TIME AND PURPOSE OF PROBLEMS

Problem 9-1 (Time 10–15 minutes)

Purpose—to provide the student with an understanding of the lower-of-cost-or-market approach to

inventory valuation, similar to Problem 9-2. The major difference between these problems is that

Problem 9-1 provides some ambiguity to the situation by changing the catalog prices near the end of

the year.

Problem 9-2 (Time 25–30 minutes)

Problem 9-3 (Time 30–35 minutes)

Problem 9-4 (Time 20–30 minutes)

Problem 9-5 (Time 40–45 minutes)

Purpose—to provide the student with a complex problem involving a fire loss where the gross profit

Problem 9-6 (Time 20–30 minutes)

Purpose—to provide the student with a problem on the retail inventory method. The problem is relatively

Problem 9-7 (Time 20–30 minutes)

Purpose—to provide the student with a problem on the retail inventory method. This problem is similar

to Problem 9-6, except that a few different items must be evaluated in finding ending inventory at retail

and cost. Unusual items in this problem are employee discounts granted and loss from breakage.

A good problem that summarizes the essentials of the retail inventory method.

Problem 9-8 (Time 20–30 minutes)

Problem 9-9 (Time 30–40 minutes)

Problem 9-10 (Time 30–40 minutes)

Purpose—to provide the student with an opportunity to write a memo explaining what is designated

market value and how it is computed. As part of this memo, the student is required to compute

inventory on the lower-of-cost-or-market basis using the individual item approach.

Time and Purpose of Problems (Continued)

*Problem 9-11 (Time 30–35 minutes)

Purpose—to provide the student with a retail inventory problem where both the conventional retail and

dollar-value LIFO method must be computed. An excellent problem for highlighting the difference

between these two approaches to inventory valuation. It should be noted that the cost-to-retail per-

centage is given for LIFO so less computation is necessary.

*Problem 9-12 (Time 30–40 minutes)

Purpose—to provide the student with a comprehensive problem covering the retail and LIFO retail

*Problem 9-14 (Time 40–50 minutes)

Purpose—to provide the student with a retail inventory problem where both the conventional retail and

dollar-value LIFO method must be computed. The problem is similar to Problem 9-10, except that the

SOLUTIONS TO PROBLEMS

PROBLEM 9-1

Item

Cost

Replacement

Cost

Ceiling*

Floor**

Designated

Market

Lower-of–

Cost-or–

Market

A

$470

$ 460

$ 450

$350

$ 450

$450

B

C

D

PROBLEM 9-2

(a) 1. The balance in the Allowance to Reduce Inventory to Market at

May 31, 2014, should be $34,600, as calculated in Exhibit 1 below.

Exhibit 1

CALCULATIONS OF PROPER BALANCE

in the Allowance to Reduce Inventory to Market

At May 31, 2014

Cost

Replace-

ment

Cost

NRV

(Ceiling)

NRV less

normal

profit

(Floor)

LCM

Aluminum siding

$ 70,000

$ 62,500

$ 56,000

$ 50,900

$ 56,000

Cedar shake siding

86,000

79,400

84,800

77,400

79,400

Louvered glass doors

Thermal windows

Totals

$408,000

2. For the fiscal year ended May 31, 2014, the loss that would be

recorded due to the change in the Allowance to Reduce Inventory

to Market would be $7,100, as calculated below.

PROBLEM 9-2 (Continued)

(b) The use of the lower-of-cost-or-market (LCM) rule is based on both the

expense recognition principle and the concept of conservatism. The

PROBLEM 9-3

(a)

12/31/14 (Cost-of–Goods-Sold Method)

Cost of Goods Sold …………………………………………………

68,000

Allowance to Reduce Inventory to Market

($780,000 – $712,000) ……………………………………

68,000

Cost of Goods Sold …………………………………………………

(b)

12/31/14 (Loss Method)

To write down inventory to market:

Loss Due to Market Decline of Inventory ………………….

68,000

Allowance to Reduce Inventory to Market …………

To write down inventory to market:

Loss Due to Market Decline of Inventory ………………….

Allowance to Reduce Inventory to Market

PROBLEM 9-4

Beginning inventory ……………………………………………..

