EXERCISE 21-7 (Continued)

(d) 1/1/14 Lease Receivable ………………………. 150,000*

Cost of Goods Sold……………………. 114,654**

Sales Revenue ……………………. 144,654***

EXERCISE 21-8 (20–30 minutes)

(a) The lease agreement has a bargain-purchase option and thus meets

(b) The lease agreement has a bargain-purchase option. The collectibility

of the lease payments is reasonably predictable, and there are no

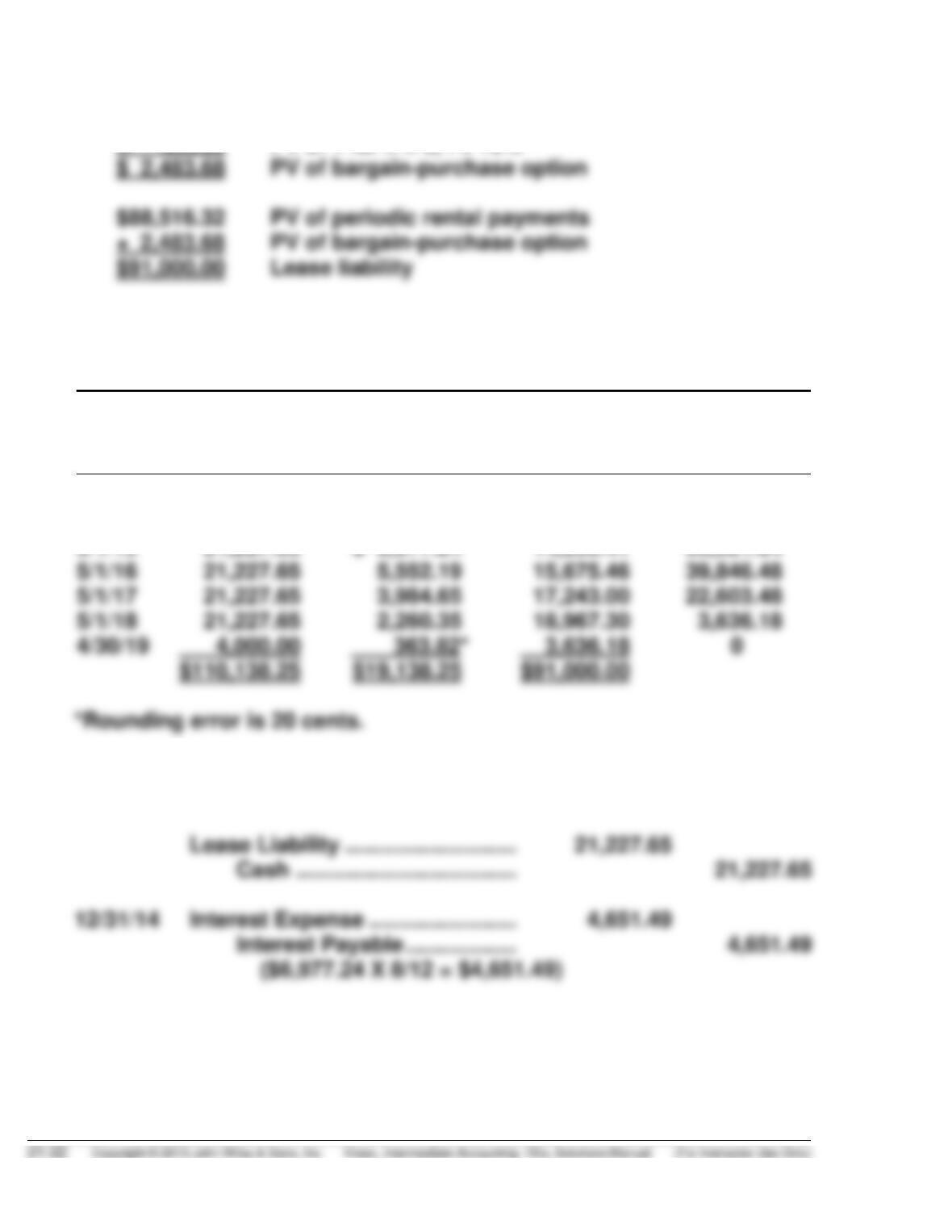

(c) Computation of lease liability:

$21,227.65 Annual rental payment

EXERCISE 21-8 (Continued)

$ 4,000.00 Bargain purchase option

X .62092 PV of 1 for n = 5, i = 10%

RODE COMPANY (Lessee)

Lease Amortization Schedule

Date

Annual Lease

Payment Plus

BPO

Interest

(10%) on

Liability

Reduction

of Lease

Liability

Lease

Liability

5/1/14

$91,000.00

5/1/14

$ 21,227.65

$21,227.65

69,772.35

5/1/15

21,227.65

$ 6,977.24

14,250.41

55,521.94

5/1/16

39,846.48

22,603.48

21,227.65

18,967.30

3,636.18

4,000.00

3,636.18

$110,138.25

$91,000.00

(d) 5/1/14 Leased Equipment ………………… 91,000.00

Lease Liability ………………… 91,000.00

EXERCISE 21-8 (Continued)

