*PROBLEM 9-13

(a)

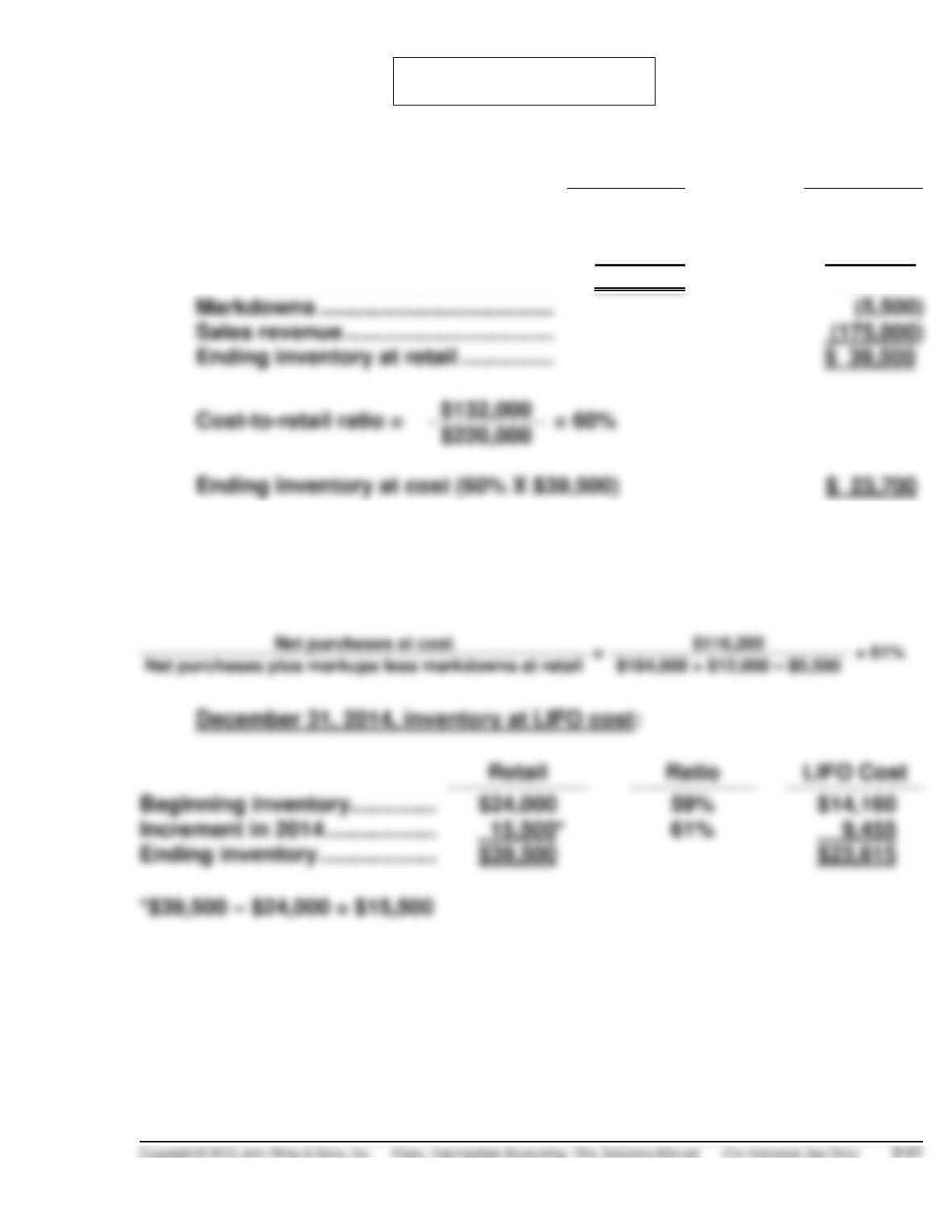

Cost

Retail

Inventory (beginning) ………………….

$ 15,800

$ 24,000

Purchases ………………………………….

116,200

184,000

Markups …………………………………….

12,000

Totals ………………………………..

$132,000

220,000

Markdowns ………………………………..

Sales revenue …………………………….

Ending inventory at retail ……………

Ending inventory at cost (60% X $39,500)

(b)

Ending inventory for 2014 under the LIFO method:

The cost-to-retail ratio for 2014 can be computed as follows:

Beginning inventory …………..

Increment in 2014 ………………

Ending inventory ……………….

*$39,500 – $24,000 = $15,500

*PROBLEM 9-14

(a) DAVENPORT DEPARTMENT STORE

COMPUTATION OF COST

OF DECEMBER 31, 2013, INVENTORY

BASED ON THE CONVENTIONAL RETAIL METHOD

At Cost

At Retail

Beginning inventory, January 1, 2013 …………..