$ 80,000

Purchases ……………………………………………………………

290,000

370,000

Purchase returns ………………………………………………….

(28,000)

Total goods available ……………………………………………

342,000

Sales revenue …………………………..………………………….

Sales returns ……………………………………………………….

Net sales ……………………………………………………………..

Less: Gross profit (35% of $394,000) …………………….

Ending inventory (unadjusted for damage) …………….

Inventory damaged ………………………………………………

Less: Salvage value of damaged inventory……………

8,150

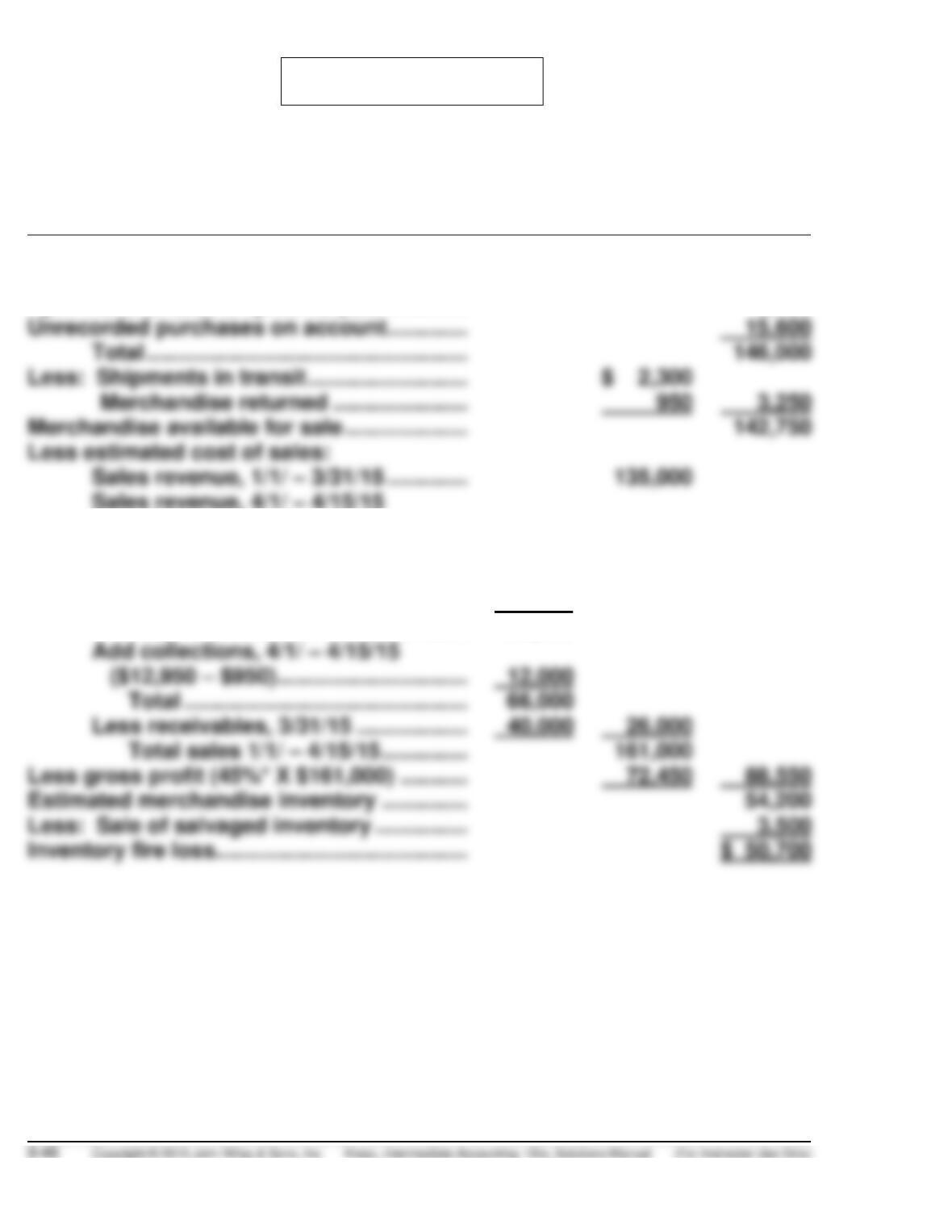

PROBLEM 9-5

STANISLAW CORPORATION

Computation of Inventory Fire Loss

April 15, 2015

Inventory, 1/1/15 …………………………..………..

