PROBLEM 10-9 (Continued)

Wiggins, Inc.’s Books

Cash ………………………………………………………………

15,000

Machienry (A) …………………………………………………

50,400**

Accumulated Depreciation—Machinery (B) ………

47,000

Machinery (B) ………………………………………….

Gain on Disposal of Machinery …………………

Computation of total gain:

Fair value of Asset B

Less: Book value of Asset B

*Gain recognized =

$15,000

X $12,000 = $2,400

$15,000 + $60,000

**Fair value of asset acquired

$60,000

Less: Gain deferred ($12,000 – $2,400)

9,600

Book value of Machinery B

Less: Portion of book value sold

Note to instructor: This illustrates the exception to no gain or loss

recognition for exchanges that lack commercial substance. Although

PROBLEM 10-10

(a) Has Commercial Substance

Marshall Construction

1.

Equipment ($82,000 + $118,000) ………………….

200,000

Accumulated Depreciation—Equipment ……..

50,000

Loss on Disposal of Equipment ………………….

8,000*

Equipment …………………………………………

Cash …………………………………………………

Brigham Manufacturing

2.

Cash …………………………………………………………

118,000

Inventory …………………………………………………..

82,000

Sales Revenue …………………………..………

Cost of Goods Sold ……………………………………

165,000

Inventory …………………………………………..

(b) Lacks Commercial Substance

1. Marshall Construction should record the same entry as in part (a)

above, since the exchange resulted in a loss.

2. Brigham should record the same entry as in part (a) above. No

PROBLEM 10-10 (Continued)