$ 29,800

$ 56,000

Add (deduct) transactions affecting cost ratio:

Purchases ………………………………………….

311,000

554,000

Purchase returns ……………………………….

Purchase discounts …………………………...

Freight-in …………………………………………..

Net markups ………………………………………

20,000

Add (deduct) other retail transactions not

considered in computation of cost ratio:

Gross sales ……………………………………….

(551,000)

Sales returns ……………………………………..

9,000

Net markdowns ………………………………….

Employee discounts …………………………..

Totals …………………………………………..

Inventory, December 31, 2013:

*PROBLEM 9-14 (Continued)

(b) COMPUTATION OF COST

OF DECEMBER 31, 2013 INVENTORY

UNDER THE LIFO RETAIL METHOD

Cost

Retail

Totals used in computing cost ratio under

conventional retail method (part a) …………….

$347,200

$620,000

Exclude beginning inventory ……………………….

Net purchases …………………………………………….

Deduct net markdowns ………………………………..

12,000

Totals used in computing cost ratio under

Cost ratio under LIFO retail method

($317,400 ÷ $552,000) ………………………………..

57.5%

Inventory, December 31, 2013:

At cost under LIFO retail method

*PROBLEM 9-14 (Continued)

(c) COMPUTATION OF 2014 AND 2015

YEAR-END INVENTORIES

UNDER THE DOLLAR-VALUE LIFO METHOD

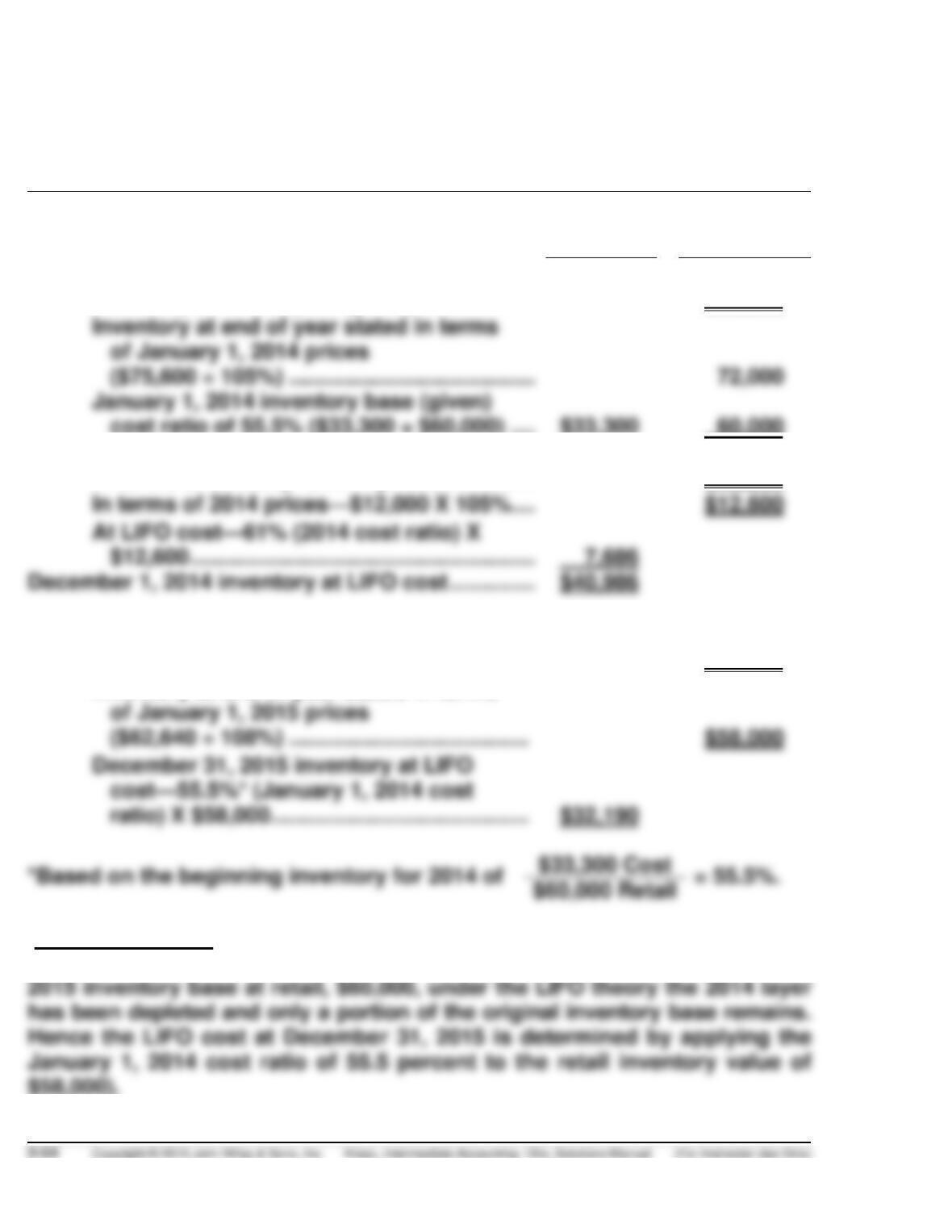

Computation of retail values on the basis of January 1, 2014, price levels

Cost

Retail

2014:

Inventory at end of year (given) ……………….

$75,600

Inventory at end of year stated in terms

of January 1, 2014 prices

($75,600 ÷ 105%) ………………………………….

January 1, 2014 inventory base (given)

cost ratio of 55.5% ($33,300 ÷ $60,000) ….

$33,300

60,000

Increment in inventory:

In terms of January 1, 2014 prices ……………

$12,000

In terms of 2014 prices—$12,000 X 105%….

$12,600

At LIFO cost—61% (2014 cost ratio) X

$12,600 ………………………………………………..

7,686

December 1, 2014 inventory at LIFO cost …………..

2015:

Inventory at end of year (given) ………………

$62,640

Inventory at end of year stated in terms

of January 1, 2015 prices

($62,640 ÷ 108%) …………………………………

$58,000

December 31, 2015 inventory at LIFO

cost—55.5%* (January 1, 2014 cost

ratio) X $58,000 ……………………………………

$33,300 Cost

$60,000 Retail

(Note to instructor: Because the retail inventory stated in terms of January 1,

2014 prices at December 31, 2015, $58,000, has fallen below the January 1,

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 9-1 (Time 15–25 minutes)

Purpose—to provide the student with an opportunity to discuss the purpose, the application, and the

CA 9-2 (Time 20–30 minutes)

Purpose—to provide the student with an opportunity to examine ethical issues related to lower-of-cost-

or-market on an individual-product basis. A relatively straightforward case.

CA 9-3 (Time 15–20 minutes)

CA 9-4 (Time 25–30 minutes)

Purpose—to provide the student with an opportunity to discuss the main features of the retail inventory

CA 9-5 (Time 15–25 minutes)

Purpose—the student discusses which costs are inventoriable, the theoretical arguments for the lower–

