FINANCIAL STATEMENT ANALYSIS CASE 1 (Continued)

(e) Occidental would record a loss of $30,000,000 as revealed in the

following entry to record the transaction:

FINANCIAL STATEMENT ANALYSIS CASE 2

Part 1

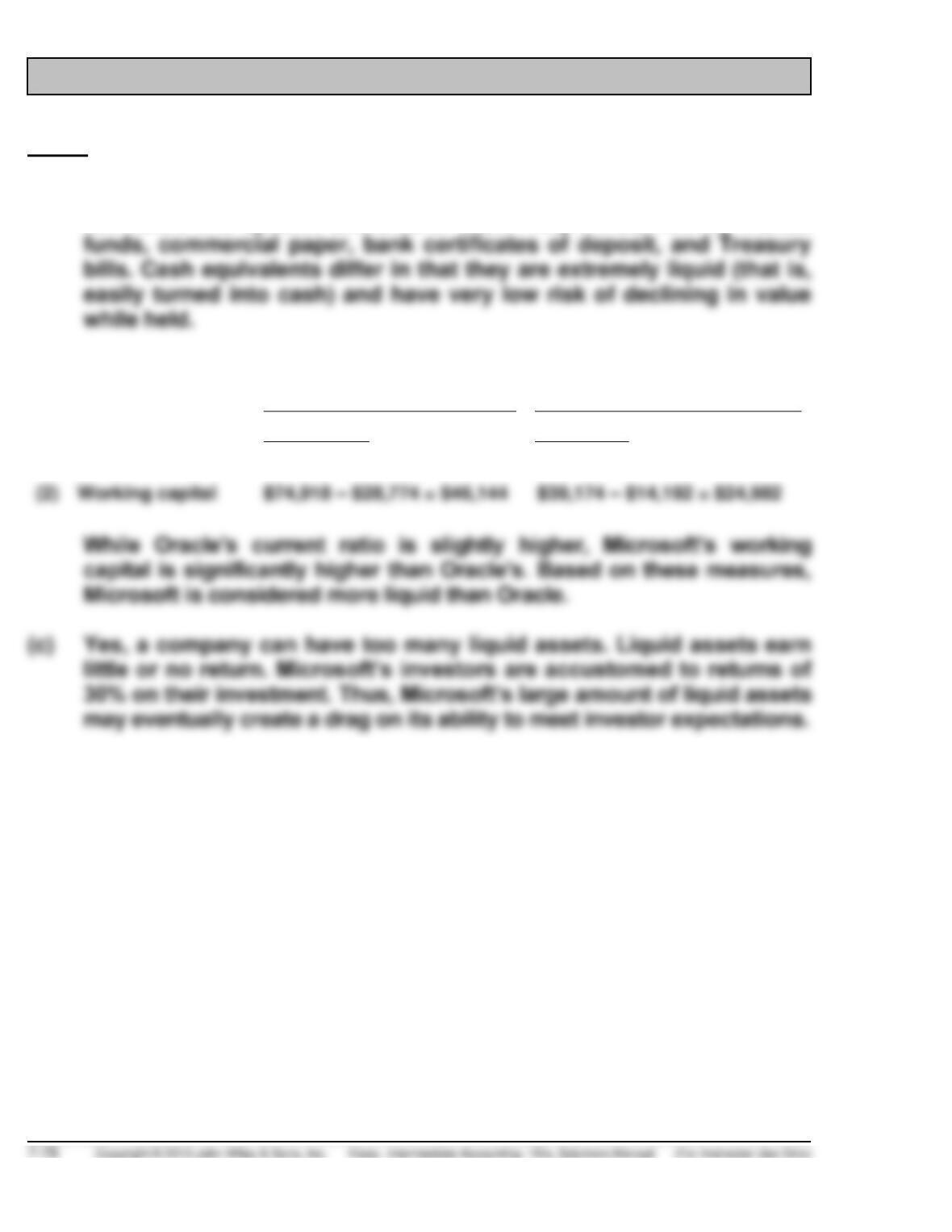

(a) Cash equivalents are short-term, highly liquid investments that can be

converted into specific amounts of cash. They include money market

(b)

(in millions)

Microsoft

Oracle

(1) Current ratio

$74,918

= 2.60

$39,174

= 2.76

$28,774

$14,192

FINANCIAL STATEMENT ANALYSIS CASE 2 (Continued)

Part 2

2011

(a)

