FINANCIAL REPORTING PROBLEM (Continued)

(c) P&G provided the following discussion related to commitments and

contingencies:

Note 10: Commitments and Contingencies

Guarantees

In conjunction with certain transactions, primarily divestitures, we may

provide routine indemnifications (e.g., indemnification for representa–

tions and warranties and retention of previously existing environmental,

tax and employee liabilities) which terms range in duration and in

Off-Balance Sheet Arrangements

We do not have off-balance sheet financing arrangements, including

variable interest entities, that have a material impact on our financial

statements.

FINANCIAL REPORTING PROBLEM (Continued)

Purchase Commitments and Operating Leases

June 30

2012

2013

2014

2015

2016

Thereafter

Purchase obiligations

$1,351

$762

$368

$154

$104

$273

Such amounts represent future purchases in line with expected usage

to obtain favorable pricing. Approximately 26% of our purchase

commitments relate to service contracts for information technology,

June 30

2012

2013

2014

2015

2016

Thereafter

Operating leases

$264

$224

$192

$173

$141

$505

Litigation

We are subject to various legal proceedings and claims arising out of

our business which cover a wide range of matters such as

governmental regulations, antitrust and trade regulations, product

FINANCIAL REPORTING PROBLEM (Continued)

the Company is doing. Competition and antitrust law inquiries often

continue for several years and, if violations are found, can result in

substantial fines.

In response to the actions of the European Commission and national

authorities, the Company launched its own internal investigations into

potential violations of competition laws. The Company has identified

violations in certain European countries and appropriate actions were

taken.

Several regulatory authorities in Europe have issued separate

complaints pursuant to their investigations alleging that the

In accordance with U.S. GAAP, certain of the reserves included in this

amount represent the low end of a range of potential outcomes.

Accordingly, the ultimate resolution of these matters may result in

fines or costs in excess of the amounts reserved that could materially

impact our income statement and cash flows in the period in which

COMPARATIVE ANALYSIS CASE

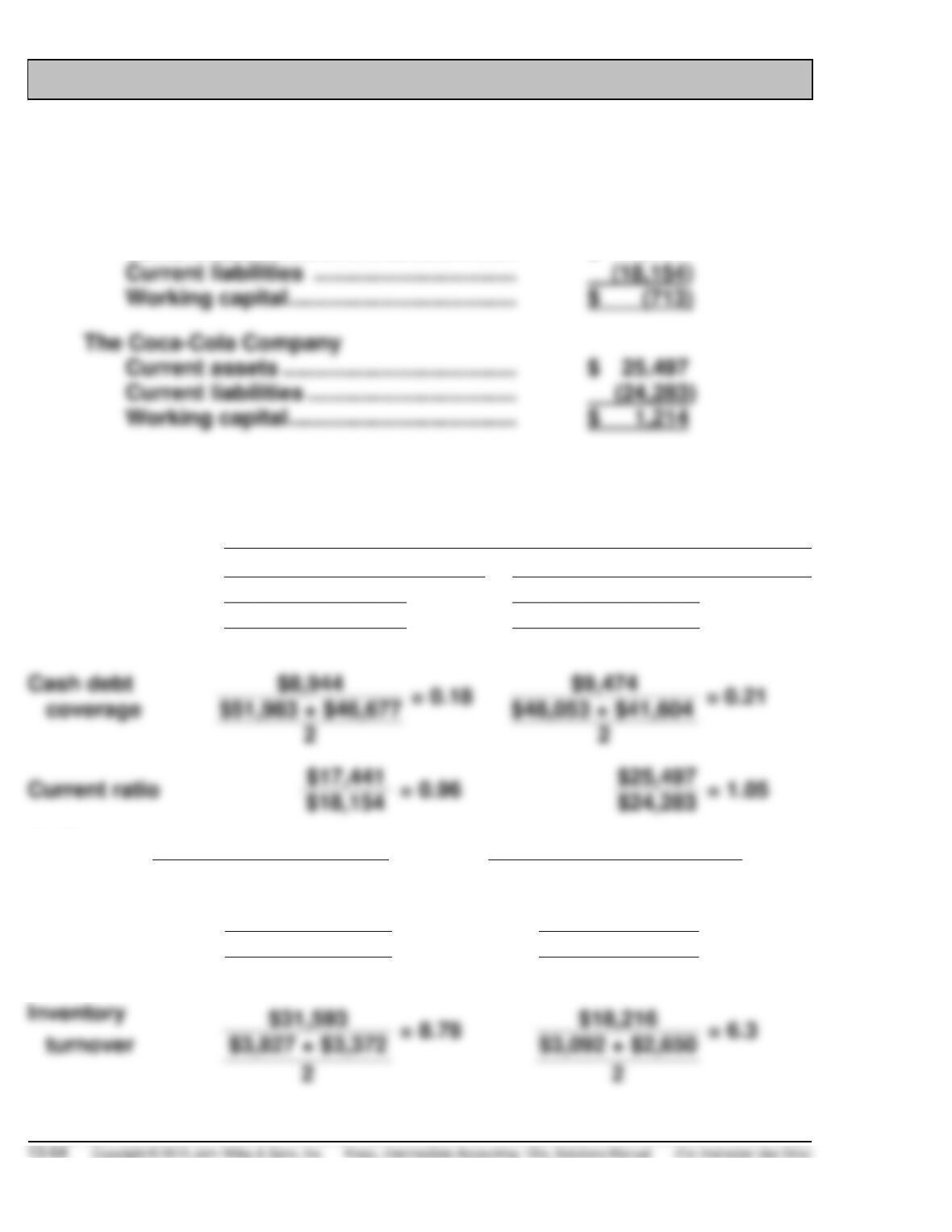

(a) The working capital position of the two companies is as follows:

($ millions)

PepsiCo, Inc.

