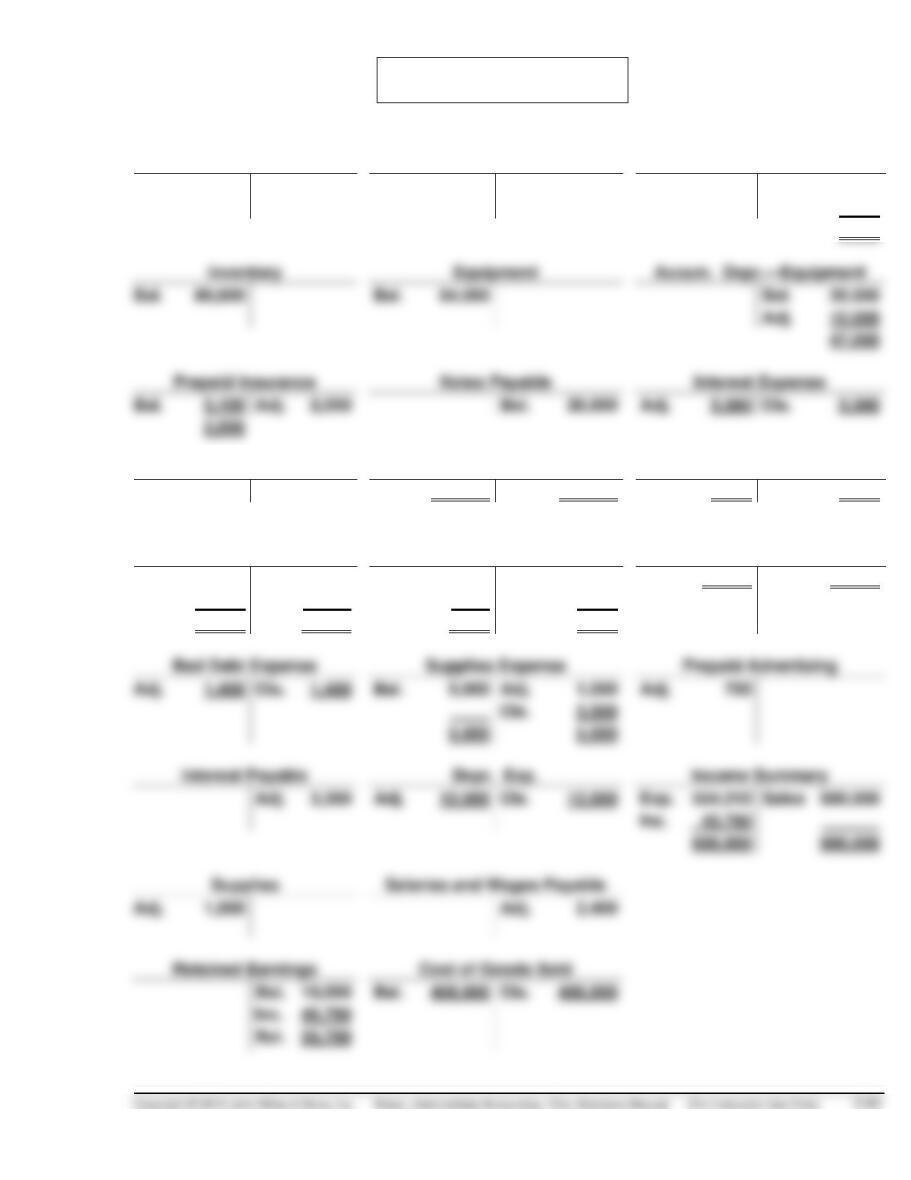

PROBLEM 3-10

(a), (b), (c)

Cash

Accounts Receivable

Allow. for Doubtful Accts.

Bal.

18,500

Bal.

32,000

Bal.

700

Adj.

1,400

2,100

Bal.

80,000

Bal.

84,000

Bal.

35,000

Adj.

