E14-17B (15–20 minutes)

(a)

Face value of the zero-interest-bearing note…………………

$500,000

Discounting factor (15% for 5 periods) …………………………

X 0.49718

Amount to be recorded for the land at January 1, 2015 ……

$248,590

Carrying value of the note at January 1, 2015 ……………….

Applicable interest rate (12%) ……………………………………..

X 0.15

Interest expense to be reported in 2015 ……………………….

$ 37,289

(b)

January 1, 2015

Cash ……………………………………………………….

1,000,000

Discount on Notes Payable …………………………..

288,220

Notes Payable…………………………………………………

1,000,000

Unearned Revenue …………………………..

*$1,000,000 – ($1,000,000 X 0.71178) = $288,220

Carrying value of the note

at January 1, 2015 …………………………..

Applicable interest rate (12%) …………………………..

Interest expense to be

reported for 2015 …………………………..

**$1,000,000 – $288,220 = $711,780

E14-18B (15–20 minutes)

(a)

Cash ………………………………………………………………………

200,000

Discount on Notes Payable …………………………..

41,234

Notes Payable…………………………………………………

Unearned Revenue

($200,000 – $158,766) …………………………..

Face value

for 3 years

E14-18B (Continued)

Discount on Notes Payable …………………………..

12,701

Unearned Revenue ($41,234 ÷ 3) …………………………..

Sales ……………………………………………………….

