EXERCISE 19-8 (10–15 minutes)

(a) 2014

Income Tax Expense ………………………………………. 336,000

Deferred Tax Asset ($20,000 X 40%) ………………… 8,000

Deferred Tax Liability ($30,000 X 40%) ……… 12,000

(b)

Current assets

Deferred tax asset ($8,000 + $4,000 + $3,200) $15,200

(c)

Pretax financial income $945,000

Income tax expense

Current $377,200

EXERCISE 19-9 (15–20 minutes)

2011

Income Tax Expense ……………………………………………….. 32,000

Income Taxes Payable ($80,000 X 40%) ……………… 32,000

Deferred Tax Asset ………………………………………………….. 120,000

Benefit Due to Loss Carryforward

(Income Tax Expense) …………………………………… 120,000

[40% X ($380,000 – $80,000)]

2014

EXERCISE 19-10 (20–25 minutes)

(a) Income Tax Refund Receivable ………………………….. 29,950

[($17,000 X 35%) + ($48,000 X 50%)]

Benefit Due to Loss Carryback ……………………. 29,950

(c) Income Tax Expense …………………………………………. 36,000

Deferred Tax Asset …………………………..………… 34,000

Income Taxes Payable ………………………………… 2,000

[40% X ($90,000 – $85,000)]

(d) Income before income taxes $90,000

Income tax expense

Current $ 2,000

Deferred 34,000 36,000

Net income $54,000

EXERCISE 19-11 (10–15 minutes)

Resulting

Deferred Tax

Related Balance Sheet

Temporary Difference

(Asset)

Liability

Account

Classification

Depreciation

$200,000

Plant Assets

Noncurrent

*$120,000 X 40% = $48,000 **$225,000 – $48,000 = $177,000

Current assets

Deferred tax asset ($50,000 – $48,000) $ 2,000

EXERCISE 19-12 (20–25 minutes)

(a) To complete a reconciliation of pretax financial income and taxable

income, solving for the amount of pretax financial income, we must

first determine the amount of temporary differences arising or

reversing during the year. To accomplish that, we must determine the

EXERCISE 19-12 (Continued)

Cumulative temporary difference at 12/31/14

which will result in future deductible amounts $95,000

Cumulative temporary difference at 1/1/14

which will result in future deductible amounts 50,000

Originating difference in 2014 which will

result in future deductible amounts $45,000

(b) Income Tax Expense …………………………………………. 56,000

Deferred Tax Asset ……………………………………………. 18,000

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

First one

($230,000

40%

$92,000

Second one

40%

Totals

$92,000*

EXERCISE 19-12 (Continued)

Deferred tax asset at the end of 2014 $(38,000

Deferred tax asset at the beginning of 2014 20,000

(c) Income before income taxes $140,000

Income tax expense

Current $42,000

EXERCISE 19-13 (20–25 minutes)

(a) Income Tax Expense …………………………..…………. 178,500

Income Taxes Payable …………………………….. 128,000

Future Years

2014

2015

2016

2017

Total

Enacted tax rate

Future taxable (deductible)

EXERCISE 19-13 (Continued)

(b) Income Tax Expense ………………………………………. 156,500

Income Taxes Payable ……………………………… 128,000

Deferred Tax Liability ……………………………….. 28,500

EXERCISE 19-14 (20–25 minutes)

(a) Income Tax Expense ………………………………………. 298,000

Deferred Tax Asset …………………………………………. 30,000

Income Taxes Payable ……………………………… 328,000

EXERCISE 19-14 (Continued)