$ 75,000

Purchases, 1/1/ – 3/31/15…………………………

52,000

April merchandise shipments paid ………….

3,400

Unrecorded purchases on account ………….

Total …………………………………………….

Less: Shipments in transit ……………………..

Merchandise returned ………………….

Merchandise available for sale ………………..

Less estimated cost of sales:

Sales revenue, 4/1/ – 4/15/15

Receivables acknowledged

at 4/15/15 ………………………………

$46,000

Estimated receivables not

acknowledged ………………………

8,000

Total ……………………………………….

54,000

Add collections, 4/1/ – 4/15/15

Total ……………………………………….

66,000

Less receivables, 3/31/15 ………………

26,000

Less gross profit (45%* X $161,000) ………..

54,200

Less: Sale of salvaged inventory ……………

PROBLEM 9-5 (Continued)

*Computation of Gross Profit Rate

Net sales, 2013 …………………………………………

$390,000

Net sales, 2014 …………………………………………

530,000

Total net sales …………………………………

920,000

Beginning inventory ………………………………….

Net purchases, 2013 ………………………………….

Net purchases, 2014 ………………………………….

Total ……………………………………………….

Less: Ending inventory …………………………....

506,000

PROBLEM 9-6

(a)

Cost

Retail

Beginning inventory ………………………

$ 17,000

$ 25,000

Purchases …………………………………….

82,500

137,000

Freight-in ………………………………………

7,000

Purchase returns …………………………..

(2,300)

(3,000)

Totals …………………………………..

180,000

Net markdowns ……………………………..

(4,000)

Sales revenue ……………………………….

$(95,000)

Sales returns ………………………………..

Inventory losses due to breakage …..

Ending inventory at retail ………………

$ 83,000

(b)