12,000

47,000

Bal.

Adj.

2,550

Bal.

28,000

Adj.

3,360

Cls.

3,360

Common Stock

Sales Revenue

Insurance Expense

Bal.

80,600

Cls.

600,000

Bal.

600,000

Adj.

2,550

Cls.

2,550

Salaries and Wages

Expense (Sales)

Advertising Expense

Salaries and Wages Expense

(Administrative)

Bal.

50,000

Cls.

52,400

Bal.

6,700

Adj.

700

Adj.

65,000

Cls.

65,000

Adj.

2,400

Cls.

6,000

52,400

52,400

6,700

6,700

Supplies Expense

Adj.

Cls.

1,400

Bal.

5,000

Adj.

1,500

Adj.

700

Cls.

3,500

5,000

5,000

Income Summary

Adj.

Adj.

12,000

Cls.

12,000

Exp.

554,210

Sales

600,000

Inc.

600,000

600,000

Salaries and Wages Payable

Adj.

Adj.

2,400

Cost of Goods Sold

Bal.

10,000

Bal.

408,000

Cls.

408,000

Inc.

45,790

PROBLEM 3-10 (Continued)

(b)

-1-

Bad Debt Expense ……………………………………………………….

1,400

Allowance for Doubtful Accounts …………………………..

1,400

-2-

Depreciation Expense ($84,000 ÷ 7) …………………………..

12,000

Accumulated Depreciation—Equipment …………………………..

12,000

-3-

Insurance Expense ……………………………………………………….

2,550

Prepaid Insurance ……………………………………………………….

2,550

-4-

Interest Expense ……………………………………………………….

3,360

Interest Payable ……………………………………………………….

3,360

-5-

Salaries and Wages Expense (Sales) …………………………..

2,400

Salaries and Wages Payable …………………………..

2,400

-6-

Prepaid Advertising ……………………………………………………….

Advertising Expense ……………………………………………………….

-7-

Supplies …………………………………………………………………………………

1,500

Supplies Expense ……………………………………………………….

1,500

PROBLEM 3-10 (Continued)

(c)

Dec. 31

Sales Revenue ……………………………………………………….

600,000

Income Summary ……………………………………………………….

600,000

Dec. 31

Income Summary ……………………………………………………….

554,210

Cost of Goods Sold ……………………………………………………….

408,000

Advertising Expense …………………………..…………………………..

Salaries and Wages Expense (Admin.) …………………………..

Salaries and Wages Expense (Sales) …………………………..

Supplies Expense ……………………………………………………….

Insurance Expense ……………………………………………………….

Bad Debt Expense ……………………………………………………….

Depreciation Expense ……………………………………………………….

Interest Expense ……………………………………………………….

Dec. 31

Income Summary ……………………………………………………….

45,790

Retained Earnings ……………………………………………………….

*PROBLEM 3-11

(a) ARKANSAS SALES AND SERVICE

Income Statement

For the Month Ended January 31, 2014

(1)

Cash Basis

(2)

Accrual Basis

Revenues ……………………………………………………….

$ 75,000

$98,400*

Expenses

Cost of computers & printers:

Purchased and paid …………………………..

Cost of goods sold …………………………..

Salaries and wages …………………………..

Rent ……………………………………………………….

Other operating expenses ……………………….

Total expenses …………………………..

