CHAPTER 4

SOLUTIONS TO B PROBLEMS

PROBLEM 4-1B

MARLIN COMPANY

Income Statement

For the Year Ended December 31, 2014

Sales revenue …………………………………………………………

$53,000,000

Cost of goods sold ………………………………………………….

33,000,000

Gross profit …………………………………………………………….

20,000,000

Selling and administrative expenses ………………………..

8,900,000

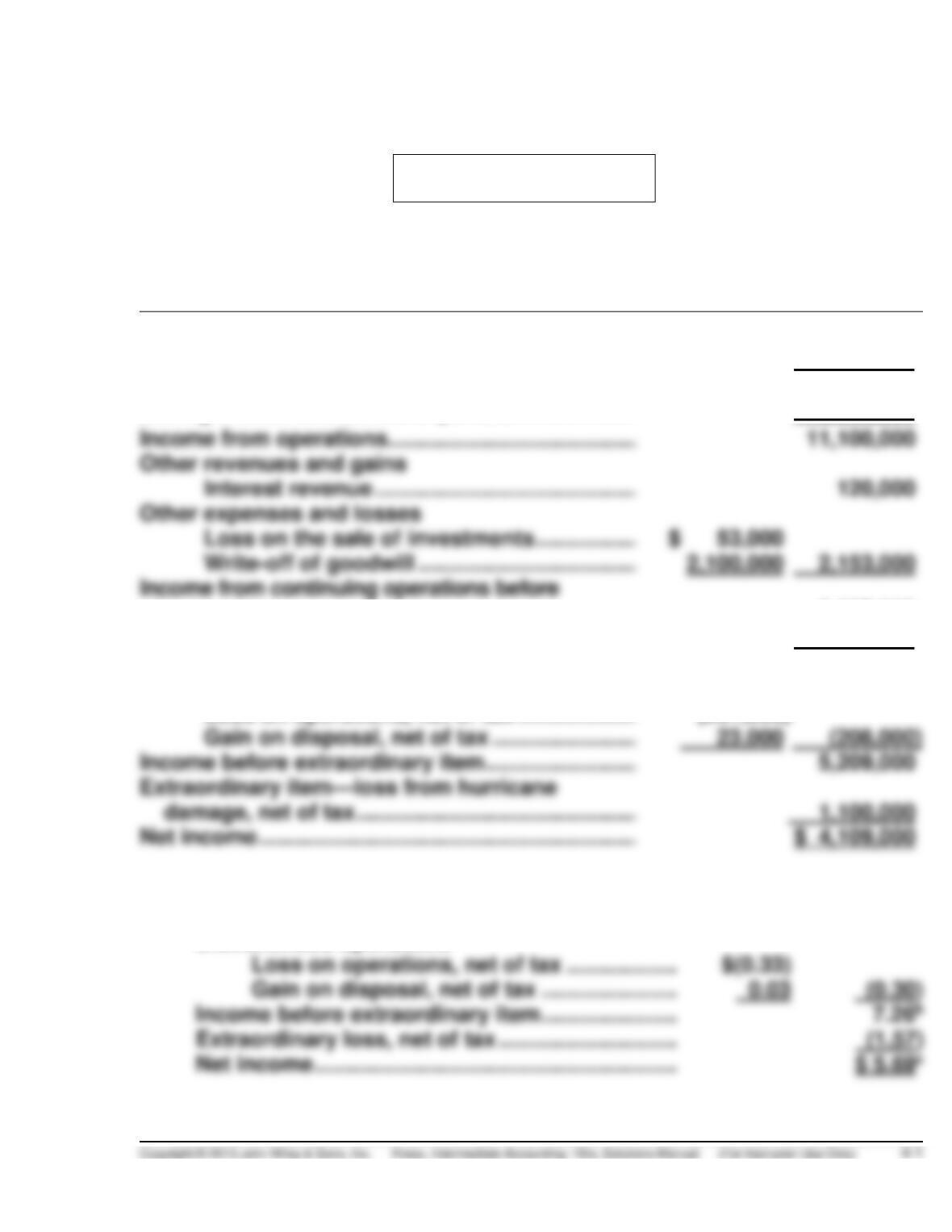

Income from operations…………………………………………..

