PROBLEM 6-8B

Vendor A:

$ 50,000

payment

X 3.99271

(PV of ordinary annuity 8%, 5 periods)

$ 199,636

+ 40,000

down payment

+ 47,000

maintenance contract

$ 286,636

total cost from Vendor A

Vendor B:

$ 14,000

semiannual payment

(PV of annuity due 4%, 40 periods)

$ 288,183

Vendor C:

$ 3,000

X 6.71008

(PV of ordinary annuity of 10 periods, 8%)

$ 20,130

PV of first 10 years of maintenance

$ 5,000

[PV of ordinary annuity 20 per., 8% (9.81815) –

X 3.10807

PV of ordinary annuity 10 per., 8% (6.71008)]

$ 15,540

PV of next 10 years of maintenance

$ 12,000

[(PV of ordinary annuity 30 per., 8% (11.25778) –

PV of ordinary annuity 20 per., 8% (9.81815)]

$ 17,276

PV of last 10 years of maintenance

Total cost of stamping machine and maintenance Vendor C:

$ 225,000

cash purchase price

maintenance years 1–10

maintenance years 11–20

17,276

maintenance years 21–30

$ 277,946

PROBLEM 6-9B

(a) Time diagram for the first ten payments:

i = 12%

PV–AD = ?

R =

$600,000 $600,000 $600,000 $600,000 $600,000 $600,000 $600,000

n = 10

Formula for the first ten payments:

Formula for the last ten payments:

Note: The present value of an ordinary annuity is used here, not the

present value of an annuity due.

PROBLEM 6-9B (Continued)

OR

Time diagram for the last ten payments:

i = 12%

PV = ? R = $500,000 $500,000 $500,000 $500,000

Formulas for the last ten payments:

(i) Present value of the last ten payments:

PROBLEM 6-9B (Continued)

(ii) Present value of the last ten payments at the beginning of current

year:

(b) Time diagram:

i = 12%

PV – OA = ?

R =

PROBLEM 6-9B (Continued)

Formula: PV – OA = R (PVF – OAn, i)

(c) Time diagram:

Amount paid =

$297,000

(i) Implied interest for the period from the end of discount period to

the due date:

PROBLEM 6-9B (Continued)

(ii) Convert the implied interest rate to annual basis:

PROBLEM 6-10B

1. Purchase.

Time diagrams:

Installments

Property taxes and other costs

i = 8%

PV – OA = ?

R =

PROBLEM 6-10B (Continued)

Insurance

i = 8%

PV – AD = ?

R =

$60,000 $60,000 $60,000 $60,000 $60,000 $60,000

Salvage Value

i = 8%

PV = ? FV = $250,000

Formula for installments:

PROBLEM 6-10B (Continued)

Formula for property taxes and other costs:

Formula for insurance:

Formula for salvage value:

PROBLEM 6-10B (Continued)

Present value of net purchase costs:

Down payment………………………………………………..

$ 600,000

Installments ……………………………………………………

Property taxes and other costs ………………………..

Insurance ……………………………………………………….

554,654

Total costs ……………………………………………………..

$6,906,359

Less: Salvage value ……………………………………….

2. Lease.

Time diagrams:

Lease payments

i = 8%

PV – AD = ?

R =

Interest lost on the deposit

i = 8%

PV – OA = ?

R =

PROBLEM 6-10B (Continued)

Formula for lease payments:

Formula for interest lost on the deposit:

Interest lost on the deposit per year = $75,000 (8%) = $6,000

Cost for leasing the facilities = $6,933,180 + $51,357 = $6,984,537

PROBLEM 6-11B

(a) Annual retirement benefits.

Tom–current salary

$ 60,000

X 1.86030

(future value of 1, 21 periods, 3%)

annual salary during last year of work

X 0.60

retirement benefit %

John–current salary

$ 45,000

X 1.75351

(future value of 1, 19 periods, 3%)

78,908

annual salary during last year of work

X 0.40

retirement benefit %

$ 31,563

annual retirement benefit

Jennifer–current salary

$ 40,000

X 1.86030

(future value of 1, 21 periods, 3%)

74,412

annual salary during last year of work

X 0.40

retirement benefit %

$ 29,765

annual retirement benefit

Jerry–current salary

$ 38,000

X 2.03279

(future value of 1, 24 periods, 3%)

77,246

annual salary during last year of work

X 0.40

retirement benefit %

$ 30,898

annual retirement benefit

$ 35,000

(future value of 1, 25 periods, 3%)

retirement benefit %

$ 29,313

annual retirement benefit

PROBLEM 6-11B (Continued)