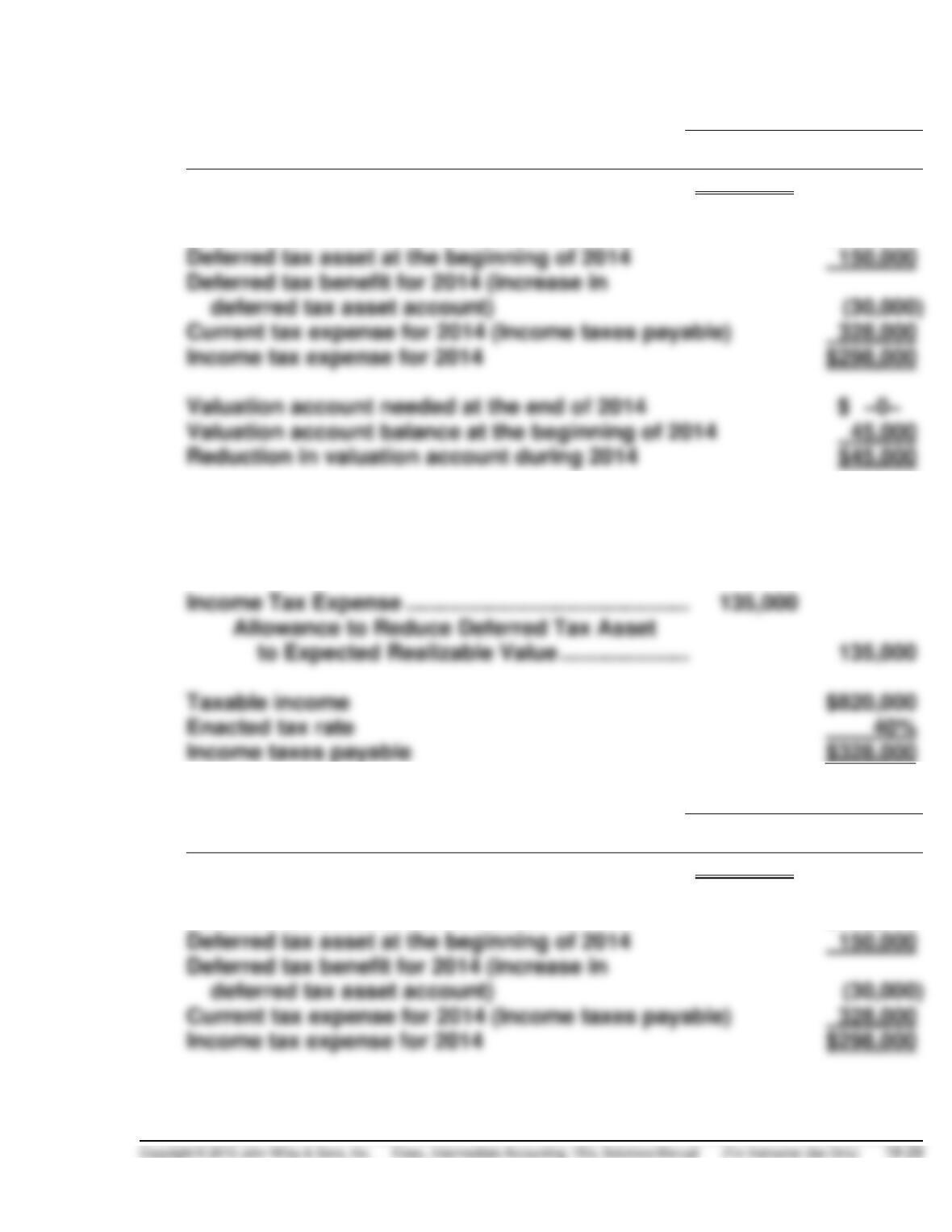

Deferred tax asset at the end of 2014 $180,000

Deferred tax asset at the beginning of 2014 150,000

(b) The journal entry at the end of 2014 to establish a valuation account:

Income Tax Expense …………………………..………….. 30,000

Allowance to Reduce Deferred Tax Asset

to Expected Realizable Value ………………… 30,000

Note to instructor: Although not requested by the instructions, the

pretax financial income can be computed by completing the following

reconciliation:

EXERCISE 19-15 (20–25 minutes)

(a) Income Tax Expense …………………………..…………. 298,000

Deferred Tax Asset ………………………………………… 30,000

EXERCISE 19-15 (Continued)

Date

Cumulative Future Taxable

(Deductible) Amounts

Tax Rate

Deferred Tax

(Asset)

Liability

12/31/14

$(450,000)

40%

$(180,000)

Deferred tax asset at the end of 2014 $180,000

(b) Income Tax Expense ………………………………………. 298,000

Deferred Tax Asset …………………………………………. 30,000

Income Taxes Payable ……………………………… 328,000

Date

Cumulative Future Taxable

(Deductible) Amounts

Tax Rate

Deferred Tax

(Asset)

Liability

12/31/14

$(450,000)

40%

$(180,000)

Deferred tax asset at the end of 2014 $180,000

EXERCISE 19-15 (Continued)