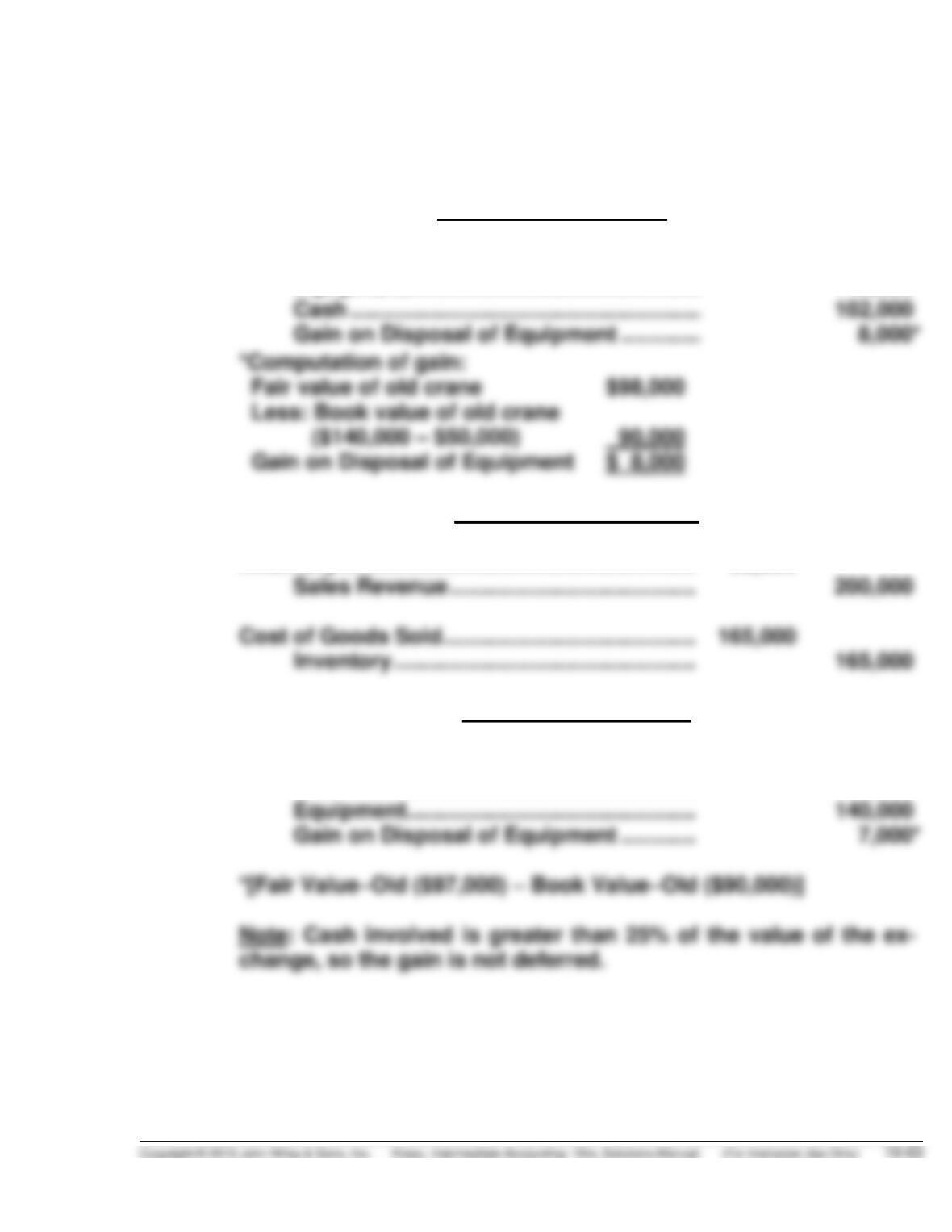

(c) Has Commercial Substance

Marshall Construction

1.

Equipment ($98,000 + $102,000)………………….

200,000

Accumulated Depreciation—Equipment ……..

50,000

Equipment…………………………………………

140,000

Cash …………………………………………………

102,000

Gain on Disposal of Equipment ………….

Brigham Manufacturing

2.

Cash ………………………………………………………..

102,000

Inventory ………………………………………………….

98,000

Sales Revenue ………………………………….

200,000

Cost of Goods Sold …………………………………..

165,000

Inventory ………………………………………….

165,000

(d)

Marshall Construction

1.

Equipment ……………………………………………….

200,000

Accumulated Depreciation—Equipment …….

50,000

Cash ………………………………………………..

103,000

Equipment………………………………………..

140,000

Gain on Disposal of Equipment …………

*[Fair Value–Old ($97,000) – Book Value–Old ($90,000)]

change, so the gain is not deferred.

PROBLEM 10-10 (Continued)

Brigham Manufacturing

2.

Cash ……………………………………………………….

103,000

Inventory ………………………………………………….

97,000

Sales Revenue …………………………..……..

200,000

Cost of Goods Sold …………………………………..

Inventory ………………………………………….

165,000

PROBLEM 10-11

(a) The major characteristics of plant assets, such as land, buildings, and

equipment, that differentiate them from other types of assets are

presented below.

1. Plant assets are acquired for use in the regular operations of the

enterprise and are not for resale.

(b) Transaction 1. To properly reflect cost, assets purchased on deferred

payment contracts should be accounted for at the present value of the

consideration exchanged between the contracting parties at the date

of the consideration. When no interest rate is stated, interest must

PROBLEM 10-11 (Continued)

Transaction 2. The lump-sum purchase of a group of assets should be

accounted for by allocating the total cost among the various assets

on the basis of their relative fair values. The $8,000 of interest

expense incurred for financing the purchase is a period cost and is

not a factor in determining asset cost.

Inventory $220,000 X ($ 50,000/$250,000) = $ 44,000

(c) 1. A building purchased for speculative purposes is not a plant

asset as it is not being used in normal operations. The building

is more appropriately classified as an investment.

2. The two-year insurance policy covering plant equipment is not a

plant asset because it has no physical substance and is not

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 10-1 (Time 20–25 minutes)

Purpose—to provide the student with a problem to decide which expenditures related to purchasing

CA 10-2 (Time 20–25 minutes)

Purpose—to provide the student with a situation involving the proper allocation of costs to self–

CA 10-3 (Time 30–40 minutes)

Purpose—to provide the student with a situation to determine capitalization of interest and to explain in

a memorandum the conceptual basis for interest capitalization.

CA 10-4 (Time 30–40 minutes)

CA 10-5 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the proper accounting treatment involving

CA 10-6 (Time 20–25 minutes)

Purpose—to provide the student with a case involving allocation of costs between land and buildings,

including ethical issues.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 10-1

(a) Expenditures should be capitalized when they benefit future periods. The cost to acquire the land

should be capitalized and classified as land, a nondepreciable asset. Since tearing down the small

factory is readying the land for its intended use, its cost is part of the cost of the land and should

(b) A gain should be recognized on the sale of the land and building because income is realized

whenever the earning process has been completed and a sale has taken place.