Ending inventory at lower-of-average-cost-or-market

(63% of $83,000) …………………………

$ 52,290

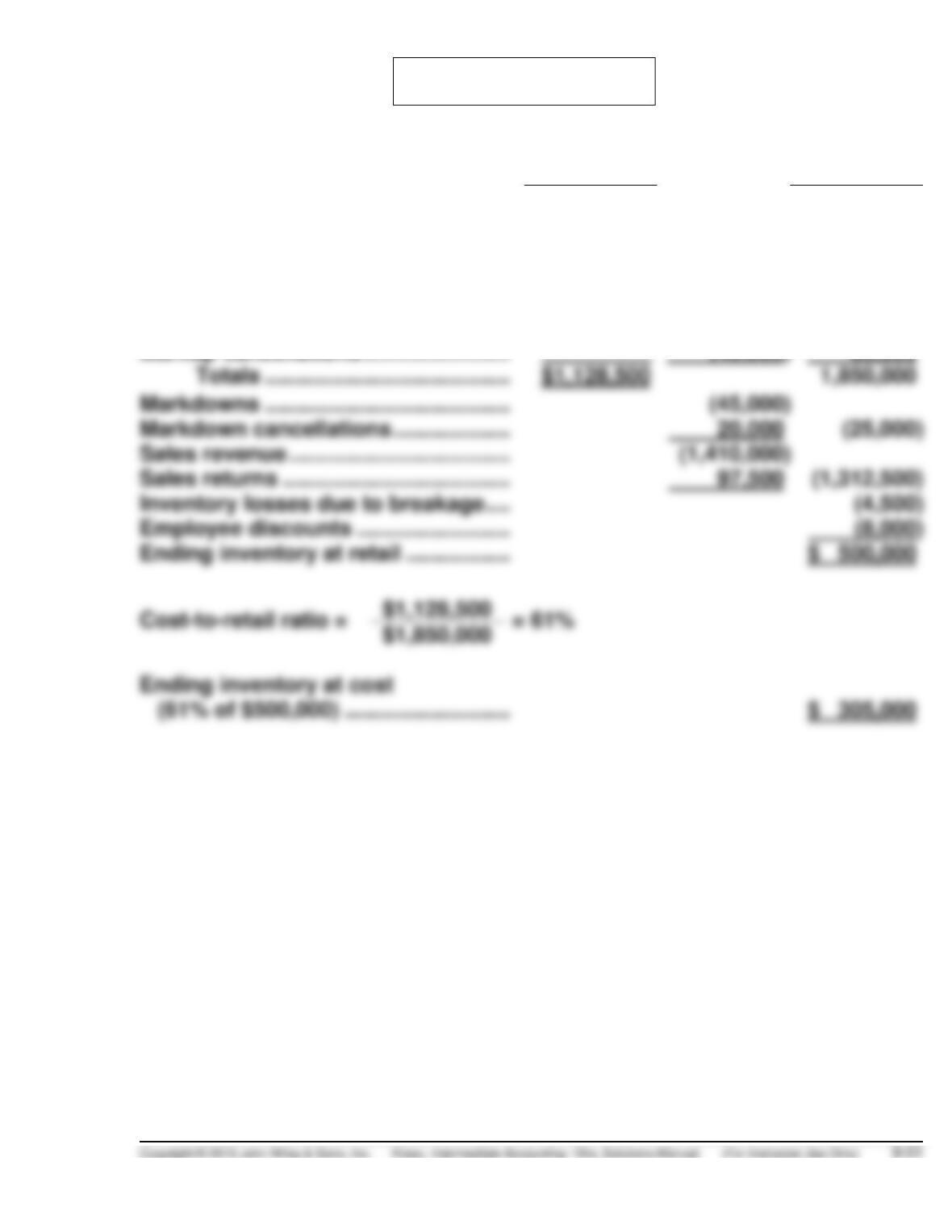

PROBLEM 9-7

Cost

Retail

Beginning inventory ……………………..

$ 250,000

$ 390,000

Purchases ……………………………………

914,500

1,460,000

Purchase returns ………………………….

(60,000)

(80,000)

Purchase discounts ……………………..

(18,000)

Freight-in …………………………………….

42,000

Markups ………………………………………

$ 120,000

Markup cancellations ……………………

(40,000)

80,000

Markdowns ………………………………….

Markdown cancellations ……………….

20,000

(25,000)

Sales revenue …………………………..….

Sales returns ……………………………….

Inventory losses due to breakage ….

Employee discounts …………………….

(8,000)

