E10-15B (Continued)

(c)

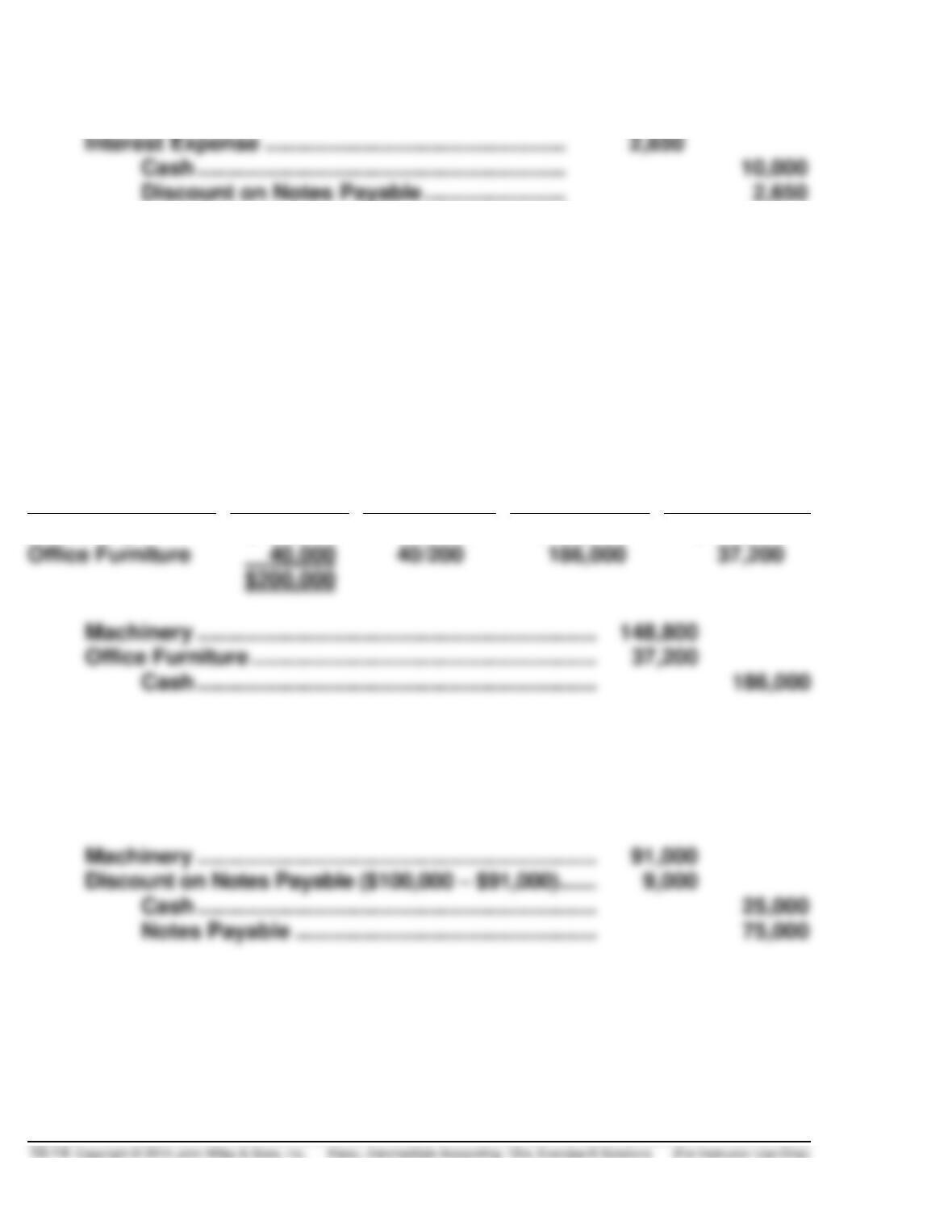

Notes Payable ……………………………………………………….

10,000

Interest Expense …………………………………………………….

Discount on Notes Payable …………………………..