Other revenues and gains

Interest revenue …………………………………………….

Other expenses and losses

Loss on the sale of investments ……………………..

Write-off of goodwill ………………………………………

2,153,000

income tax …………………………………………………………………..

9,067,000

Income tax ……………………………………………………….…….

3,650,000

Income from continuing operations …………………………

5,417,000

Discontinued operations

Loss on operations, net of tax ………………………..

(231,000)

Gain on disposal, net of tax …………………………...

(208,000)

Income before extraordinary item …………………………….

damage, net of tax ……………………………………………….

Earnings per share:

Income from continuing operations …………………

$ 7.56a

Discontinued operations

Loss on operations, net of tax …………………

Gain on disposal, net of tax …………………….

Income before extraordinary item …………………….

Extraordinary loss, net of tax …………………………..

PROBLEM 4-1B (Continued)

MARLIN COMPANY

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, January 1 …………………………..

Add: Net income …………………………………………..

4,109,000

6,359,000

Less: Dividends

Preferred stock ……………………………………..

$ 125,000

Common stock ……………………………………..

350,000

475,000

Retained earnings, December 31 ……………………..

$ 5,884,000

PROBLEM 4-2B

DUNN CORPORATION

Income Statement

For the Year Ended December 31, 2014

Revenues

Net sales ($2,250,000 – $21,600 – $9,400) …….

Rent revenue …………………………………………….

Expenses

Cost of goods sold* …………………………………..

1,461,000

Selling expenses ……………………………………….

Administrative expenses …………………………...

Loss on sale of land ………………………………….

Total expenses ………………………………….

Income before income tax …………………………………..

359,000

Income tax ………………………………………………..

91,900

Net income …………………………..…………………………….

$ 267,100

Earnings per share ($86,100 ÷ 100,000) ………………..

$2.67

*Cost of goods sold: Can be verified as follows:

Inventory, Jan. 1 ………………………………………………

Less: Purchase discounts ……………………………….

Net purchases………………………………………………….

1,414,000

Inventory available for sale ………………………………

Less: Inventory, Dec. 31 ………………………………….

PROBLEM 4-2B (Continued)

DUNN CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, January 1 …………………………………………

$ 132,500

Less: Cash dividends ……………………………………………………

PROBLEM 4-3B

VANPOP INC.

Income Statement (Partial)

For the Year Ended December 31, 2014

Income from continuing operations

before income tax ……………………………………………….

$596,000(a)

Income tax …………………………………………………..

151,800(b)

Income from continuing operations ……………………….

Discontinued operations

Less: Applicable income tax reduction …………

Income before extraordinary item …………………………..

Extraordinary item:

Major casualty loss ………………………………………

Less: Applicable income tax reduction …………

Per share of common stock:

Income from continuing operations ………………

$1.77

Discontinued operations, net of tax ………………

(0.73)*

Income before extraordinary items ……………….

Extraordinary item, net of tax ……………………….

(0.39)

*Rounded

(a)Computation of income from cont. operations before taxes:

As previously stated …………………………………………

$463,000

Gain on sale of securities …………………………………

40,000

policy ($500,000 – $410,000) ………………………….

As restated………………………………………………………….

PROBLEM 4-3B (Continued)

(b)Computation of income tax:

Income from continuing operations before taxes ……….

$596,000

Nontaxable income (gain on life insurance) ……………….

(90,000)

Taxable income………………………………………………………..

Tax rate …………………………………………………………………..