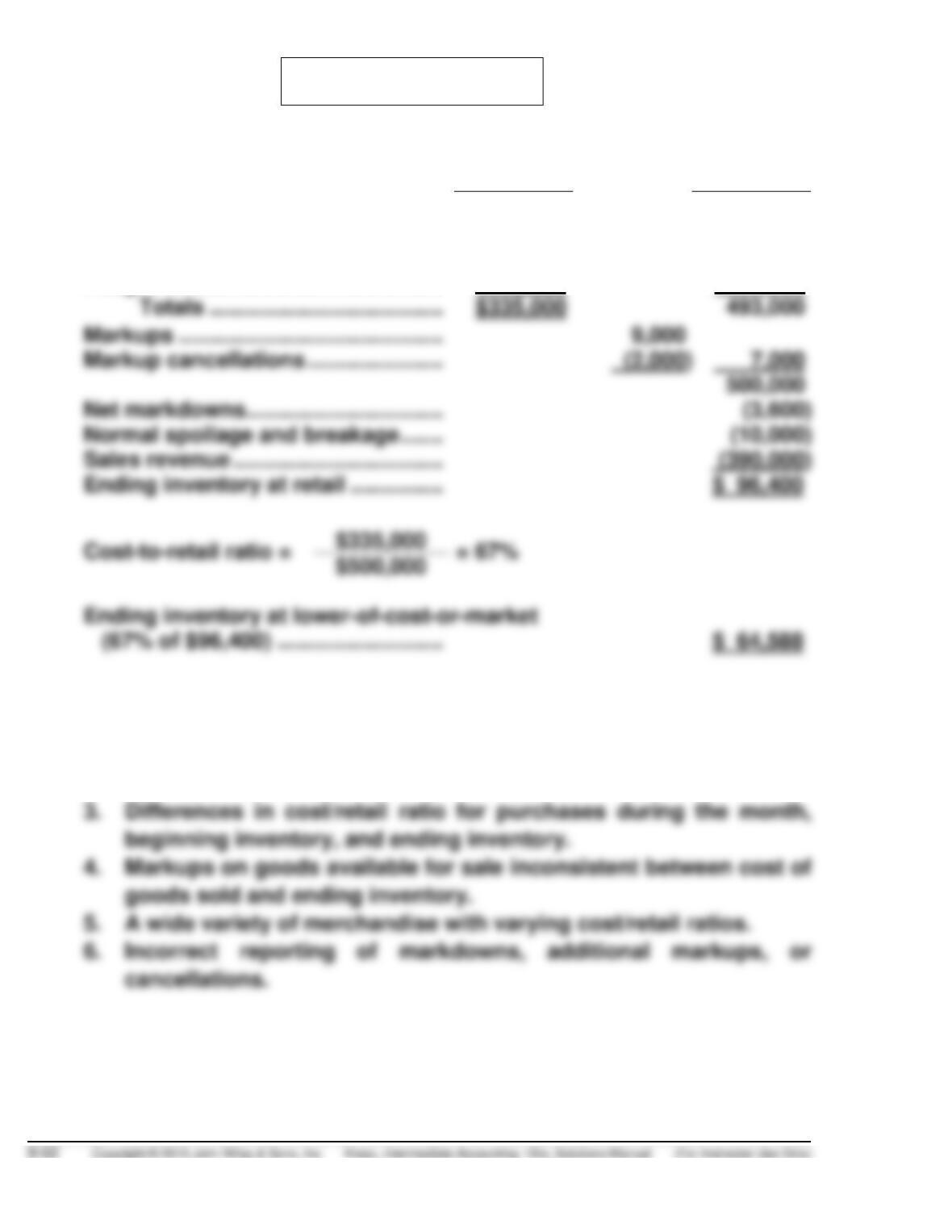

PROBLEM 9-8

(a)

Cost

Retail

Inventory (beginning) ………………….

$ 52,000

$ 78,000

Purchases ………………………………….

272,000

423,000

Purchase returns ………………………..

(5,600)

(8,000)

Freight-in ……………………………………

16,600

Markups …………………………………….

Markup cancellations ………………….

7,000

Net markdowns …………………………..

Normal spoilage and breakage …….

Sales revenue …………………………….

$335,000

$500,000

Ending inventory at lower-of-cost-or-market

(b) The difference between the inventory estimate per retail method and

the amount per physical count may be due to:

1. Theft losses (shoplifting or pilferage).

2. Spoilage or breakage above normal.

PROBLEM 9-9

(a) The inventory section of Maddox’s balance sheet as of November 30,

2014, including required footnotes, is presented below. Also presented

below are the inventory section supporting calculations.

Current assets

Inventory section (Note 1.)

Finished goods (Note 2.) ……………………

Work-in-process ………………………………..

Raw materials ……………………………………

Factory supplies………………………………..

Note 1. Lower-of-cost (first-in, first-out) or-market is applied on a

Note 2. Seventy-five percent of bar end shifters finished goods

inventory in the amount of $136,500 ($182,000 X .75) is

PROBLEM 9-9 (Continued)

Supporting Calculations

Finished

Goods

Work-in-

Process

Raw

Materials

Factory

Supplies

Down tube shifters at market ……..

$266,000

Bar end shifters at cost ……………..

182,000

Head tube shifters at cost ………….

195,000

$108,700

Derailleurs at market …………………

Remaining items at market ………..

Supplies at cost ………………………..

(b) The decline in the market value of inventory below cost may be

reported using one or two alternate methods, the direct write-down of

inventory (cost-of-goods-sold method) or the (loss method). An

allowance may be used under either method to report inventory on

(c) Purchase contracts for which a firm price has been established should

be disclosed on the financial statements of the buyer. If the contract

price is greater than the current market price and a loss is expected

PROBLEM 9-10

(a) Schedule A

Item

On Hand

Quantity

Replacement

Cost/Unit

NRV

(Ceiling)

NRV—

Normal

Profit

(Floor)