The net book value at the date of sale would be composed of the capitalized cost of the land, the

CA 10-2

(a) Materials and direct labor used in the construction of the equipment definitely should be charged to

the equipment account. It should be emphasized that no gain on self-construction should be

recorded because such an approach violates the historical cost principle. The controversy centers

on the assignment of indirect costs, called overhead or burden, consisting of power, heat, light,

insurance, property taxes on factory buildings, etc. The suggested approaches are discussed below.

(b) 1. Many believe that only the variable overhead costs that increase as a result of the construction

should be assigned to the cost of the asset. This approach assumes that the company will

have the same fixed costs regardless of whether the company constructs the asset or not, so

CA 10-2 (Continued)

CA 10-3

To: Jane Esplanade, President

From: Good Student, Manager of Accounting

Date: January 15, 2014

Subject: Capitalization of avoidable interest on the warehouse

construction project

I am writing in response to your questions about the capitalized interest

costs for the warehouse construction project. This brief explanation of my

calculations should facilitate your understanding of these costs.

Generally, the accounting profession does not allow accrued interest to be

capitalized along with an asset’s cost. However, the FASB made an excep-

To determine the amount capitalized, we must calculate both the actual and

the avoidable interest during 2013. Actual interest is computed by applying

the interest rates of 12%, 10%, and 11% to their related debt. Thus, total

actual interest for this period is $490,000 (see Schedule #1).

CA 10-3 (Continued)

Calculations for avoidable interest are more complex. First, interest can be

capitalized only on the weighted-average amount of accumulated expenditures.

Although total costs amounted to $5,200,000 for the project, an average of

only $3,500,000 was outstanding during the period of construction.

Second, of the total $4,400,000 debt outstanding during this period, only

Third, we compute our avoidable interest as follows: calculate the interest

on the loan directly associated with the construction. Apply the weighted–

average interest rate to the remainder of the weighted-average accumulated

expenditures. Add these products. Avoidable interest for 2013 amounts to

$396,300 (see Schedule #3).

