PROBLEM 8-5B (Continued)

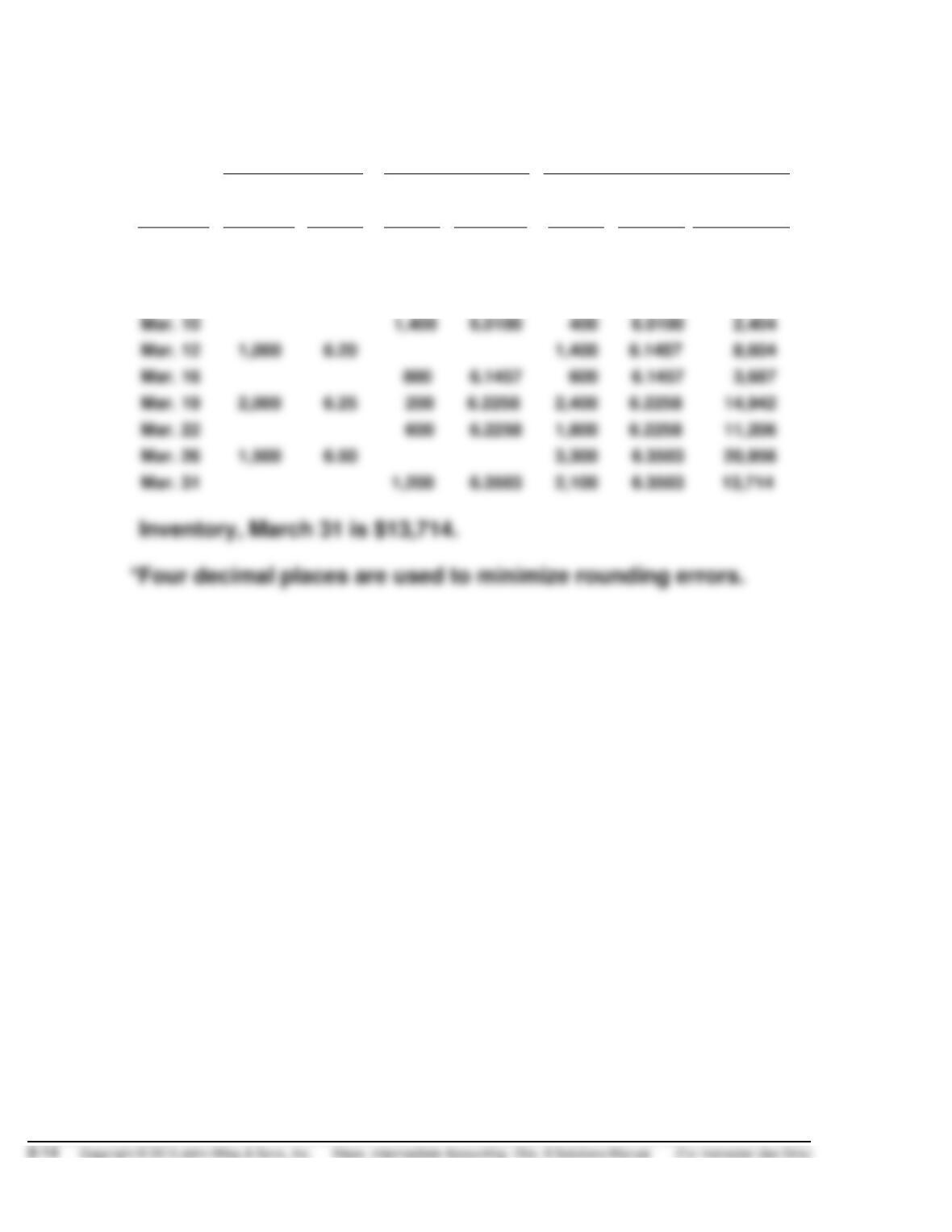

3. Average cost.

Received

Issued

Balance

Date

No. of

units

Unit

cost

No. of

units

Unit

cost

No. of

units

Unit

cost*

Amount

Mar. 1

2,000

$6.00

2,000

$6.0000

$12,000

Mar. 6

500

6.05

2,500

6.0100

5,025

Mar. 8

700

$6.0100

1,800

6.0100

10,818

Mar. 10

1,400

400

6.0100

Mar. 12

1,000

6.20

Mar. 16

600

6.1457

Mar. 19

200

2,400

6.2258

Mar. 22

600

1,800

Mar. 26

3,300

6.3503

Mar. 31

2,100

6.3503

13,714

PROBLEM 8-6B

(a)

Beginning inventory …………………

1,600

Purchases (3,500 + 2,000) ………….