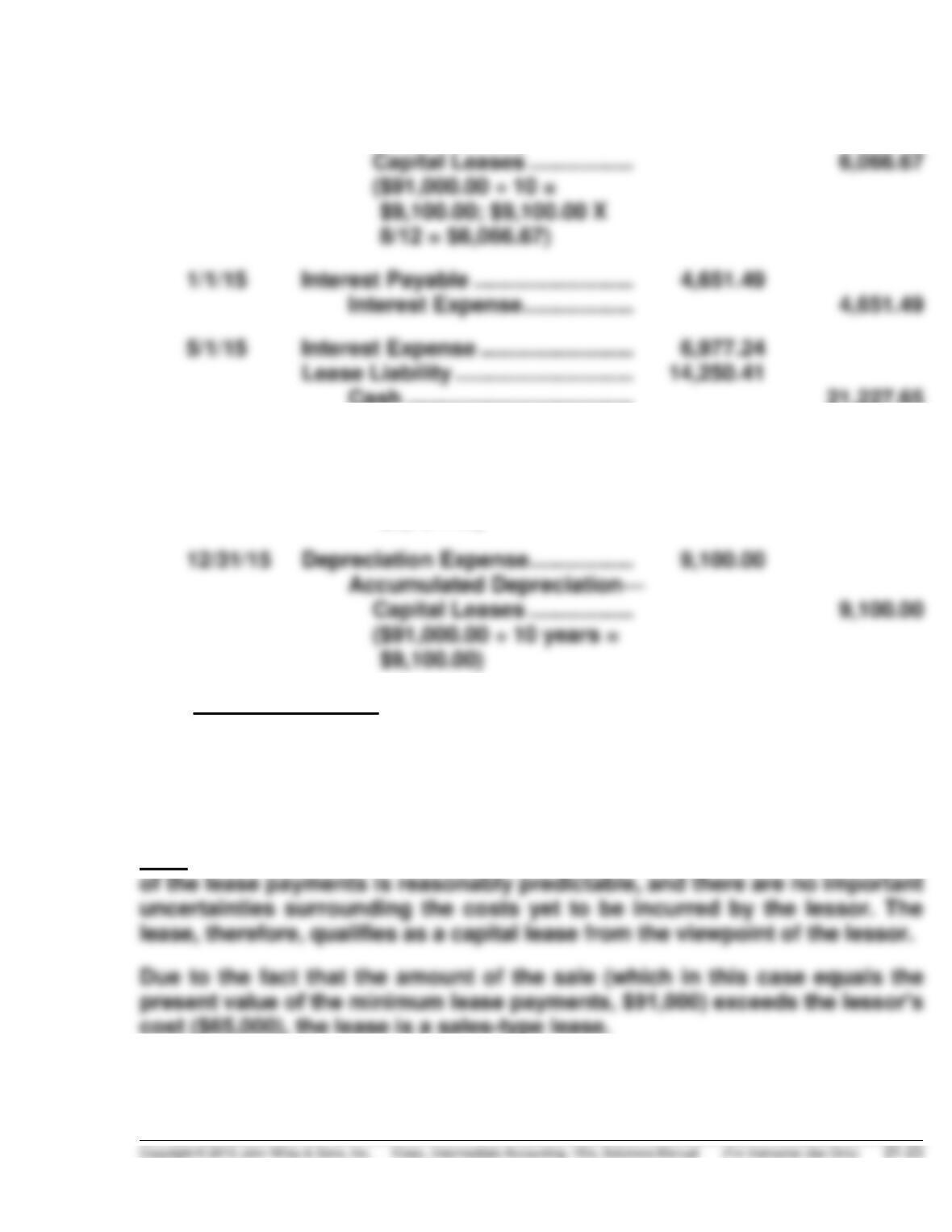

Depreciation Expense …………….. 6,066.67

Accumulated Depreciation—

Cash ………………………………. 21,227.65

12/31/15 Interest Expense ……………………. 3,701.46

Interest Payable ………………. 3,701.46

($5,552.19 X 8/12 =

($3,701.46)

(Note to instructor: Because a bargain-purchase option was involved,

the leased asset is depreciated over its economic life rather than over

the lease term.)

EXERCISE 21-9 (20–30 minutes)

Note: The lease agreement has a bargain-purchase option. The collectibility

EXERCISE 21-9 (Continued)

The minimum lease payments associated with this lease are the periodic

annual rents plus the bargain purchase option. There is no residual value

relevant to the lessor’s accounting in this lease.

(a) The lease receivable is computed as follows:

$21,227.65 Annual rental payment

X 4.16986 PV of an annuity due of 1 for n = 5, i = 10%

(b) MOONEY LEASING COMPANY (Lessor)

Lease Amortization Schedule

Date

Annual Lease

Payment Plus

BPO

Interest (10%)

on Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

5/1/14

$91,000.00

5/1/14

$ 21,227.65

$21,227.65

69,772.35

5/1/15

5/1/16

39,846.48

22,603.48

4,000.00

3,636.18

$110,138.25

$91,000.00

EXERCISE 21-9 (Continued)

(c) 5/1/14 Lease Receivable …………………. 91,000.00

Cost of Goods Sold………………. 65,000.00

Sales Revenue ………………. 91,000.00

Inventory ………………………. 65,000.00

5/1/15 Cash ……………………………………. 21,227.65

Lease Receivable ………….. 14,250.41

Interest Receivable ………… 4,651.49

Interest Revenue …………… 2,325.75

($6,977.24 – $4,651.49)

EXERCISE 21-10 (15–25 minutes)