106,500

*PROBLEM 3-11 (Continued)

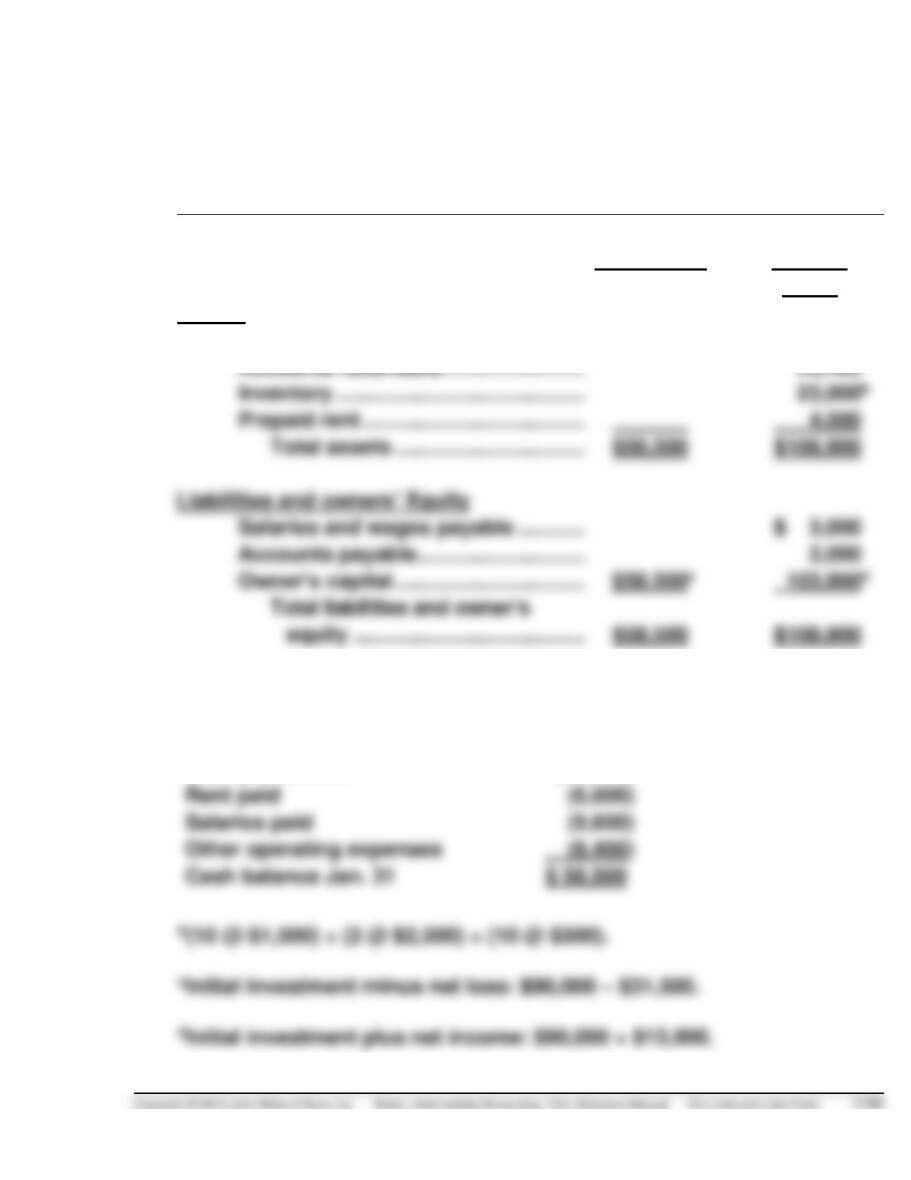

(b) ARKANSAS SALES AND SERVICE

Balance Sheet

As of January 31, 2014

(1)

Cash Basis

(2)

Accrual

Basis

Assets

Cash ………………………………………………………

$58,500a

$ 58,500a

Inventory ………………………………………………..

Prepaid rent ……………………………………………

Total assets …………………………..…………..

Liabilities and owners’ Equity

Salaries and wages payable …………………….

Accounts payable …………………………..

$58,500c

aOriginal investment $ 90,000

Cash sales 75,000

Cash purchases (82,500)

*PROBLEM 3-11 (Continued)

2. The cost of computers and printers sold in January is overstated

by $23,000. The unsold computers and printers are an asset of

$23,000 in the form of inventory.