5,500

Units available for sale ……………..

Sales (1,000 + 4,000) …………………

Periodic FIFO

$161,800

(b)

Perpetual FIFO

Same as periodic:

$161,800

(c)

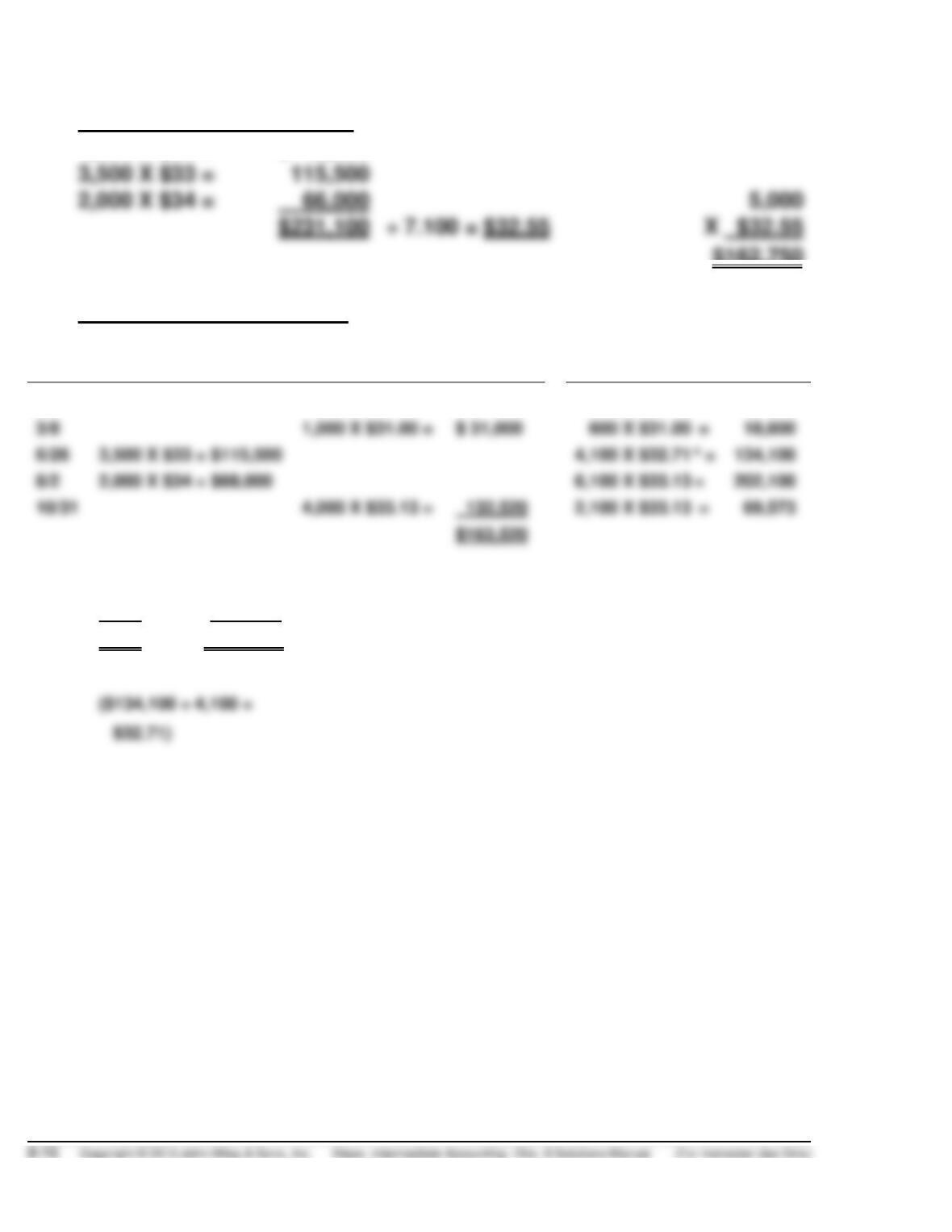

Periodic LIFO

2,000 X $34 =

(d)

Perpetual LIFO

Date

Purchased

Sold

Balance

1/1

1,600 X $31

$ 49,600

3/6

1,000 X $31

$31,000

600 X $31

$ 18,600

6/26

3,500 X $33 = $115,500

600 X $31

3,500 X $33

8/2

2,000 X $34 = $68,000

600 X $31

3,500 X $33

2,000 X $34

10/31

2,000 X $34

$68,000

600 X $31

PROBLEM 8-6B (Continued)

(e)

