EXERCISE 17-7 (Continued)

(c) December 31, 2014

Securities

Cost

Fair Value

Unrealized

Gain (Loss)

Clemson Corp. stock

$20,000

$19,100

($ (900)

Buffaloes Co. stock

( 500)

EXERCISE 17-8 (5–10 minutes)

The unrealized gains and losses resulting from changes in the fair value of

available-for-sale securities are recorded in an unrealized holding gain or

EXERCISE 17-9 (10–15 minutes)

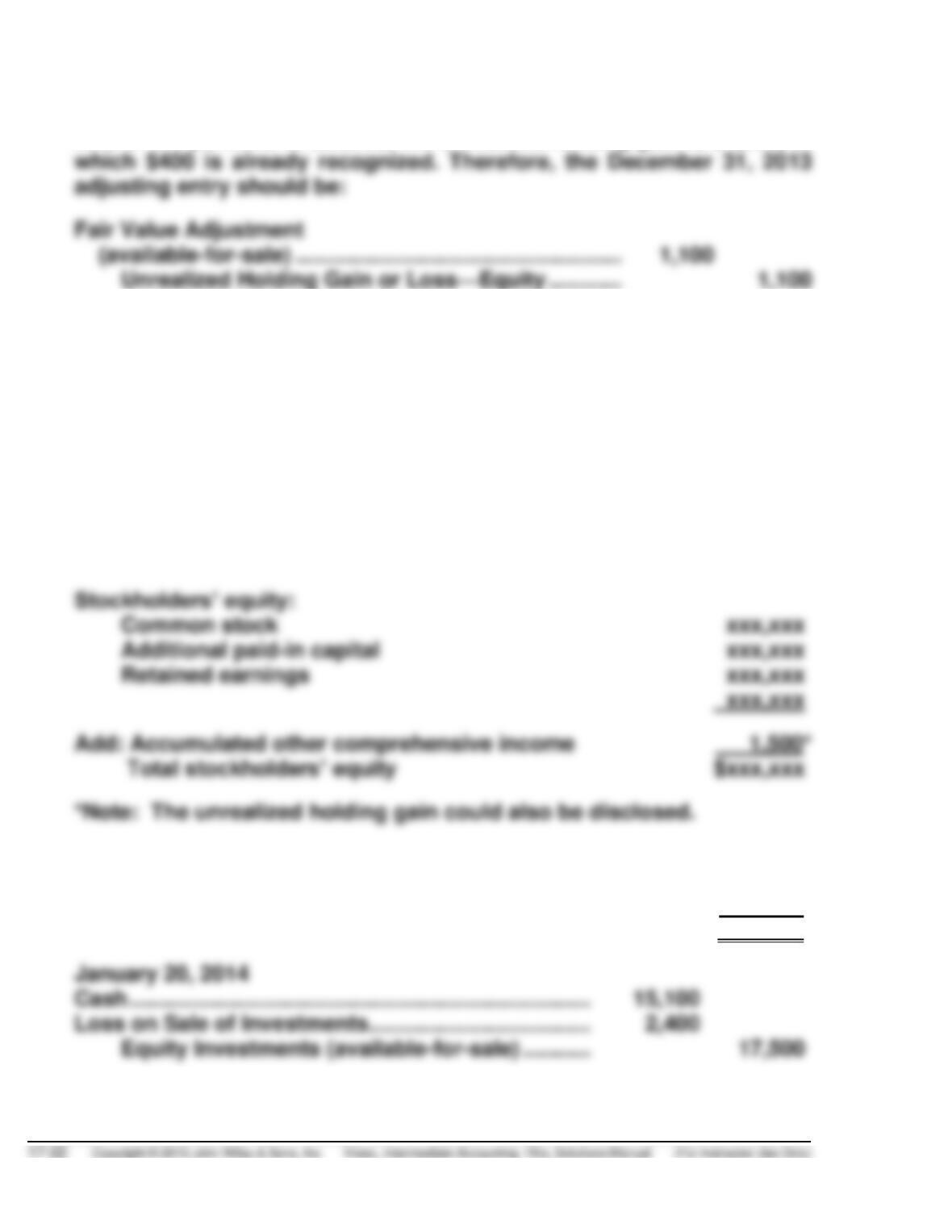

(a) The portfolio should be reported at the fair value of $54,500. Since the

cost of the portfolio is $53,000, the unrealized holding gain is $1,500, of

(b) The unrealized holding gain of $1,500 (including the previous balance of

$400) should be reported as an addition to stockholders’ equity and the

Fair Value Adjustment (available-for-sale) account balance of $1,500

should be added to the cost of the investment account.

STEFFI GRAF, INC.

Balance Sheet

As of December 31, 2013

____________________________________________________________

Current assets:

Equity investments $54,500

(c) Computation of realized gain or loss on sale of stock:

Net proceeds from sale of security A $15,100

Cost of security A 17,500

Loss on sale of stock ($ 2,400)

EXERCISE 17-10 (20–25 minutes)

(a) STEFFI GRAF, INC.

Statement of Comprehensive Income

For the Year Ended December 31, 2013

_____________________________________________________________

Net income $120,000

(b) STEFFI GRAF, INC.