13,745

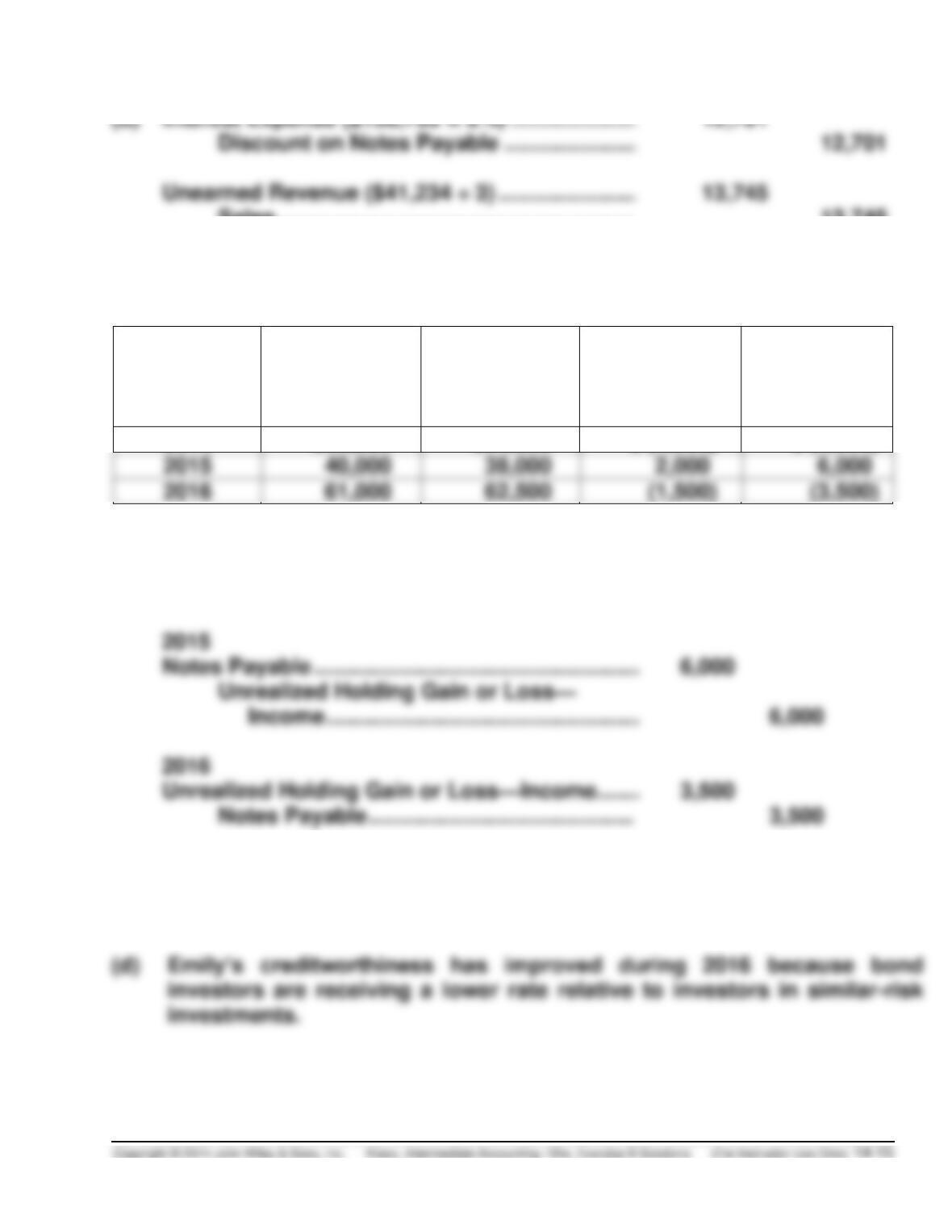

E14–19B (10–15 minutes)

Year Ending

Carrying

Value

Fair Value

Unrealized

Holding Gain

(Loss)

Change in

Unrealized

Holding

Gain (Loss)

2014

$50,000

$54,000

$ (4,000)

$ (4,000)

2016

(a)

2014

Unrealized Holding Gain or Loss—Income. ……………….

4,000

Notes Payable …………………………..………..

4,000

Notes Payable ……………………………………………………….

2016

Unrealized Holding Gain or Loss—Income. ……………….

Notes Payable …………………………..………..

(b) The fair value of $38,000.

(c) Unrealized holding loss of $3,500.

E14–20B (10–15 minutes)