Periodic weighted-average

1,600 X $31 =

$ 49,600

3,500 X $33 =

2,000 X $34 =

66,000

$162,750

(f)

Perpetual moving average

Date

Purchased

Sold

Balance

1/1

1,600 X $31.00 =

$ 49,600

3/8

1,000 X $31.00 =

$ 31,000

18,600

6/26

3,500 X $33 = $115,500

4,100 X $32.71 a =

134,100

8/2

2,000 X $34 = $68,000

6,100 X $33.13 =

202,100

10/31

4,000 X $33.13 =

69,573

$163,520

a

600 X $31 = $ 18,600

3,500 X $33 = 115,100

4,100 $ 134,100

PROBLEM 8-7B

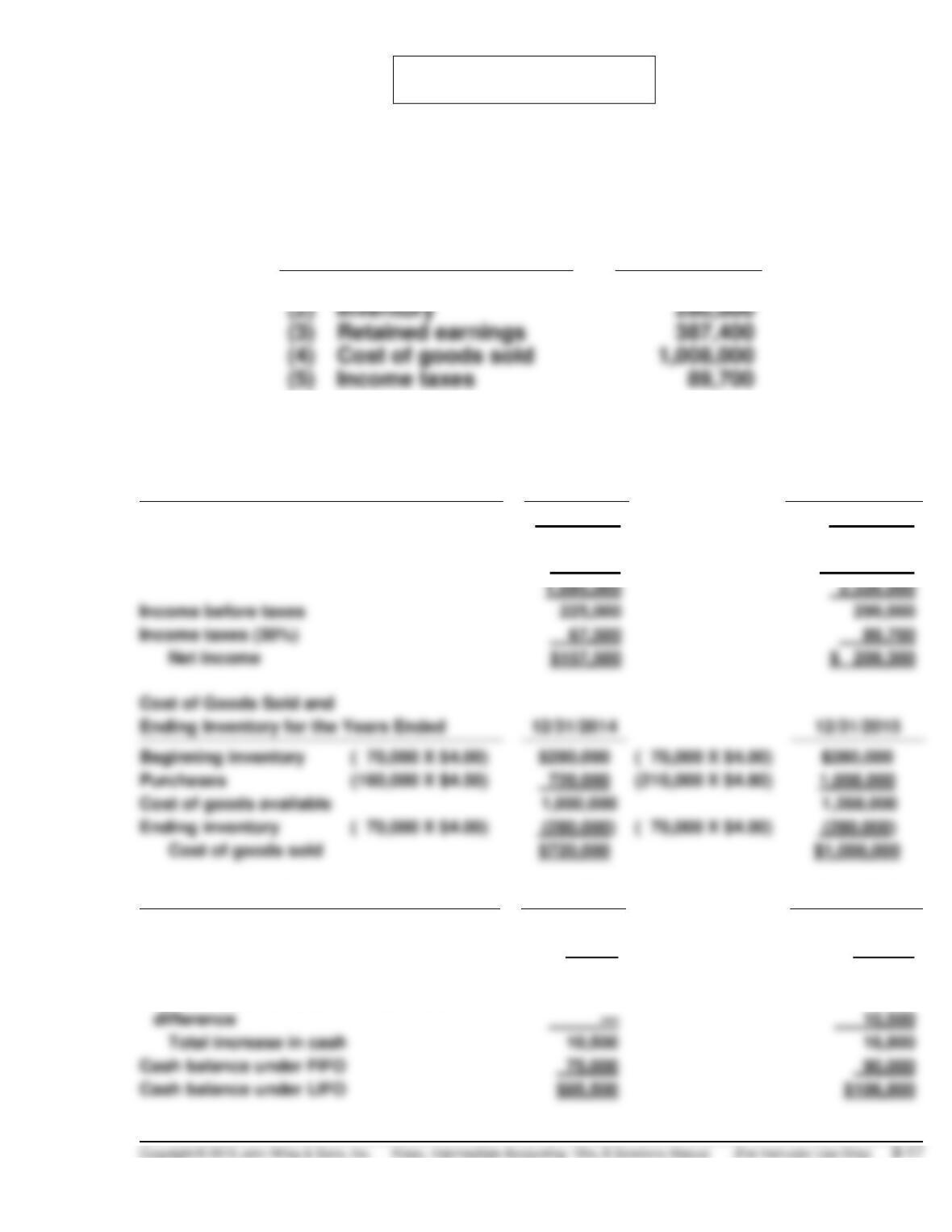

The accounts in the 2015 financial statements which would be affected by

a change to LIFO and the new amount for each of the accounts are as

follows:

Account

New amount

for 2015

(1)

Cash

$106,800

(2)

Inventory

(3)

Retained earnings

(4)

Cost of goods sold

The calculations for both 2014 and 2015 to support the conversion to LIFO

are presented below.

Income for the Years Ended

12/31/2014

12/31/2015

Sales revenue

$1,920,000

$2,625,000

Less: Cost of goods sold

720,000

1,008,000

Other expenses

975,000

1,318,000

Income before taxes

225,000

299,000

Income taxes (30%)

Net income

Ending Inventory for the Years Ended

12/31/2014

12/31/2015

Beginning inventory

( 70,000 X $4.00)

( 70,000 X $4.00)

Purchases

Cost of goods available

Ending inventory

( 70,000 X $4.00)

(280,000)

( 70,000 X $4.00)

Determination of Cash at

12/31/2014

12/31/2015

Income taxes under FIFO

$ 78,000

$96,000

Income taxes as calculated under LIFO

67,500

89,700

Increase in cash

10,500

6,300

difference

10,500

Total increase in cash

10,500

Adjust cash at 12/31/2015 for 2014 tax

PROBLEM 8-7B (Continued)

Determination of Retained Earnings at

12/31/2014

12/31/2015

Net income under FIFO

$182,000

$224,000

Net income under LIFO

(157,500)

(209,300)

Reduction in retained earnings

for 2014 reduction

Total reduction in retained earnings

Retained earnings under FIFO

PROBLEM 8-8B

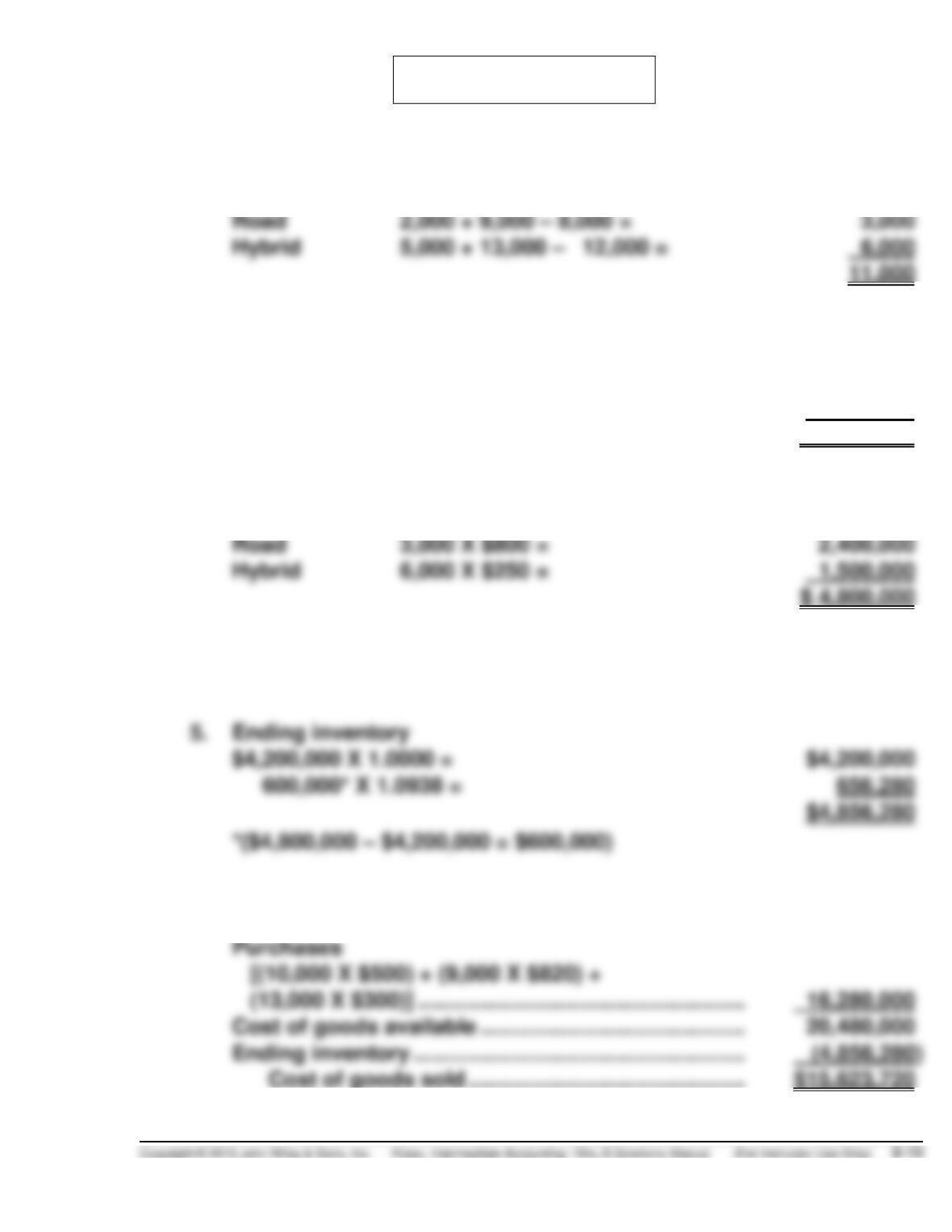

(a)

1.

Ending inventory in units

Mountain

3,000 + 10,000 – 11,000 =

2,000

Road

2,000 + 9,000 – 8,000 =

3,000

Hybrid

5,000 + 13,000 – 12,000 =

2.

Ending inventory at current cost

Mountain

2,000 X $495 =

$ 990,000

Road

3,000 X $820 =

2,460,000

Hybrid

6,000 X $300 =

1,800,000

$ 5,250,000

3.

Ending inventory at base-year cost

Mountain

2,000 X $450 =

$ 900,000

Road

3,000 X $800 =

Hybrid

6,000 X $250 =

1,500,000

$ 4,800,000

4.

Price index

$5,250,000 ÷ $4,800,000 = 1.0938

5.

Ending inventory

$4,200,000 X 1.0000 =

600,000* X 1.0938 =

*($4,800,000 – $4,200,000 = $600,000)

6.

Cost of goods sold

Beginning inventory ………………………………………….

$ 4,200,000

Purchases

Cost of goods available …………………………………….

Ending inventory ………………………………………………

Cost of goods sold ………………………………………

PROBLEM 8-8B (Continued)

7.

Gross profit

Sales revenue

(12,000 X $500)] …………………………………………………..

$21,450,000

Cost of goods sold …………………………………………………

(b)

1.

Ending inventory at current cost restated to base cost

Mountain

$ 990,000 ÷ 1.100a =

$ 900,000

a. $495 ÷ $450

b. $820 ÷ $800

c. $300 ÷ $250

2.

Ending inventory

Mountain

$ 900,000 X 1.000 =

$ 900,000

Road

800,000 X 1.025 =

Hybrid

300,000

3.

Cost of good sold

Cost of good available …………………………………………

$20,480,000

Ending inventory …………………………..…………………….

(4,870,000)

Cost of goods sold …………………………………………

$15,610,000

4.

Gross profit

Sales revenue ……………………………………………………..

$21,450,000

Cost of goods sold ………………………………………………

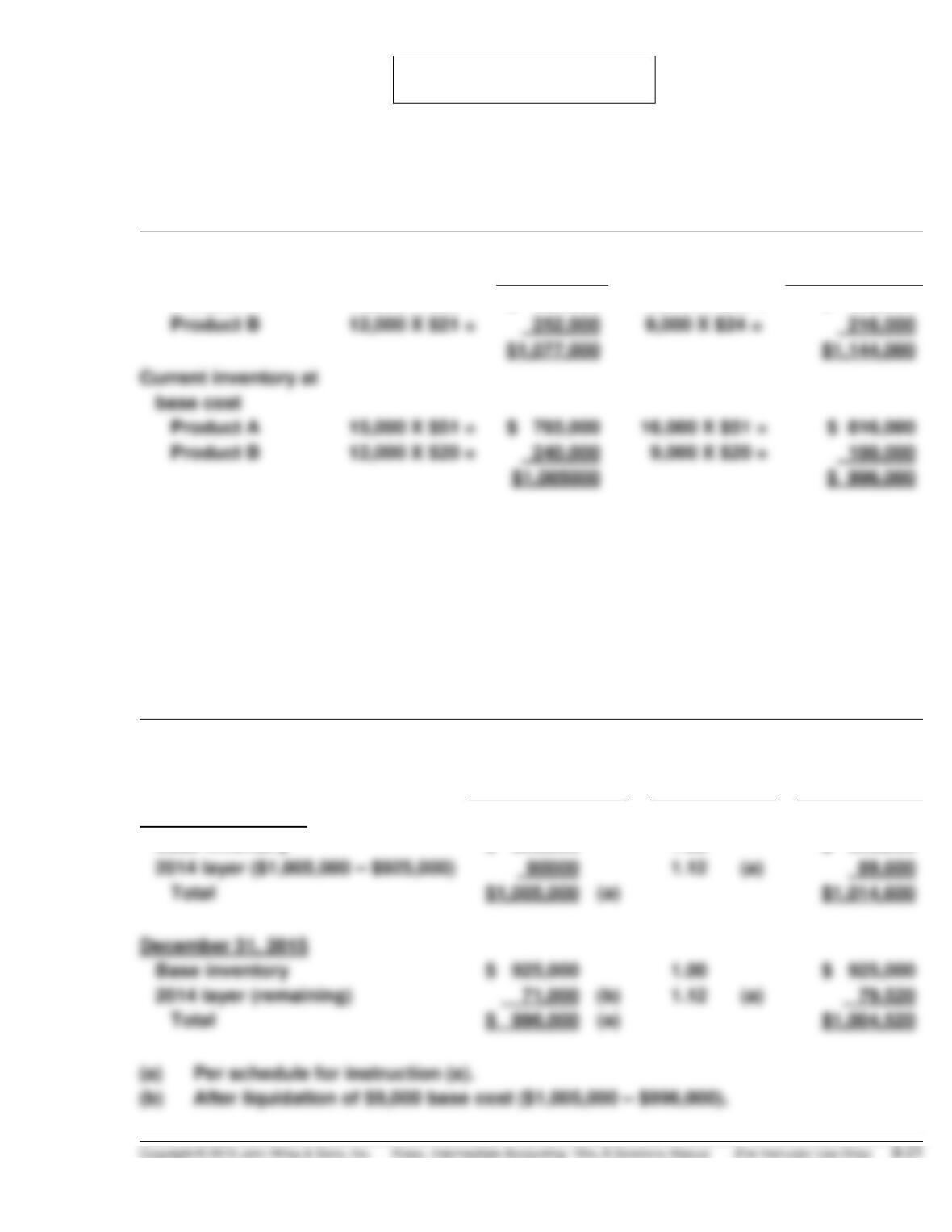

PROBLEM 8-9B

(a) SQUID FISHTANKS INC.

Computation of Internal Conversion Price Index

for Inventory Pool No. 1 Double Extension Method

Current inventory at

current-year cost

2014

2015

Product A

15,000 X $55 =

$ 825,000

16,000 X $58 =

$ 928,000

Product B

Current inventory at

base cost

Product A

16,000 X $51 =

Product B

12,000 X $20 =

Conversion price index

$1,177,000 ÷ $1,055,000 = 1.12 $1,144,000 ÷ $996,000 = 1.15

(b) SQUID FISHTANKS INC.

Computation of Inventory Amounts

Under Dollar-Value LIFO Method for Inventory Pool No. 1

at December 31, 2014 and 2015

Current

Inventory at

base cost

Conversion

price index

Inventory at

LIFO cost

December 31, 2014

Base inventory

$ 925,000

1.00

$ 925,000

2014 layer ($1,005,000 – $925,000)

December 31, 2015

Base inventory

2014 layer (remaining)

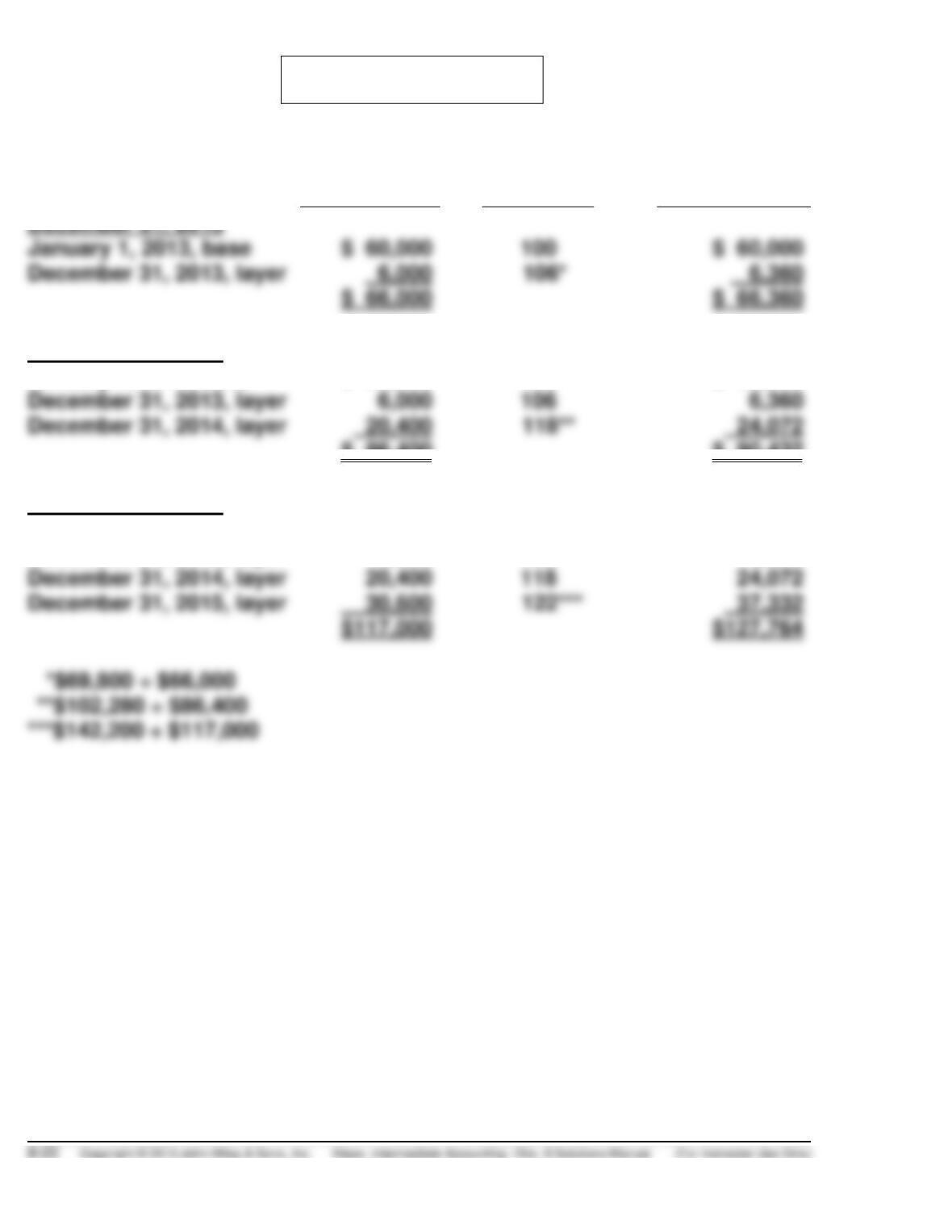

PROBLEM 8-10B

Base-Year

Cost

Index %

Dollar-Value

LIFO

December 31, 2013

January 1, 2013, base

$ 60,000

100

$ 60,000

December 31, 2013, layer

6,000

$ 66,000

$ 66,360

December 31, 2014

January 1, 2013, base

$ 60,000

100

$ 60,000

December 31, 2013, layer

106

December 31, 2014, layer

$ 86,400

$ 90,432

December 31, 2015

January 1, 2013, base

$ 60,000

100

$ 60,000

December 31, 2013, layer

6,000

106

6,360

December 31, 2014, layer

December 31, 2015, layer

$117,000

$127,764

*$69,800 ÷ $66,000

***$142,200 ÷ $117,000

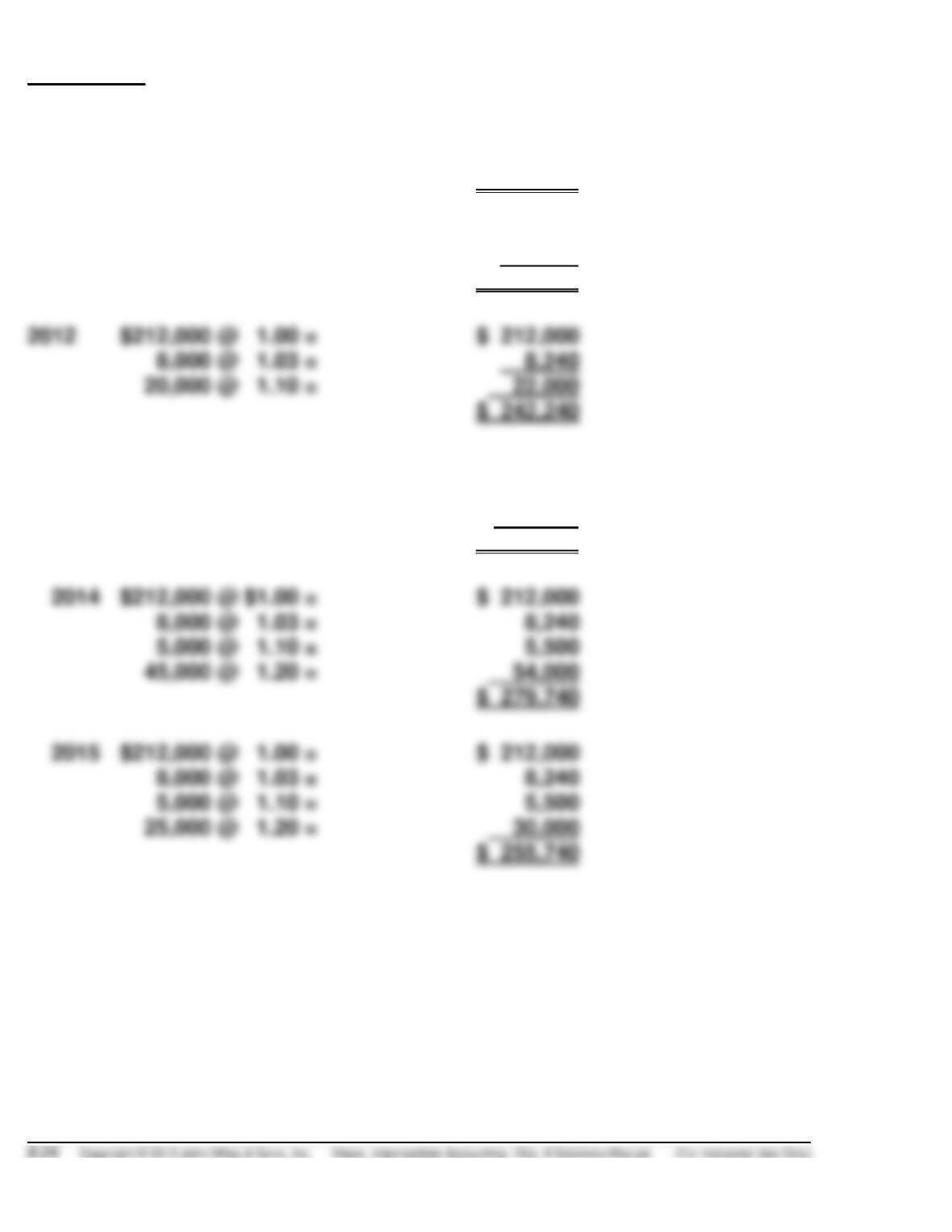

PROBLEM 8-11B

(a)

Schedule A

A

B

C

D

Current $

Price Index

Base-Year $

Change from

Prior Year

2010

$ 212,000

1.00

$ 212,000

—

2011

226,600

1.03

220,000

+$8,000

2012

264,000

1.10

2013

2014

324,000

1.20

270,000

2015

312,500

1.25

250,000

Schedule B

Ending Inventory-Dollar-Value LIFO:

2010

$ 212,000

2011

$212,000 @ $1.00 =

$ 212,000

8,000 @ 1.03 =

8,240

2012

$212,000 @ 1.00 =

$ 212,000

8,000 @ 1.03 =

8,240

20,000 @ 1.10 =

$ 220,240

2013

$212,000 @ 1.00 =

$ 212,000

8,000 @ 1.03 =

8,240

5,000 @ 1.10 =

5,500

$ 225,740

$212,000 @ $1.00 =

$ 212,000

8,000 @ 1.03 =

8,240

5,000 @ 1.10 =

5,500

45,000 @ 1.20 =

$ 279,740

$212,000 @ 1.00 =

8,000 @ 1.03 =

8,240

5,000 @ 1.10 =

PROBLEM 8-11B (Continued)

(b)

To: Landon Company

From: Accounting Student

Subject: Dollar-Value LIFO Pool Accounting

Dollar-value LIFO is an inventory method which values groups or “pools”

of inventory in layers of costs. It assumes that any goods sold during a

Because dollar-value LIFO combines various related costs in groups or

“pools,” no attempt is made to keep track of each individual inventory item.

Instead, each group of annual purchases forms a new cost layer of inventory.

Further, the most recent layer will be the first one carried to cost of goods

sold during this period.

To do this valuation, you need to know both the ending inventory at year-

end prices and the price index used to adjust the current year’s new layer.

The idea is to convert the current ending inventory into base-year costs.

PROBLEM 8-11B (Continued)

1. Refer to Schedule A. To express each year’s ending inventory (Column A)

in terms of base-year costs, simply divide the ending inventory by the

2. Next, compute the difference between the previous and the current

3. Finally, express this increment in current-year terms. For the second

year, this computation is straightforward: the base-year ending

Be careful with this last step in subsequent years. Notice that, in 2013, the

change from the previous year is –$15,000, which causes the 2012 layer to

be eroded during the period. Thus, the 2013 ending inventory is valued at

the original base-year cost $212,000 plus the 2011 layer of $8,240 plus the

remainder valued at the 2012 price index, $5,000 times 1.10. See 2013

computation on Schedule B.

These instructions should help you implement dollar-value LIFO in your

inventory valuation.