Statement of Comprehensive Income

For the Year Ended December 31, 2014

_____________________________________________________________

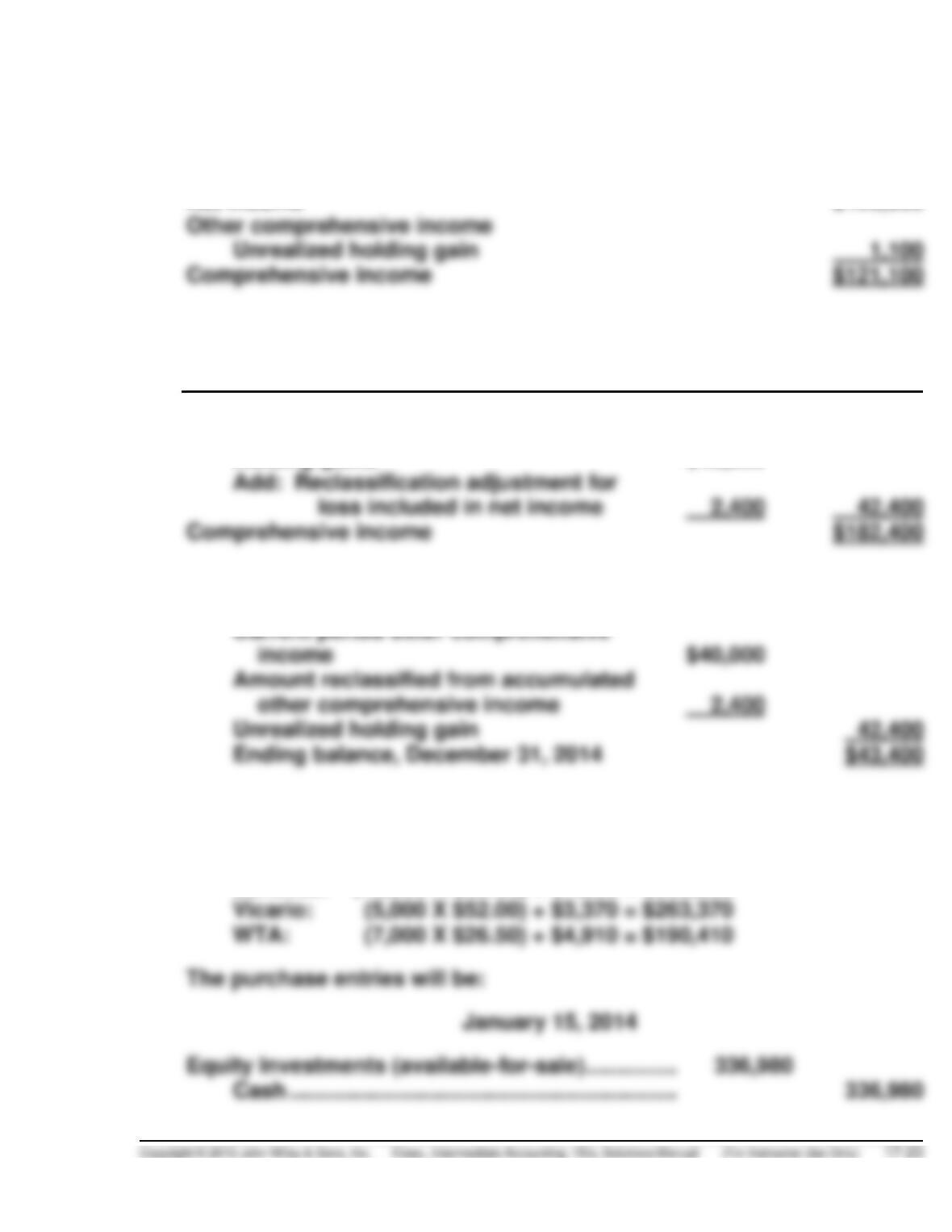

Net income $140,000

Other comprehensive income

Holding gains $40,000

Accumulated other comprehensive income:

Beginning balance, January 1, 2014 $1,100

EXERCISE 17-11 (20–25 minutes)

(a) The total purchase price of these investments is:

Sanchez: (10,000 X $33.50) + $1,980 = $336,980

EXERCISE 17-11 (Continued)

April 1, 2014

Equity Investments (available-for-sale) …………… 263,370

Cash ……………………………………………………… 263,370

September 10, 2014

Equity Investments (available-for-sale) …………… 190,410

Cash ……………………………………………………… 190,410

(b) Gross selling price of 4,000 shares at $35 $140,000

May 20, 2014

Cash ……………………………………………………………… 136,150

(c)

Securities

Cost

Fair Value

Unrealized

Gain (Loss)

Sanchez Co.

$202,188*

$180,000(1)

$(22,188)

Vicario Co.

263,370

275,000(2)

(11,630

WTA Co.

190,410

196,000(3)

5,590

Total portfolio value

*$336,980 X 0.6 = $202,188.

(1)(6,000 X $30) (2)(5,000 X $55) (3)(7,000 X $28)

December 31, 2014

EXERCISE 17-12 (15–20 minutes)

Situation 1: Journal entries by Conchita Cosmetics:

To record purchase of 20,000 shares of Martinez Fashion at a cost of $13

per share:

March 18, 2014

December 31, 2014

Fair Value Adjustment

(available-for-sale) ………………………………………………… 40,000

Unrealized Holding Gain or Loss—Equity …………… 40,000*

January 1, 2014

Equity Investments (Seles Corp.). ……………………………… 81,000

Cash [(30,000 X 30%) X $9] ………………………………… 81,000

EXERCISE 17-12 (Continued)