Designated

Market

Cost

Lower-of–

Cost-or–

Market

A

1,100

$8.40

$9.00

$7.20

$8.40

$7.50

$7.50

B

800

7.90

8.50

7.30

7.90

8.20

7.90

C

1,000

5.40

6.05

5.45

5.45

5.60

5.45

D

4.20

5.50

4.00

4.20

3.80

3.80

E

1,400

6.30

6.00

5.00

6.00

6.40

6.00

Schedule B

Item

Cost

Lower-of-Cost-or-Market

Difference

A

1,100 X $7.50 = $8,250

1,100 X $7.50 = $8,250

None

C

1,000 X $5.60 = $5,600

1,000 X $5.45 = $5,450

D

1,000 X $3.80 = $3,800

1,000 X $3.80 = $3,800

None

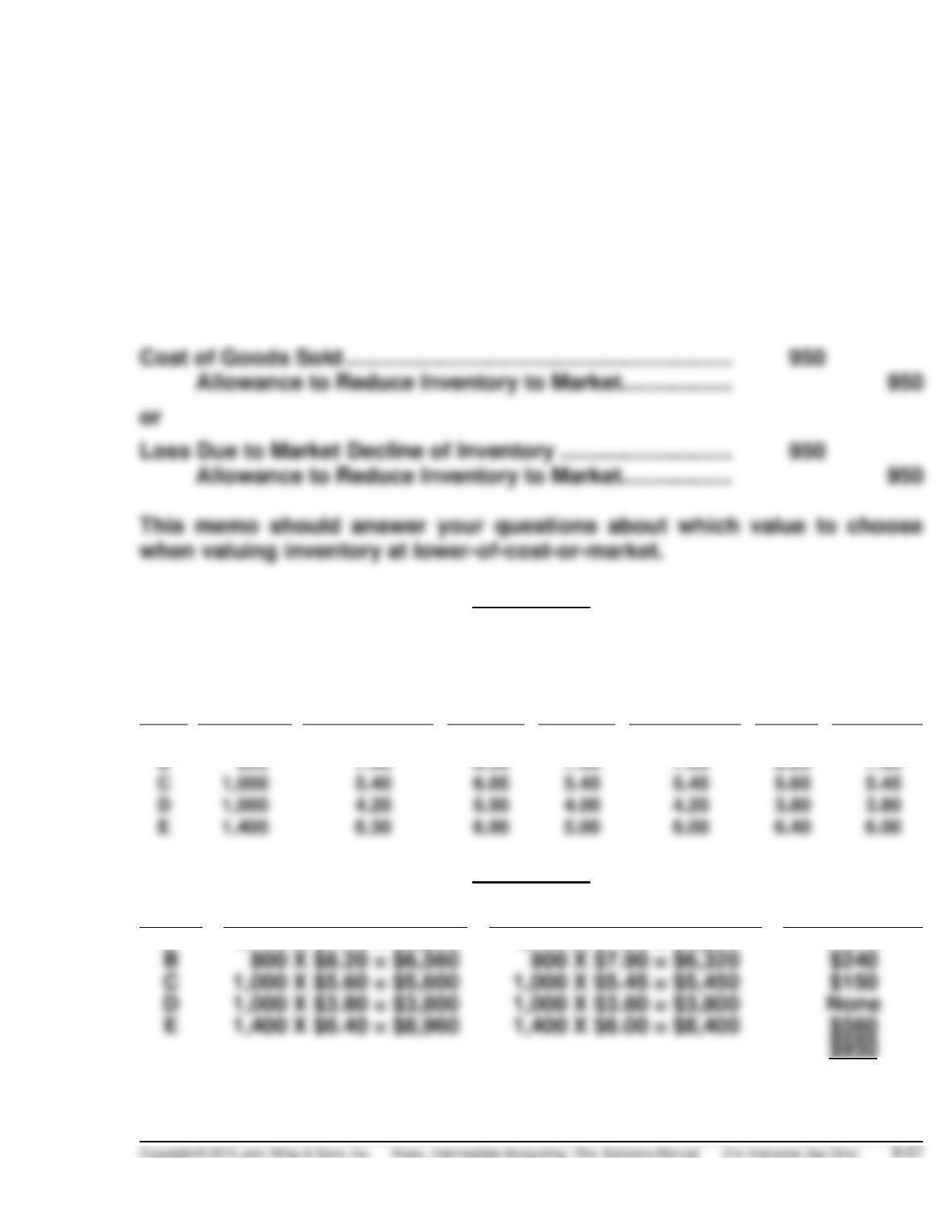

(b) Cost of Goods Sold ……………………………………………………….