E10-16B (25–35 minutes)

OGDEN INDUSTRIES

Acquisition of Assets 1 and 2

Use appraised values to break-out the lump-sum purchase

Description

Appraisal

Percentage

Lump-Sum

Value on

Books

Machinery

$160,000

160/200

$186,000

$148,800

Office Furniture

40,000

37,200

Office Furniture ………………………………………………………

Acquisition of Asset 3

Use the cash price as a basis for recording the asset with a discount recorded on

the note.

Machinery ………………………………………………………………

Cash ………………………………………………………………

Notes Payable ………………………………………………..

E10-16B (Continued)

Acquisition of Asset 4

Since the exchange lacks commercial substance, a gain will be recognized in

the proportion of cash received ($20,000/$96,000) times the $6,000 gain (FMV

of $96,000 minus BV of $90,000). The gain recognized will then be $1,250 with

In this case, the Machinery should be placed on the books at the fair market

value of the stock. The difference between the stock’s par value and its fair

value should be credited to Paid-in Capital in Excess of Par.

Schedule of Weighted-Average Accumulated Expenditures

Date

Amount

Current Year

Capitalization

Period

Weighted-Average

Accumulated

Expenditures

March 1

$ 120,000

6/12

$ 60,000

E10-16B (Continued)

Avoidable Interest

Weighted-Average

Accumulated Expenditures

Interest Rate

Avoidable Interest

$285,000

X

10%

=

$28,500

Land ………………………………………………………………………

Cash ……………………………………………………….

Interest Expense …………………………………………….

E10-17B (10–15 minutes)

Phillips Corporation

Machine ($680 + $170) ……………………………………………..

850

Accumulated Depreciation ………………………………………

280

Loss on Disposal of Machine …………………………..………

130

Machine (old) ………………………………………………….

Cash ………………………………………………………………

Computation of loss:

Book value of old machine ($580 – $280)

Fair value of old machine

E10-17B (15–20 minutes)

Luzinski Business Machine Company

Cash ……………………………………………………………………….

Inventory (old) ……………………………………………………….

Cost of Goods Sold …………………………………………………

Sales ………………………………………………………………

Inventory (new) ……………………………………………….

E10-18B (20–25 minutes)

(a)

Exchange has commercial substance:

Depreciation Expense …………………………..…………………

1,700

Accumulated Depreciation—Press …………………..

1,700

($35,000 – $1,000 = $34,000;

$34,000 ÷ 10 = $3,400;

$3,400 X 6/12 = $1,700)