CA 9-6 (Time 10–15 minutes)

Purpose—to provide the student with a case that allows examination of ethical issues related to the

recording of purchase commitments.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 9-1

(a) The purpose of using the lower-of-cost-or-market method is to reflect the decline of inventory value

below its original cost. A departure from cost is justified on the basis that a loss of utility should be

reported as a charge against the revenues in the period in which it occurs.

(b) The term “market” in the phrase “the lower–of-cost-or-market” generally means the cost to replace

the item by purchase or reproduction. Market is limited, however, to an amount that should not ex–

(c) The lower-of-cost-or-market method may be applied either directly to each inventory item, to a

category, or to the total inventory. The application of the rule to the inventory total, or to the total

(d) Conceptually, the lower-of-cost-or-market method has some deficiencies. First, decreases in the

value of the asset and the charge to expense are recognized in the period in which loss in utility

occurs—not in the period of sale. On the other hand, increases in the value of the asset are

recognized only at the point of sale. This situation is inconsistent and can lead to distortions in the

presentation of income data.

From the standpoint of accounting theory there is little to justify the lower-of-cost-or-market rule.

Although conservative from the balance sheet point of view, it permits the income statement to

show a larger net income in future periods than would be justified if the inventory were carried

CA 9-2

(a) The accountant’s ethical responsibility is to provide fair and complete financial information. In this

case, the loss method distorts the cost of goods sold and hides the decline in market value.

CA 9-3

2. The lower-of-cost-or-market rule is used to report the inventory in the balance sheet at its

future utility value. It also recognizes a decline in the utility of inventory in the income state–

ment in the period in which the decline occurs.

CA 9-4

(a) The retail inventory method can be employed to estimate retail, wholesale, and manufacturing

finished goods inventories.

The valuation of inventory under this method is arrived at by reducing the ending inventory at retail

to an estimate of the lower-of-cost-or-market. The retail value of ending inventory can be computed

CA 9-4 (Continued)

(b) Since the retail method is based on an estimated cost ratio involving total merchandise available

during the period, its validity depends on the underlying assumption that the merchandise in

ending inventory is a representative mixture of all merchandise handled. If this condition does not

exist, the cost ratio may not be appropriate for the merchandise in ending inventory and can result

in significant error.