950

Allowance to Reduce Inventory to Market …………………

950

or

Loss Due to Market Decline of Inventory …………………………

950

Allowance to Reduce Inventory to Market …………………

950

PROBLEM 9-10 (Continued)

(c)

To: Greg Forda, Clerk

From: Accounting Manager

Date: January 14, 2015

Subject: Instructions on determining lower–of-cost-or-market for inven-

tory valuation

This memo responds to your questions regarding our use of lower–of–cost-

or-market for inventory valuation. Simply put, value inventory at whichever

is the lower: the actual cost or the market value of the inventory at the time

of valuation.

Refer to Item A on the attached schedule. The values for the replacement

cost, net realizable value, and net realizable value less a normal profit margin

are $8.40, $9.00 ($10.50 – $1.50), and $7.20 ($9.00 – $1.80) respectively. The

middle value is the replacement cost, $8.40, which becomes the designated

PROBLEM 9-10 (Continued)

Proceed in the same way, always choosing the middle value among replace-

ment cost, net realizable value, and net realizable value less a normal profit,

and compare that middle value to the actual cost. The lower of these will

always be the amount at which you value the particular item.

After you have aggregated the total lower–of-cost-or-market for all items,

you will be likely to have a loss on inventory which must be accounted for.

In our example, the loss is $950. You can journalize this loss in one of two

ways:

Schedule A

Item

On Hand

Quantity

Replacement

Cost/Unit

NRV

Ceiling

NRV—

Normal

Profit

(Floor)

Designated

Market

Cost

Lower-of–

Cost-or–

Market

A

1,100

$8.40

$9.00

$7.20

$8.40

$7.50

$7.50

B

C

1,000

D

1,000

E

1,400

Schedule B

Item

Cost

Lower-of-Cost-or-Market

Difference

A

1,100 X $7.50 = $8,250

1,100 X $7.50 = $8,250

None

B

800 X $8.20 = $6,560

800 X $7.90 = $6,320

C

1,000 X $5.60 = $5,600

1,000 X $5.45 = $5,450

D

1,000 X $3.80 = $3,800

1,000 X $3.80 = $3,800

None

1,400 X $6.40 = $8,960

1,400 X $6.00 = $8,400

*PROBLEM 9-11

(a)

Cost

Retail

Inventory, January 1 …………………..

$ 30,000

$ 43,000

Purchases ………………………………….

104,800

155,000

Purchase returns ………………………..

(2,800)

(4,000)

Totals ………………………………..

132,000

194,000

Add: Net markups

Markups …………………………...

Markup cancellations …………

(3,200)

6,000

Deduct: Net markdowns

Markdowns ………………………..

Markdown cancellations ……..

4,000

Sales price of goods available …….

196,000

Sales revenue …………………………….

Sales returns and allowances ……..

Ending inventory at retail ……………

$ 50,000

Cost-to-retail ratio =

$132,000

= 66%

$200,000

(b)

Ending inventory at retail at January 1 price level

($59,400 ÷ 1.08) …………………………………………………………

$ 55,000

Less beginning inventory at retail ………………………………..

43,000

Inventory increment at retail, January 1 price level ………..