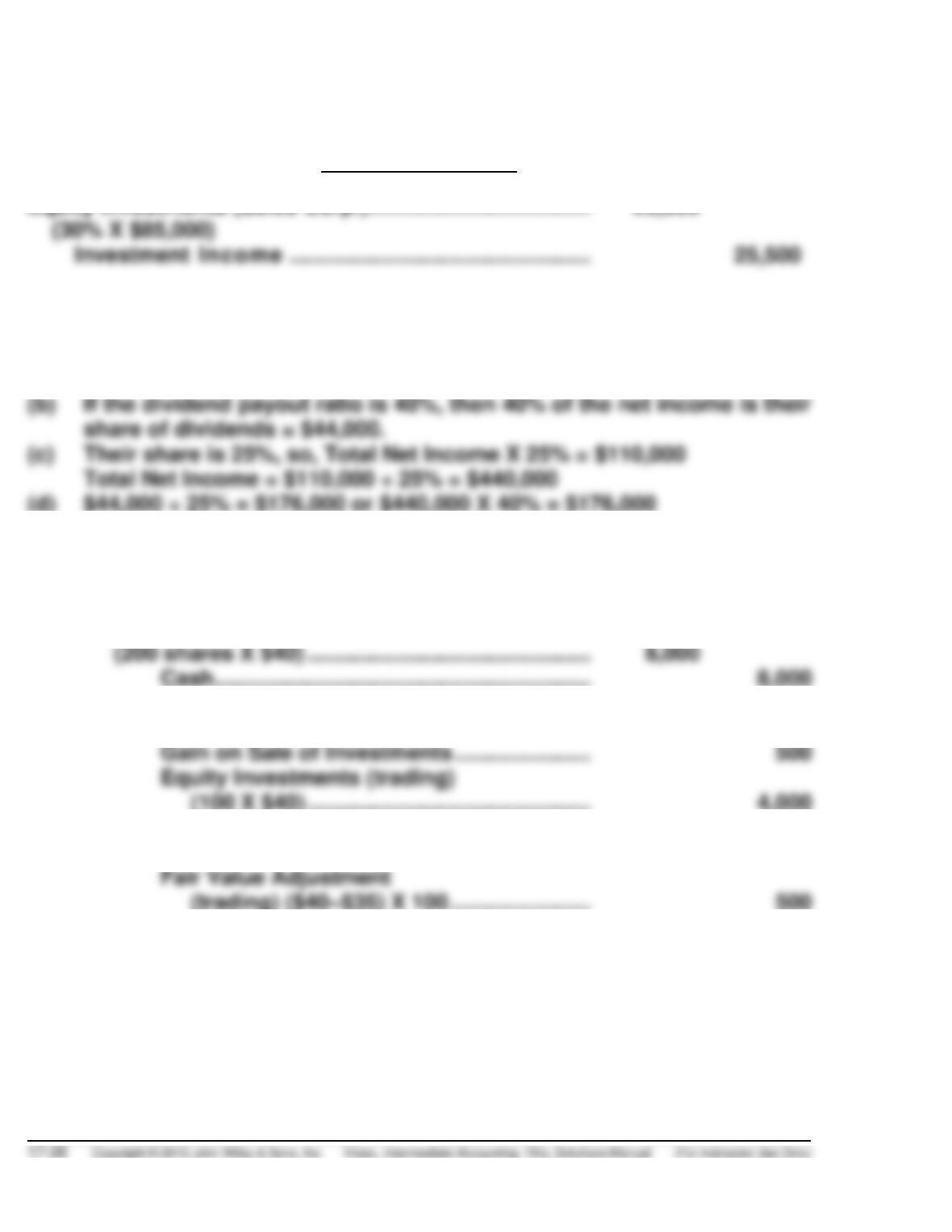

To record Monica’s share (30%) of Seles Corporation’s net income of $85,000:

December 31, 2014

EXERCISE 17-13 (10–15 minutes)

(a) $110,000, the increase to the Investment account.

EXERCISE 17-14 (10–15 minutes)

1. Equity Investments (trading)

2. Cash (100 shares X $45) ………………………………….. 4,500

3. Unrealized Holding Gain or Loss—Income ……….. 500

EXERCISE 17-15 (15–20 minutes)

(a) Unrealized Holding Gain or Loss—Income ………….. 7,900

Fair Value Adjustment (trading) …………………… 7,900

(d)

Securities

Cost

Fair Value

Unrealized

Gain (Loss)

Wallace Corp., Common

$180,000

$175,000

$ (5,000)

Earnhart Corp., Common

53,800

50,400

(3,400)

Previous fair value adjustment—Cr.

EXERCISE 17-16 (15–20 minutes)

(a) December 31, 2013

Equity Investments (available-for-sale) ……….. 1,200,000

Cash ………………………………………………….. 1,200,000

EXERCISE 17-16 (Continued)

