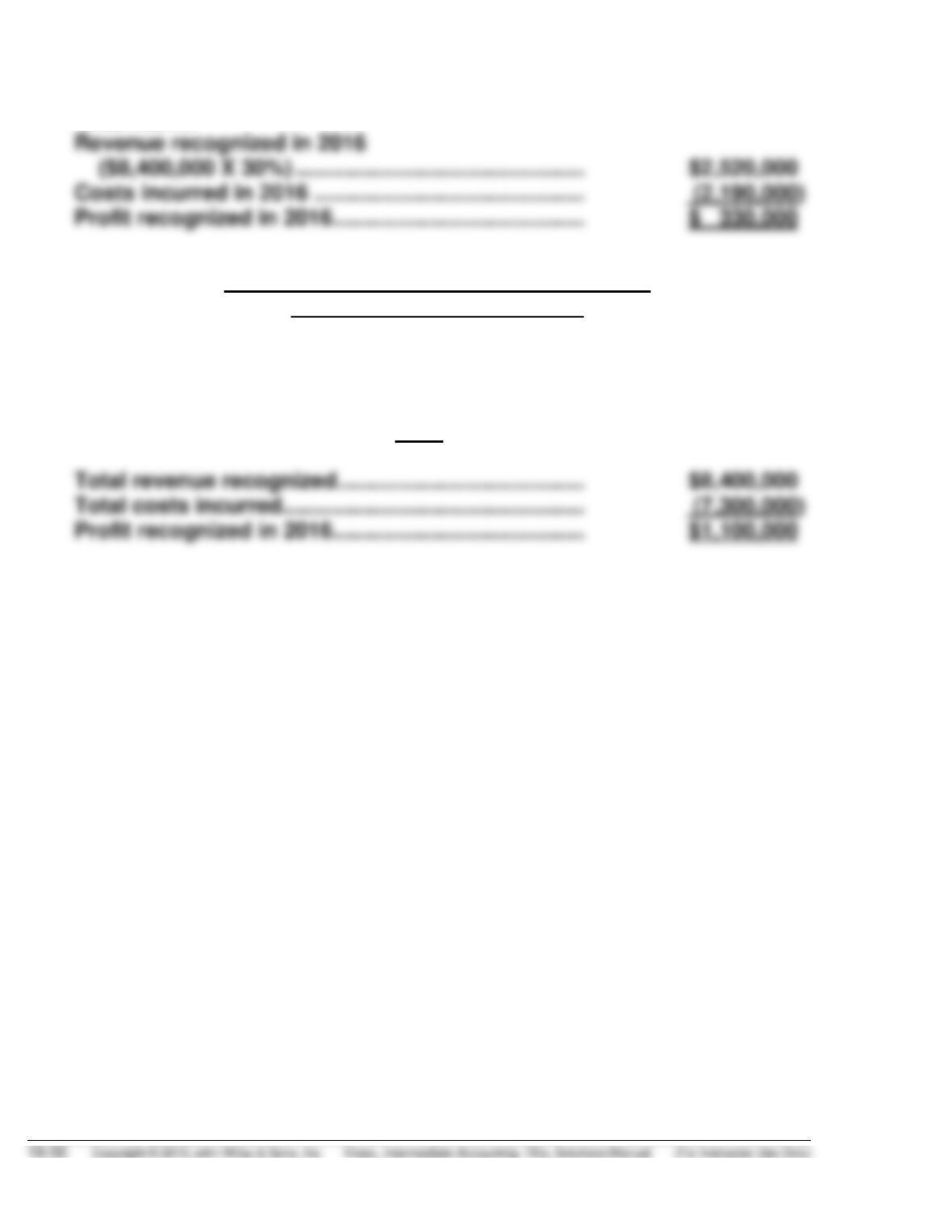

2016

Total revenue recognized …………………………………. $8,400,000

PROBLEM 18-6 (Continued)