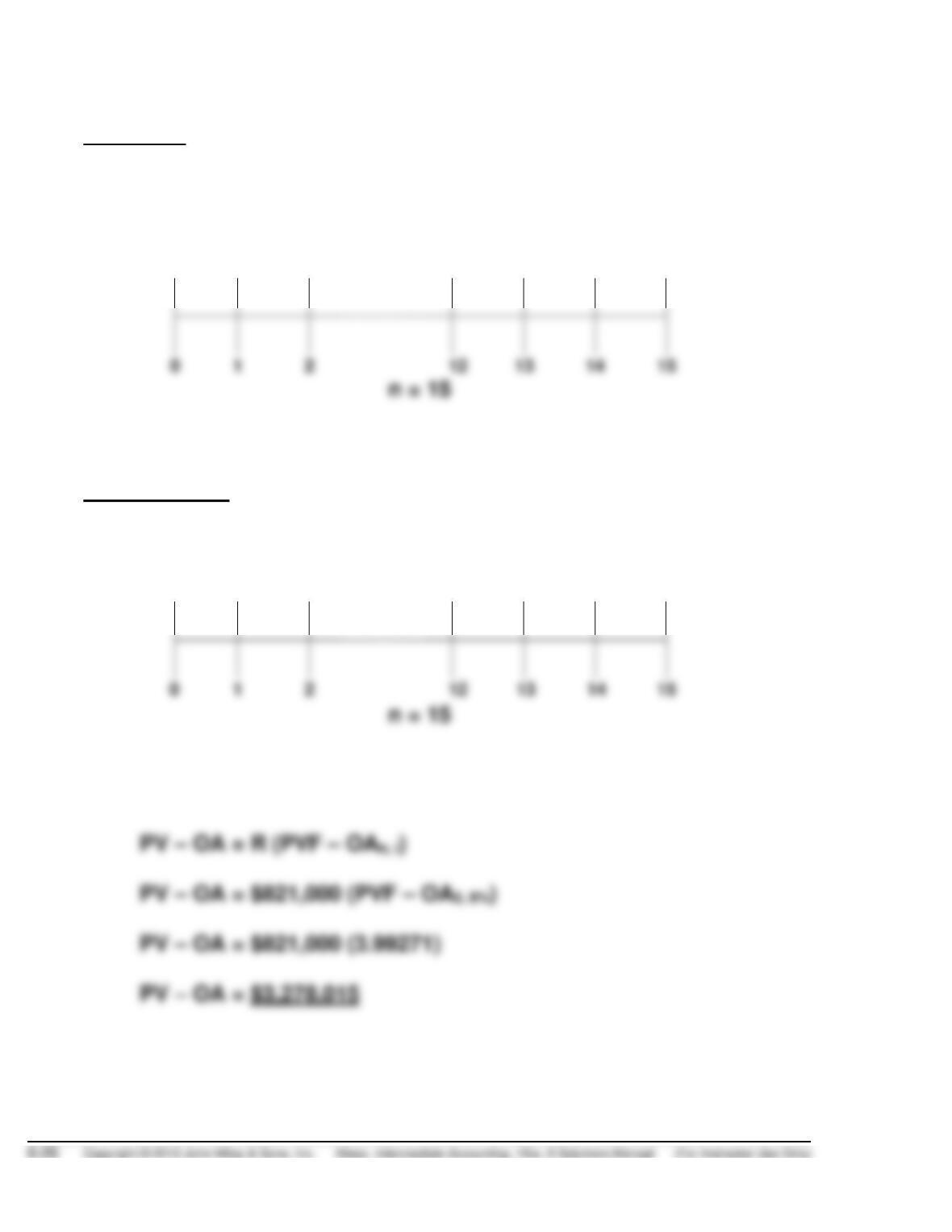

(b) Fund requirements after 20 years of deposits at 8%.

Tom will retire 2 years after deposits stop.

John will retire the beginning of the year after deposits stop.

$ 31,563

annual plan benefit

X 9.24424

(PV of an annuity due for 15 periods)

$ 291,776

Jennifer will retire 2 years after deposits stop.