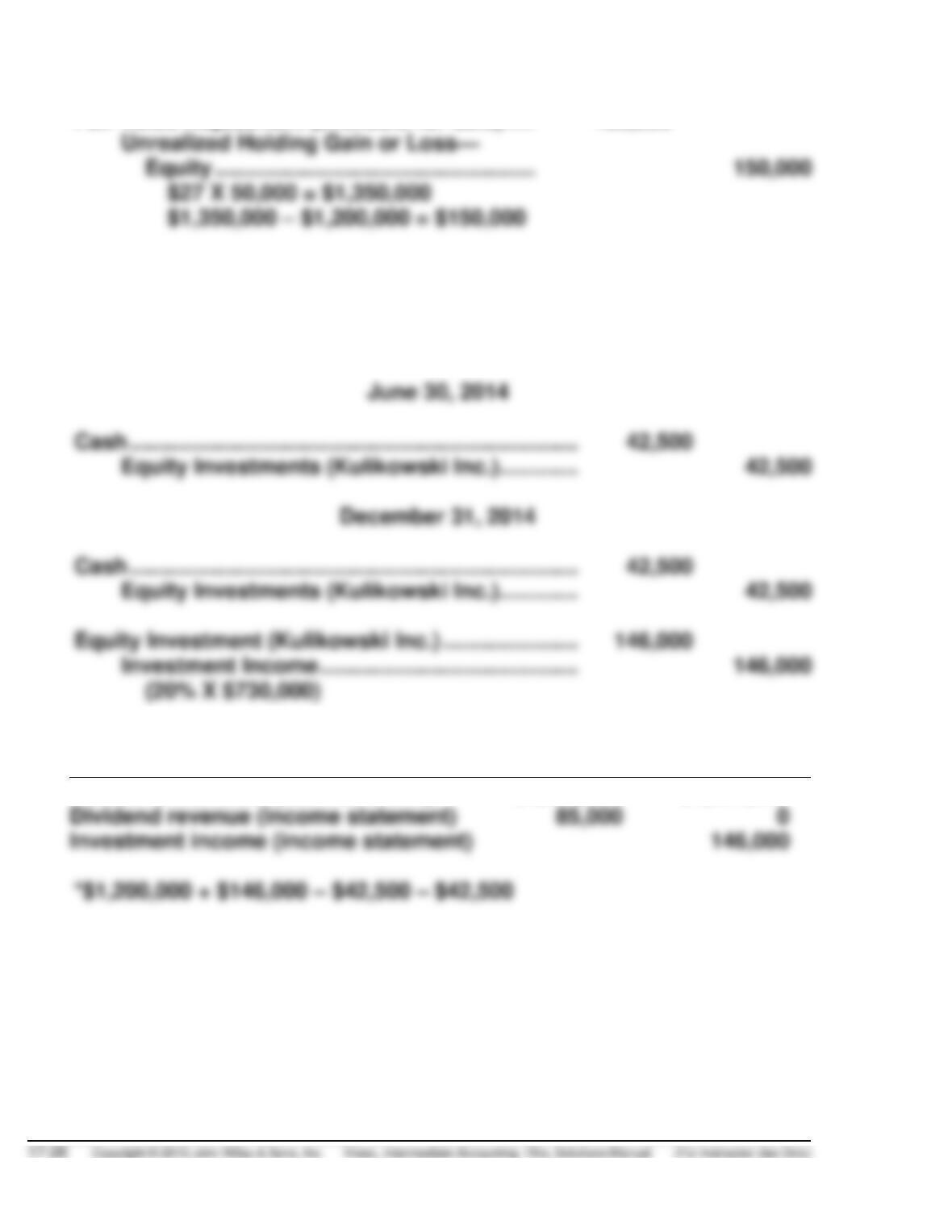

Fair Value Adjustment (available-for-sale) ….. 150,000

(b) December 31, 2013

Equity Investments (Kulikowski) ……………………… 1,200,000

Cash ……………………………………………………….. 1,200,000

(c)

Fair Value

Method

Equity Method

Investment amount (balance sheet)

$1,350,000

*$1,261,000*

Dividend revenue (income statement)

EXERCISE 17-17 (10–15 minutes)

Equity Investments (Edwards Co.) …………………… 180,000

EXERCISE 17-18 (15–20 minutes)

(a) Loss on Impairment ($800,000 – $720,000) ……….. 80,000

Debt Investments (available-for-sale) ………… 80,000

EXERCISE 17-19 (15-20 Minutes)

(a) Unrealized Holding Gain or Loss—Income

($100,000 – $80,000) …………………………………….. 20,000

Equity Investments (Arroyo Company) ……… 20,000

EXERCISE 17-20 (15-20 minutes)

(a) Net income before security gains or losses ………… $905,000

Sale of Investment in Woods Inc. stock

EXERCISE 17-21 (15-20 minutes)

(a) Net income before security gains and losses………. $100,000

Investment in debt securities ($41,000 – $40,000) … 1,000

Investment in Chen Company stock

*EXERCISE 17-22 (15–20 minutes)

(a) Call Option ……………………………………………………… 300

Cash ……………………………………………………….. 300

*EXERCISE 17-23 (20–25 minutes)