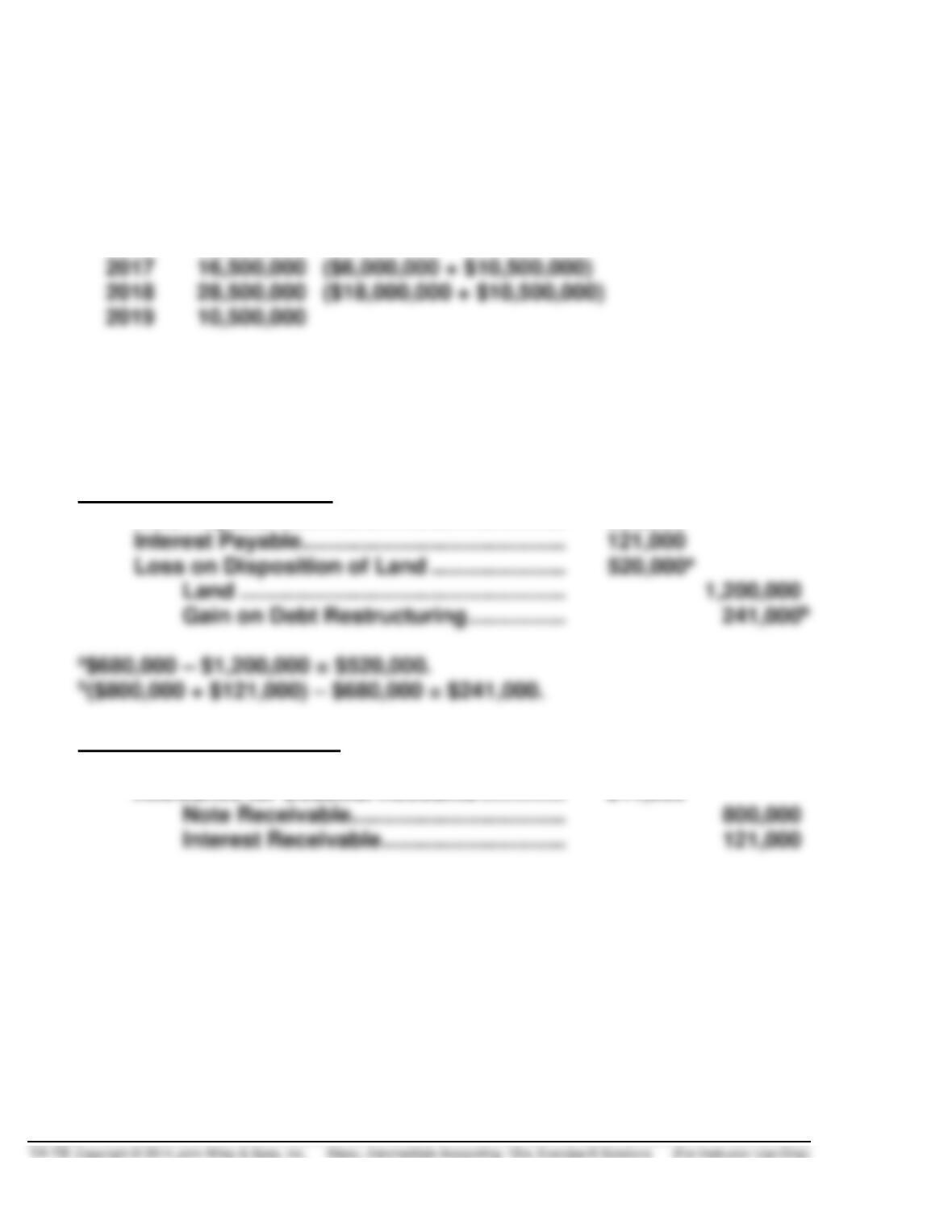

At December 31, 2014, disclosures would be as follows:

Maturities and sinking fund requirements on long-term debt are as follows:

2015

$ 0

2016

10,500,000

2017

($6,000,000 + $10,500,000)

2018

($18,000,000 + $10,500,000)

2019

10,500,000

*E14-21B (15–20 minutes)

(a)

Transfer of property on December 31, 2014:

Nixim Company (Debtor):

Note Payable ………………………………………………….

800,000

Interest Payable ………………………………………………

121,000

Loss on Disposition of Land …………………………..

Land ……………………………………………………….

Gain on Debt Restructuring ………………………

2nd State Bank (Creditor):

Land ……………………………………………………….

680,000

Allowance for Doubtful Accounts …………………….

241,000

Note Receivable……………………………………….

Interest Receivable …………………………..

*E14-21B (Continued)

(b) “Loss on Land” and the “Gain on Debt Restructuring” should be

reported as an ordinary item on the income statement.

(c)

Granting of equity interest on December 31, 2014:

Nixim Company (Debtor):

Note Payable …………………………………………………..

800,000

Interest Payable ………………………………………………

121,000

Common Stock ………………………………………..

Additional Paid-in Capital …………………………

Gain on Debt Restructuring ………………………

2nd State Bank (Creditor):

Investment (Trading) ……………………………………….

680,000

Allowance for Doubtful Accounts …………………….

241,000

Note Receivable ……………………………………….

Interest Receivable …………………………..

*E14-22B (20–30 minutes)

(a) No. The gain recorded by Larkin is not equal to the loss recorded by

Zettlein Bank under the debt restructuring agreement. (You will see why

(b) No. There is no gain under the modified terms because the total future

cash flows after restructuring exceed the total pre-restructuring carrying

amount of the note (principal):

Principal …………………………………………………………

Interest ($8,000,000 X 10% X 3) ………………………..

*E14-22B (Continued)

(c) The interest payment schedule is prepared as follows:

LARKIN COMPANY

Interest Payment Schedule After Debt Restructuring

Effective-Interest Rate 1.4276%

Date

Cash

Interest

(10%)

Effective

Interest

(1.4276%)

Reduction

of Carrying

Amount

Carrying

Amount of

Note

12/31/14

$10,000,000

12/31/15

$ 800,000a

$142,760b

$ 657,240c

9,342,760

12/31/16

800,000

12/31/17

800,000

8,000,000

Total

$2,400,000

$400,000

(d)

Interest payment entry for Larkin Company is:

December 31, 2016

Note Payable ……………………………………………………….

666,623

Interest Expense …………………………………………………….

133,377

Cash ……………………………………………………….

(e)

The payment entry at maturity is:

January 1, 2018

Note Payable ……………………………………………………….

Cash ……………………………………………………….

*E14-23B (25–30 minutes)

(a) Zettlein Bank should use the historical interest rate of 12% to calculate

the loss.