Current assets ……………………………….. $ 17,441

(b) The overall liquidity of both companies is good as indicated from the

ratio analysis provided below:

(all computations in millions)

PepsiCo, Inc.

Coca-Cola

Current cash debt

$8,944

= 0.53

$9,474

= 0.44

coverage

$18,154 + $15,892

$24,283 + $18,508

2

2

Cash debt

= 0.18

= 0.21

coverage

Current ratio

$17,441

$25,497

= 1.05

Acid-test

$4,067 + $358 + $6,912

= 0.62

$13,891 + $144 + $4,920

= 0.78

ratio

$18,154

$24,283

Accounts

$66,504

= 10.05

$46,542

= 9.96

receivable

$6,912 + $6,323

$4,920 + $4,430

turnover

2

2

COMPARATIVE ANALYSIS CASE (Continued)

(c) As indicated in the chapter, a company can exclude a short-term obli-

gation from current liabilities only if both of the following conditions

are met:

(d) Coca-Cola discusses its contingencies in the following note:

NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Contingencies

Our Company is involved in various legal proceedings and tax

NOTE 11: COMMITMENTS AND CONTINGENCIES

Guarantees

As of December 31, 2011, we were contingently liable for guarantees

of indebtedness owed by third parties of $654 million, of which $321

million was related to VIEs. Refer to Note 1 for additional information

related to the Company’s maximum exposure to loss due to our

COMPARATIVE ANALYSIS CASE (Continued)

Legal Contingencies

The Company is involved in various legal proceedings. We establish

reserves for specific legal proceedings when we determine that the

likelihood of an unfavorable outcome is probable and the amount of

During the period from 1970 to 1981, our Company owned Aqua–

Chem, Inc., now known as Cleaver-Brooks, Inc. (“Aqua-Chem”).

During that time, the Company purchased over $400 million of

insurance coverage, which also insures Aqua-Chem for some of its

prior and future costs for certain product liability and other claims. A

division of Aqua-Chem manufactured certain boilers that contained

gaskets that Aqua–Chem purchased from outside suppliers. Several

years after our Company sold this entity, Aqua-Chem received its

COMPARATIVE ANALYSIS CASE (Continued)

certain insurers of Aqua-Chem. In that case, five plaintiff insurance

companies filed a declaratory judgment action against Aqua-Chem,

the Company and 16 defendant insurance companies seeking a

determination of the parties’ rights and liabilities under policies

issued by the insurers and reimbursement for amounts paid by

triggered is jointly and severally liable for 100 percent of Aqua–

Chem’s losses up to policy limits. The court’s judgment concluded

the Wisconsin insurance coverage litigation. The Georgia litigation

remains subject to the stay agreement. The Company and Aqua-Chem

continued to negotiate with various insurers that were defendants in

and the Company prevail in the coverage-in-place settlement

litigation, these three insurance companies will remain subject to the

court’s judgment in the Wisconsin insurance coverage litigation.

The Company is unable to estimate at this time the amount or range

of reasonably possible loss it may ultimately incur as a result of

COMPARATIVE ANALYSIS CASE (Continued)

as during the past five years, and (b) the various insurers that cover

the asbestos-related claims against Aqua-Chem remain solvent,

regardless of the outcome of the coverage-in-place settlement

litigation, there will likely be little defense or indemnity costs that are

Indemnifications

At the time we acquire or divest our interest in an entity, we

sometimes agree to indemnify the seller or buyer for specific

Tax Audits

The Company is involved in various tax matters, with respect to some

Risk Management Programs

The Company has numerous global insurance programs in place to help

protect the Company from the risk of loss. In general, we are self-

COMPARATIVE ANALYSIS CASE (Continued)

Workforce (Unaudited)

We refer to our employees as “associates.” As of December 31, 2011,

our Company had approximately 146,200 associates, of which

approximately 67,400 associates were located in the United States.