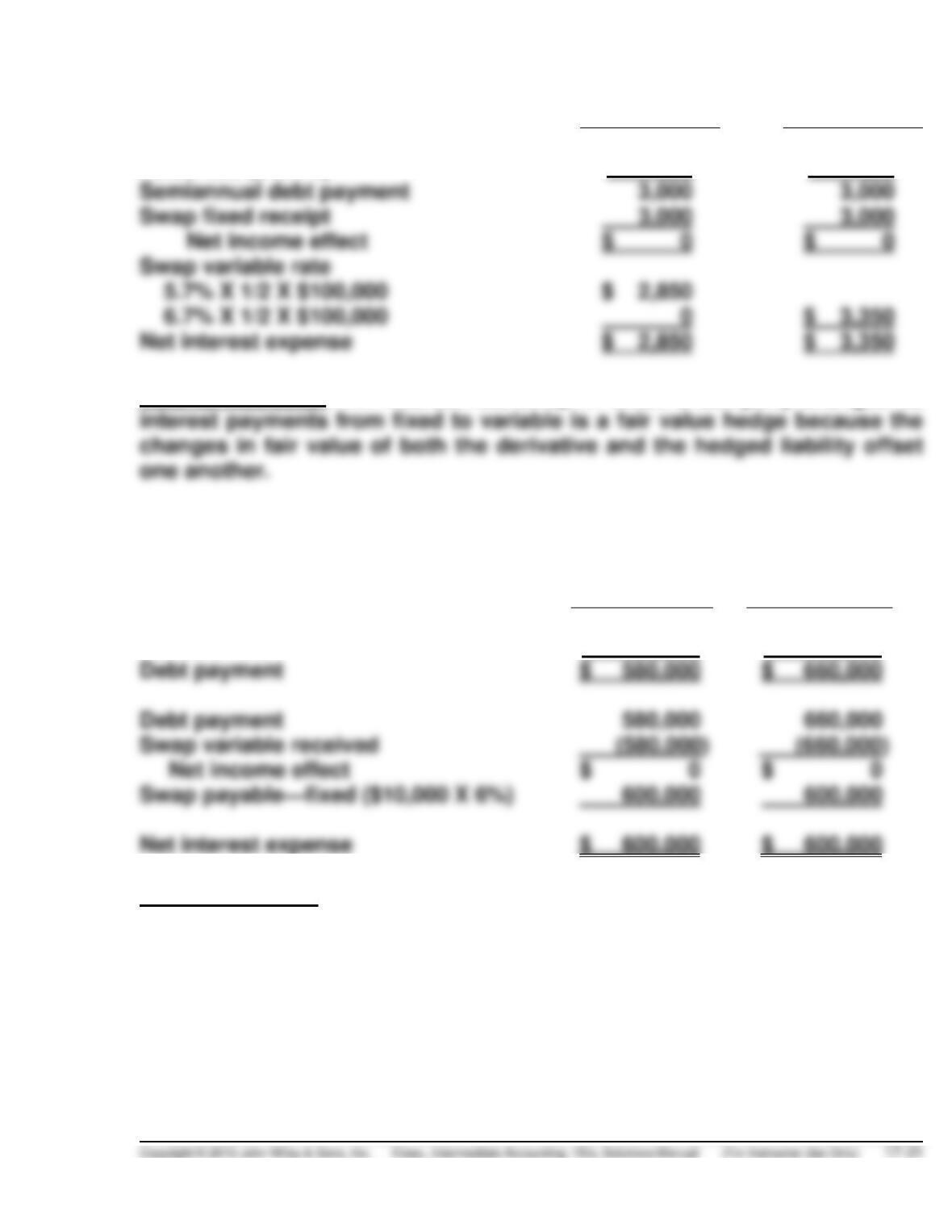

(a)

6/30/14

(b)

12/31/14

Fixed-rate debt

$100,000

$100,000

Fixed rate (6% ÷ 2)

3%

3%

Semiannual debt payment

Swap fixed receipt

3,000

3,000

Net income effect

$ 0

$ 0

Swap variable rate

5.7% X 1/2 X $100,000

$ 2,850

6.7% X 1/2 X $100,000

Net interest expense

$ 2,850

$ 3,350

Note to instructor: An interest rate swap in which a company changes its

*EXERCISE 17-24 (20–25 minutes)

(a)

12/31/14

(b)

12/31/13

Variable-rate debt

$10,000,000

$10,000,000

Variable rate

X5.8%

X6.6%

Debt payment

$ 580,000

Debt payment

580,000

Swap variable received

(580,000)

Net income effect

$ 0

600,000

Net interest expense

$ 600,000

$ 600,000

Note to instructor: An interest swap in which a company changes its interest

payments from variable to fixed is a cash flow hedge because interest costs

are always the same.

*EXERCISE 17-25 (15–20 minutes)

(a) Interest Expense ………………………………………………. 75,000

Cash (7.5% X $1,000,000) ……………………………. 75,000

*EXERCISE 17-26 (20–25 minutes)