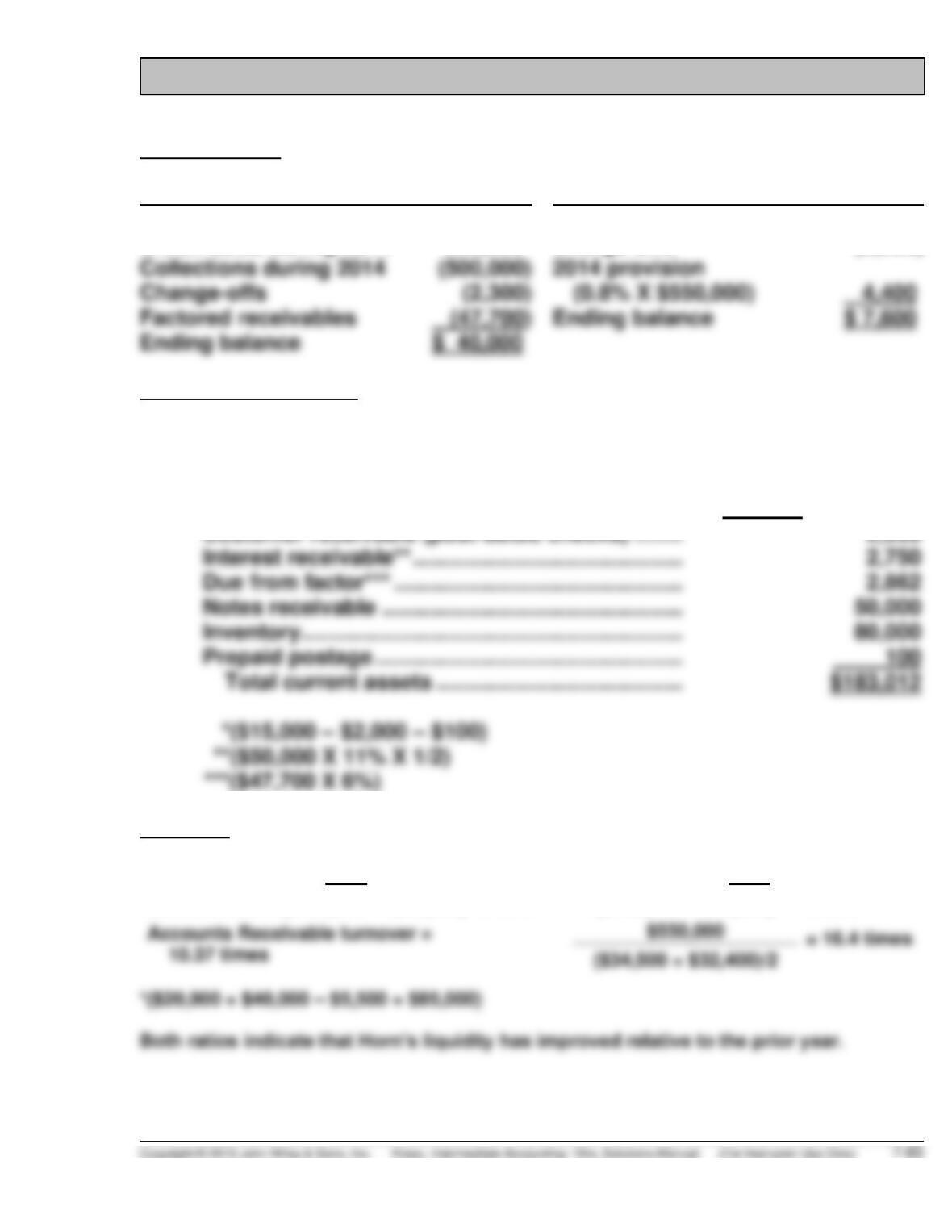

Receivables Turnover

$69,943

=

$69,943

= 5.0 times

($14,987 + $13,014)/2

$14,001

(c) Accounts receivable is reduced by the amount of bad debts in the

allowance account. This makes the denominator of the turnover ratio

ACCOUNTING, ANALYSIS, AND PRINCIPLES

ACCOUNTING

(a) Accounts Receivable:

Beginning balance

$46,000

Credit sales during 2014

Collections during 2014

(228,000)

Charge-offs

Factored receivables

Ending balance

Allowance for Doubtful Accounts:

Beginning balance

$550

Charge-offs

(1,600)

Ending balance

(b) Current assets section of December 31, 2014 The Flatiron Pub’s

balance sheet:

Cash

$ 5,575

Accounts receivable (net of $1,535

allowance for uncollectibles)

59,865

Interest receivable

Due from factor

Note receivable

Postage stamps

ACCOUNTING, ANALYSIS, AND PRINCIPLES (continued)

Calculations:

ANALYSIS

(a) 2013 current ratio = ($2,000 + $46,000 – $550 + $8,500) ÷ $37,000 = 1.51

(b) With a secured borrowing, the receivables would stay on The Flatiron

Pub’s books and a note payable would be recorded. This would

reduce both the current ratio and accounts receivable turnover ratio.