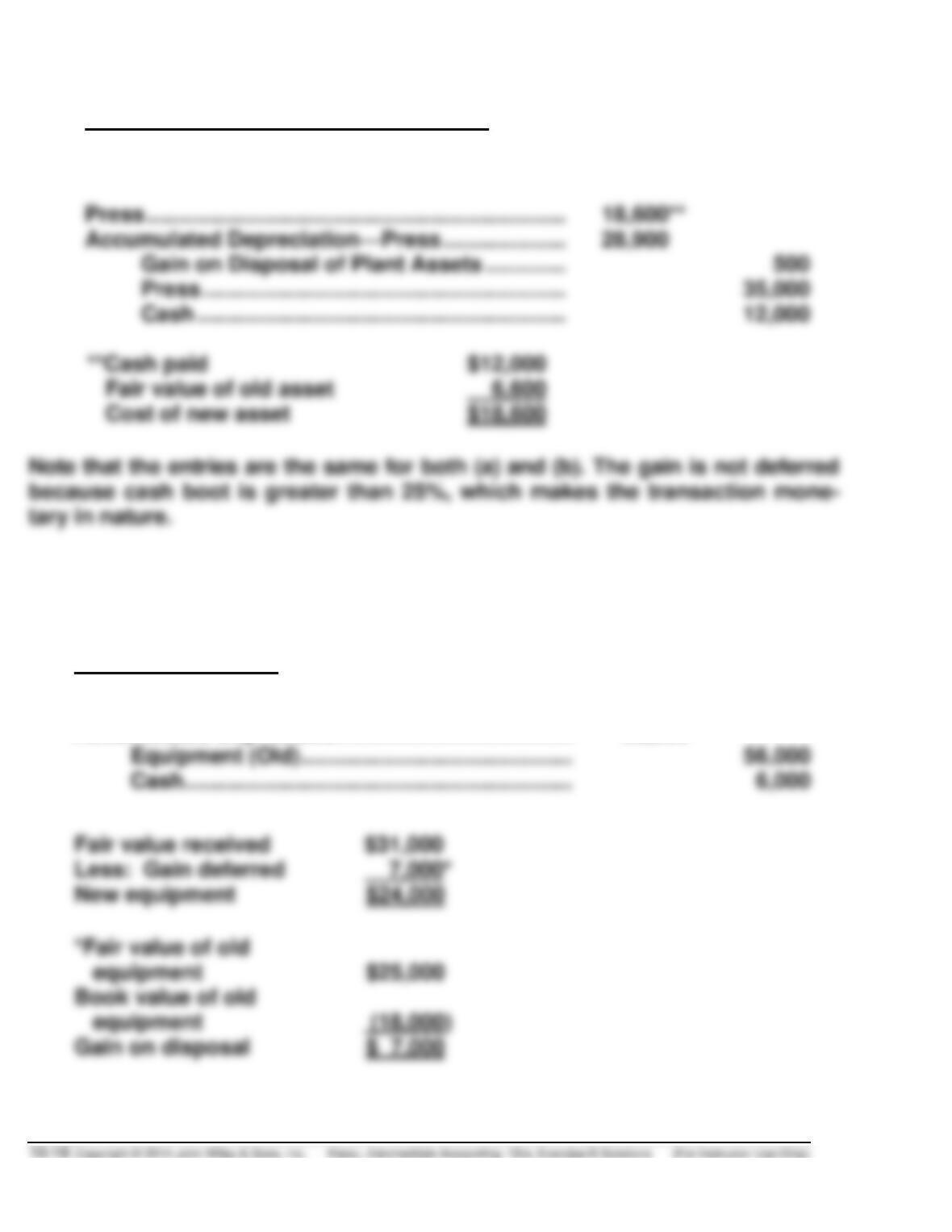

Press ……………………………………………………………………..

Accumulated Depreciation—Press …………………………..

Gain on Disposal of Plant Assets ……………………..

Press ……………………………………………………….

35,000

Cash ……………………………………………………….

*Cost of old asset

$35,000

Accumulated depreciation

($27,200 + $1,700)

(28,900)

Book value

6,100

Fair value of old asset

Gain (on disposal of plant asset)

$ 500

**Cash paid

Fair value of old press

6,600

E10-18B (Continued)

(b)

Exchange lacks commercial substance:

Depreciation Expense ……………………………………………..

1,700

Accumulated Depreciation—Press …………………..

1,700

Press ……………………………………………………………………..

Accumulated Depreciation—Press …………………………..

Gain on Disposal of Plant Assets …………………….

Press ……………………………………………………….

Cash ……………………………………………………….

**Cash paid

Fair value of old asset

E10-19B (15–20 minutes)

(a) Exchange lacks commercial substance

Mathews Company:

Equipment (New) …………………………………………………….

24,000

Accumulated Depreciation ……………………………………….

38,000

Equipment (Old) ………………………………………………

Cash ……………………………………………………….

Fair value received

Less: Gain deferred

*Fair value of old

equipment

Book value of old

equipment

E10-19B (Continued)