(a) August 15, 2013

Call Option ……………………………………………………………. 360

Cash ……………………………………………………………… 360

(b) September 30, 2013

Call Option ……………………………………………………………. 3,200

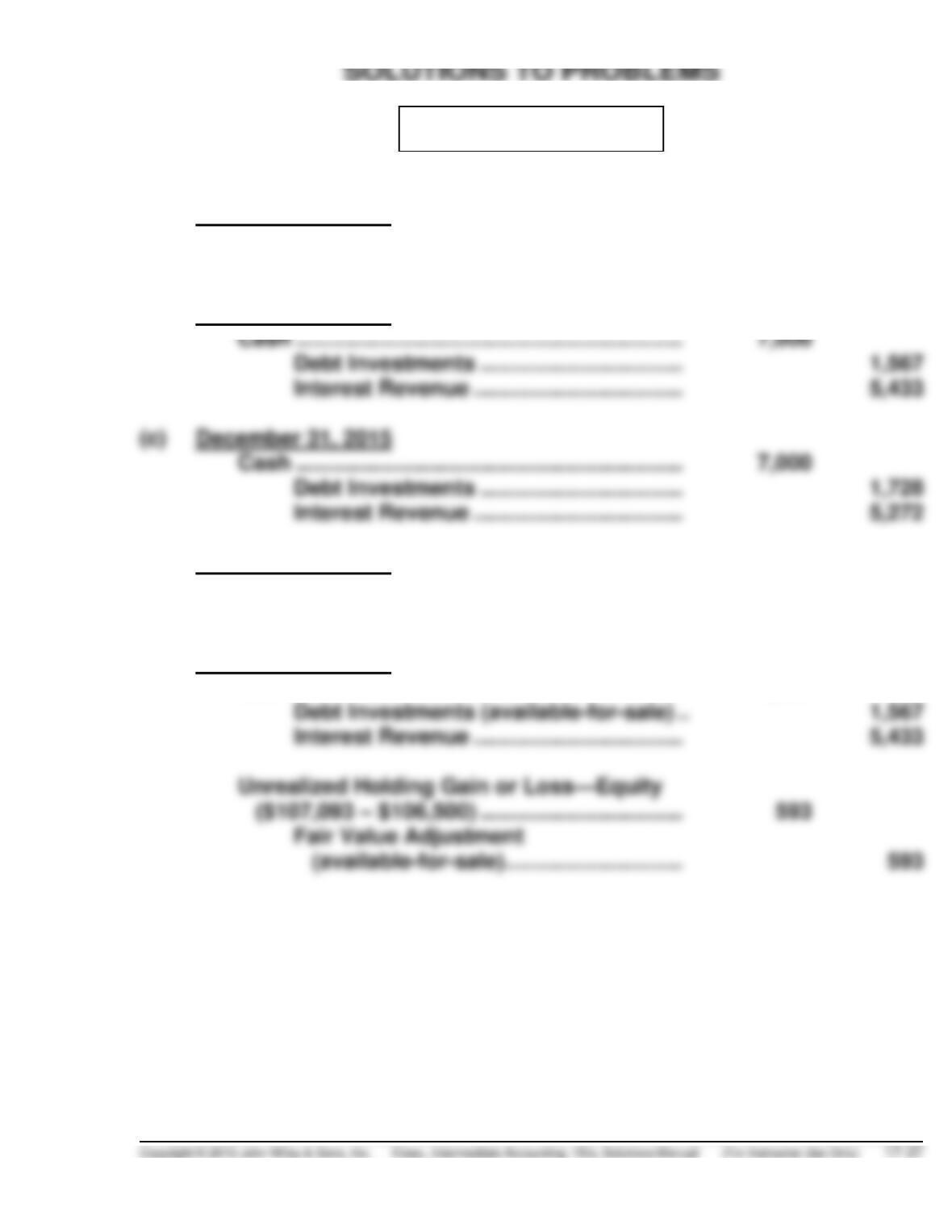

(c) December 31, 2013

Unrealized Holding Gain or Loss—Income ……………… 800

Call Option ($2 X 400) …………………………………….. 800

*EXERCISE 17-26 (Continued)

(d) January 15, 2014

Unrealized Holding Gain or Loss—Income ……………… 35

Call Option ($65 – $30) …………………………..……….. 35

**Computation of Gain: $370 (400 shares X $1) – $30

**Value of Call Option at settlement:

Call Option

360

180

800

115

(a) May 1, 2014

Memorandum entry to indicate entering into the futures contract.

(b) June 30, 2014

Futures Contract …………………………………………….. 4,000

*EXERCISE 17-27 (Continued)

(d) October 5, 2014

Inventory ………………………………………………………. 105,000

Cash ($525 X 200 ounces) ……………………….. 105,000

(e) December 15, 2014

Cash ……………………………………………………………… 250,000

Sales Revenue ………………………………………… 250,000

(f) HART GOLF CO.

Partial Income Statement

For the Quarter Ended December 31, 2014

Sales revenue $250,000

TIME AND PURPOSE OF PROBLEMS

Problem 17-1 (Time 20–30 minutes)

Problem 17-2 (Time 30–40 minutes)

Purpose—The student is required to prepare journal entries and adjusting entries for available-for-sale

debt investments, along with an amortization schedule and a discussion of financial statement

presentation.

Problem 17-3 (Time 25–30 minutes)

Problem 17-4 (Time 25–35 minutes)

Problem 17-5 (Time 25–35 minutes)

Problem 17-6 (Time 25–35 minutes)

Problem 17-7 (Time 25–35 minutes)

Purpose—the student is required to prepare during-the-year and year-end entries for available-for-sale

debt investments and to explain how the entries would differ if the securities were classified as held-to–

maturity.

Problem 17-8 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of the accounting for trading and available-for-

Problem 17-9 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of the proper accounting treatment with respect

Problem 17-10 (Time 20–30 minutes)

Purpose—to provide the student with an opportunity to prepare entries for available-for-sale transactions

and to report the results in a comprehensive income statement and a balance sheet.

Time and Purpose of Problems (Continued)

Problem 17-11 (Time 30–40 minutes)

Problem 17-12 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of the reporting problems associated with

available-for-sale equity investments. Description and amounts that should be reported on a company’s

comparative financial statements are then required.

*Problem 17-13 (Time 20–25 minutes)

Purpose—the student is required to prepare the entries at purchase, throughout the life, and at expiration

for a stand-alone derivative (call option).

*Problem 17-16 (Time 30–40 minutes)

Purpose—the student is provided with an opportunity to prepare the entries for a fair value hedge in the

context of an interest rate swap, including how the effects of the swap will be reported in the financial

statements.

*Problem 17-17 (Time 25–35 minutes)

Purpose—the student is provided with an opportunity to prepare the entries for a cash flow hedge in the

*Problem 17-18 (Time 25–35 minutes)

PROBLEM 17-1

(a) December 31, 2012

Debt Investments …………………………………… 108,660

Cash ……………………………………………… 108,660

(b) December 31, 2013

(d) December 31, 2012

Debt Investments (available-for-sale) ………. 108,660

Cash ……………………………………………… 108,660

(e) December 31, 2013

Cash ……………………………………………………… 7,000

PROBLEM 17-1 (Continued)

(f) December 31, 2015

Cash ……………………………………………………….. 7,000

Debt Investments (available-for-sale)

Amortized

Cost

Fair

Value

Unrealized

Gain (Loss)