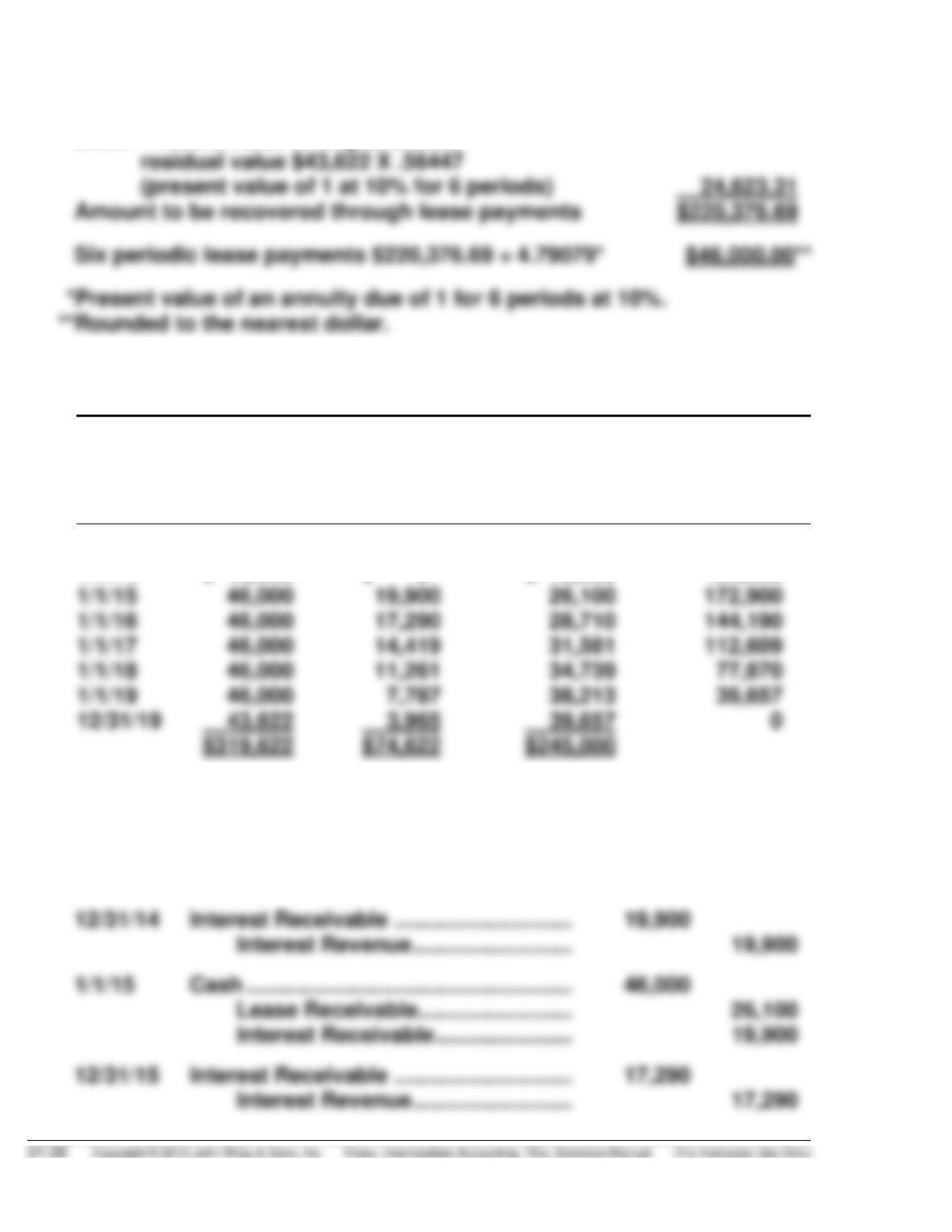

(a) Fair value of leased asset to lessor $245,000.00

Less: Present value of unguaranteed

(b) MORGAN LEASING COMPANY (Lessor)

Lease Amortization Schedule

Date

Annual

Lease

Payment

Plus URV

Interest (10%)

on Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

1/1/14

$245,000

1/1/14

$ 46,000

$ –0–

$ 46,000

199,000

1/1/15

172,900

112,609

43,622

39,657

$319,622

$245,000

(c) 1/1/14 Lease Receivable ………………………….. 245,000

Equipment ……………………………… 245,000

1/1/114 Cash …………………………………………….. 46,000

Lease Receivable ……………………. 46,000

EXERCISE 21-11 (20–30 minutes)

Note: This lease is a capital lease to the lessee because the lease term

(five years) exceeds 75% of the remaining economic life of the asset (five years).

(a) PLOTE COMPANY (Lessee)

Lease Amortization Schedule

Date

Annual Lease

Payment

Interest (10%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/14

$75,653.56

1/1/14

$18,142.95

$ –0–

$18,142.95

57,510.61

1/1/15

18,142.95

45,118.72

18,142.95

16,493.45

*Rounding error is 15 cents.