$ 29,765

annual plan benefit

[PV of an annuity due for 17 periods – PV of an annuity

due for 2 periods (9.85137 – 1.92593)]

$ 235,901

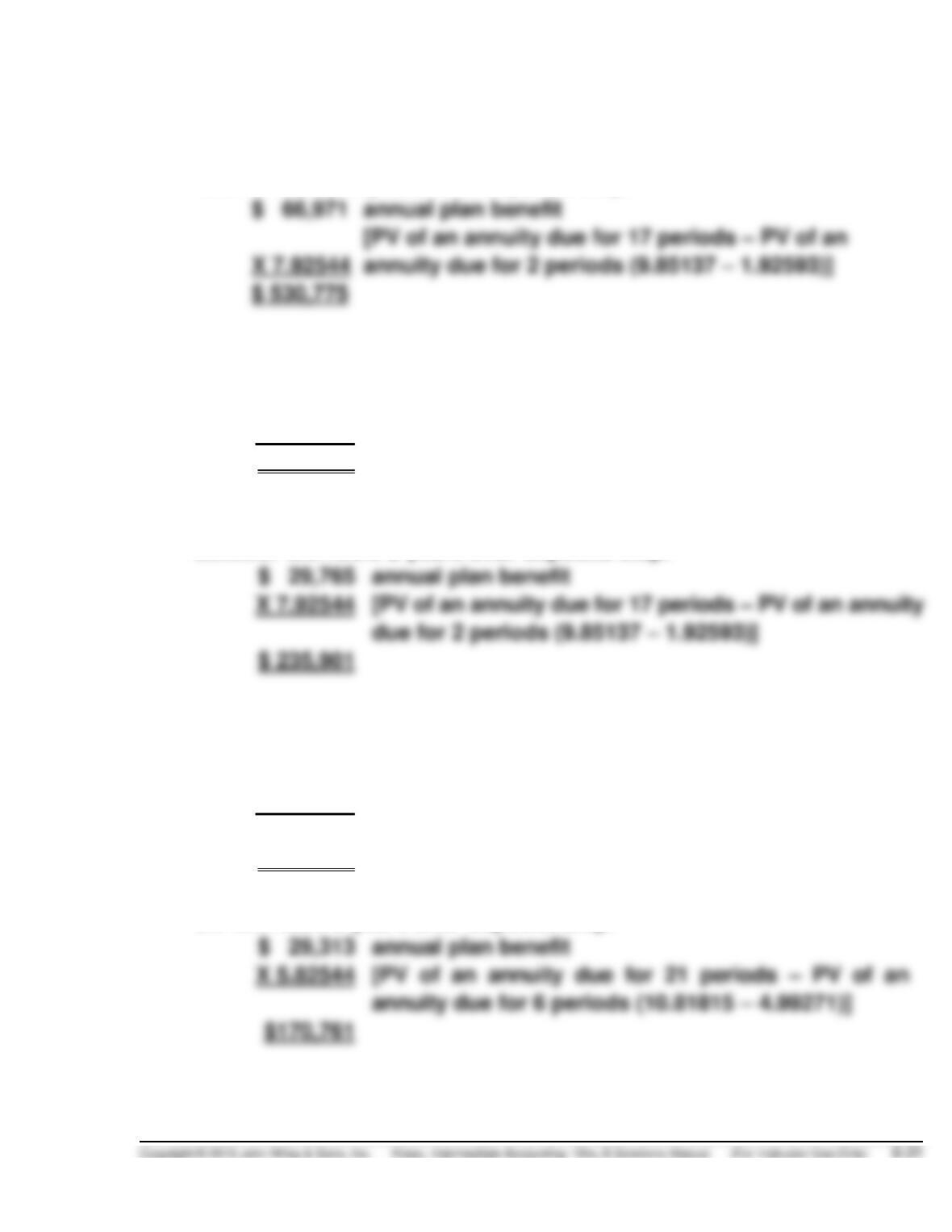

Jerry will retire 5 years after deposits stop.

$ 30,898

annual plan benefit

X 6.29147

[PV of an annuity due for 20 periods – PV of an

annuity due for 5 periods (10.60360 – 4.31213)]

$ 194,394

Jill will retire 6 years after deposits stop.

$ 29,313

annual plan benefit

X 5.82544

[PV of an annuity due for 21 periods – PV of an

annuity due for 6 periods (10.81815 – 4.99271)]

PROBLEM 6-11B (Continued)

$530,775

Tom

John

(c) Required annual beginning-of-the-year deposits at 8%:

Deposit X (future value of an annuity due for 20 periods at 8%) = FV

Deposit X (49.42292) = $1,423,607

PROBLEM 6-12B

(a) The time value of money would suggest that Omega’s discount rate

was substantially higher than Zion Security’s. The actuaries at Omega

(b) As the controller of Chicago Apple, Hudson assumes a fiduciary

responsibility to the present and future retirees of the corporation. As

a result, she is responsible for ensuring that the pension assets are

(c) If Chicago Apple switched to Omega

The primary beneficiaries of Hudson’s decision would be the corporation

and its many stockholders by virtue of reducing $11.5 million of

annual pension costs.