Spangler Company, 7% bonds

$103,719

$105,650

$1,931

PROBLEM 17-2

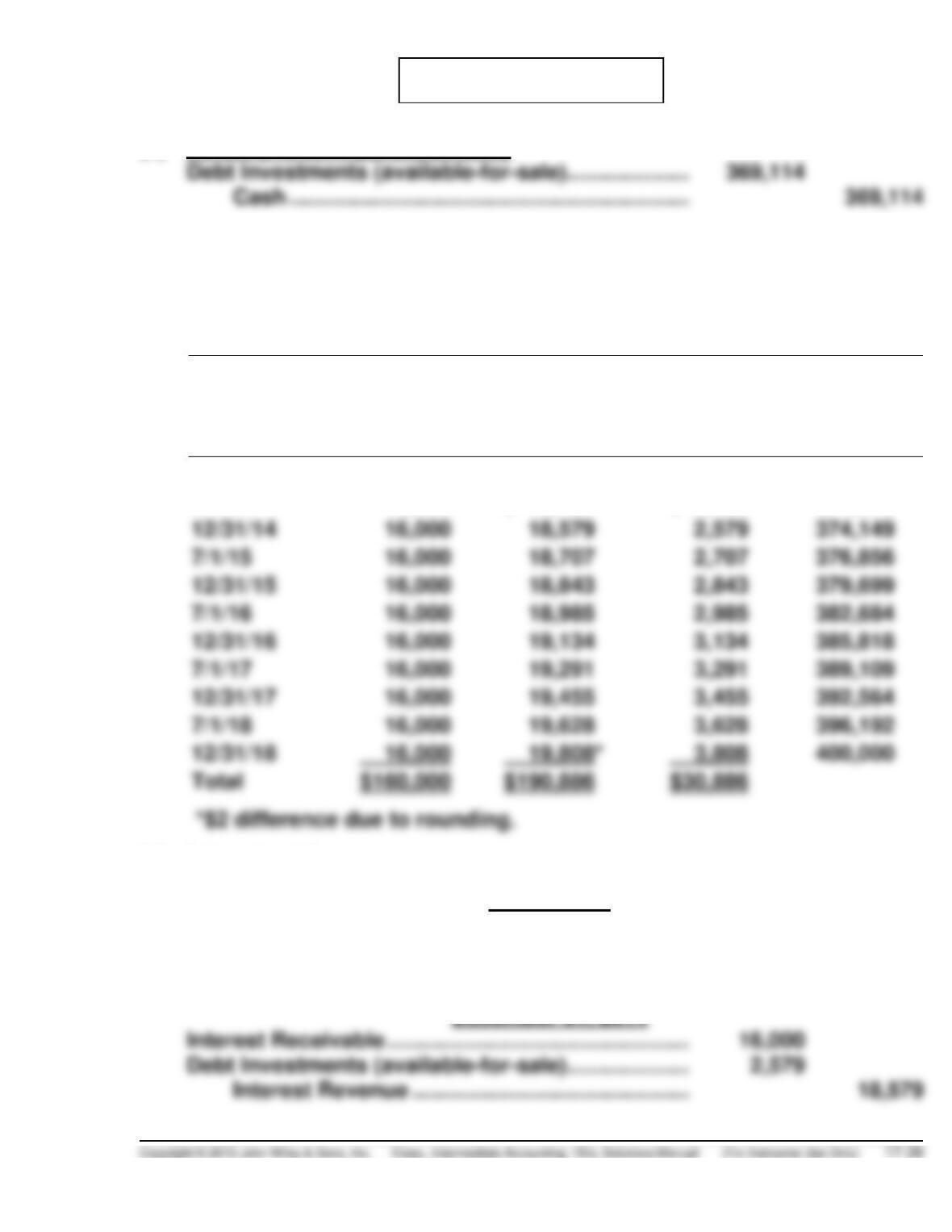

(a) January 1, 2014 purchase entry:

(b) The amortization schedule is as follows:

Schedule of Interest Revenue and Bond Discount

Amortization—Effective-Interest Method

8% Bonds Purchased to Yield 10%

Date

Interest

Receivable

Or

Cash Received

Interest

Revenue

Bond

Discount

Amortization

Carrying

Amount of

Bonds

1/1/14

$369,114

7/1/14

16,000

$ 18,456

$ 2,456

371,570

12/31/14

16,000

18,579

374,149

7/1/15

16,000

18,707

376,856

12/31/15

16,000

18,843

379,699

7/1/16

16,000

18,985

382,684

7/1/17

16,000

19,291

389,109

12/31/17

16,000

19,455

392,564

7/1/18

16,000

19,628

396,192

12/31/18

19,808*

3,808

400,000

$190,886

$30,886

(c) Interest entries:

July 1, 2014

Cash ………………………………………………………………. 16,000

Debt Investments (available-for-sale)……………….. 2,456

Interest Revenue ……………………………………… 18,456

December 31, 2014

PROBLEM 17-2 (Continued)