PROBLEM 4-4B

(a) CASTLE CORPORATION

Income Statement

For the Year Ended June 30, 2014

Sales Revenue

Sales revenue …………………………..…………………………

$2,100,500

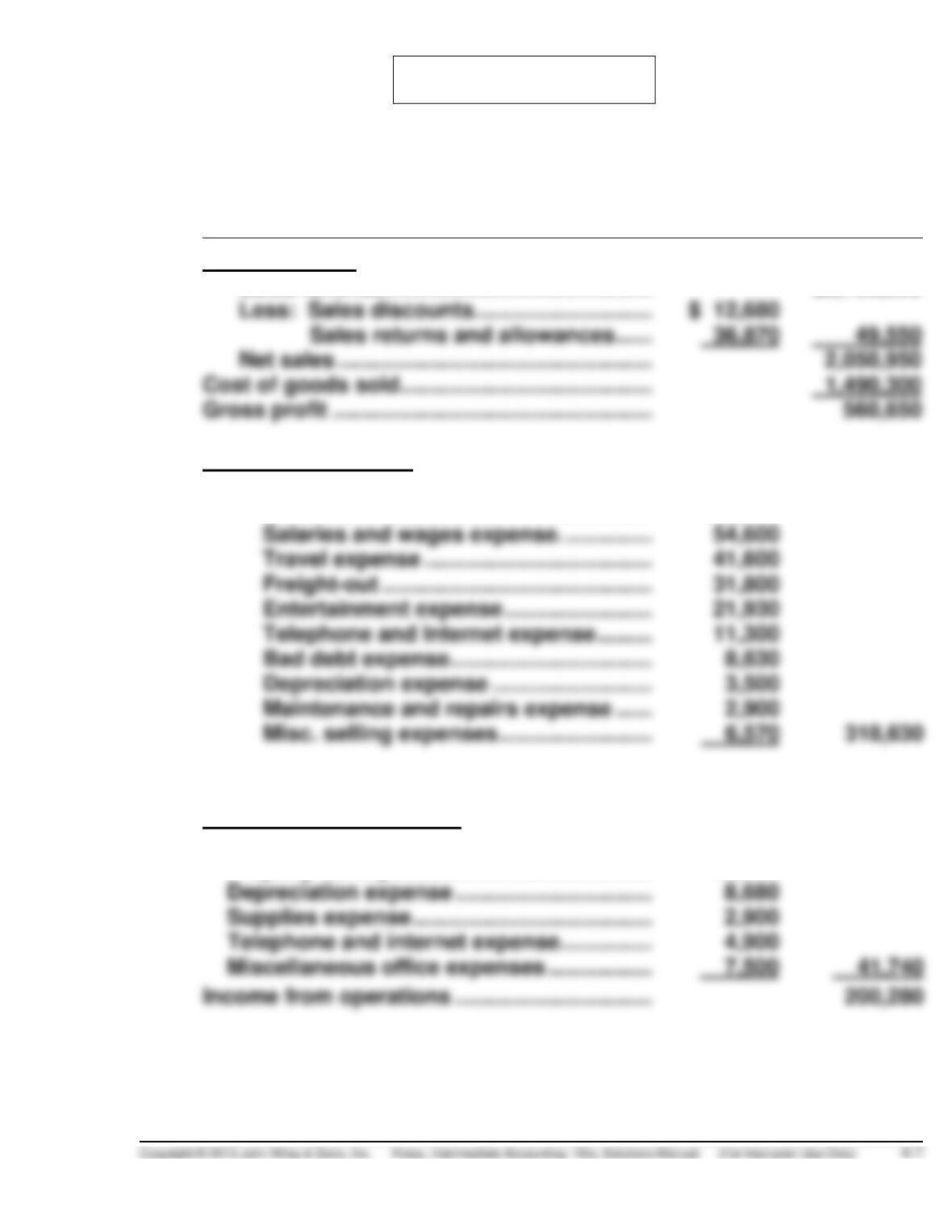

Less: Sales discounts …………………………………………

Sales returns and allowances …………………….

Net sales …………………………………………………………….

Cost of goods sold …………………………..……………………….

Gross profit ……………………………………………………………..