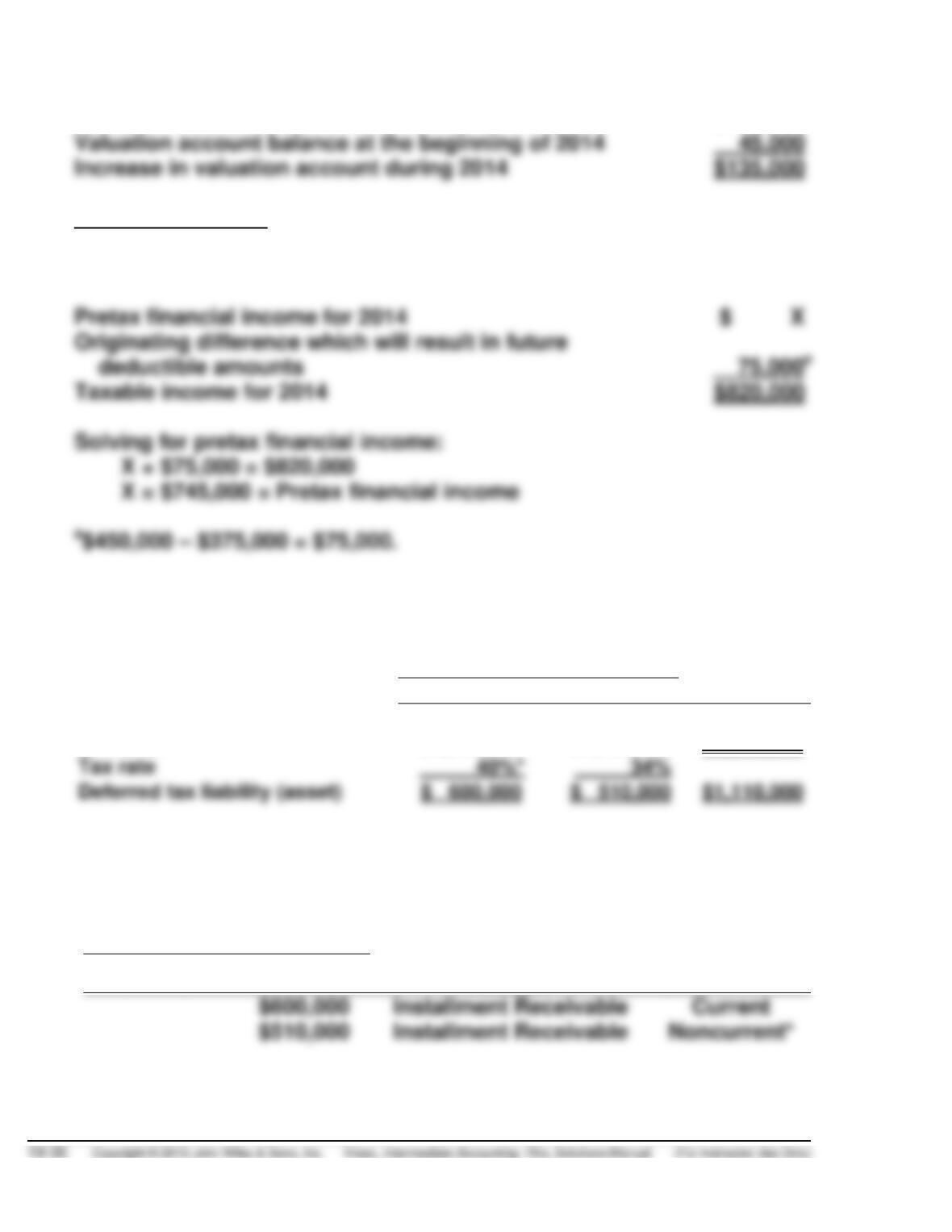

Valuation account needed at the end of 2014 $180,000

Note to instructor: Although not requested by the instructions, the

pretax financial income can be computed by completing the following

reconciliation:

EXERCISE 19-16 (15–20 minutes)

(a)

Future Years

2014

2015

Total

Future taxable (deductible)

amounts

$1,500,000

$1,500,000

$3,000,000

*The prior tax rate of 40% is computed by dividing the $1,200,000

balance of the deferred tax liability account at January 1, 2013, by the

$3,000,000 cumulative temporary difference at that same date.

Resulting Deferred Tax

Related Balance Sheet

Account

Classification

(Asset)