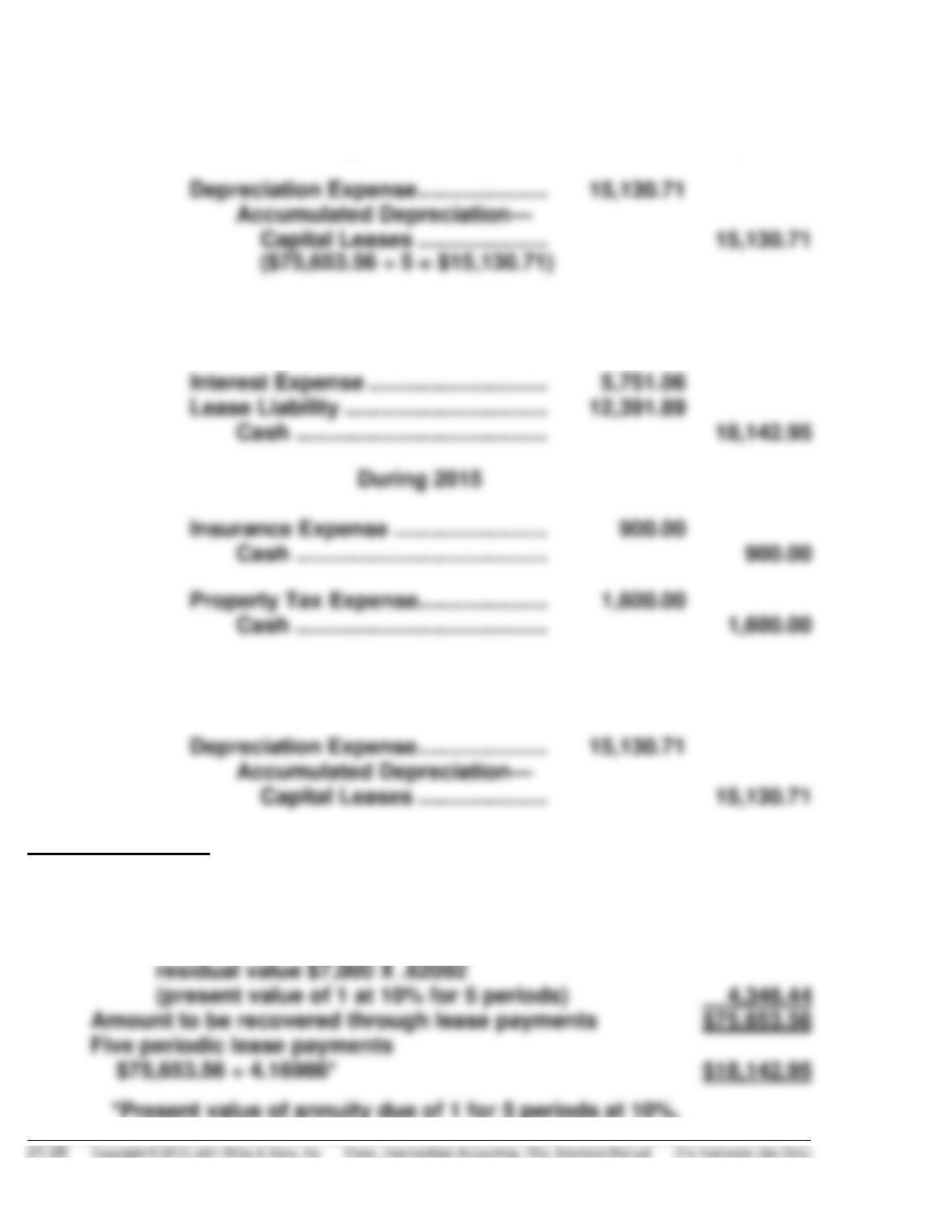

(b) 1/1/14 Leased Equipment …………………. 75,653.56

Lease Liability …………………. 75,653.56

1/1/14 Lease Liability ……………………….. 18,142.95

Cash ………………………………. 18,142.95

During 2014

Insurance Expense ………………… 900.00

Cash ………………………………. 900.00

Property Tax Expense ……………. 1,600.00

Cash ………………………………. 1,600.00

EXERCISE 21-11 (Continued)

12/31/14 Interest Expense ……………………….. 5,751.06

Interest Payable ………………….. 5,751.06

1/1/15 Interest Payable …………………………. 5,751.06

Interest Expense …………………. 5,751.06

12/31/15 Interest Expense ……………………….. 4,511.87

Interest Payable ………………….. 4,511.87

Note to instructor:

1. The lessor sets the annual rental payment as follows:

Fair value of leased asset to lessor $80,000.00

Less: Present value of unguaranteed

EXERCISE 21-11 (Continued)

2. The unguaranteed residual value is not subtracted when depreciating

the leased asset.

EXERCISE 21-12 (10–20 minutes)

(a) Entries for Doug Nelson are as follows:

1/1/14 Buildings …………………………………. 4,500,000

Cash …………………………………….. 4,500,000

(b) Entries for Patrick Wise are as follows:

12/31/14 Rent Expense …………………………... 275,000

Cash …………………………………. 275,000

EXERCISE 21-13 (15–20 minutes)

(a) Annual rental revenue $210,000

EXERCISE 21-13 (Continued)

(b) Rent expense $210,000

Note: Both the rent security deposit and the last month’s rent prepayment

should be reported as a noncurrent asset.

EXERCISE 21-14 (15–20 minutes)