Operating Expenses

Selling expenses

Sales commissions ………………………………………….

135,800

Salaries and wages expense. …………………………...

Travel expense ………………………………………………..

Freight-out ………………………………………………………

Entertainment expense …………………………………….

Telephone and Internet expense ……………………….

Bad debt expense…………………………………………….

Depreciation expense ………………………………………

Maintenance and repairs expense …………………….

Administrative Expenses

Maintenance and repairs expense ……………..

4,860

Property tax expense …………………………………..

12,900

Depreciation expense ……………………………….

8,680

Supplies expense ……………………………………..

2,900

Telephone and internet expense ………………..

Miscellaneous office expenses ………………….

Income from operations ……………………………….

PROBLEM 4-4B (Continued)

Other Revenues and Gains

Other Expenses and Losses

Interest expense ……………………………………….

37,500

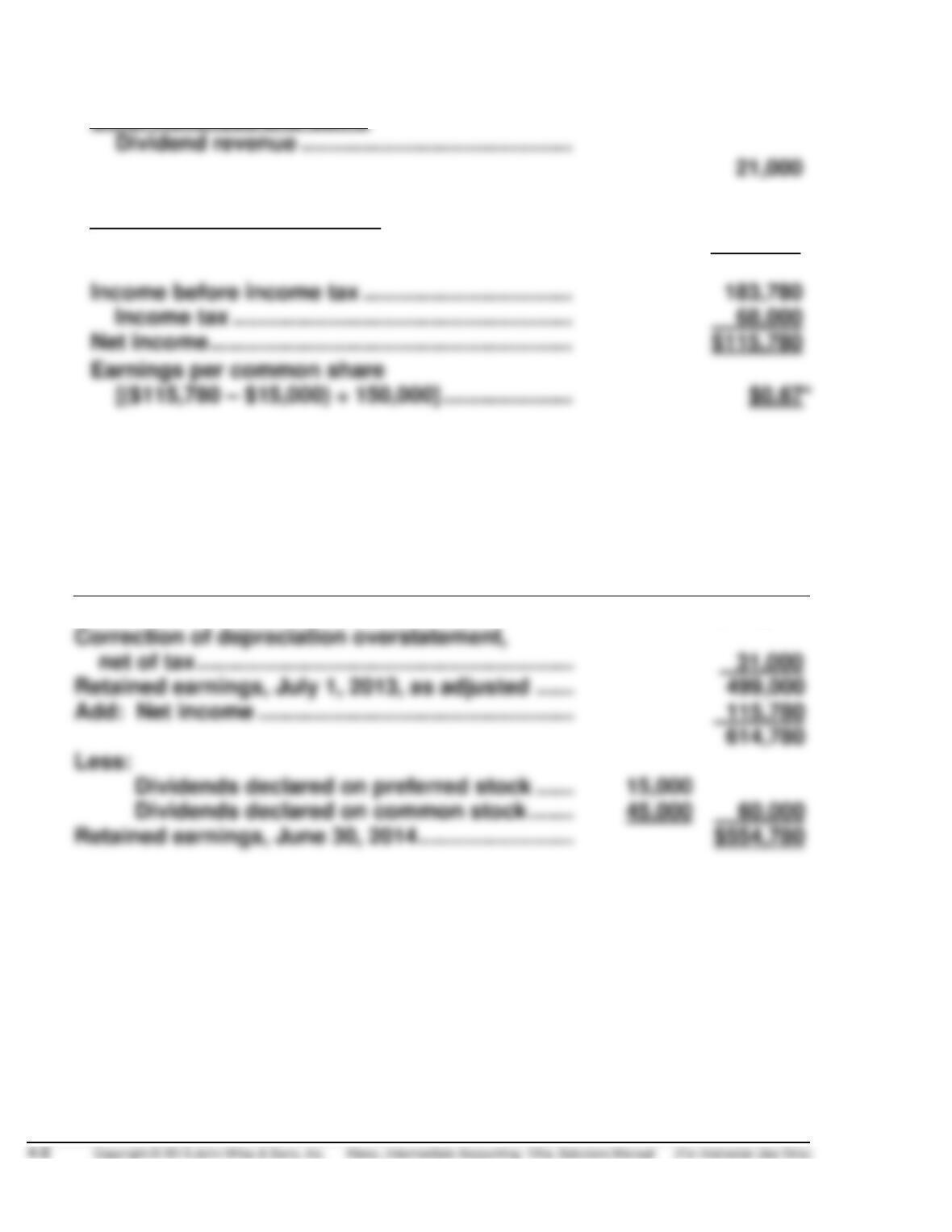

Income before income tax …………………………….

Income tax ……………………………………………….

68,000

*Rounded

CASTLE CORPORATION

Retained Earnings Statement

For the Year Ended June 30, 2014

Retained earnings, July 1, 2013, as reported …………..

$468,000

net of tax …………………………………………………………..

499,000

Dividends declared on common stock …………..

60,000

PROBLEM 4-4B (Continued)

(b) CASTLE CORPORATION

Income Statement

For the Year Ended June 30, 2014

Revenues

Net sales …………………………………………………………….