Material quantities of special sale merchandise handled during the period may also bias the result

of this method because merchandise data included in arriving at the estimated cost ratio may

not be proportionately represented in ending inventory. This condition may be avoided by

accumulating special sale merchandise data in separate accounts.

(c) The advantages of using the retail method as compared to cost methods include the following:

1. Approximate inventory values can be determined without maintaining perpetual inventory records.

(d) The treatments to be accorded net markups and net markdowns must be considered in light of

their effects on the estimated cost ratio. If both net markups and net markdowns are used in

CA 9-5

(a) 1. Olson’s inventoriable cost should include all costs incurred to get the lighting fixtures ready for

2. No, administrative costs are assumed to expire with the passage of time and not to attach to

the product. Furthermore, administrative costs do not relate directly to inventories, but are

2. The net realizable value less a normal profit margin should be used to value the inventories

because market should not be less than net realizable value less a normal profit margin. To

carry the inventories at net realizable value less a normal profit margin provides a means of

measuring residual usefulness of an inventory expenditure.

(c) Olson’s beginning inventories at cost and at retail would be included in the calculation of the cost

ratio.

Net markdowns would be excluded from the calculation of the cost ratio. This procedure reduces

CA 9-6

(a) Accounting standards require that when a contracted price is in excess of market, as it is in this

case (market is $5,000,000 and the contract price is $6,000,000), and it is expected that losses will

(b) If the loss is material, new and continuing shareholders are harmed by nonrecognition of the loss.

Herman should insist on statement preparation in accordance with GAAP. If Hands will not accept

Herman’s position, Herman will have to consider alternative courses of action such as contacting

higher-ups at Prophet and assess the consequences of each course of action.

FINANCIAL REPORTING PROBLEM

(a) Inventories are valued at the lower-of-cost–or-market value. Product-

related inventories are primarily maintained on the first-in, first-out

(b) Inventories are reported on the balance sheet simply as “inventories”

with sub-totals reported for (1) Materials and supplies, (2) Work in

process, and (3) Finished goods.

(c) In its note describing Cost of Products Sold, P&G indicates that cost of

products sold is primarily comprised of direct materials and supplies

(d)

Inventory turnover =

Cost of Goods Sold

=

$40,768

Average Inventory

$7,379 + $6,384

2

Its gross profit percentages for 2011 and 2010 are as follows:

2011

2010

Net sales ………………………

$82,559

$78,938

Cost of goods sold ………..

Gross profit …………………..

Gross profit percentage …

P&G had an increase in its gross profit but a decrease gross profit

percentage. Sales in 2011 showed a 4.6% increase. It appears that

P&G has not been able to manage its costs to increase gross margin

levels on these higher sales.

COMPARATIVE ANALYSIS CASE

(a) Coca-Cola reported inventories of $3,092 million, which represents 3.9%

of total assets. PepsiCo reported inventories of $3,827 million, which

represents 5.3% of its total assets.

(b) Coca-Cola determines the cost of its inventories on the basis of average

cost or first-in, first-out (FIFO) methods; its inventories are valued at

(d) Inventory turnover ratios and days to sell inventory for 2011:

Coca-Cola

PepsiCo

$18,216

= 6.3 times

$31,593

= 8.8 times

$3,092 + $2,650

$3,827 + $3,372

365 ÷ 8.8 = 41 days

FINANCIAL STATEMENT ANALYSIS CASE 1

(a) Although no absolute rules can be stated, preferability for LIFO can

ordinarily be established if (1) selling prices and revenues have been

increasing, whereas costs have lagged, to such a degree that an unre–

alistic earnings picture is presented, and (2) LIFO has been traditional,

(b) It may provide this information (although it is not required to do so)

because it believes that this information tells the reader that both its

income and inventory would be higher if FIFO had been used.

(c) The LIFO liquidation reduces operating costs because low price goods

FINANCIAL STATEMENT ANALYSIS CASE 2

(a) There are probably no finished goods because gold is a highly liquid

commodity, and so it can be sold as soon as processing is complete.

Ore in stockpiles is probably a noncurrent asset because processing

takes more than one year.

(b) Sales are recorded as follows:

(c)

Balance Sheet

Income Statement

Inventory

Overstated

Cost of goods sold

Understated

Retained earnings

Overstated

Net income

Overstated

Accounts payable

Working capital

Overstated

Current ratio

Overstated