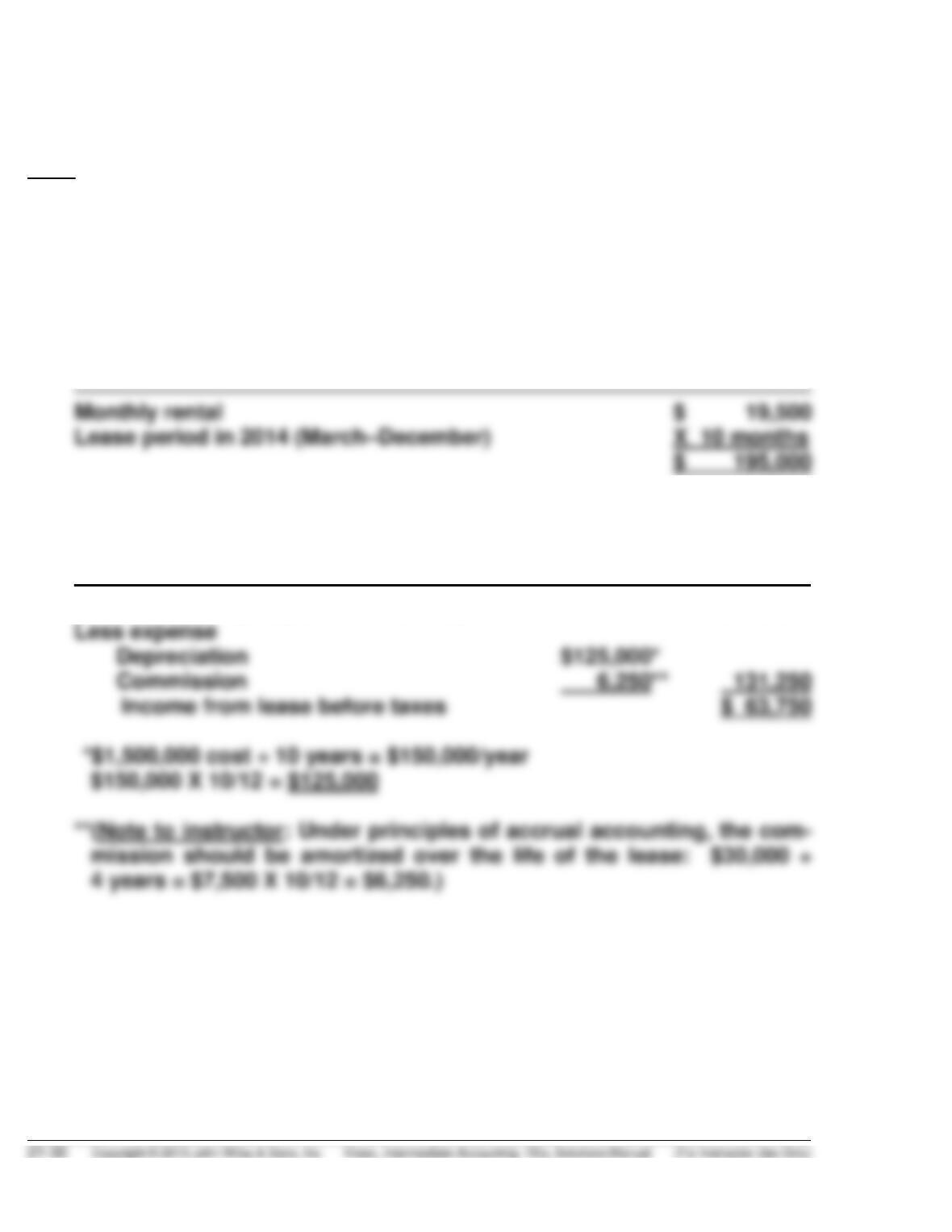

(a) RUDY COMPANY

Rent Expense

For the Year Ended December 31, 2014

(b) BARBARA BRENT INC.

Income or Loss from Lease before Taxes

For the Year Ended December 31, 2014

Rental revenue ($19,500 X 10 months) $195,000

*EXERCISE 21-15 (20–30 minutes)

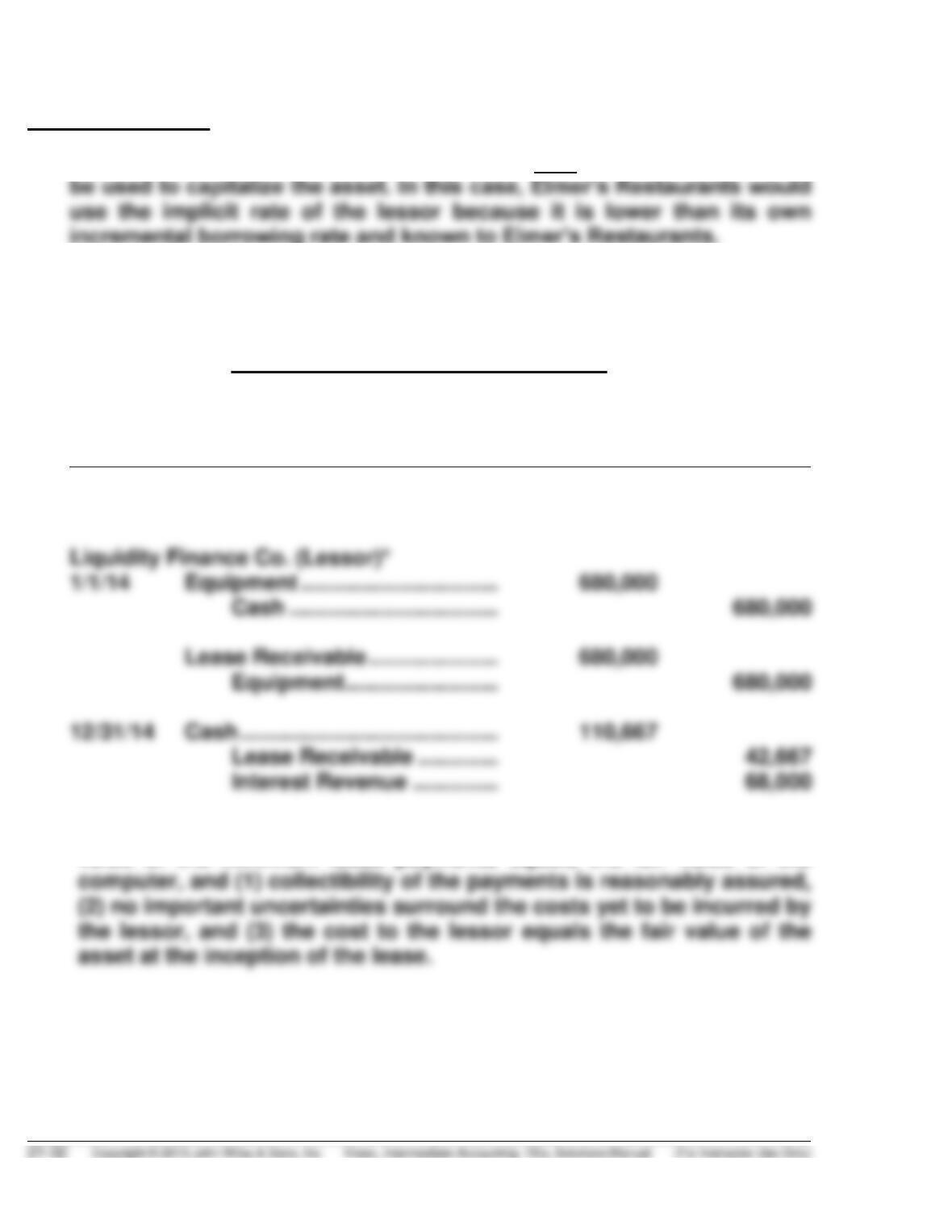

Elmer’s Restaurants (Lessee)*

1/1/14 Cash ……………………………………………. 680,000

Equipment …………………………….. 600,000

Unearned Profit on Sale—

Leaseback………………………….. 80,000

12/31/14 Unearned Profit on Sale—

Leaseback ………………………………… 8,000

Depreciation Expense** ………….. 8,000

($80,000 ÷ 10)

12/31/14 Depreciation Expense …………………… 68,000

*EXERCISE 21-15 (Continued)

Note to instructor:

1. The present value of an ordinary annuity at 10% for 10 periods should

2. The unearned profit on the sale-leaseback should be amortized on the

same basis that the asset is being depreciated.