Beginning inventory at cost …………………………………………

Ending inventory at dollar-value LIFO cost ……………………

*PROBLEM 9-12

(a) The retail method is appropriate in businesses that sell many different

items at relatively low unit costs and that have a large volume of

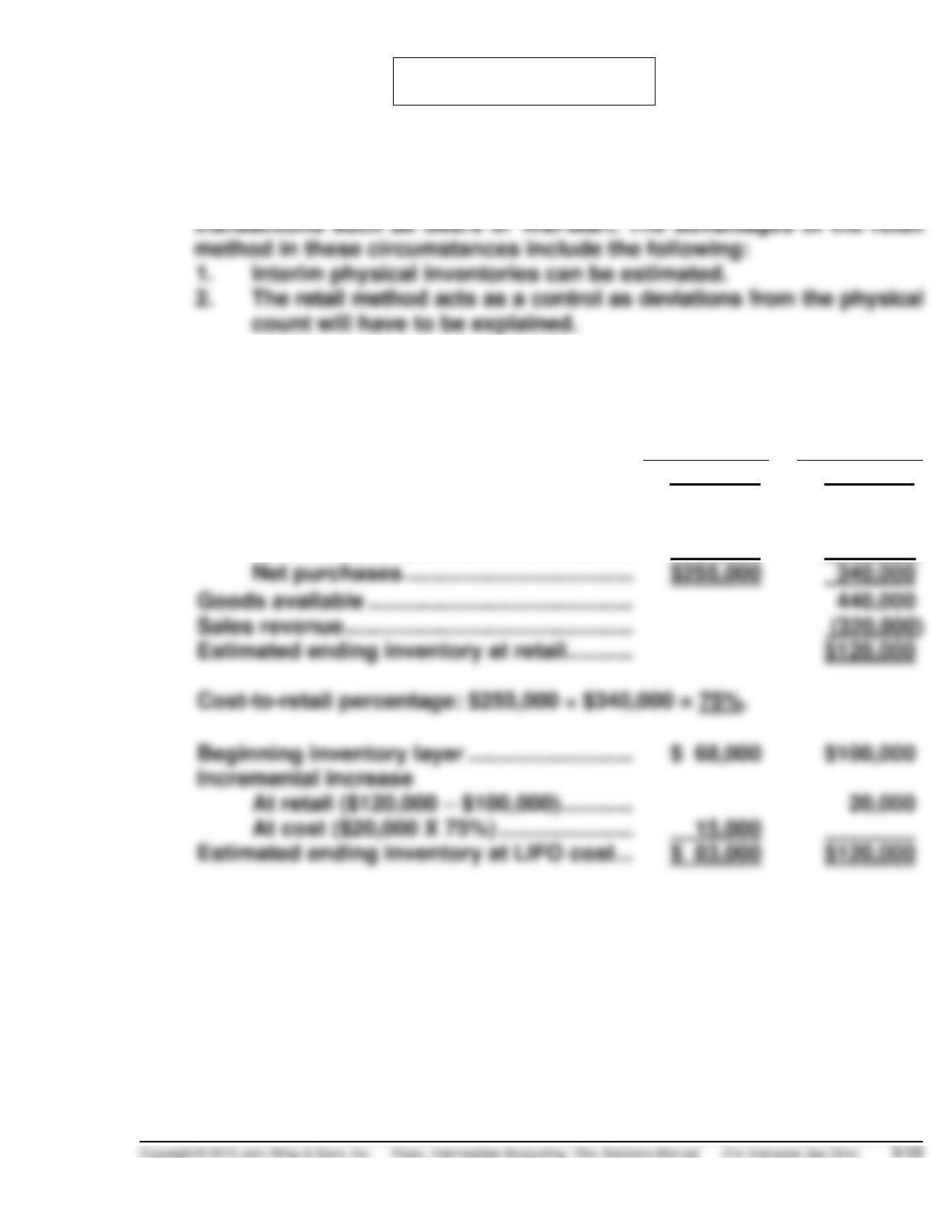

(b) Becker Department Stores’ ending inventory value, at cost, is $83,000,

calculated as follows:

Cost

Retail

Beginning inventory ………………………………

$ 68,000

$100,000

Purchases ……………………………………………..

$255,000

$400,000

Net markups ………………………………….

50,000

Net markdowns ……………………………..

(110,000)

Goods available …………………………………….

440,000

Sales revenue ………………………………………..

(320,000)

Estimated ending inventory at retail ………..

$120,000

Beginning inventory layer ………………………

$ 68,000

$100,000

Incremental increase

20,000

At cost ($20,000 X 75%) ………………….

15,000

*PROBLEM 9-12 (Continued)

(c) The estimated shortage amount, at retail, for Becker Department Stores

is $5,000 calculated as follows:

Estimated ending inventory at retail ………………………….

$120,000

Actual ending inventory at retail ……………………………….

(d) When using the retail inventory method, the four expenses and allow–

ances noted are treated in the following manner:

1. Freight costs are added to the cost of purchases.

2. Purchase returns are considered as reductions to both the cost