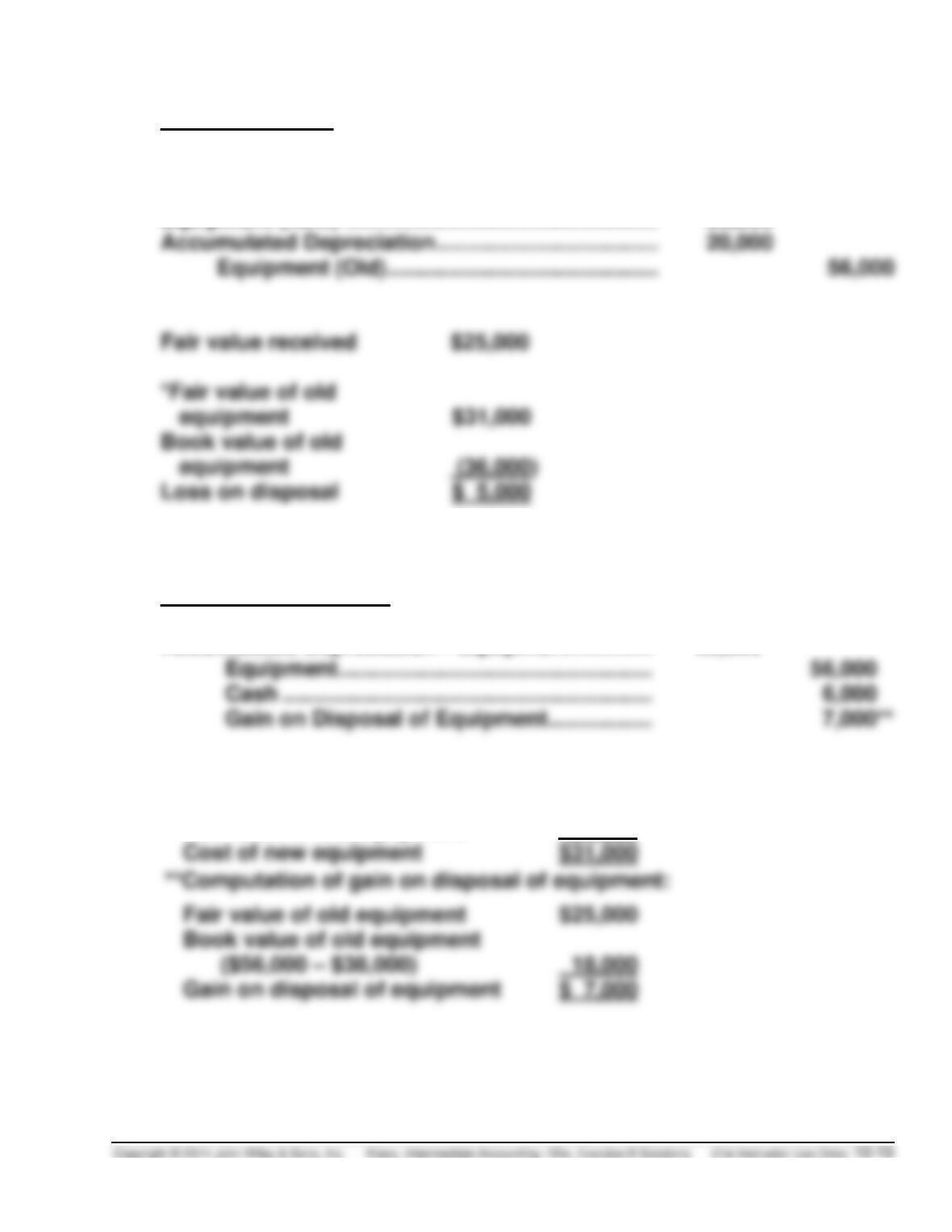

Biggio Company:

Cash ……………………………………………………………………….

6,000

Loss on Disposal of Equipment …………………………..

5,000

Equipment (New) …………………………………………………….

25,000

Accumulated Depreciation ……………………………………….

Equipment (Old) ………………………………………………

Fair value received

*Fair value of old

equipment

Book value of old

equipment

(b)

Exchange has commercial substance

Mathews Corporation:

Equipment ……………………………………………………….

31,000*

Accumulated Depreciation—Equipment …………………….

38,000

Equipment ………………………………………………………

Cash ……………………………………………………….

Gain on Disposal of Equipment………………………..

*Cost of new equipment:

Cash paid

$ 6,000

Fair value of old equipment

25,000

**Computation of gain on disposal of equipment:

Fair value of old equipment

$25,000

E10-19B (Continued)

Biggio Company:

Cash ………………………………………………………………………

6,000

Equipment ……………………………………………………….

25,000*

Accumulated Depreciation—Equipment (Old) ……………..

20,000

Loss on Disposal of Equipment …………………………..