3. The cash basis ignores $3,000 of the salaries that have been

earned by the employees in January and will be paid in February.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 3-67

*PROBLEM 3-12

(a) COOKE COMPANY

Worksheet

For the Year Ended September 30, 2014

50,000

107,700

2,000

14,000

280,500

109,000

30,500

9,400

16,900

50,000

107,700

2,000

280,500

14,000

109,000

30,500

9,400

16,900

2,000

(d)

50,000

107,700

2,000

278,500

14,000

109,000

30,500

9,400

16,900

Mortgage Payable

Common Stock

Dividends

Retained Earnings

Service Revenue

Sal. and Wages Exp.

Maintenance and

Repairs Expense

Advertising Expense

Utilities Expenses

*PROBLEM 3-12 (Continued)

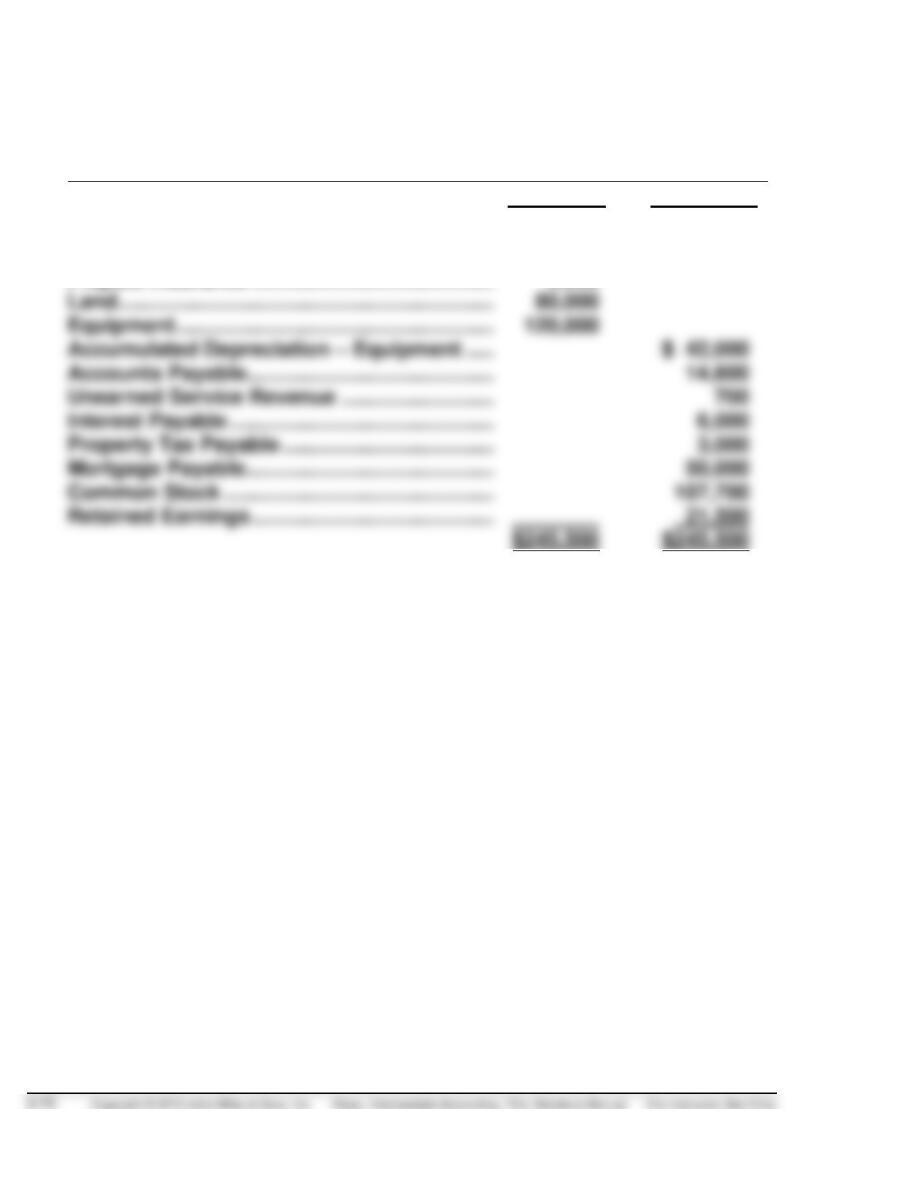

(b) COOKE COMPANY

Balance Sheet

September 30, 2014

Assets

Current assets

Cash ……………………………………………………….