Partial Lease Amortization Schedule

Date

Annual

Lease

Payment

Interest (10%)

Amortization

Balance

1/1/14

$680,000

12/31/14

$110,667

$68,000

$42,667

637,333

*Lease should be treated as a direct financing lease because the present

value of the minimum lease payments equals the fair value of the

*EXERCISE 21-16 (20–30 minutes)

(a) Sale-leaseback arrangements are treated as though two transactions

were a single financing transaction if the lease qualifies as a capital

lease. Any gain or loss on the sale is deferred and amortized over the

(b) A sale-leaseback is usually treated as a single financing transaction

in which any profit on the sale is deferred and amortized by the seller.

However, FASB 28 amends this general rule when either only a

minor part of the remaining use of the property is retained, or more

(c) The profit on the sale of $121,000 should be deferred and amortized

over the lease term. Since the leased asset is being depreciated using

the sum-of-the-years’ depreciation method, the deferred gain should

also be reported in the same manner. Therefore, in the first year, $22,000

(10/55 X $121,000) of the gain would be recognized.

(d) In this case, Sondgeroth would report a loss of $87,300 ($300,000 –

TIME AND PURPOSE OF PROBLEMS

Problem 21-1 (Time 20–25 minutes)

Purpose—to develop an understanding of the accounting principles used in a sales-type lease for both

Problem 21-2 (Time 20–30 minutes)

Purpose—to develop an understanding of the accounting treatment for operating leases. The student is

Problem 21-3 (Time 35–45 minutes)

Purpose—to develop an understanding of the accounting procedures involved in a sales-type leasing

Problem 21-4 (Time 30–40 minutes)

Problem 21-5 (Time 30–40 minutes)

Purpose—to provide an understanding of how lease information is reported on the balance sheet and

income statement for three different years in regard to the lessor. In addition, the year–end month is

changed in order to help provide an understanding of the complications involved with partial periods.

Problem 21-6 (Time 25–35 minutes)

Purpose—to provide an understanding of the journal entries to be recorded by the lessee given a

guaranteed residual value. Journal entries for two periods are required.

Problem 21-7 (Time 25–30 minutes)

Purpose—to develop an understanding of the accounting for a capital lease by the lessee in an annuity

Problem 21-8 (Time 20–30 minutes)

Purpose—to develop an understanding of the accounting by the lessee for a capital lease. The student

Time and Purpose of Problems (Continued)

Problem 21-9 (Time 20–30 minutes)

Problem 21-10 (Time 30–40 minutes)

Purpose—to develop an understanding of the accounting treatment accorded a sales-type lease involving

Problem 21-11 (Time 30–40 minutes)

Purpose—to develop an understanding of a capital lease with an unguaranteed residual value. The

student explains why it is a capital lease and computes the amount of the initial liability. The student

prepares a 10-year amortization schedule and all of the lessee’s journal entries for the first year.

Problem 21-12 (Time 40–50 minutes)

Purpose—to develop an understanding of the accounting for capital leases where the lease payments

Problem 21-13 (Time 30–40 minutes)

Purpose—to develop an understanding of a sales-type lease with a guaranteed residual value. The

Problem 21-14 (Time 30–40 minutes)

Problem 21-15 (Time 30–40 minutes)

Purpose—to develop a memo to your audit supervisor to discuss: (a) why you inspected the lease

agreement, (b) what you determined about the lease, and (c) how you advised your client to account for

the lease. As part of the discussion you are required to make the journal entry necessary to record the

lease property.

Problem 21-16 (Time 30–40 minutes)

Purpose—to develop an understanding of how residual values affect the accounting for the lessee and