If Chicago Apple stayed with Zion Security

In the short run, the primary beneficiaries of Hudson’s decision would

be the employees and retirees of Chicago Apple given the lower risk

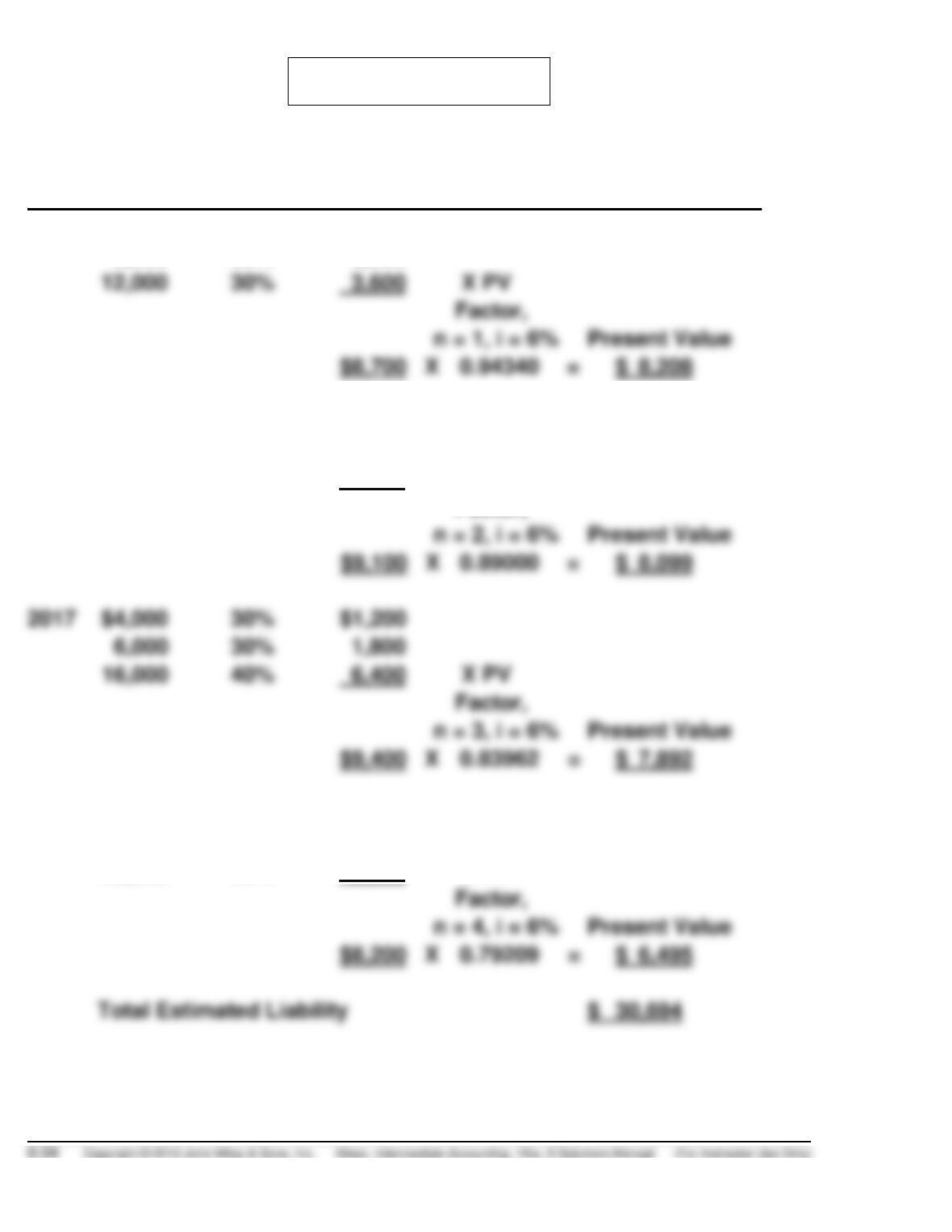

PROBLEM 6-13B

Cash Flow Probability

Estimate X Assessment = Expected Cash Flow

2015 $15,000 10% $1,500

6,000 60% 3,600

2016 $3,000 20% $ 600

8,000 50% 4,000

15,000 30% 4,500 X PV

Factor,

2018 $ 3,000 60% $1,800

7,000 20% 1,400

25,000 20% 5,000 X PV

PROBLEM 6-14B

Cash Flow Probability

Estimate X Assessment = Expected Cash Flow

2015 $ 8,000 30% $ 2,400

11,000 70% 7,700 X PV

Factor,

Scrap

Value

Received

at the End

of 2016 $ 600 60% $ 360

1,200 40% 480 X PV

PROBLEM 6-15B

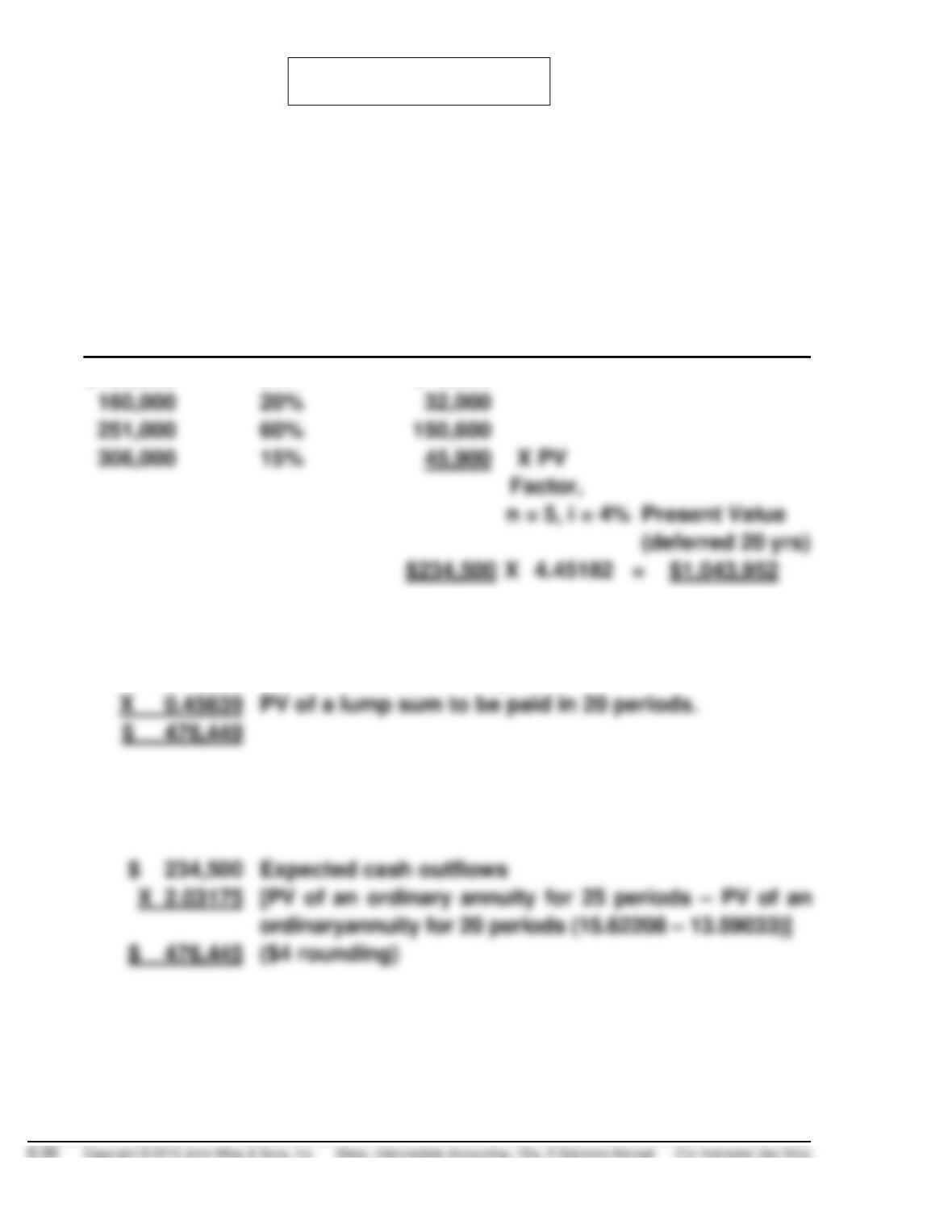

(a) The expected cash flows to meet the asset retirement obligation repre-

sent a deferred annuity. Developing a fair value estimate requires

determining the present value of the annuity of expected cash flows

to be paid in three years and then determine the present value of that

amount today.

Cash Flow Probability

Estimate X Assessment = Expected Cash Flow

$120,000 5% $ 6,000

The value today of the annuity payments to commence in 20 years is:

$ 1,043,952

Present value of annuity

PV of a lump sum to be paid in 20 periods.

Alternatively, the present value of the deferred annuity can be computed

as follows:

Expected cash outflows

(b) This fair value estimate is based on unobservable inputs—DLI’s own

data on the expected future cash flows associated with the obligation

to restore the site. This fair value estimate is considered Level 3, as

discussed in Chapter 2.