$37,400

Supplies ……………………………………………………….

4,200

Prepaid insurance …………………………..

Property, plant, and equipment

Equipment …………………………..………………………….

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ……………………………………………

$14,600

Current maturity of long-term debt …………………..

10,000

Interest payable ………………………………………….

6,000

Property taxes payable ……………………………………

3,000

Unearned service revenue …………………………..

Total current liabilities …………………………..

Long-term liabilities

Mortgage payable ……………………………………………

Total liabilities ………………………………………..

*PROBLEM 3-12 (Continued)

(c)

Sep. 30

Insurance Expense …………………………..

28,000

Prepaid Insurance …………………………..

28,000

30

Supplies Expense ……………………………………………………….

14,400

Supplies ……………………………………………………….

14,400

Depreciation Expense …………………………..

30

Unearned Service Revenue …………………………..

Service Revenue …………………………..

30

Property Tax Expense …………………………..

Property Taxes Payable …………………………..

30

Interest Expense ……………………………………………………….

Interest Payable …………………………..

(d)

Sep. 30

Service Revenue …………………………..…………………………..

280,500

Income Summary …………………………..

280,500

30

Income Summary ……………………………………………………….

247,000

Salaries and Wages Expense …………………………..

109,000

Maintenance and Repairs

Expense ……………………………………………………….

30,500

Insurance Expense …………………………..

Property Tax Expense …………………………..

21,000

Supplies Expense …………………………..

14,400

Utilities Expenses …………………………..

Interest Expense …………………………..

12,000

Advertising Expense …………………………..

Depreciation Expense …………………………..

Income Summary ……………………………………………………….

33,500

Retained Earnings …………………………..

Retained Earnings …………………………..

14,000

*PROBLEM 3-12 (Continued)

(e) COOKE COMPANY

Post-Closing Trial Balance

September 30, 2014

Debit

Credit

Cash ……………………………………………………….

$ 37,400

Supplies ……………………………………………………….

4,200

Prepaid Insurance ……………………………………………………

3,900

Land ……………………………………………………….

Equipment ……………………………………………………….

Accumulated Depreciation – Equipment ……………………

Accounts Payable …………………………………………………….

14,600

Unearned Service Revenue …………………………..

Interest Payable ……………………………………………………….

Property Tax Payable …………………………..…………………..

Mortgage Payable …………………………………………………….

50,000

Common Stock ……………………………………………………….

Retained Earnings ……………………………………………………

FINANCIAL REPORTING PROBLEM

(a) June 30, 2011 total assets: $138,354 million.

June 30, 2010 total assets: $128,172 million.