Liability

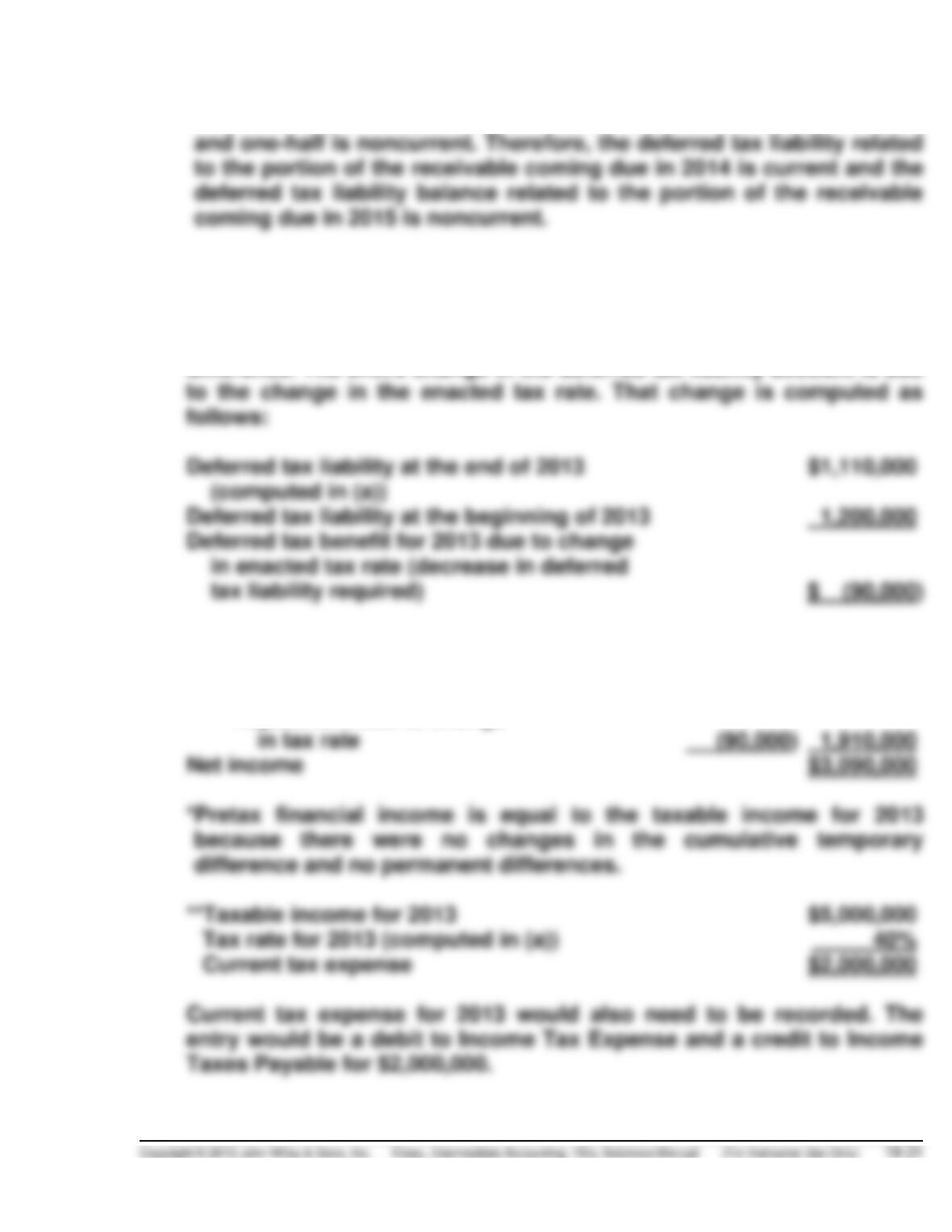

EXERCISE 19-16 (Continued)