Operating Leases

The following table summarizes our minimum lease payments under

noncancelable operating leases with Initial or remaining lease terms in

excess of one year as of December 31, 2011 (in millions):

Years Ending December 31,

Operating Lease

Payments

2012

$ 241

2013

174

2014

133

101

Thereafter

$ 997

COMPARATIVE ANALYSIS CASE (Continued)

is reasonably possible and/or for which no estimate of possible

losses can be made. Management believes that any liability to the

Company that may arise as a result of currently pending legal

Note 9

Debt Obligations and Commitments

2011

2010

Short-term debt obligations

Current maturities of long-term debt

$ 2,549

$ 1,626

Commercial paper (0.1% and 0.2%)

2,973

2,632

$ 6,165

$ 4,898

Long-term debt obligations

Notes due 2011 (4.4%)

$ –

$ 1,513

Notes due 2012 (3.0% and 3.1%)

2,353

2,437

Notes due 2013 (2.3% and 3.0%)

Notes due 2014 (4.6% and 5.3%)

Notes due 2015 (2.3% and 2.6%)

1,632

Notes due 2016 (3.9% and 5.5%)

Notes due 2017–2040 (4.8% and 4.9%)

10,806

Other, due 2012–2020 (9.9% and 9.8%)

23,117

21,625

Less: current maturities of long-term debt

obligations

(2,549)

(1,626)

Total

$20,568

$19,999

The interest rates in the above table reflect weighted-average rates at

year-end.

COMPARATIVE ANALYSIS CASE (Continued)

In the third quarter of 2011, we issued:

The net proceeds from the issuances of all the above notes were used

for general corporate purposes.

In the third quarter of 2011, we entered into a new four-year

unsecured revolving credit agreement (Four-Year Credit Agreement)

Also, In the third quarter of 2011, we entered into a new 364-day

unsecured revolving credit agreement (364-Day Credit Agreement)

which expires in June 2012. Effective August 8, 2011, commitments

under this agreement were increased to enable us to borrow up to

The Four-Year Credit Agreement and the 364-Day Credit

Agreement, together replaced our $2 billion unsecured revolving

credit agreement, our $2.575 billion 364-day unsecure revolving credit

agreement and our $1.080 billion amended PBG credit facility. Funds

COMPARATIVE ANALYSIS CASE (Continued)

and integration charges) in the third quarter, primarily representing

the premium paid in the tender offer.

In addition, as of December 31, 2011, $848 million of our debt

Long-Term Contractual Commitments(a)

Payments Due by Period

Total

2012

2013–

2014

2015–

2016

2017

and

beyond

Long-term debt

obligations(b)

$19,738

$ –

$6,084

$3,451

$10,203

Interest on debt

7,445

852

4,108

Operating

1,825

423

598

337

Purchasing commitments

2,434

1,113

957

302

62

Marketing commitments

2,519

240

589

535

1,155

$33,961

$2,628

$9,622

$5,716

$15,995

(a) Reflects non-cancelable commitments as of December 31, 2011,

based on year-end foreign exchange rates and excludes any

reserves for uncertain tax positions as we are unable to reasonably

COMPARATIVE ANALYSIS CASE (Continued)

Most long-term contractual commitments, except for our long term debt

obligations, are not recorded on our balance sheet. Non-cancelable

operating leases primarily represent building leases. Non-cancelable

purchasing commitments are primarily for sugar and other sweeteners,

packaging materials, oranges and orange juice. Non-cancelable marketing

Off-Balance-Sheet Arrangements

It is not our business practice to enter into off-balance-sheet arrangements,

other than in the normal course of business. See Note 8 regarding

FINANCIAL STATEMENT ANALYSIS CASE 1

NORTHLAND CRANBERRIES

(a) Working capital is calculated as current assets – current liabilities, while

the current ratio is calculated as current assets/current liabilities. For

Northland Cranberries these ratios are calculated as follows:

Current year

Prior year

Working capital

$6,745,759 – $10,168,685 = $–3,422,926

$5,598,054 – $4,484,687 = $1,113,367

Current ratio

($6,745,759/$10,168,685) = .66

($5,598,054/$4,484,687) = 1.25

Historically, it was generally believed that a company should maintain

a current ratio of at least 2.0. In recent years, because companies have

(b) This illustrates a potential problem with ratios like the current ratio,

that rely on balance sheet numbers that present a company’s finan–

cial position at a particular point in time. That point in time may not be

representative of the average position of the company during the course

FINANCIAL STATEMENT ANALYSIS CASE 2

MOHICAN COMPANY

(a) Under the cash basis, warranty costs are charged to expense as they

are incurred; in other words, warranty costs are charged in the period

in which the seller or manufacturer performs in compliance with the

warranty. No liability is recorded for future costs arising from warranties,

(b) When the warranty is sold separately from the product, the sales war–

ranty approach is employed. Revenue on the sale of the extended

warranty is deferred and is generally recognized on a straight-line basis

over the life of the contract. Revenue is deferred because the seller of

the warranty has an obligation to perform services over the life of the

contract.

(c) The general approach is to use the straight-line method to recognize

deferred revenue on warranty contracts. If historical evidence indicates

FINANCIAL STATEMENT ANALYSIS CASE 3

(a) BOP’s working capital and current ratio have declined in 2014 com-

pared to 2013. While this would appear to be bad news, the acid-test

ratio has improved. This is due to BOP carrying relatively more liquid

receivables in 2014 (receivable days has increased.) And while

(b) Answers will vary depending on the companies selected. This activity

is a great spreadsheet exercise. The analysis for Best Buy and Circuit

City for the years 2005 – 2007 is presented on the next page (just

before Circuit City went out of business).