(b)

The loss is computed as follows:

Pre-restructuring carrying amount of note

$10,000,000

Less: Present value of restructured future cash flows:

Present value of principal $8,000,000

due in 3 years at 12%

paid annually for 3 years at 12%

(c) The interest receipt schedule is prepared as follows:

ZETTLEIN BANK

Interest Receipt Schedule After Debt Restructuring

Effective-Interest Rate 12%

Date

Cash

Interest

(10%)

Effective

Interest

(12%)

Increase

in Carrying

Amount

Carrying

Amount of

Note

12/31/14

$7,615,704

12/31/17

*E14-23B (Continued)

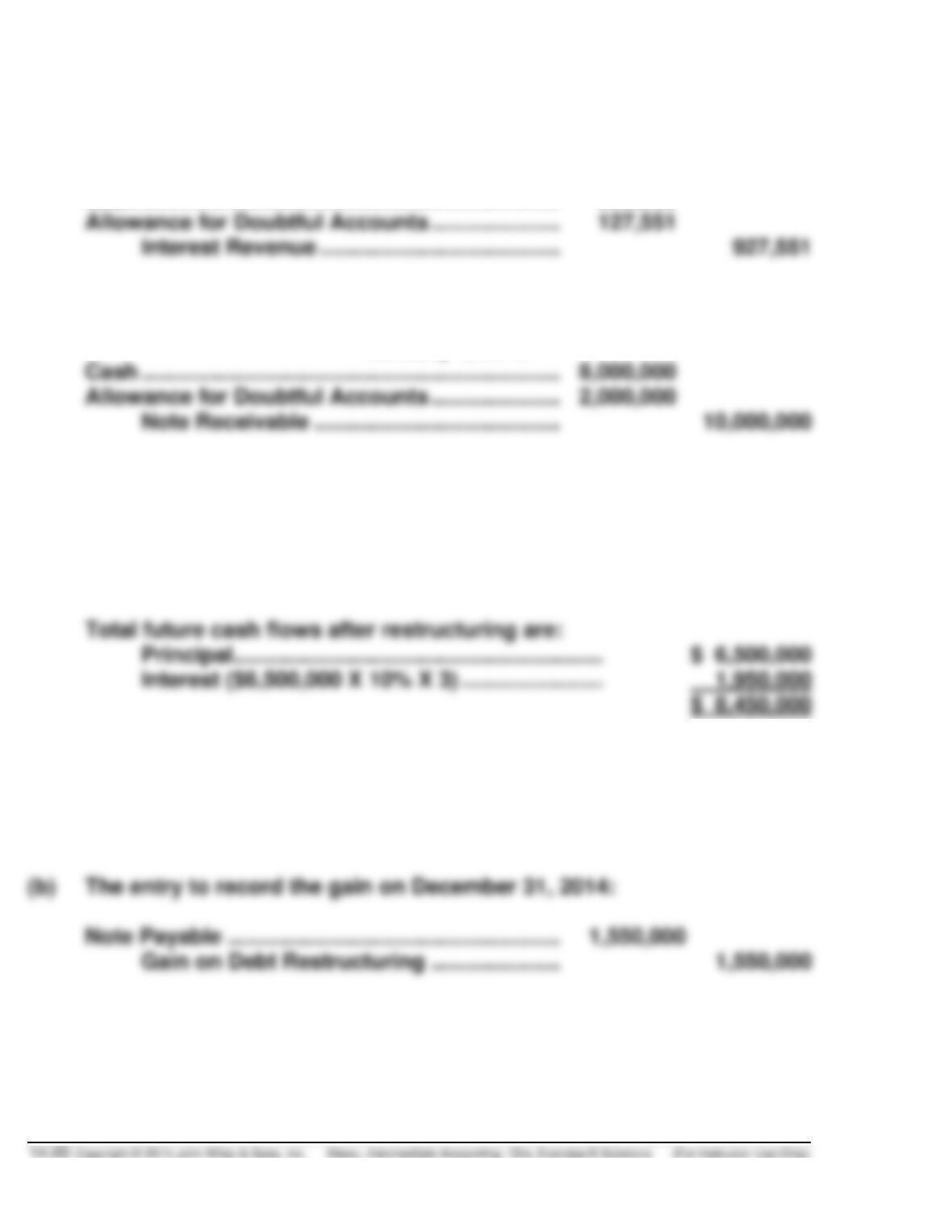

(d)

Interest receipt entry for Zettlein Bank is:

December 31, 2016

Cash ………………………………………………………………………

800,000

Allowance for Doubtful Accounts …………………………..

