FINANCIAL REPORTING PROBLEM

(a) 1. Per P&G’s 2011 income statement:

Income taxes …………………………………………… $ 3,392 million

3. Per P&G’s 2011 statement of cash flows:

In cash flows provided by operating

(b) P&G’s effective tax rates:

2009: (25.9%), 2010: (27.3%), 2011: (22.3%)

FINANCIAL REPORTING PROBLEM (Continued)

Deferred tax assets

Pension and postretirement benefits ……………………………… $ 1,406

Stock-based compensation …………………………………………… 1,284

Loss and other carryforwards………………………………………… 874

Deferred tax liabilities

Goodwill and other intangible assets ……………………………… $12,206

COMPARATIVE ANALYSIS CASE

(a) 2011 provision for income taxes (In Millions):

(b) 2011 income tax payments (In Millions):

Coca-Cola ……………………………………………………………………. $1,612

PepsiCo (Note 14) ………………………………………………………… $2,218

(c) The 2011 U.S. Federal statutory tax rate was 35.0%.

(d)

(In Millions)

Coca-Cola

PepsiCo

1.

Gross deferred tax assets

$5,128

$4,930

Gross deferred tax liabilities

8,512

7,816

(e) Net operating loss carryforwards at year-end 2011:

FINANCIAL STATEMENT ANALYSIS CASE

(a) Of the total provision for income taxes (reported in the income

(b) Future taxable amounts increase taxable income relative to pretax

financial income in the future due to temporary differences existing at

(c) The carryback and carryforward provisions will affect the amounts to

be reported for the resulting deferred tax asset and deferred tax liability.

In computing deferred tax account balances to be reported at a balance

sheet date, the appropriate enacted tax rate is applied to future taxable

For future taxable amounts:

1. If taxable income is expected in the year that a future taxable

FINANCIAL STATEMENT ANALYSIS CASE (Continued)

2. If an NOL is expected in the year that a future taxable amount is

For future deductible amounts:

1. If taxable income is expected in the year that a future deductible

amount is scheduled, use the enacted rate for that future year to

calculate the related deferred tax asset.

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

Taxable income for 2014:

Pretax financial income …………………………………………………. $500,000

Income taxes payable for 2014:

Taxable income …………………………………………………………….. $ 50,000

De John has future taxable amounts arising from temporary differences as

follows:

Future Years

2015

2016

2017

2018

Total

Enacted tax rate

Deferred tax liability (asset)

$ 44,800

Future taxable (deductible)

The $179,200 is a deferred tax liability because the temporary difference is

from future taxable amounts. The deferred tax liability needed is $179,200.

Journal entry:

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Analysis

The temporary difference in this case is due to the installment receivable.

Because the installment receivable would likely be classified as current

(despite collection over four subsequent years; see Chapter 18), the $179,200

deferred tax liability would also be classified as current. Income taxes

payable would also be classified as current.

The income tax expense portion of the income statement would look as

follows:

Principles

We can use the conceptual framework to determine that deferred taxes

PROFESSIONAL RESEARCH

(a) According to FASB ASC 740-10–30-18 (Income Taxes, Overall, Initial

(b) According to FASB ASC 740-10–30-18 (Income Taxes, Overall, Initial

Measurement):

The following four possible sources of taxable income may be

available under the tax law to realize a tax benefit for deductible

temporary differences and carryforwards:

a. Future reversals of existing taxable temporary differences

d. Tax-planning strategies (see paragraph 740-10–30-19) that would, if

necessary, be implemented to, for example:

(1) Accelerate taxable amounts to utilize expiring carryforwards

Evidence available about each of those possible sources of taxable

income will vary for different tax jurisdictions and, possibly, from year

PROFESSIONAL RESEARCH (Continued)

(c) According to FASB ASC 740–10-30 (Income Taxes, Overall, Initial

Measurement):

30–19 In some circumstances, there are actions (including elections

for tax purposes) that:

a. Are prudent and feasible.

30–22 Examples (not prerequisites) of positive evidence that might

support a conclusion that a valuation allowance is not needed

when there is negative evidence include, but are not limited to,

the following:

a. Existing contracts or firm sales backlog that will produce

PROFESSIONAL RESEARCH (Continued)

c. A strong earnings history exclusive of the loss that created

30–23 An entity shall use judgment in considering the relative impact

of negative and positive evidence. The weight given to the poten-

tial effect of negative and positive evidence shall be commensu–

30–24 Future realization of a tax benefit sometimes will be expected for

a portion but not all of a deferred tax asset, and the dividing line

between the two portions may be unclear. In those circum-

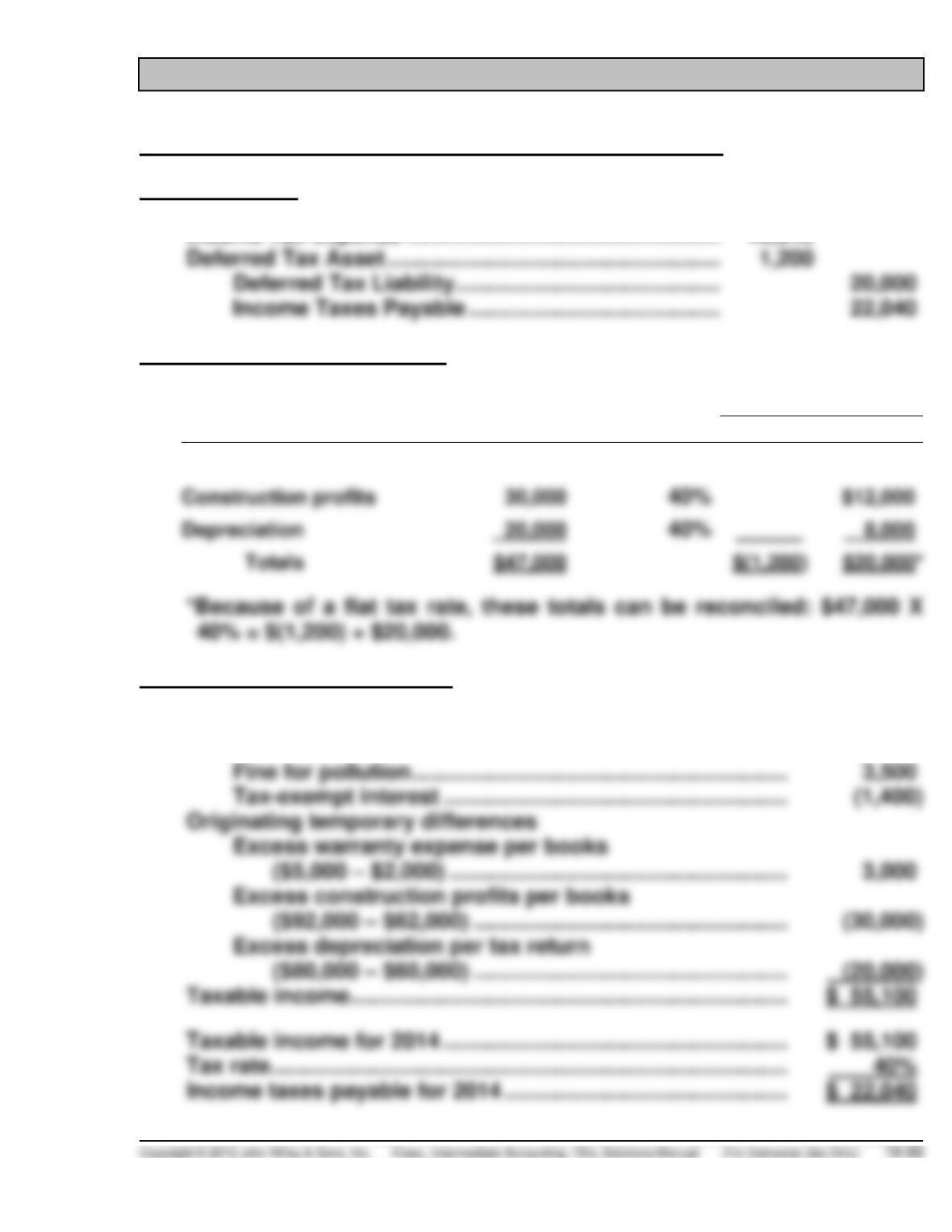

PROFESSIONAL SIMULATION

Note: This assignment is available on the Kieso website.

Journal Entries

Income Tax Expense …………………………………………… 40,840

Calculation of Deferred Taxes

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Warranty costs

$ (3,000)

40%

$(1,200)

40%

40%

Calculation of Taxable Income

Pretax financial income …………………………………………………. $100,000

Permanent differences

PROFESSIONAL SIMULATION (Continued)

Deferred tax liability at the end of 2014 …………………………... $ 20,000

Financial Statements

Income before income taxes …………………………….. $100,000

Income tax expense

IFRS CONCEPTS AND APPLICATION

IFRS19-1

The accounting for income taxes in IFRS is covered in IAS 12 “Income

Taxes”.

IFRS19-2

Both IFRS and GAAP use the asset and liability approach for recording

• Under IFRS, an affirmative judgment approach is used by which a

deferred tax asset is recognized up to the amount that is probable to

be realized. GAAP uses an impairment approach. In this situation, the

• The tax effects related to certain items are reported in equity under

IFRS. That is not the case under GAAP, which charges or credits the

tax effects to income.

• GAAP requires companies to assess the likelihood of uncertain tax

IFRS19-3

The IASB and the FASB have been working to address some of the

differences in the accounting for income taxes. Some of the issues under

discussion are the term “probable” under IFRS for recognition of a

IFRS19-4

Deferred tax accounts are reported on the statement of financial position

as assets and liabilities. They should be classified in a net non-current

amount.

IFRS19-5

Deferred tax assets and deferred tax liabilities are separately recognized

IFRS19-6

Income Tax Expense ………………………………………………. 60,000

Deferred Tax Asset ………………………………………….. 60,000

IFRS19-7

Income Tax Refund Receivable ($350,000 X .40) .. 140,000

Benefit Due to Loss Carryback ………………….. 140,000

IFRS19-9

Non-current liabilities

Deferred tax liability ($69,000 – $24,000) …….. $45,000

IFRS19–10

Date

Cumulative Future Taxable

(Deductible) Amounts

Tax Rate

Deferred Tax

(Asset)

Liability

12/31/15

$(500,000)

40%

$(200,000)

IFRS19-11 (Continued)

Deferred tax asset at the end of 2015 …………………………….. $200,000

(b) The journal entry at the end of 2015:

Income Tax Expense …………………………..………….. 30,000

Deferred Tax Asset …………………………………… 30,000

Note to instructor: Although not requested by the instructions, the pretax

financial income can be computed by completing the following

reconciliation:

IFRS19–12

(a) According to IAS 12, paragraph 34, “A deferred tax asset shall be

IFRS19-12 (Continued)

(b) This question relates to the information found in paragraph 36, which

states, “An entity considers the following criteria in assessing the

probability that taxable profit will be available against which the

unused tax losses or unused tax credits can be utilised:

(1) whether the entity has sufficient taxable temporary differences

relating to the same taxation authority and the same taxable entity,

which will result in taxable amounts against which the unused tax

(c) Paragraph 30 discusses tax planning opportunities: “Tax planning

opportunities are actions that the entity would take in order to create

or increase taxable income in a particular period before the expiry of a

tax loss or tax credit carryforward. For example, in some jurisdictions,

taxable profit may be created or increased by:

(1) electing to have interest income taxed on either a received or

receivable basis;

IFRS19-13

(a) 1. Per M&S’s 2012 consolidated income statement:

Total income tax expense …………………………. £168.4 million

2. Per M&S’s 31 March, 2012 statement of financial position:

(b) M&S’s effective tax rates:

2012: (25.6%), 2011: (23.3%)

(c) Income tax expense:

Deferred Tax Assets

Other short-term temporary differences ………………… £ 6.5

Deferred Tax Liabilities

Non-current assets temporary differences …………….. £ 58.2