SOLUTIONS TO PROBLEMS

PROBLEM 21-1

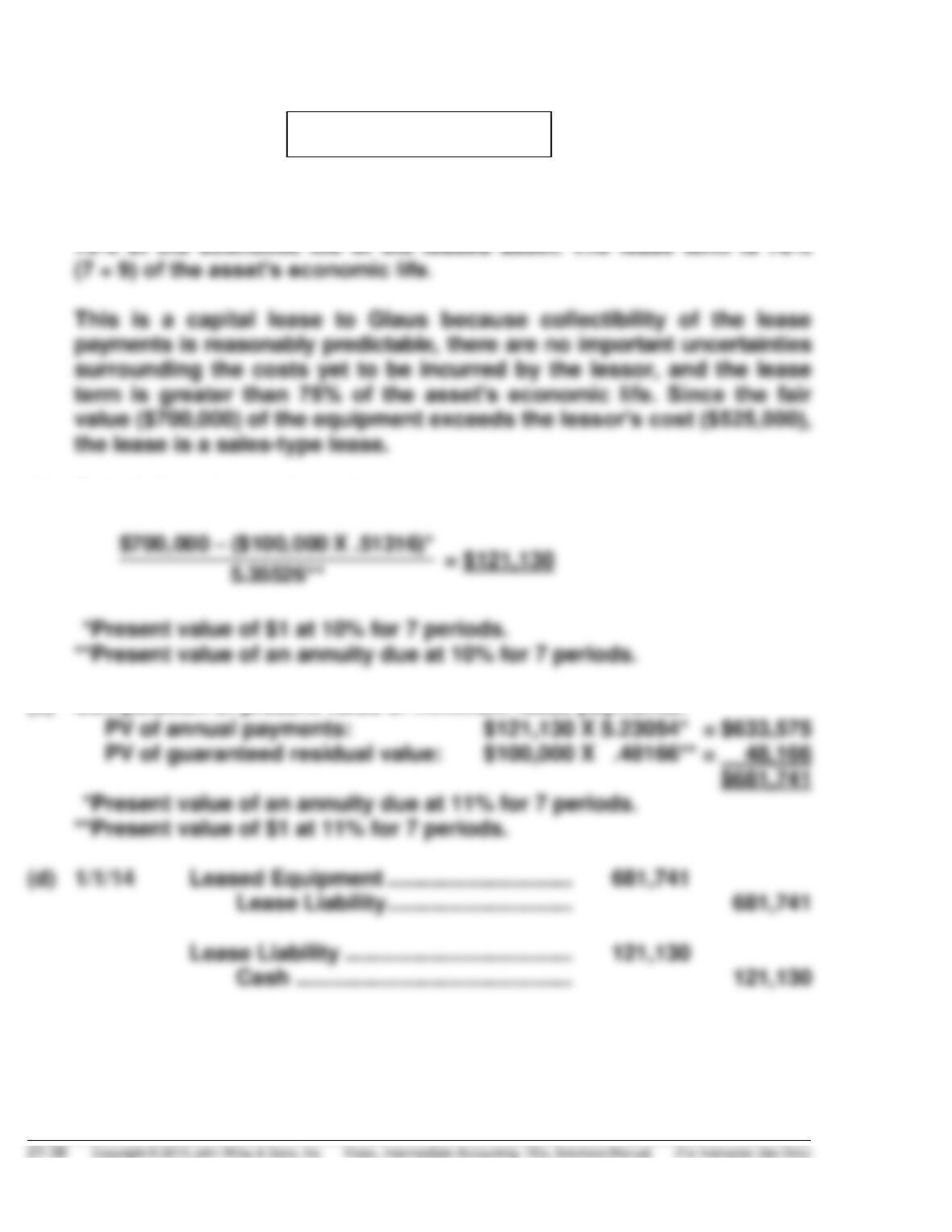

(a) This is a capital lease to Jensen since the lease term is greater than

(b) Calculation of annual rental payment:

(c) Computation of present value of minimum lease payments:

PROBLEM 21-1 (Continued)