$2,050,950

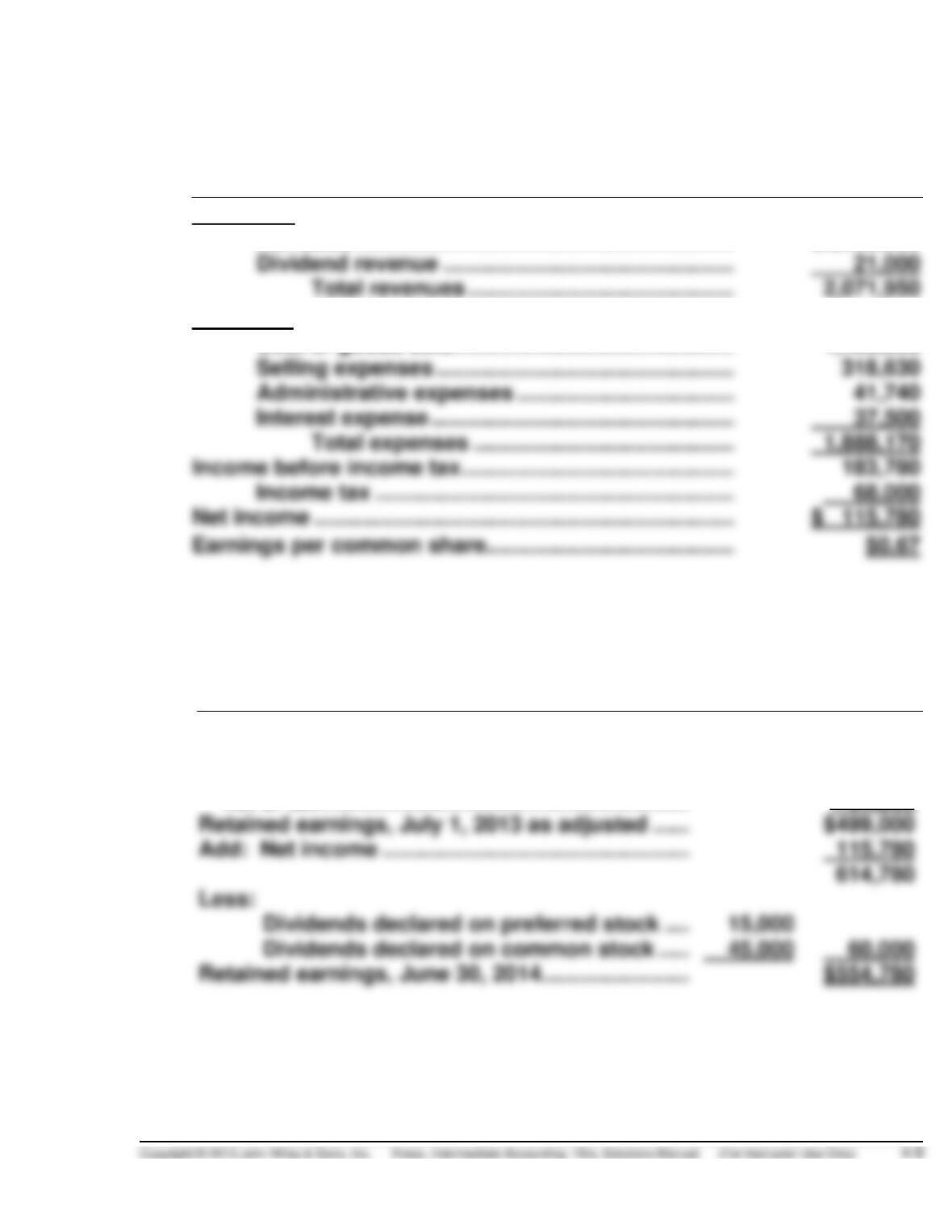

Dividend revenue ………………………………………………..

21,000

Expenses

Cost of goods sold ………………………………………………

1,490,300

Selling expenses …………………………………………………

Administrative expenses ……………………………………..

Interest expense ………………………………………………….

37,500

Total expenses ……………………………………………

Income before income tax ……………………………………………..

Income tax ………………………………………………………….

68,000

CASTLE CORPORATION

Retained Earnings Statement

For the Year Ended June 30, 2014

Retained earnings, July 1, 2013, as reported …………….

$468,000

Correction of depreciation overstatement,

net of tax ……………………………………………………….……

31,000

Retained earnings, July 1, 2013 as adjusted …………….

Add: Net income ……………………………………………………

Dividends declared on preferred stock …………..

Dividends declared on common stock ……………

PROBLEM 4-5B

1. The usual but infrequently occurring charge of $11,000,000 should be

disclosed separately, assuming it is material. This charge is shown

above income before extraordinary items and would not be reported net

2. The extraordinary item of $8,500,000 should be reported net of tax in a

separate section for extraordinary items. An adjustment should be made

to income taxes to report this amount at $40,200,000. The $3,200,000 tax

3. The adjustment required for correction of an error is inappropriately

labeled and also should not be reported in the retained earnings

statement. Changes in estimate should be handled in current and future

4. Earnings per share should be reported on the face of the income

statement and not in the notes to the financial statements. Because