(e) An adjusting entry for deferrals is necessary when the receipt/disburse–

ment precedes the recognition in the financial statements. Accounts

such as prepaid insurance and prepaid rent may be included in the

Prepaid Expenses and Other Current Assets ($4,408 million at June 30,

(f) 2011 Depreciation and amortization expense: $2,838 million

2010 Depreciation and amortization expense: $3,108 million

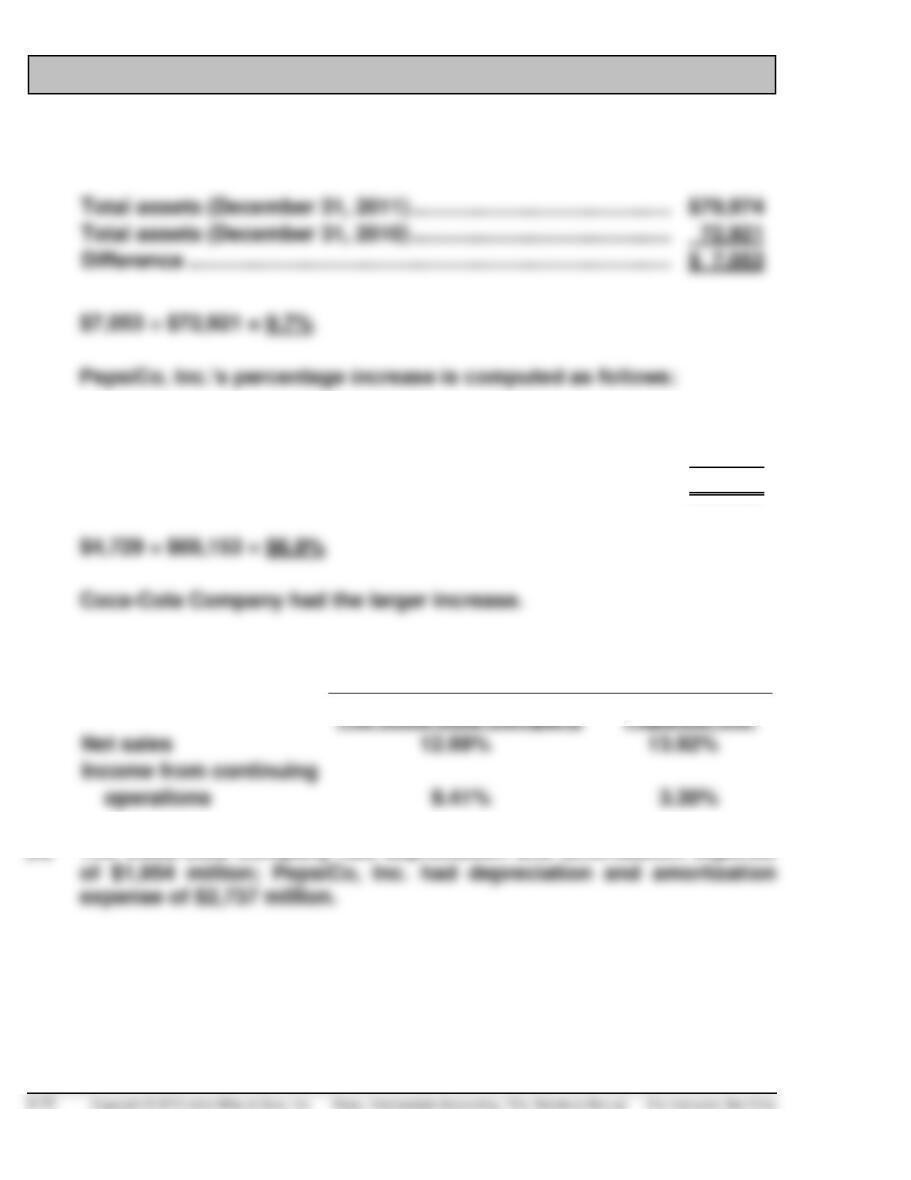

COMPARATIVE ANALYSIS CASE

(a) The Coca-Cola Company percentage increase is computed as follows:

Total assets (December 31, 2011) …………………………………………….

$79,974

Total assets (December 31, 2010) …………………………………………….

72,921

Difference ………………………………………………………………………………

$ 7,053

Total assets (December 29, 2011) …………………………………………….

$72,882

Total assets (December 30, 2010) …………………………………………….

68,153

Difference ………………………………………………………………………………

$ 4,729

(b)

5-Year Growth Rate

The Coca-Cola Company

PepsiCo, Inc.

Net sales

operations

(c) The Coca-Cola Company had depreciation and amortization expense