12/31/14 Depreciation Expense …………………….. 83,106

Accumulated Depreciation—

Capital Leases

($681,741 – $100,000) ÷ 7 ……… 83,106

(e) 1/1/14 Lease Receivable …………………………... 700,000

Cost of Goods Sold………………………… 525,000

Sales Revenue ………………………… 700,000

Inventory ………………………………… 525,000

Cash ……………………………………………… 121,130

Lease Receivable ……………………. 121,130

PROBLEM 21-2

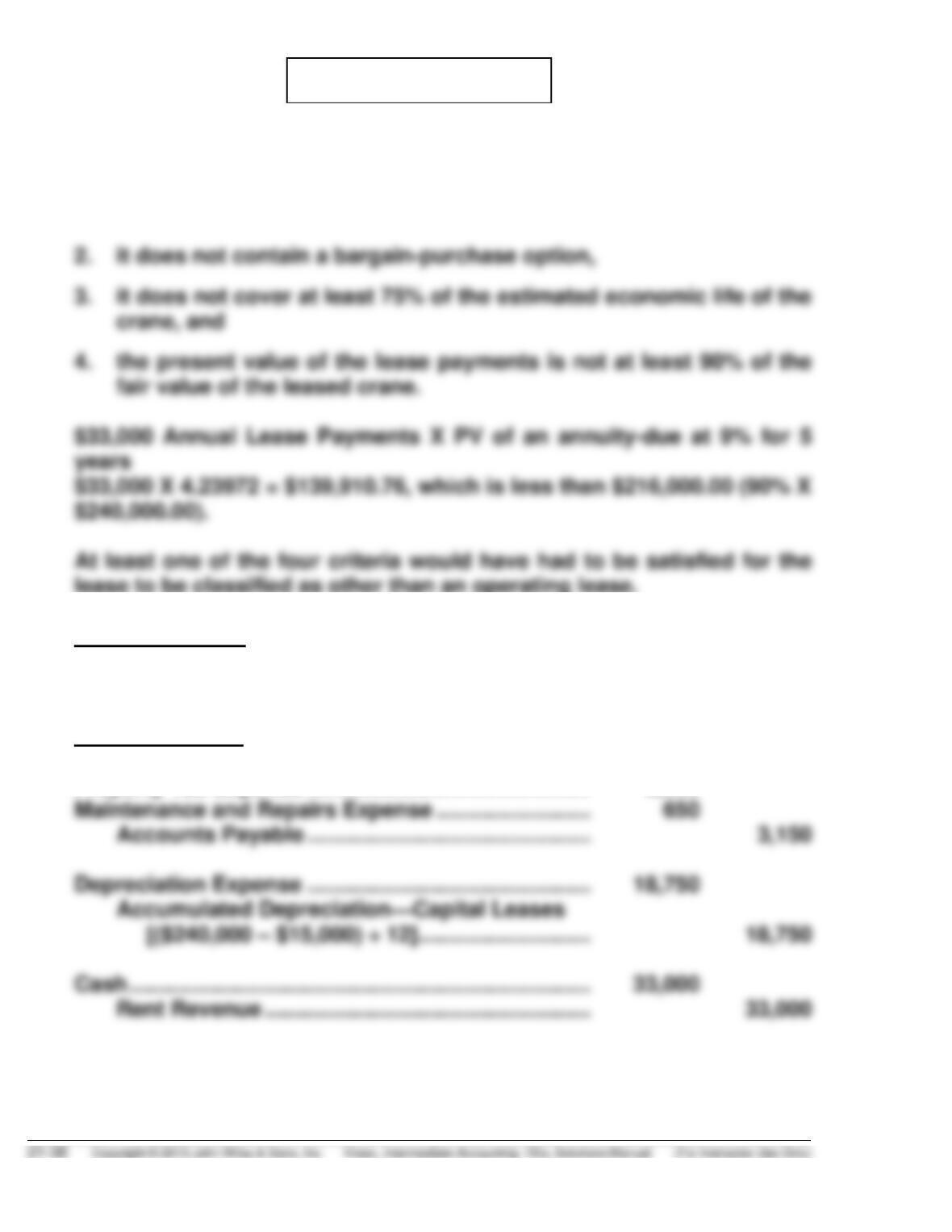

(a) The lease is an operating lease to the lessee and lessor because:

1. it does not transfer ownership,

lease to be classified as other than an operating lease.

(b) Lessee’s Entries

Rent Expense …………………………………………………… 33,000

Cash …………………………..……………………………… 33,000

Lessor’s Entries

Insurance Expense …………………………………………… 500

Property Tax Expense ………………………………………. 2,000

PROBLEM 21-2 (Continued)

(c) Abriendo as lessee must disclose in the income statement the $33,000

of rent expense and in the notes the future minimum rental payments

required as of January 1 (in total, $132,000) and for each of the succeed–

PROBLEM 21-3

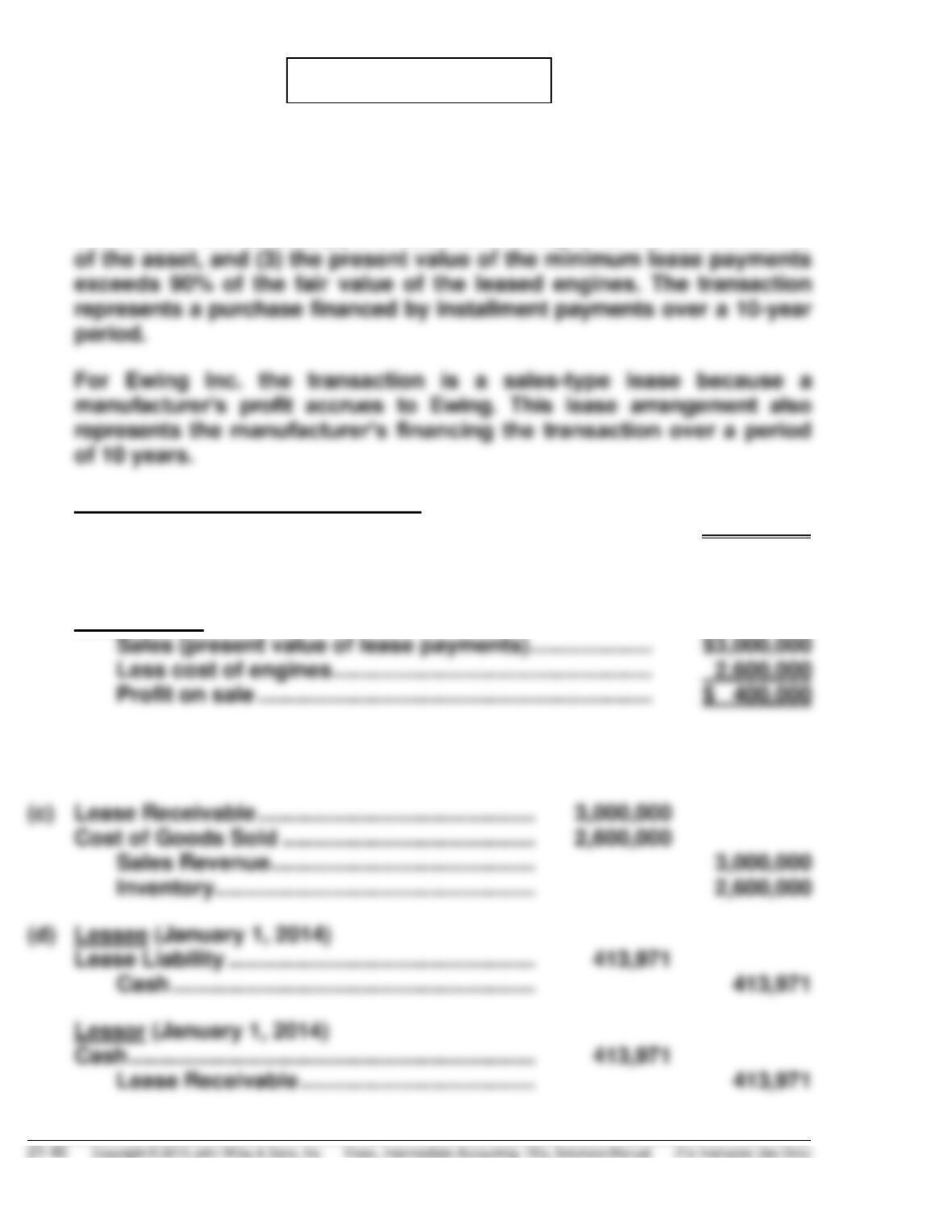

(a) The lease should be treated as a capital lease by Winston Industries

requiring the lessee to capitalize the leased asset. The lease qualifies for

capital lease accounting by the lessee because: (1) title to the engines

transfers to the lessee, (2) the lease term is equal to the estimated life

Present Value of Lease Payments

$413,971 X 7.24689* …………………………………………. $3,000,000

*Present value of an annuity due at 8% for 10 years, rounded by $2.

Dealer Profit

(b) Leased Equipment ……………………………………. 3,000,000

Lease Liability ……………………………………. 3,000,000