*Alternative

(b) Computation of Recognizable Profit/Loss

Completed-Contract Method

2014—NONE

2015—NONE

2016

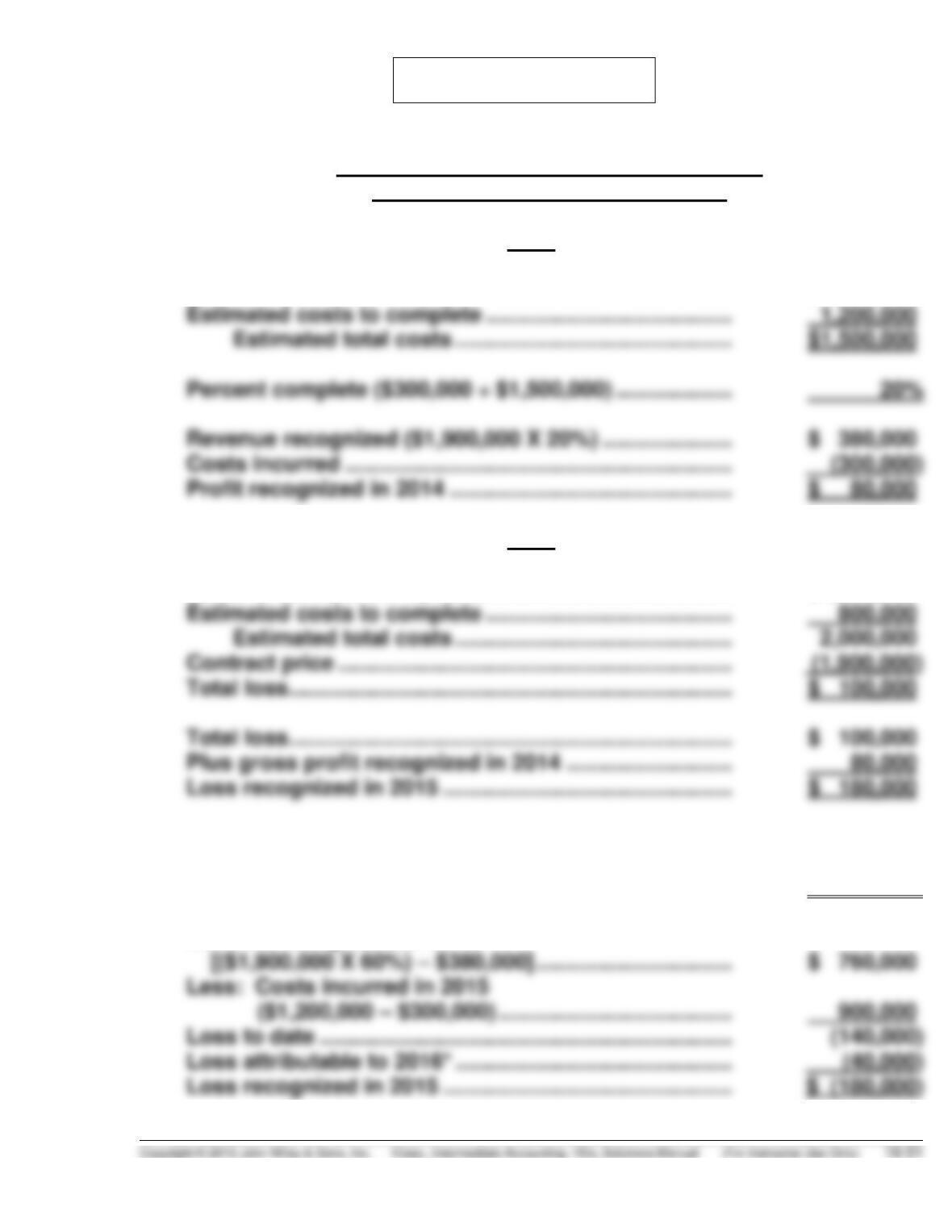

PROBLEM 18-7

(a) Computation of Recognizable Profit/Loss

Percentage-of–Completion Method

2014