PROBLEM 4-6B

(a) COOPER CORP.

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, January 1, as reported …………………………………

$616,050

Correction of error from prior period (net of tax) ………………………..

49,700

Retained earnings, January 1, as adjusted …………………………………

Add: Net income …………………………………………………………………….

(b) 1. Gain on sale of investments—body of income statement. This gain

should not be shown net of tax on the income statement.

2. Refund on litigation with government—body of income statement,

possibly unusual item. This refund should not be shown net of tax

PROBLEM 4-7B

RAFTER CORP.

Income Statement (Partial)

For the Year Ended December 31, 2014

Income from continuing operations

before income tax ………………………………

$2,686,000*

Income tax ……………………………………

805,800**

Income from continuing operations ………..

1,880,200

Discontinued operations

discontinued subsidiary …………….

reduction ……………………..

$ 273,000

Loss from disposal of subsidiary ……..

reduction ……………………..

Income before extraordinary item …………..

Extraordinary item:

Loss on condemnation ………………….

Net income ……………………………………………

Per share of common stock:

Income from continuing operations …………………………….

$4.70

Discontinued operations, net of tax …………………………....

Income before extraordinary item …………………………..…..

Extraordinary item, net of tax ……………………………………..

Net income ($1,529,200 ÷ 400,000) ………………………………

PROBLEM 4-7B (Continued)

*Computation of income from continuing operations

before income tax:

Restated

**Computation of income tax expense:

$2,686,000 X 0.30 = $805,800