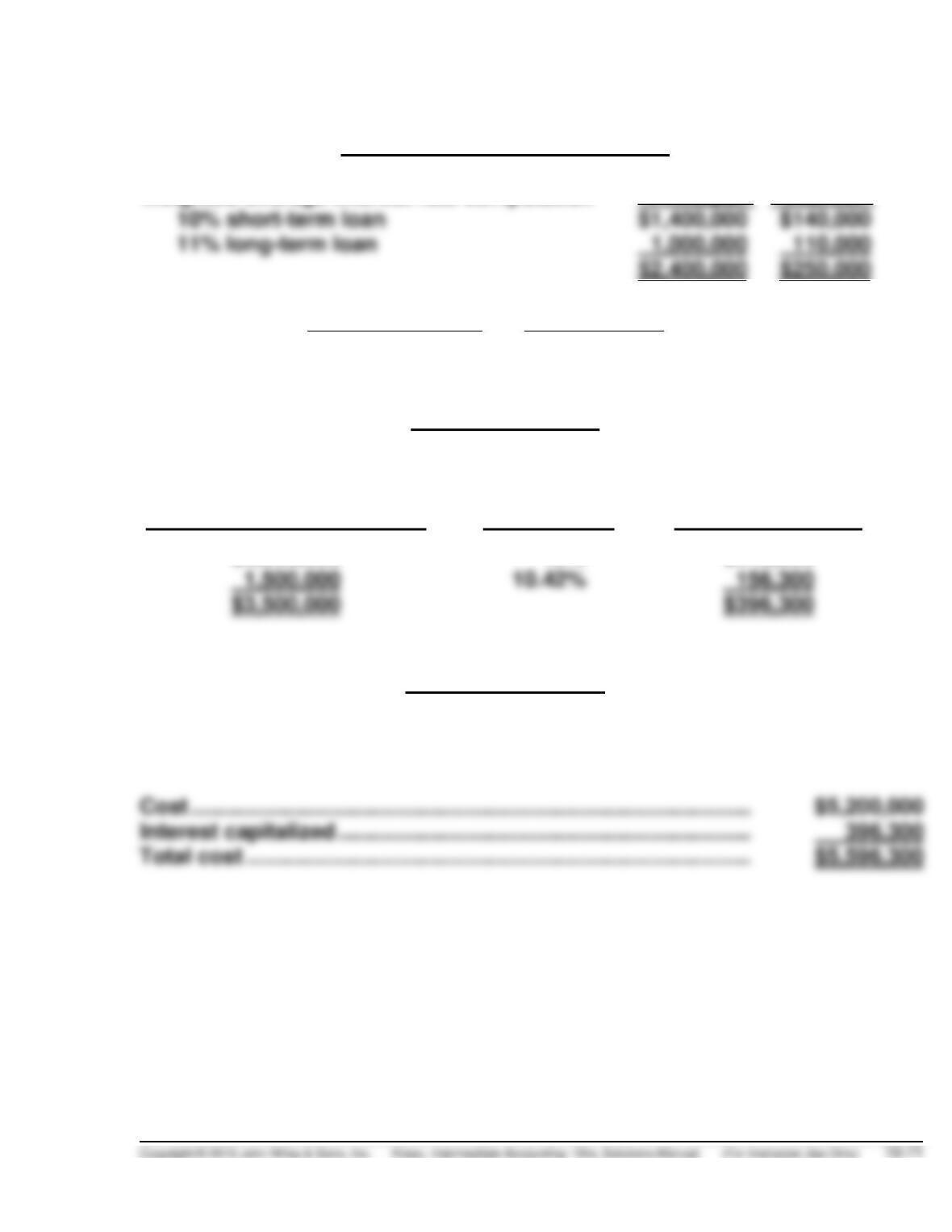

Schedule #1

Actual Interest

Construction loan

$2,000,000 X 12% =

$240,000

Short-term loan

$1,400,000 X 10% =

140,000

Long-term loan

$1,000,000 X 11% =

CA 10-3 (Continued)

Schedule #2

Weighted-Average Interest Rate

Weighted-average interest rate computation

Principal

Interest

10% short-term loan

$1,400,000

11% long-term loan

$2,400,000

Total Interest

=

$250,000

= 10.42%

Total Principal

$2,400,000

Schedule #3

Avoidable Interest

Weighted-Average

Accumulated Expenditures

X

Interest Rate

=

Avoidable Interest

$2,000,000

12%

$240,000

10.42%

Schedule #4

Interest Capitalized

Because avoidable interest is lower than actual interest, use avoidable

interest.

Cost ……………………………………………………………………………….

Interest capitalized ………………………………………………………….

Total cost …………………………..…………………………………………..

CA 10-4

(a) Client A

Treatment if the exchange has commercial substance

Client A would recognize a gain of $20,000 on the exchange. The basis of the asset acquired

would be $100,000. The entry would be as follows:

(b) Treatment if the exchange lacks commercial substance

Client A would be prohibited from recognizing a $20,000 gain on the exchange. This is because

the transaction lacks commercial substance. The new asset on their books would have a basis of

(c) Memo to the Controller:

TO: The Controller

RE: Exchanges of Assets—Commercial Substance Issues.

Financial statement effect of treating the exchange as having commercial substance versus not.

1. The income statement will reflect a before-tax gain of $20,000. This gain will increase the

reported income on this year’s financial statements. Future income statements will show a

CA 10-4 (Continued)

(d) Client B

Treatment if the exchange has commercial substance

In this situation, the full $30,000 gain would be recognized on this year’s income statement. The

new asset would go on the books at its fair value. The entry is as follows:

Machinery …………………………………………………………………………………..

80,000

Accumulated Depreciation—Machinery …………………………………………..

80,000

Cash ……………………………………………………….…………………………………

20,000

Gain on Disposal of Machinery………………………………………………..

Gain on disposal of machinery $ 30,000

(e) Treatment if the exchange lacks commercial substance

Machinery ($80,000 – $24,000) …………………………..………………………….

56,000

80,000

20,000

Machinery …………………………………………………………………………….

Gain on Disposal of Machinery ………………………………………………..