* One-half of the installment receivable is classified as a current asset

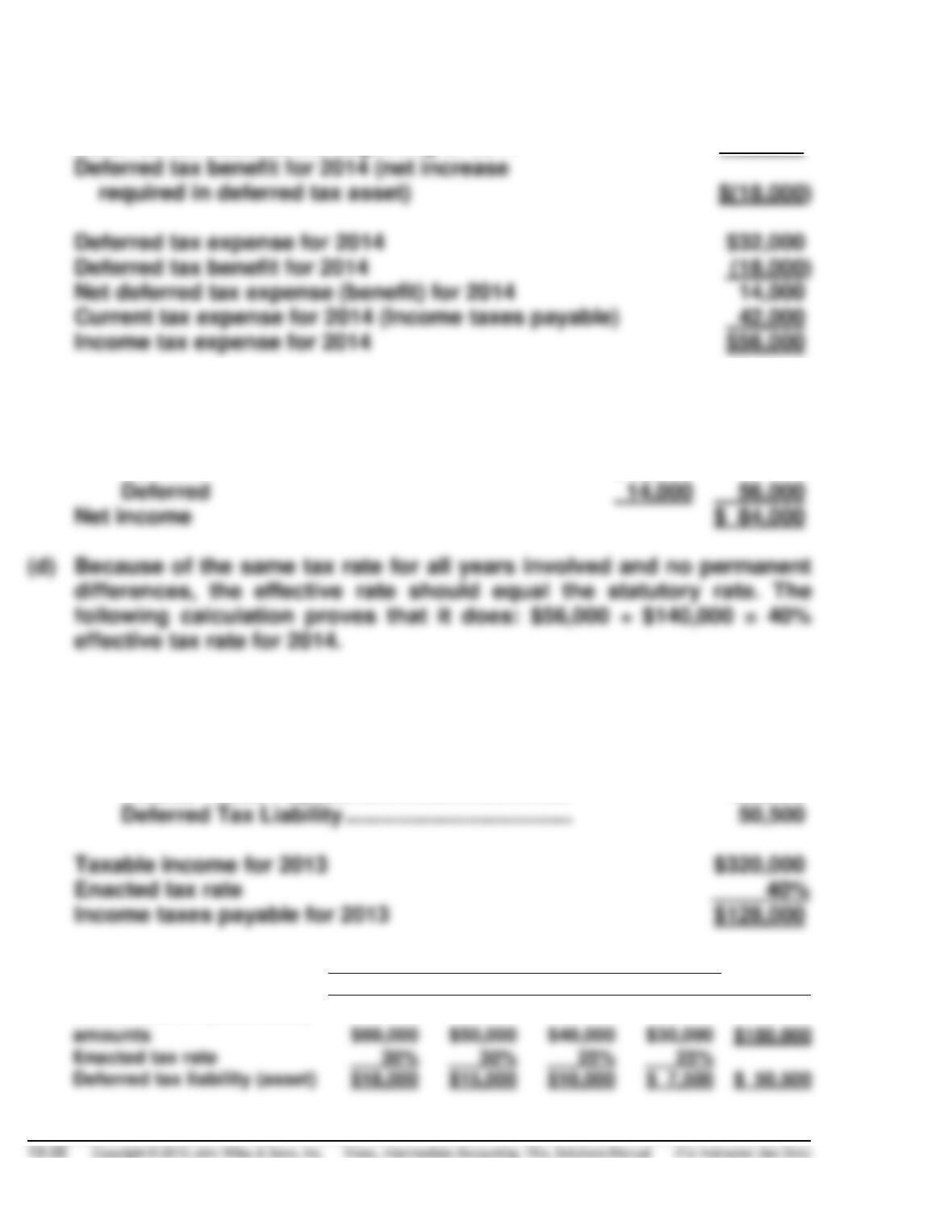

(b) Deferred Tax Liability ………………………………………… 90,000

Income Tax Expense …………………………………… 90,000

There are no changes during 2013 in the cumulative temporary

difference. The entire change in the deferred tax liability account is due

(c) Income before income taxes $5,000,000*

Income tax expense

Current $2,000,000**

Adjustment due to change

EXERCISE 19-17 (30–35 minutes)

Journal entry at December 31, 2013:

Income Tax Expense …………………………..……………. 67,900

Deferred Tax Asset …………………………………………… 4,500

The deferred tax account balances at December 31, 2013, are determined

as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Rate

Deferred Tax

(Asset)