Costs to date (12/31/14) …………………………………………. $ 300,000

2015

Costs to date (12/31/15) …………………………………………. $1,200,000

OR

Percent complete ($1,200,000 ÷ $2,000,000) ……………. 60%

Revenue recognized in 2015

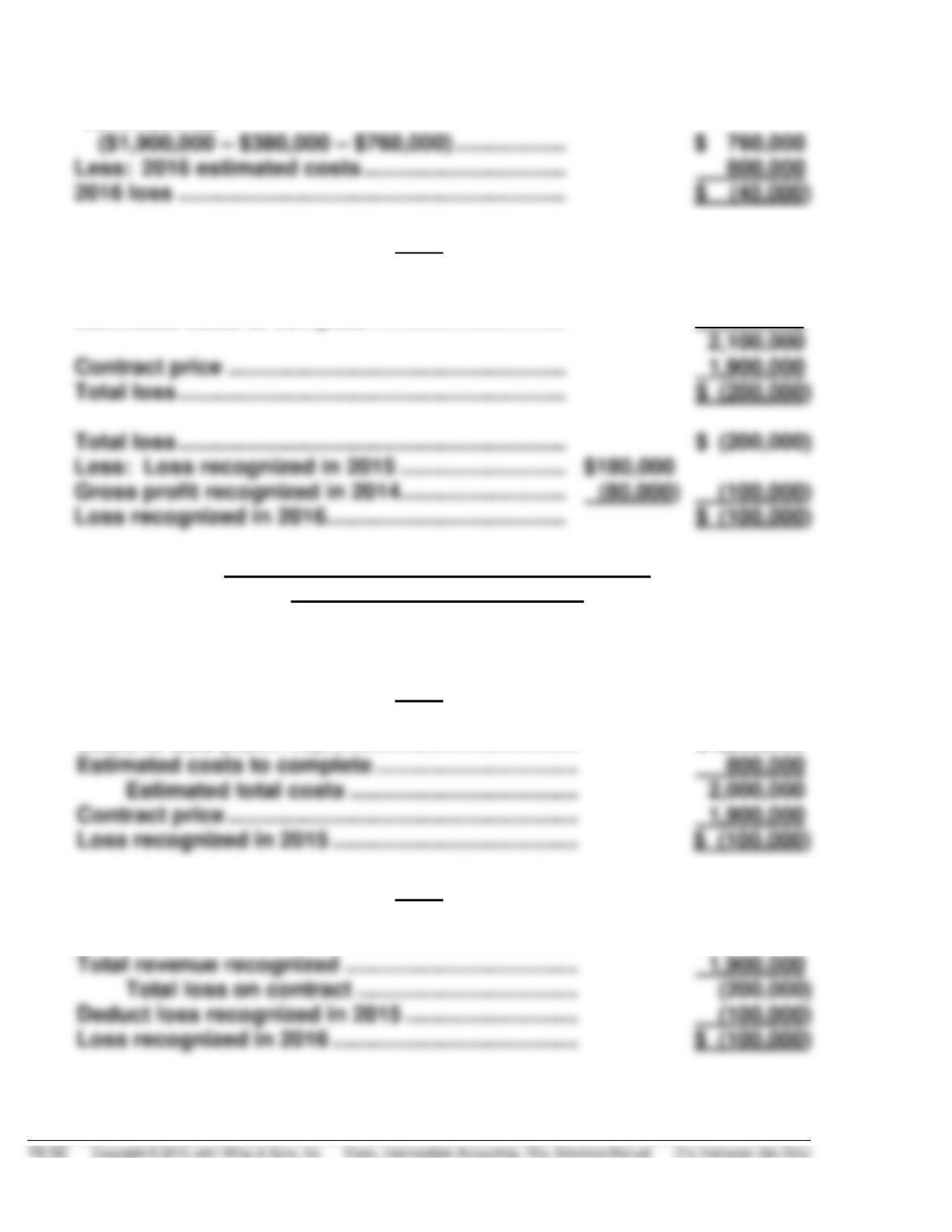

PROBLEM 18-7 (Continued)