127,551

Interest Revenue …………………………………………….

(e)

The receipt entry at maturity is:

January 1, 2018

Cash ………………………………………………………………………

Allowance for Doubtful Accounts …………………………..

Note Receivable ……………………………………………..

*E14-24B (25–30 minutes)

(a) Yes. Larkin Company can record a gain under this term modification.

The gain is calculated as follows:

Total future cash flows after restructuring are:

Principal ……………………………………………………….

Interest ($6,500,000 X 10% X 3) ………………………..

Total pre-restructuring carrying amount of note

(principal): ……………………………………………………….

$10,000,000

Therefore, the gain = $10,000,000 – $8,450,000 = $1,550,000.

(b)

The entry to record the gain on December 31, 2014:

Note Payable …………………………..…………………………..

Gain on Debt Restructuring …………………………..

*E14-24B (Continued)

(c)

Because the new carrying value of the note ($10,000,000 – $1,550,000 =

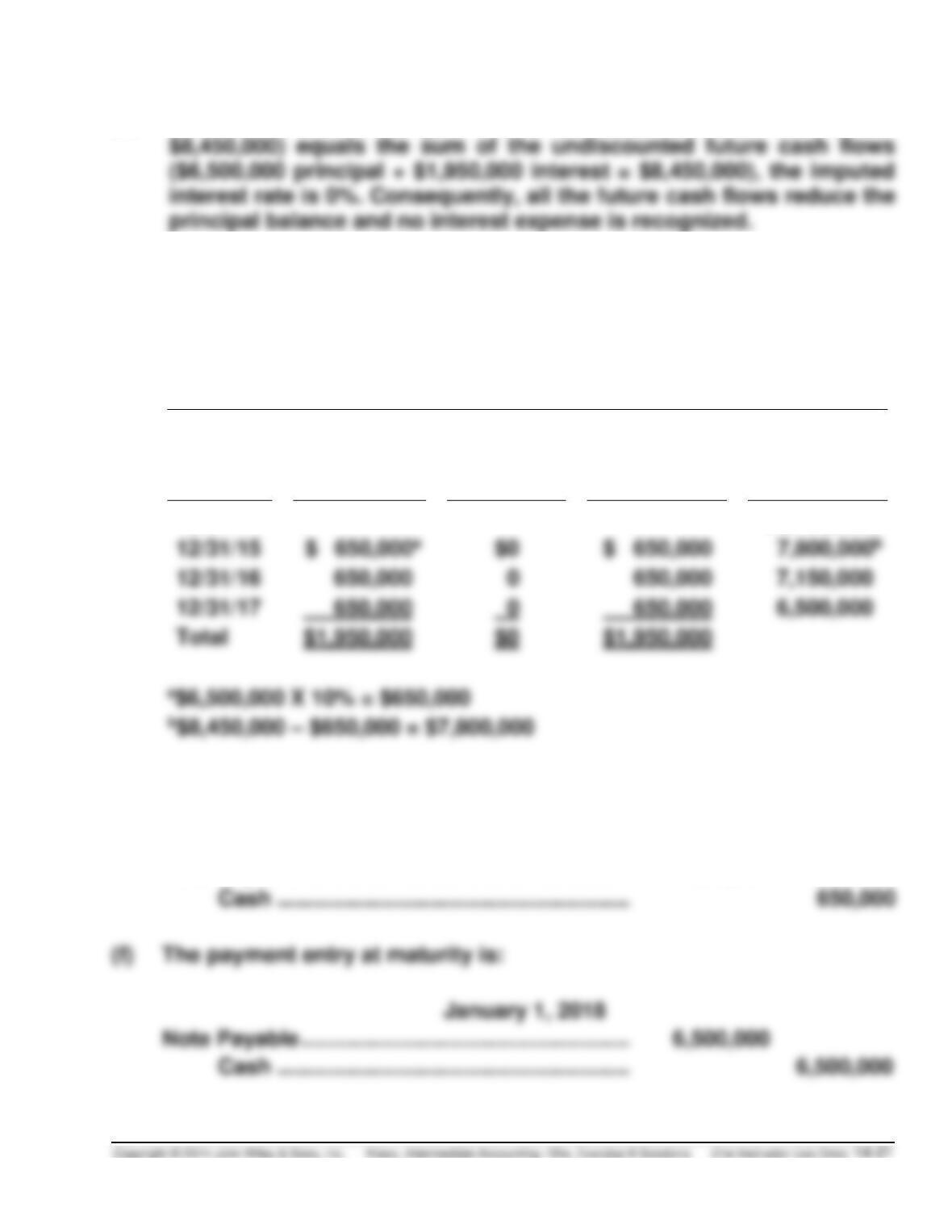

(d) The interest payment schedule is prepared as follows:

LARKIN COMPANY

Interest Payment Schedule After Debt Restructuring

Effective-Interest Rate 0%

Date

Cash

Interest

(10%)

Effective

Interest

(0%)

Reduction

of Carrying

Amount

Carrying

Amount of

Note

12/31/14

$8,450,000

12/31/15

$ 650,000

12/31/17

650,000

(e)

Cash interest payment entries for Larkin Company are:

December 31, 2015, 2016, and 2017

Note Payable ……………………………………………………….

650,000

The payment entry at maturity is:

Note Payable ……………………………………………………….

*E14-25B (20–30 minutes)

(a)

The loss can be calculated as follows:

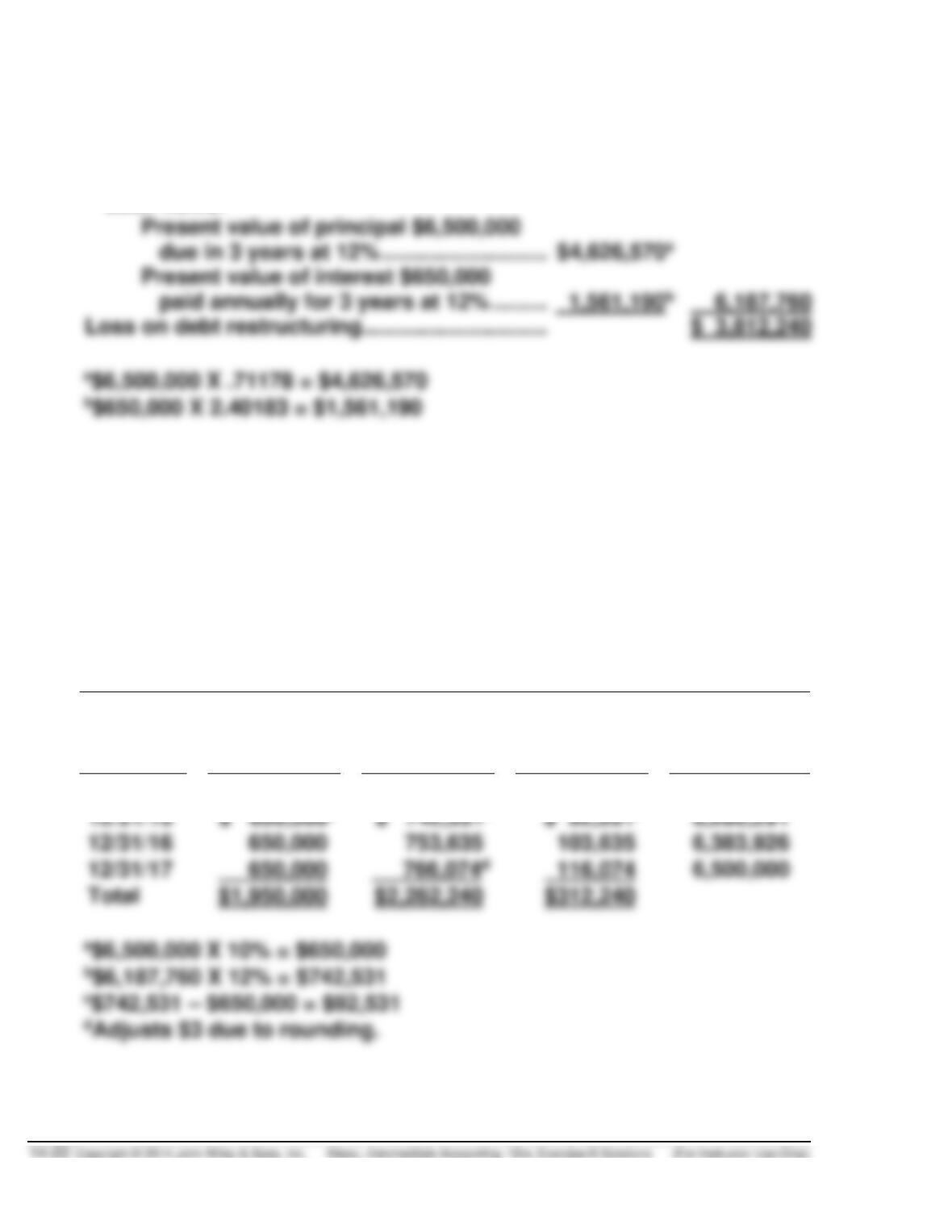

Pre-restructuring carrying amount of note ……………….

$10,000,000

Less: Present value of restructured future

Cash flows:

Present value of principal $6,500,000

due in 3 years at 12% …………………………..

Present value of interest $650,000

paid annually for 3 years at 12% ……………………

6,187,760

December 31, 2014

Bad Debt Expense …………………………………………………..

3,812,240

Allowance for Doubtful Accounts …………………….

3,812,240

(b) The interest receipt schedule is prepared as follows:

ZETTLEIN BANK

Interest Receipt Schedule After Debt Restructuring

Effective-Interest Rate 12%

Date

Cash

Interest

(10%)

Effective

Interest

(12%)

Increase

in Carrying

Amount

Carrying

Amount of

Note

12/31/14

$6,187,760

12/31/17

650,000

*E14-25B (Continued)

(c)

Interest receipt entries for Zettlein Bank are:

December 31, 2015

Cash ………………………………………………………………………

650,000

Allowance for Doubtful Accounts …………………………..

92,531

Interest Revenue …………………………………………….

742,531

Cash ………………………………………………………………………

Allowance for Doubtful Accounts …………………………..

Interest Revenue …………………………………………….

753,635

Cash ………………………………………………………………………