Liability

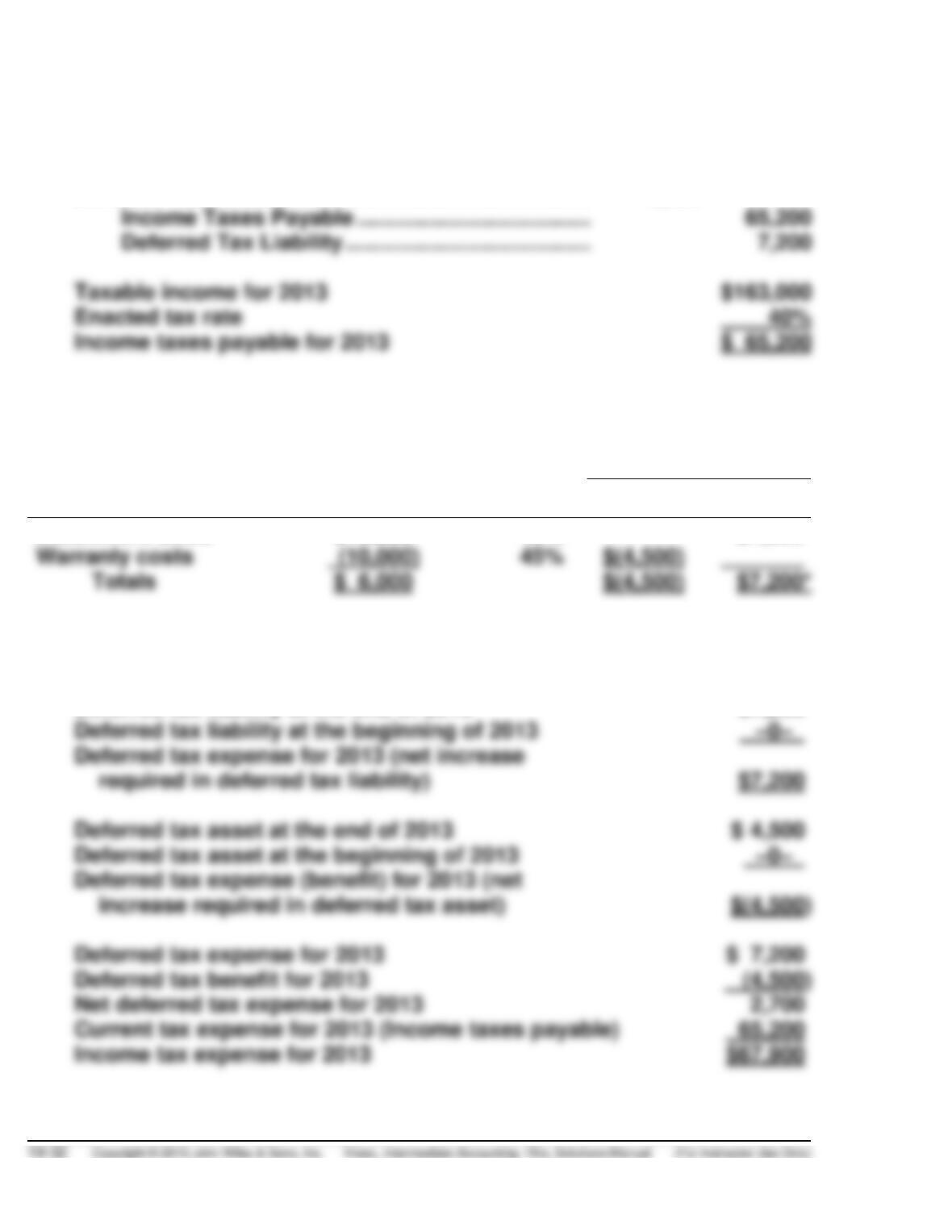

Installment sales

($16,000

45%

$7,200

Warranty costs

45%

*Because all deferred taxes were computed at the same rate, these totals

can be reconciled as follows: $6,000 X 45% = $(4,500) + $7,200.

Deferred tax liability at the end of 2013 $7,200

EXERCISE 19-17 (Continued)

Journal entry at December 31, 2014:

Income Tax Expense ………………………………………… 94,500

The deferred tax account balances at December 31, 2014, are determined

as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Rate

Deferred Tax

(Asset)

Liability

Installment sales

($8,000

45%

$3,600

Warranty costs

( (5,000)

45%

Totals

$3,600*

*Because all deferred taxes were computed at the same rate, these totals

can be reconciled as follows: $3,000 X 45% = $(2,250) + $3,600.

Deferred tax liability at the end of 2014 $(3,600

EXERCISE 19-17 (Continued)

Journal entry at December 31, 2015:

Income Tax Expense …………………………..……………. 40,500

Deferred Tax Liability ……………………………………….. 3,600

Deferred tax asset at the end of 2015 $ 0

Deferred tax asset at the beginning of 2015 2,250

Deferred tax expense for 2015 (decrease

required in deferred tax asset) $2,250

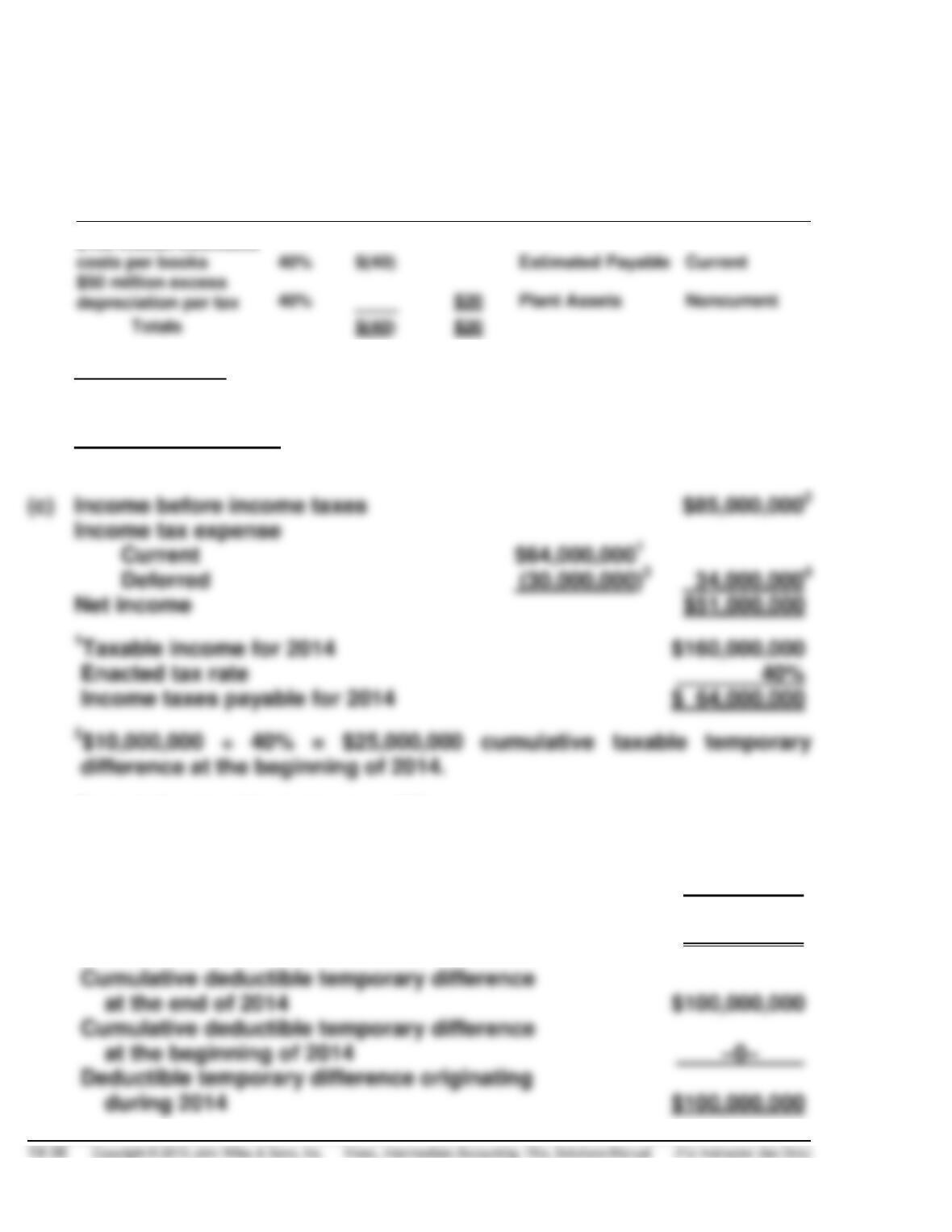

EXERCISE 19-18 (20–25 minutes)

(a)

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

December 31, 2014

Deferred Tax

(Asset)

Liability

Installment sales

($ 96,000)

40%

$38,400

Depreciation

40%

Unearned rent

40%

Totals

($ 26,000)

$50,400*

EXERCISE 19-18 (Continued)

(b) Pretax financial income for 2014 $250,000

(c) Income Tax Expense ………………………………………. 111,200

Deferred Tax Asset …………………………………………. 40,000

Income Taxes Payable ……………………………… 100,800

Deferred Tax Liability ……………………………….. 50,400

Deferred tax asset at the end of 2014 $ 40,000

Deferred tax asset at the beginning of 2014 –0–

Deferred tax benefit for 2014 (net increase

required in deferred tax asset) $(40,000)