Equipment …………………………..…………………………

56,000

Fair value of equipment

Less: Cash received

Fair value of equipment (Old)

E10-20B (15–20 minutes)

(a)

Exchange has commercial substance

Equipment ……………………………………………………….

55,300

Accumulated Depreciation—Equipment …………………..

38,500*

Gain on Disposal of Equipment ……………………….

Equipment …………………………..…………………………

Cash ($16,000 + $2,500) …………………………..

Valuation of equipment

Cash

$16,000

Installation cost

Market value of used equipment

E10-20B (Continued)

Computation of gain

Cost of old asset

$71,000

Accumulated depreciation

Book value

Gain on disposal of equipment

(b)

Fair value not determinable

Automatic Equipment ……………………………………………..

51,000*

Accumulated Depreciation—Equipment ……………………

38,500

Equipment ………………………………………………………

Cash ……………………………………………………….

Book value of old equipment

Cash paid (including installation costs)

E10-21B (20–25 minutes)

(a) Any addition to plant assets is capitalized because a new asset has been

created. This addition increases the service potential of the plant.

E10-21B (Continued)

(d) Conceptually, the book value of the old plumbing system should be

removed. However, practically it is often difficult if not impossible to

determine this amount. In this case, one of two approaches is followed. One

(e) See discussion in (d) above. In this case, because the useful life of the

asset has increased, a debit to Accumulated Depreciation would appear

to be the most appropriate.

E10-22B (15–20 minutes)

1/30

Accumulated Depreciation—Buildings …………………….

142,500*

Loss on Disposal of Plant Assets …………………………..

125,500**

Buildings ……………………………………………………….

250,000

Cash ……………………………………………………….

18,000

**($250,000 – $142,500) + $18,000

3/10

Cash ($1,500 – $1,000) …………………………………………….

500

Accumulated Depreciation—Machinery ……………………

14,000*

Machinery …………………………..………………………….

20,000

**($20,000 – $14,000 – $500)

E10-22B (Continued)

3/20

Equipment Repairs and Maintenance Expense …………….

750

Cash ……………………………………………………….

750

5/18

Machinery (New) ……………………………………………………..

6,000

Accumulated Depreciation—Machinery ……………………

1,800*

Loss on Disposal of Plant Assets …………………………..

1,200**

Machinery (Old) …………………………..………………….

Cash ……………………………………………………….

**($3,000 – $1,800)

6/23

Building Maintenance and Repairs Expense ……………..

Cash ……………………………………………………….

12,000

E10-23B (20–25 minutes)

(a) C

(b) C

E10-24B (20–25 minutes)

(a)

Depreciation Expense (10/12 X $72,000) …………………..

60,000

Accumulated Depreciation—Machine ………………

60,000

Cash ………………………………………………………………………

460,000

Accumulated Depreciation—Machine

($720,000 + $60,000) ……………………………………………..

780,000

Machine ……………………………………………………….

Gain on Disposal of Machine

$460,000 – ($980,000 – $780,000) …………………..

(b)

Depreciation Expense (5/12 X $72,000) …………………….

30,000

Accumulated Depreciation—Machine ………………

30,000

Cash ………………………………………………………………………

300,000

Accumulated Depreciation—Machine

($720,000 + $30,000) ……………………………………………..

750,000

Machine ……………………………………………………….

Gain on Disposal of Machine

[$300,00 – ($980,000 – $750,000)] ……………………..

(c)

Depreciation Expense (8/12 X $72,000) …………………….

48,000

Accumulated Depreciation—Machine ………………

48,000

Contribution Expense ……………………………………………..

610,000

Accumulated Depreciation—Machine

($720,000 + $48,000) ……………………………………………..

768,000

Machine ……………………………………………………….

Gain on Disposal of Machine …………………………..

*$610,000 – ($980,000 – $768,000)

E10-25B (15–20 minutes)

April 1

Cash …………………………..………………………………………….

375,000

Accumulated Depreciation—Building ………………………

125,000

Land ……………………………………………………….

Building ……………………………………………………….

Gain on Disposal of Plant Assets …………………….

Aug. 1

Land ………………………………………………………………………

Building ……………………………………………………….

525,000

Cash ……………………………………………………….