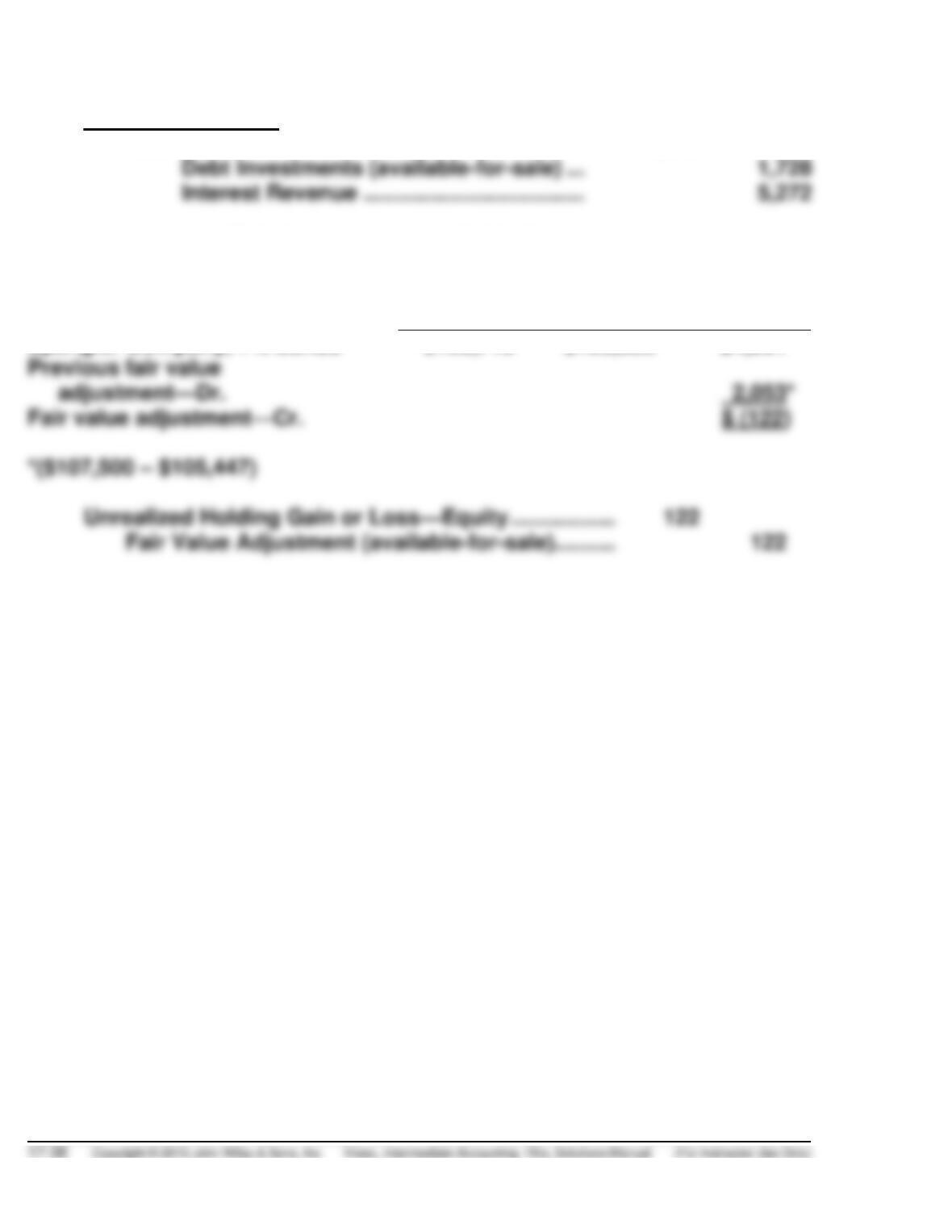

(d) December 31, 2015 adjusting entry:

Securities

Available-for-Sale

Portfolio Cost

Fair Value

Unrealized

Gain (Loss)

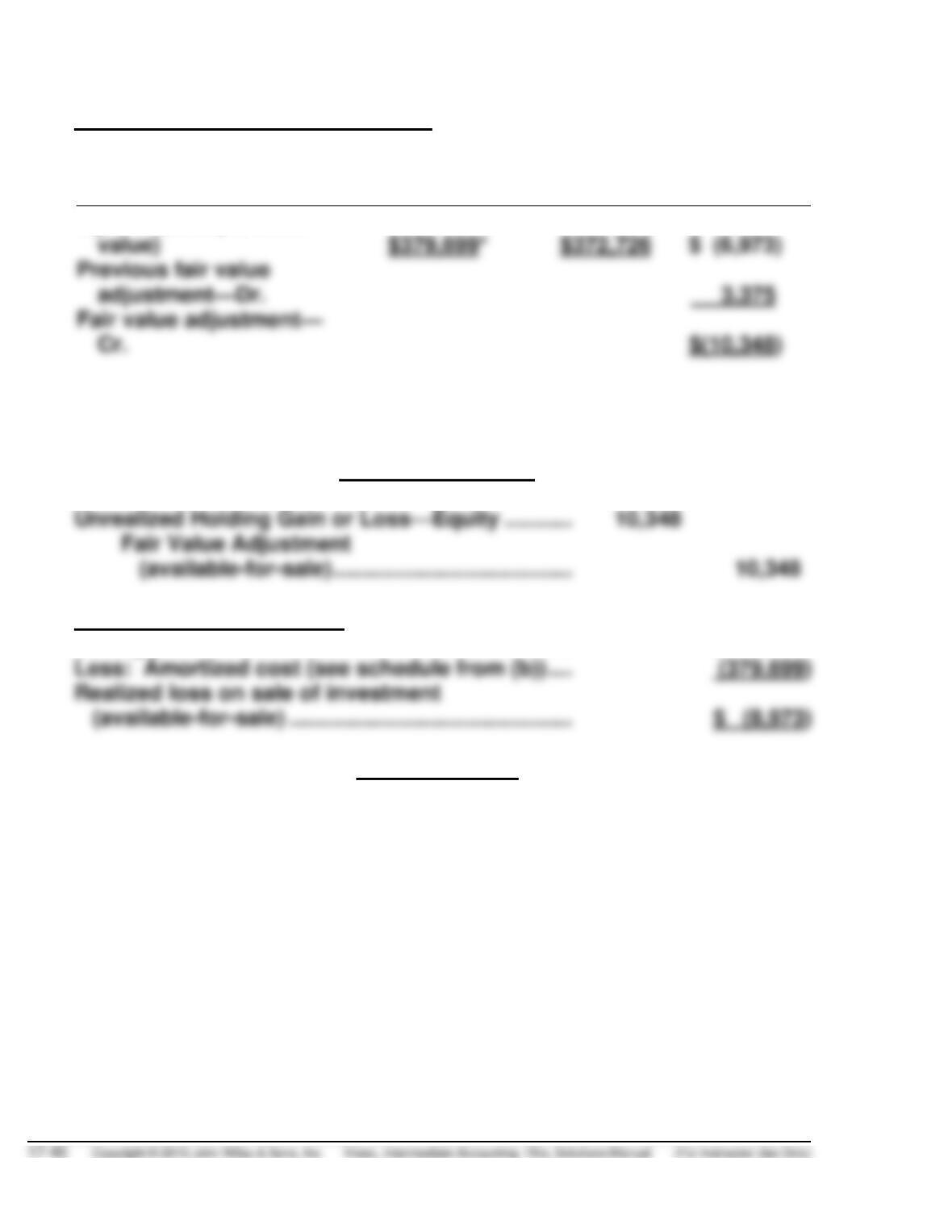

Previous fair value

Aguirre (total portfolio

*

*This is the amortized cost of the bonds on December 31, 2015. See (b)

schedule.

December 31, 2015

(e) January 1, 2016 sale entry:

Selling price of bonds ……………………………………. $370,726

January 1, 2016

Cash ……………………………………………………………… 370,726

Loss on Sale of Investments …………………………... 8,973

Debt Investments (available-for-sale) ……….. 379,699