(f) Memo to the Controller:

TO: The Controller

RE: Asset Exchanges—Commercial Substance

1. The income statement will reflect a before-tax gain of $30,000 if the exchange has commercial

substance. This gain will increase the reported income on this year’s financial statements.

CA 10-5

In general, the inclusion of the $7,500 as part of the cost of the machine is justified because the primary

(1) It may be true that these installation costs could not be recovered if the machine were to be sold.

This is not important, however, because presumably the machine was acquired to be used, not to

(2) Again, the purpose of accounting for plant assets is not to arrive at an approximation of fair

value of the assets each year over the life of the assets. However, even if this were an objective,

the question of which method would come closer to stating current market value at some later date

would revolve around the general trend of the price level over the years involved.

(3) Assuming that the $7,500 could properly be deducted, there would be some tax savings over the

years unless the tax rates applicable to the business were reduced during the following years.

CA 10-6

(a) If the land is undervalued so that a higher depreciation expense is assigned to the building,

management interests are served. The lower net income and reduced tax liability save cash to be

used for management purposes. By contrast, stockholders and potential investors are misled by

FINANCIAL STATEMENT ANALYSIS CASE

JOHNSON & JOHNSON ($ millions)

(a) The cost of building and building equipment at the end of 2009 was

$9,389.

(b) As indicated in footnote number 1 to the financial statements, the

company utilizes the straight-line method for financial statement

(c) The cash flow statement reports the amount of interest paid in cash

($576).

A review of the income statement indicates that Johnson & Johnson

(d) Free cash flow is defined as net cash flows provided by operating

activities less capital expenditures and dividends.

Free cash flow is the amount of discretionary cash flow a company has

For example, the company is able to pay its dividends without resorting

to external financing. Secondly, even if operations decline, it appears

that the company will be able to fund additions to property, plant, and

equipment. Thirdly, the company is using its free cash flow to expand its

operations by acquiring new businesses.

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

Equipment** ……………………………………………………….

62,000

Accumluated Depreciation—Equipment …………………..

80,000

Equipment ………………………………………………………

Cash ………………………………………………………………

Gain on Disposal of Equipment * ……………………..

*Fair value of old asset

Less: Cost of old asset

Gain on disposal of equipment

**Cash paid

Fair value of old equipment

Analysis

The gain on the disposal increases income, leading to a one-time increase

in the return on assets in the year of the exchange. In essence, the gain

Principles

The concept of commercial substance is a fundamental element in the

accounting for exchanges. If the transaction above lacked commercial

substance, the gain on the exchange would be deferred. That is, if the

PROFESSIONAL RESEARCH

(a) Yes; according to FASB ASC 835-20–05, it is required to capitalize interest

into the cost of assets that meet selected criteria (see (c) below).

(b) According to FASB ASC 835-20–10–1,

. . . the objectives of capitalizing interest are to obtain a measure of

(c) According to FASB ASC 835-20–15–5,

. . . interest shall be capitalized for the following types of assets

(qualifying assets):

a. Assets that are constructed or otherwise produced for an entity’s

own use, including assets constructed or produced for the entity by

others for which deposits or progress payments have been made.

(d) According to FASB ASC 835-20–30–6,

. . . the total amount of interest cost capitalized in an accounting period

shall not exceed the total amount of interest cost incurred by the entity

in that period. In consolidated financial statements, that limitation shall

be applied by reference to the total amount of interest cost incurred by

PROFESSIONAL RESEARCH (Continued)

(e) According to FASB ASC 835-20–50–1,

An entity shall disclose the following information with respect to

interest cost in the financial statements or related notes:

a. For an accounting period in which no interest cost is capitalized, the

PROFESSIONAL SIMULATION

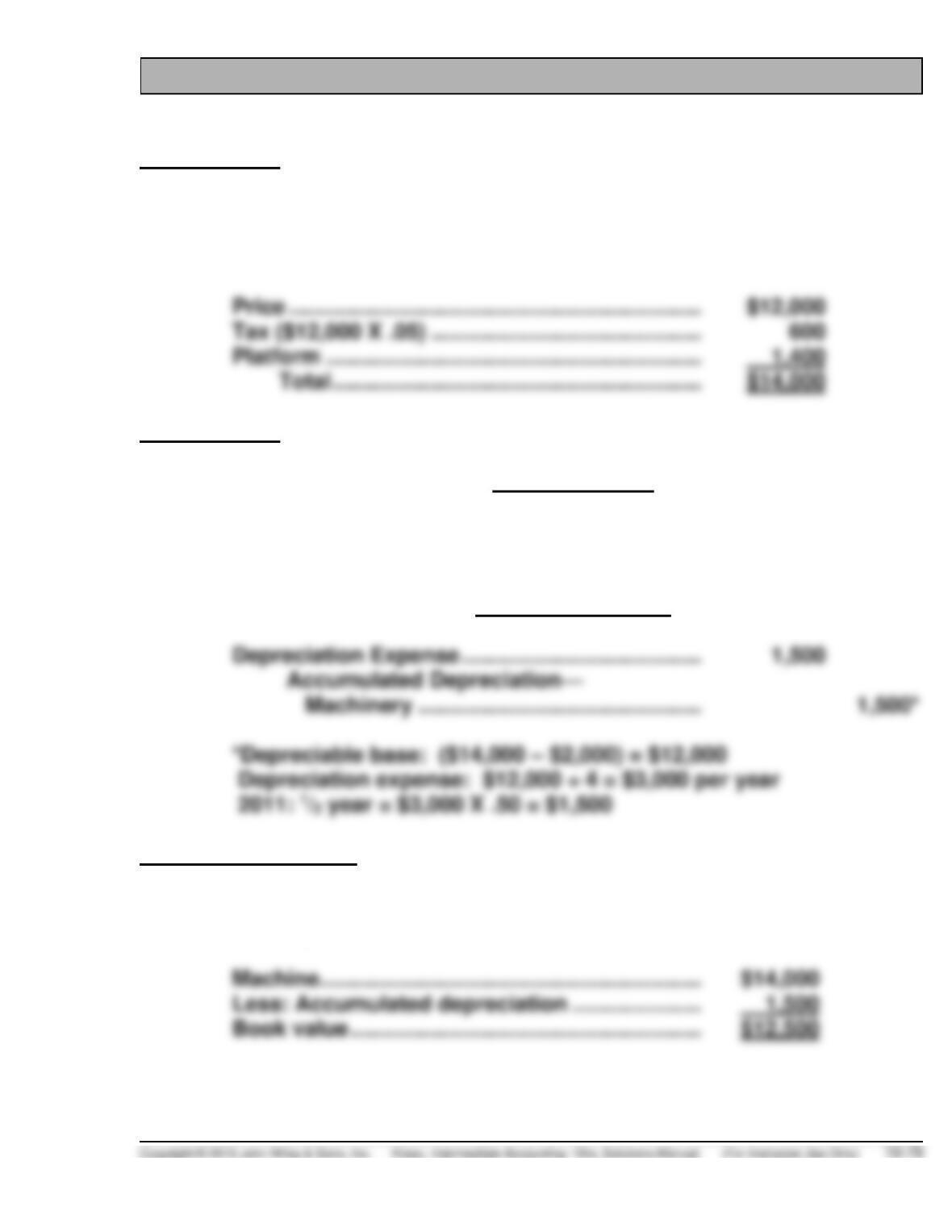

Measurement

Historical cost is measured by the cash or cash-equivalent price of obtain–

ing the asset and bringing it to the location and condition for its intended

use. For Norwel, this is:

Price ………………………………………………………….

Tax ($12,000 X .05) ……………………………………..

Platform …………………………………………………….

Journal Entry

January 2, 2014

Machinery ………………………………………………….

14,000

Cash ………………………………………………….

14,000

December 31, 2014

Depreciation Expense …………………………………

*Depreciable base: ($14,000 – $2,000) = $12,000

Depreciation expense: $12,000 ÷ 4 = $3,000 per year

Financial Statements

The amount reported on the balance sheet is the cost of the asset less

accumulated depreciation:

Machine ……………………………………………………..

Less: Accumulated depreciation …………………

Book value …………………………………………………

PROFESSIONAL SIMULATION (Continued)

Analysis

The income effect is a gain or loss, determined by comparing the book

value of the asset to the disposal value:

Cost ……………………………………………………………………

$14,000

Less: Cash received for machine and platform ……..