Allowance for Doubtful Accounts …………………………..

Interest Revenue …………………………………………….

766,074

(d)

The receipt entry at maturity is:

January 1, 2018

Cash ………………………………………………………………………

6,500,000

Allowance for Doubtful Accounts …………………………..

Note Receivable ………………………………………………

E14-26B (15–20 minutes)

(a)

Weaver Co.’s entry:

Notes Payable ……………………………………………………….

1,398,600

Property……………………………………………………….

Gain on Property Disposition …………………………..

Gain on Restructuring …………………………..

*$1,398,600 – $840,000

E14-26B (Continued)

(b)

McBride Inc.’s entry:

Property ……………………………………………………….

Allowance for Doubtful Accounts …………………………..

(or Bad Debt Expense) ………………………………………….

Notes Receivable ……………………………………………

1,398,600

*E14-27B (20–25 minutes)

Because the carrying amount of the debt, $600,000 exceeds the total future

cash flows $590,000 [$500,000 + ($30,000 X 3)], a gain is recognized and no

interest is recorded by the debtor.

(a)

Vista Corp.’s entries:

2014 Note Payable ………………………………………………….

10,000

Gain on Restructuring…………………………..

10,000

2015 Note Payable ………………………………………………….

30,000

Cash (6% X $500,000) …………………………..

Cash (6% X $500,000) …………………………..

2017 Note Payable ………………………………………………….

530,000

Cash

[$500,000 + (6% X $500,000)] ………………….

(b)

First National’s entry on December 31, 2014:

Bad Debt Expense …………………………………………………..

149,734

Allowance for Doubtful Accounts …………………….

149,734

Pre-restructure carrying amount

$600,000

Present value of restructured cash flows:

Present value of $500,000 due in 3 years

at 10%, interest payable annually

(Table 6-2); (500,000 X 0.75132) ……………………..

Present value of $30,000 interest payable

annually for 2 years at 10% (Table 6-4);

($30,000 X 2.48685)……………………………………….