*2016 revenue

2016

Costs to date (12/31/16) …………………………………. $2,100,000

Estimated costs to complete …………………………. 0

(b) Computation of Recognizable Profit/Loss

Completed-Contract Method

2014—NONE

2015

Costs to date (12/31/15)…………………………………… $1,200,000

2016

Total costs incurred ……………………………………….. $2,100,000

PROBLEM 18-8

(a)

Rate of gross profit

(

Gross profit

Sales

)

2014

2015

2016

38%

37%

35%

Gross profit realized:

38% of $ 75,000

38% of $100,000

37% of $100,000

38% of $ 50,000

37% of $120,000

35% of $100,000

(b) Installment Accounts Receivable, 2016 ………………. 280,000

Installment Sales Revenue ………………………….. 280,000

Cash …………………………………………………………………. 270,000

Deferred Gross Profit, 2014 …………………………………. 19,000

Deferred Gross Profit, 2015 …………………………………. 44,400

Deferred Gross Profit, 2016 …………………………………. 35,000

Realized Gross Profit ………………………………….. 98,400

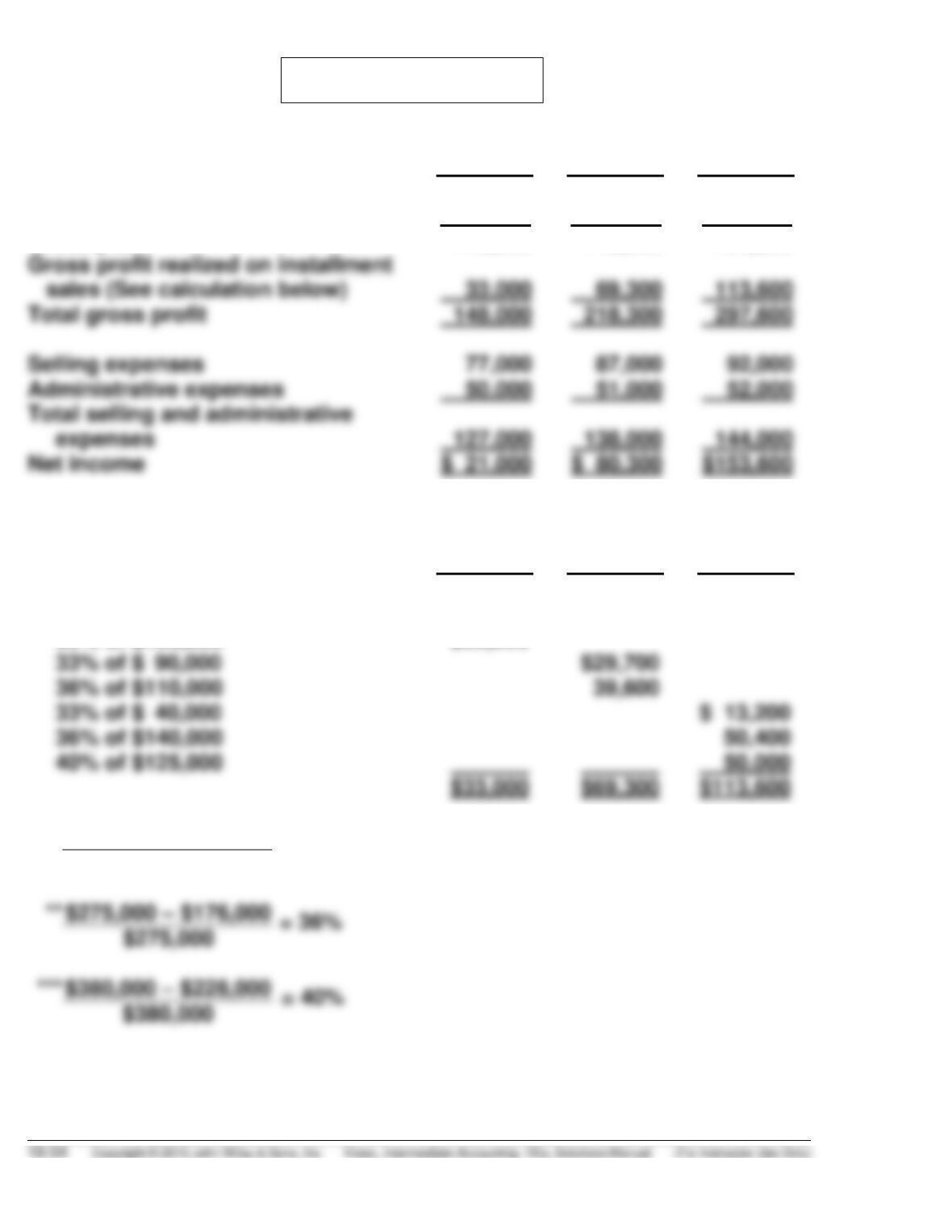

PROBLEM 18-9

2014

2015

2016

Sales

$385,000

$426,000

$525,000

Cost of sales

270,000

277,000

341,000

Gross profit

115,000

149,000

184,000

Total gross profit

Selling expenses

Administrative expenses

50,000

51,000

52,000

Net income

$ 21,000

$ 80,300

$153,600

Calculation of gross profit realized on installment sales:

2014

2015

2016

Rate of gross profit

* 33%*

** 36%**

40%***

Gross profit realized:

33% of $100,000

$33,000

33% of $ 90,000

33% of $ 40,000

36% of $140,000

40% of $125,000

$33,000

*

$320,000 – $214,400

*= 33%

$320,000

$275,000 – $176,000

$275,000

$380,000 – $228,000

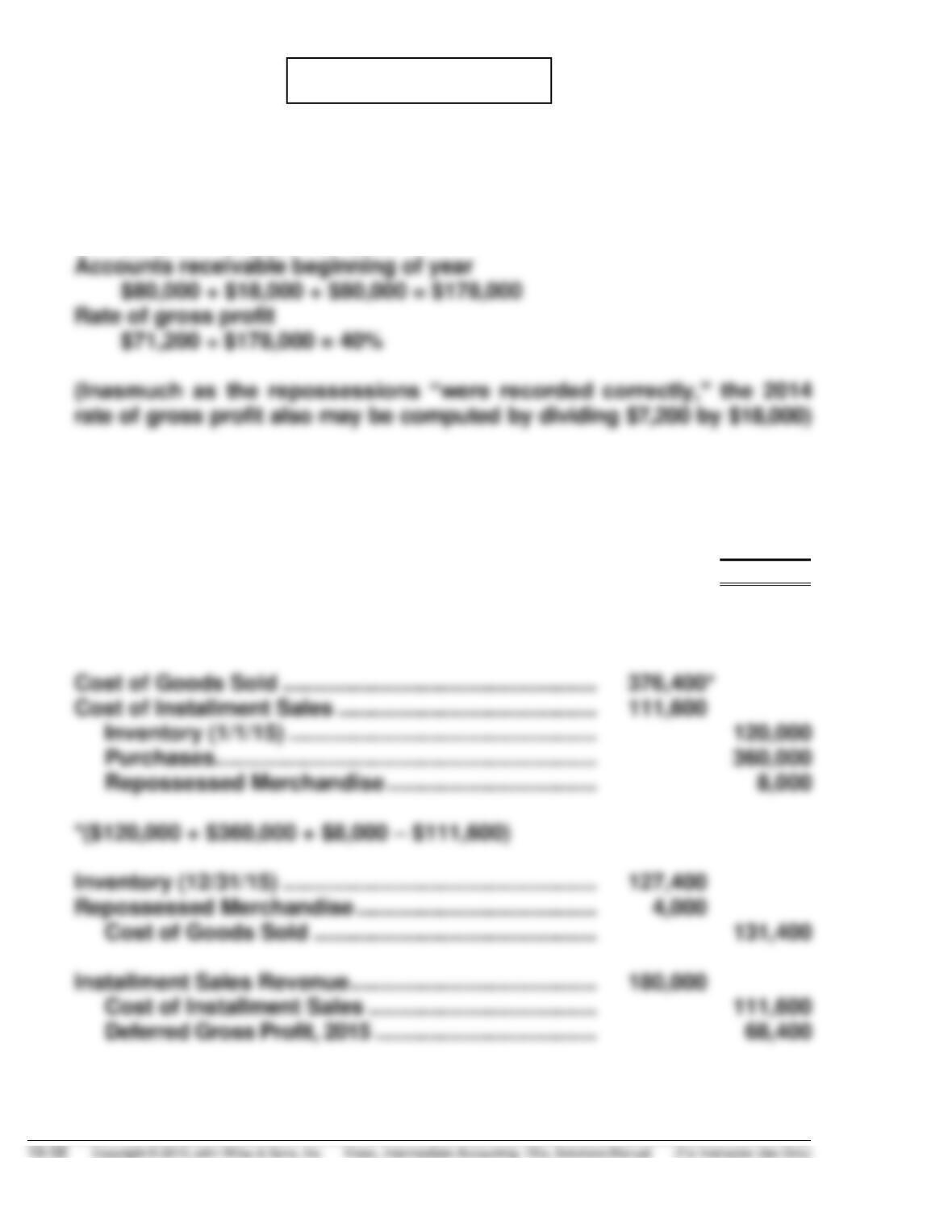

PROBLEM 18-10

(a) Rate of gross profit on 2014 installment sales:

Deferred gross profit on repossessions

(b) Installment Sales Revenue ………………………………. 200,000

Cost of Installment Sales ………………………….. 120,000

Deferred Gross Profit, 2015 ………………………. 80,000

PROBLEM 18-10 (Continued)

(c) PAUL DOBSON STORES

Income Statement

For the Year Ended December 31, 2015

Sales revenue ………………………………………………….. $343,000

PROBLEM 18-11

(a) Installment Accounts Receivable, 2014 ……………. 500,000

Installment Sales Revenue ……………………….. 500,000

*Rate of gross profit =

$150,000

= 30%

$500,000

30% X $24,000 = $7,200

**[$11,200 – ($24,000 – $7,200)]

PROBLEM 18-12

(a) Rate of gross profit—2014:

Deferred gross profit beginning of year

$64,000 + $7,200 = $71,200

Rate of gross profit—2015:

Installment sales revenue ………………………………….. $180,000