PRINCIPLES

The expense recognition principle requires that bad debt expense be

recorded in the period of the sale. Otherwise, income will be overstated by

PROFESSIONAL RESEARCH: FASB CODIFICATION

(a) Transfer of receivables is addressed in FASB ASC 860-10: Codification

String: Broad Transactions > 860 Transfers and Servicing > 10 Overall >

05 Background >

(b) The objectives associated with transfers: (FASB ASC 860–10–10)

10–1 An objective in accounting for transfers of financial assets is for

each entity that is a party to the transaction to recognize only

assets it controls and liabilities it has incurred, to derecognize

assets only when control has been surrendered, and to

PROFESSIONAL RESEARCH: FASB CODIFICATION (Continued)

(c) Definitions: (Codification String: Broad Transaction > 860 Transfers

and Servicing > 10 Overall > 20 Glossary)

Transfer

The conveyance of a noncash financial asset by and to someone other

than the issuer of that financial asset.

A transfer includes the following:

a. Selling a receivable

A transfer excludes the following:

a. The origination of a receivable

Recourse

The right of a transferee of receivables to receive payment from the

transferor of those receivables for any of the following:

Collateral

Personal or real property in which a security interest has been given.

PROFESSIONAL RESEARCH: FASB CODIFICATION (Continued)

(d) Other examples (besides recourse and collateral) that qualify as

continuing involvement:

05–4 The following are examples of continuing involvement discussed

in this Topic: (Codification String: Broad Transactions > 860

Transfers and Servicing > 10 Overall > 05 Background)

a. Recourse

for sales and secured borrowings. This Topic establishes standards

for resolving those issues.

PROFESSIONAL SIMULATION

Measurement

Trade Accounts Receivable

Allowance for Doubtful Accounts

Beginning balance

$ 40,000

Beginning balance

$ 5,500

Credit sales during 2014

550,000

Charge-offs

(2,300)

Collections during 2014

Change-offs

Factored receivables

Ending balance

$ 7,600

Ending balance

Financial Statements

Current assets

Cash*…………………………………………………………..

$ 12,900

Trade accounts receivable …………………………...

$40,000

Allowance for doubtful accounts ……………….

(7,600)

32,400

Customer receivable (post-dated checks) ……..

Interest receivable** ……………………………………..

Due from factor*** ………………………………………..

Notes receivable ………………………………………….

50,000

Inventory ……………………………………………………..

80,000

Prepaid postage …………………………………………..

Total current assets ………………………………….

$183,012

*($15,000 – $2,000 – $100)

**($50,000 X 11% X 1/2)

***($47,700 X 6%)

Analysis

2013

2014

Current ratio = ($139,500* ÷ $80,000)

= 1.74

($183,012 ÷ $86,000)

= 2.13

PROFESSIONAL SIMULATION (Continued)

Explanation

With a secured borrowing, the receivables would stay on Horn’s books and

IFRS CONCEPTS AND APPLICATION

IFRS7-1

A receivable is considered impaired when a loss event indicates a negative

impact on the estimated future cash flows to be received from the

customer. The IASB requires that the impairment assessment should be

performed as follows.

1. Receivables that are individually significant are considered for impair-

2. Any receivable individually assessed that is not considered impaired

3. Any receivables not individually assessed are collectively assessed

for impairment

IFRS7-2

Both the IASB and the FASB have indicated that they believe that financial

statements would be more transparent and understandable if companies

recorded and reported all financial instruments at fair value. That said, in

IFRS7-3

(a)

Note Amortization Schedule

(Before Impairment)

Date

Cash

Received

(0%)

Interest

Revenue

(10%)

Increase in

Carrying

Amount

Carrying

Amount of

Note

12/31/14

$62,092

12/31/16

Computation of impairment loss:

Carrying amount of investment (12/31/16) $75,131

(a)

December 31, 2016

Bad Debt Expense …………………………..………………..

18,782

Allowance for Doubtful Accounts ………………

18,782

Allowance for Doubtful Accounts ………………………

18,782

Bad Debt Expense …………………………..

18,782

IFRS7-4

(a) IAS 39, paragraphs 18-28 addresses derecognition of financial assets.

(b) According to paragraph 19, “An entity transfers a financial asset if, and

only if, it either:

a. transfers the contractual rights to receive the cash flows of the

(c) The amortised cost of a financial asset or financial liability is the

amount at which the financial asset or financial liability is measured

IFRS7-5

(a) M&S’s cash and cash equivalents include short-term deposits with

banks and other financial institutions, with an initial maturity of three

months or less and credit card payment received within 48 hours.

(b) As of March 31, 2012, M&S had 196.1 million pounds in cash and cash