*E14-27B (Continued)

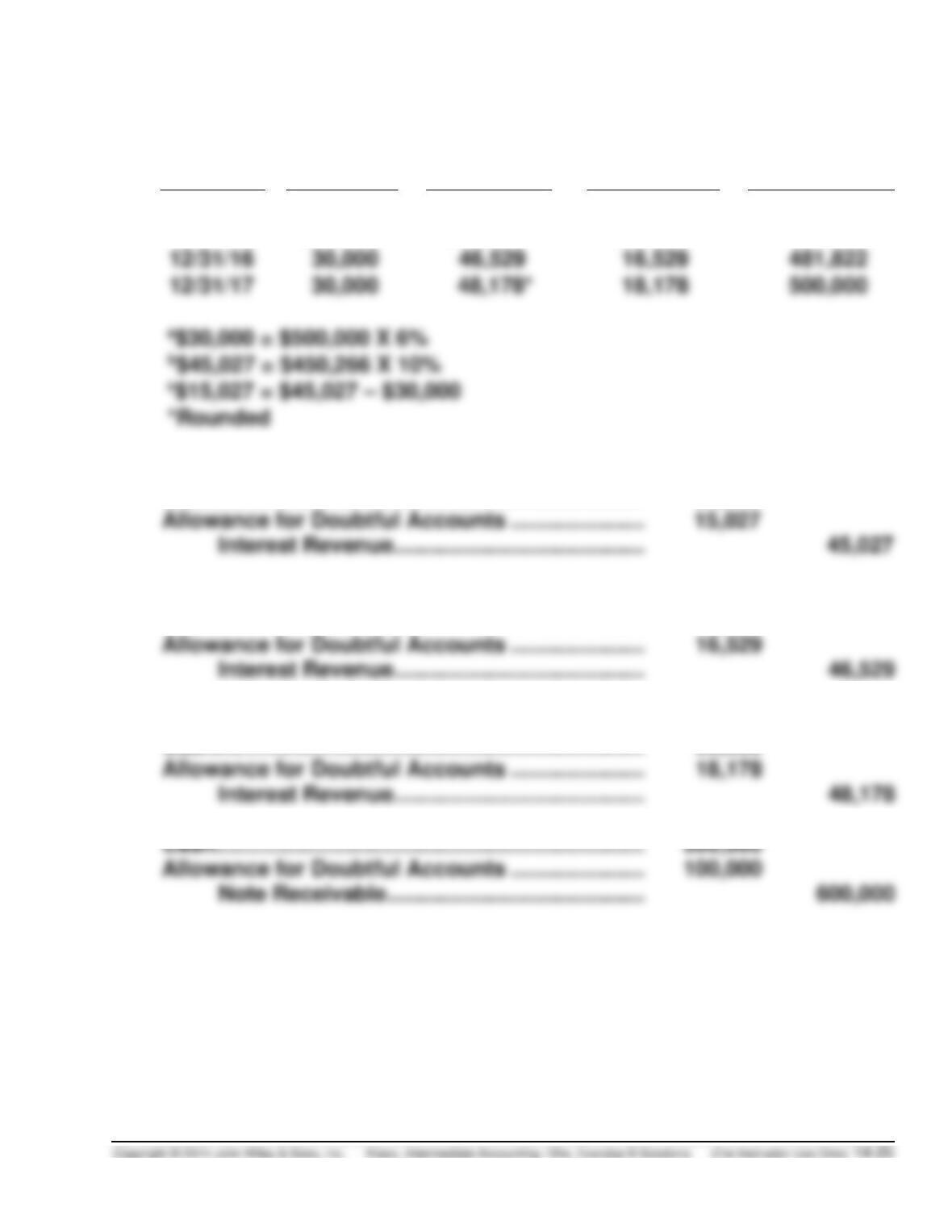

Date

Cash

Interest

Effective-

Interest

Increase

in Carrying

Amount

Carrying

Amount of

Note

12/31/14

$450,266

12/31/15

$30,000a

$45,027b

$15,027c

465,293

12/31/16

481,822

12/31/17

December 31, 2015

Cash……………………………………………………………………….

30,000

Allowance for Doubtful Accounts …………………………..

Interest Revenue ……………………………………………..

December 31, 2016

Cash……………………………………………………………………….

30,000

Allowance for Doubtful Accounts …………………………..

16,529

Interest Revenue ……………………………………………..

December 31, 2017

Cash……………………………………………………………………….

30,000

Allowance for Doubtful Accounts …………………………..

18,178

Interest Revenue ……………………………………………..

Cash……………………………………………………………………….

Allowance for Doubtful Accounts …………………………..

Note Receivable ………………………………………………