Cost of installment sales ……………………………………. 111,600

Gross profit ………………………………………………………. $ 68,400

Rate of gross profit—2015 = $68,400 ÷ $180,000 = 38%

PROBLEM 18-12 (Continued)

Deferred Gross Profit, 2014 ………………………………… 32,000

Deferred Gross Profit, 2015 ………………………………… 19,000

Realized Gross Profit ………………………………….. 51,000

(40% X $80,000 = $32,000;

38% X $50,000 = $19,000)

(b) MANTLE INC.

Income Statement

For the Year Ended December 31, 2015

Sales revenue …………………………………….. $400,000

Cost of goods sold:

Inventory, January 1 …………………….. $120,000

Purchases ………………………………….. 360,000

Merchandise repossessed ……………. 8,000

PROBLEM 18-13

-1-

November 1, 2014

-2-

December 1, 2014

Cash …………………………..……………………………………………….. 30

Installment Accounts Receivable, 2014 …………………… 30

-3-

December 31, 2014

Cost of Installment Sales ………………………………………………. 540

Inventory ………………………………………………………………. 540

-4-

January 1 to July 1, 2015

Cash ($30 X 7) …………………………..………………………………….. 210

Installment Accounts Receivable, 2014 …………………… 210

-5-

August, 2015

Repossessed Merchandise ……………………………………………. 100