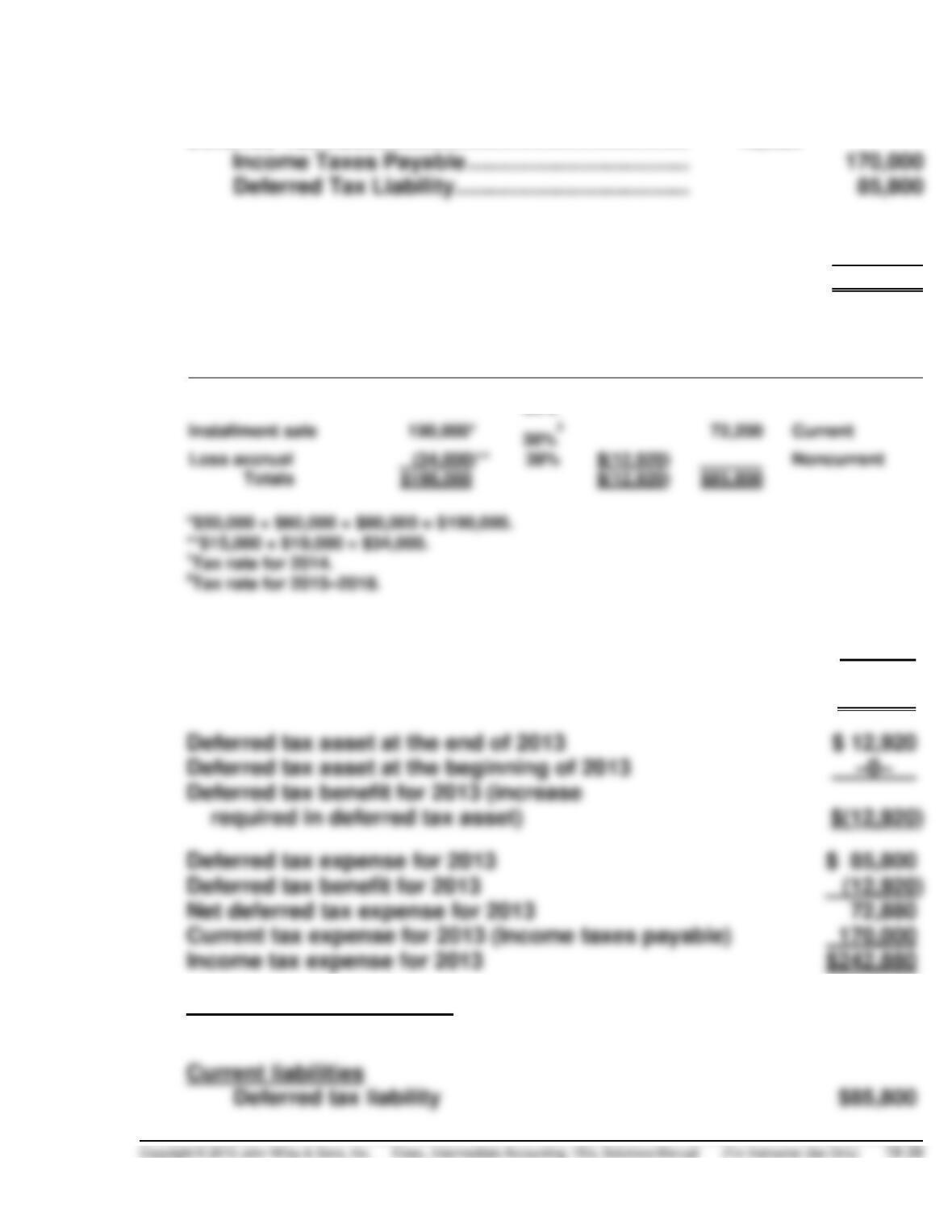

EXERCISE 19-19 (25–30 minutes)

(a) (All figures are in millions.)

Temporary

Difference

Rate

Resulting

Deferred Tax

Related Balance

Sheet Account

Classification

(Asset)

Liability

$50 million excess

$100 million estimated

(b) Current assets

Deferred tax asset $40,000,000

Long-term liabilities

Deferred tax liability $20,000,000

Cumulative taxable temporary difference

at the end of 2014 $50,000,000

Cumulative taxable temporary difference

at the beginning of 2014 25,000,000

Taxable temporary difference originating

during 2014 $25,000,000

EXERCISE 19-19 (Continued)

Pretax financial income for 2014 $ X

Taxable temporary difference originating (25,000,000)

Deductible temporary difference originating 100,000,000

Taxable income for 2014 $160,000,000

Deferred tax asset at the end of 2014 $(40,000,000

Deferred tax asset at the beginning of 2014 –0–

Deferred tax benefit for 2014 (increase in

EXERCISE 19-20 (15–20 minutes)

(a) Income Tax Expense ………………………………………. 128,800

Deferred Tax Asset …………………………………………. 68,000

Income Taxes Payable ……………………………… 176,800

EXERCISE 19-20 (Continued)

Taxable income for 2013 $520,000

Tax rate 34%

Income taxes payable for 2013 $176,800

Deferred tax liability at the end of 2013 $ 20,000

Deferred tax liability at the beginning of 2013 –0–

Deferred tax expense for 2013 (increase

required in deferred tax liability account) $ 20,000

(b) Current assets

Deferred tax asset $68,000

EXERCISE 19-21 (20–25 minutes)

(a) Income Tax Expense ………………………………………. 242,880

Deferred Tax Asset …………………………………………. 12,920

Taxable income $500,000

Enacted tax rate 34%

Income taxes payable $170,000

Temporary

Difference

Future Taxable

(Deductible)

Amounts

Tax

Rate

Deferred Tax

Classification

(Asset)

Liability

Installment sale

*$ 40,000*

34%1

$13,600

Current

Deferred tax liability at the end of 2013 $85,800

Deferred tax liability at the beginning of 2013 –0–

Deferred tax expense for 2013 (increase

required in deferred tax liability) $85,800

(b) Other assets (noncurrent)

Deferred tax asset $12,920

EXERCISE 19-21 (Continued)

The deferred tax asset is noncurrent because the related liability is

noncurrent. The liability from the accrual of the loss contingency is

noncurrent because it is expected to be settled in years later than the

year immediately following the balance sheet date.

EXERCISE 19-22 (15–20 minutes)

(a) Income Tax Expense …………………………..…………. 125,800

Taxable income $350,000

Enacted tax rate 34%

Income taxes payable $119,000

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability